The Big Picture |

- Daddy’s Home

- Jive Talkin: Rhinofy-Some Bee Gees

- US Corporate Bonds Find More Buyers

- Austerity At Work

- Deep economic collapses are dangerous – Martin Wolf of the FT

- Larry Ellison to Buy Hawaiian Island

- 10 Weekend Reads

- The Federal Reserve Extends Operation Twist

| Posted: 23 Jun 2012 07:03 PM PDT Daddy's Home

Daddy's Home |

| Jive Talkin: Rhinofy-Some Bee Gees Posted: 23 Jun 2012 12:00 PM PDT “Jive Talkin’” Four years is an eternity in popular music. But that’s how long it was since the Bee Gees’ last hit, “How Can You Mend A Broken Heart”. In the interim Jethro Tull released an album containing only one track, FM trounced AM and “Free Bird” became an anthem. But in the sporting goods store I worked in on Hollywood Boulevard, they still broadcast AM, that’s all they had. And I lived to hear this. It was my second sporting goods store gig. The first one was around the corner, on Highland, neither of these establishments exist anymore. And the clientele was always a trip. Talking to Jack Nicholson, H.R. Haldeman coming in for Tretorns. Never mind the delusional street people dropping in for the air conditioning. I never had a soft spot for the Bee Gees. But when “Jive Talkin’” came out, suddenly I did. I guess we like things that connect us to the past that are not pure nostalgia. “Jive Talkin’” may be lumped into the disco camp, but really, it’s not. It’s just a hit record. With a groove and flourishes that make you wince and smile at the same time. The keyboard riff, the percussion breakdown…this is one track I’ve never burned out on, it’s the link between what once was and was yet to be. “Stayin’ Alive” Somehow, in the history of popular music, a taint has been placed upon this track, people dismiss it, look down their noses upon it. That’s what success will do for you. Bring out the haters, the history rewriters. Sometimes something’s so great, you can’t say a negative thing about it, and when it comes to “Stayin’ Alive”, that’s the way it should be. Forget the disco backlash, blowing up records in Comiskey Park, everybody loved “Stayin’ Alive”, not only the polyester-clad dancers but the dyed-in-the-wool rockers. Because it’s so damn good! You’ve got to understand, it snuck up on people. It wasn’t like today, with endless movie hype. A film with John Travolta based on a Nik Cohn story in “New York”, which years later turned out to be completely fabricated…there was no built-in desire. And then you went to see it. Travolta walking down the street with a swagger, putting one slice of pizza atop another, it was movie magic…and it wouldn’t have been half as good without the soundtrack, “Stayin’ Alive”. Movies were platformed, they didn’t open in thousands of theatres, word took months to spread, “Saturday Night Fever” was an immediate hit, but unlike today’s flicks, it played for six months, not six weeks. And the more the movie played, the more people bought the soundtrack, the more these songs were on the radio. The Bee Gees ended up on a victory lap they still haven’t recovered from. That’s the power of a hit song. Especially when matched with a hit movie. And don’t you love those drums at 3:44! “If I Can’t Have You” My favorite non-Bee Gees song on the soundtrack was the Trammps’ “Disco Inferno”… But that was not a movie original, that was another of those disco songs we rockers secretly admitted we loved. But my second favorite was a movie original, by Yvonne Elliman, “If I Can’t Have You”, written, of course, by the Bee Gees, not that many knew this at the time… And this is one of the rare cases wherein the writers’ version is inferior, still, listen, you might not have heard it… And talk about a hook… “If I can’t have you We all know this feeling, it’s the human condition. “Holiday” Despite the cheery title, this song has such a depressing feel. Maybe that’s why it appeals to me. We live in an upbeat world where if you’ve got problems you’re scuttled aside, unless you’re a celebrity and go on “Oprah” and confess. But that’s anything but personal. Depression is personal. As is so much of the greatest music, beamed directly from the speakers into your heart. This was not the first Bee Gees track I heard, but it was the first one that clicked. We had season tickets at Bromley. A ski area with a lot of character that faces south and is right upon the highway which I love with all my heart. And at the end of each ski day, the teenagers would congregate on the main floor, around the corner, where the jukebox was. I’m gonna do a whole playlist on the tracks that emanated from that machine, that changed my life, that I had to buy. Stuff you wouldn’t expect, like “Boogaloo Down Broadway”, by the Fantastic Johnny C…and this. You see that’s what’s great about a jukebox, about the AM radio of yore…you don’t get to hear what you want to, but what others want to. And then you end up hearing these songs enough they become your favorites too. I can still see the townies, with their Moriarty hats pushed up high. The tension between the locals and the weekenders, the way we connected as the winter months wore on, drinking our hot chocolate and eating our monster glaze donuts. That’s what’s great about life, the memories. When you’re depressed, you think back and you smile. “New York Mining Disaster 1941″ This was the first Bee Gees song I heard. But since it was not on the Bromley jukebox, I did not know it as well. What I love is the endless repetition of “Mr. Jones”…you think he really exists. “Massachusetts” I was always flummoxed by this. How a band from the U.K. via Australia could pick out such a tiny state and write a song about it. Massachusetts was just the next state over. The one we drove through to get to Vermont, the one that contained my grandparents. You know how you feel a special connection with a song that mentions your name? That’s how I feel about this song. Especially in the sixties, all the glamour, all the references, were based on California, the west coast. Sure, most of the people lived on the east coast, but popular culture seemed to be based out west, but not in this song. “Lonely Days” And I love all the aforementioned records. “Massachusetts” was the follow-up to “Holiday”, they were on a roll. But then came “Words”, “I’ve Gotta Get A Message To You” and the execrable “I Started A Joke”. Who was this music made for? Sure, I could get depressed, but this music seemed to be made for hobbits who never left the house, who never saw the sun shine, people who were perpetually under the weather. You made fun of these songs. And if you say otherwise, you weren’t there. But then there was a last hurrah. Just when I’d written them off, the Bee Gees released my favorite song, “Lonely Days”… The track started off like another dirge, and then… “Good morning mister sunshine, you brighten up my day The harmonies were exquisite, they made you feel all warm inside, the strings swirled underneath… And then there was the rhyme of “restaurant” and “nonchalant”… And then the song changed completely, it became a rocker… Someone started banging on the piano, like you would at home, only with more talent, there were random horns, you felt like you were at a football game and wanted to get out on the field and march with the band. Then the track devolved into dreaminess, something the Beatles were so good at, but the Bee Gees did well too. The track went back to the quiet verse… But when the chorus came back this time, it was truly vociferous. LONELY DAYS The brass is squeezing out the notes, the boys are shouting and harmonizing, the strings are swirling…it’s a tour de force. And I’ll bet what Barry Gibb is feeling right now is lonely. With three of his four brothers deceased. You don’t want to survive, you want to go first, otherwise it’s just too painful. You’ve got no one to share your memories with, no one to sing with… But we the listeners are not burdened by the death of three of the brothers Gibb. For us, the songs still live. This was an act that hung in there, kept trying, for decades, experimenting, getting it right. Their only mistake was to become so successful that the public put them in a box and they became inhibited by their own legacy. Spotify playlist: http://spoti.fi/p6HcZ8 Previous Rhinofy playlists: http://www.rhinofy.com/lefsetz |

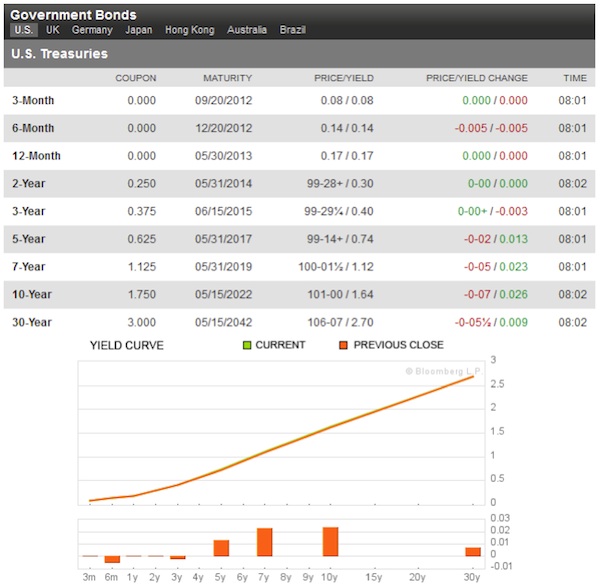

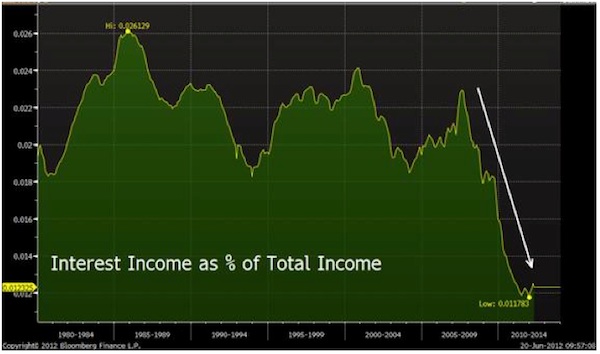

| US Corporate Bonds Find More Buyers Posted: 23 Jun 2012 12:00 PM PDT

Source: |

| Posted: 23 Jun 2012 08:00 AM PDT Covering the waterfront of some recent economic and political matters, herewith some thoughts as you prepare to enjoy your summer’s first Bloody Mary: I’ve still not seen a supply side response to this wonderful piece by Mark Dow. If anyone has, please drop a link in comments. President Obama was excoriated recently for his clearly inappropriate comment that “the private sector is fine.” Of course, the private sector is not fine, nor will it be until we’re consistently printing ~200K/month or more nonfarm jobs. To be fair, though, the comment for which Obama was ridiculed was taken a bit out of context. In context, it was really a comparison of the private sector to the public sector:

On that score, he is exactly right. Let’s take a look, shall we, at what the president is referring to.

What we’ve got above is State (green) and Local (black) jobs, indexed to 100 at January 2001 and January 2009 – the inaugural months of our past two presidents. Also, for the record – and I’ve written about this before – are private sector jobs (gold), which have grown better in this recovery than in the previous one. Let’s attach some numbers to the chart beyond the percentage change up or down from 100.

(Source: St. Louis Fed, author calculations. Thousands of persons.) So, where Bush had picked up 800,000 State and Local jobs in the first 41 months of his term, Obama has presided over a loss of 636,000. (On a Federal level – which is by far the smallest of the three public sectors – Obama has added a whopping 34,000 jobs, whereas at this point in his first term Bush had shed 21,000.) These lost jobs are our teachers, firefighters, police and other civil servants. This is what austerity looks like. (Mind you, I don’t recall seeing anyone lambasting Bush for public sector job growth on his watch.) Obama has simply not presided over a massive expansion of government, in terms of either spending or hiring. Arthur Laffer and Stephen Moore wrote an op-ed in the WSJ titled Obama’s Real Spending Record. In it, they used the following chart to demonstrate what a big spender Obama is. Seriously, they did. The beauty of it was the mental gymnastics they went through to convince their readership to ignore the actual decline in spending we’ve seen for the past 2+ years. See that (very inconvenient) red line moving down and to the right? And they used that chart anyway. Mind bending – I actually could have used their chart in my May piece demonstrating Obama’s relative frugality. To their credit, though, they do get one thing right: “Sadly for fiscal conservatives, the biggest surge in government spending came during the last two years of President George W. Bush’s eight years in office (2007-2008).” As an aside, since they were kind enough to run the chart starting in 1990, can we discuss for a moment who presided over a decline in Federal government expenditures as a percent of GDP and left his successor with a pretty damn good looking balance sheet? To my untrained eye, it appears as though spending really only declines under Democratic administrations.

Moving on, Census recently released an interesting report titled Sharing a Household: Household Composition and Economic Well-Being: 2007–2010 [PDF], which examines the incidence of “doubling up” from 2007 – 2010. The results are, on the one hand, distressing, but on the other hand offer a glimmer of hope for the housing market and, by extension, economy overall. The statistics about the growth of doubling up are indeed troubling. However, we should consider that (hopefully) at some point these individuals will find their way into their own residence. For example: “The number of adults aged 25 to 34 who lived in someone else's household increased by 18.1 percent, while the number aged 35 to 64 increased by 9.7 percent between 2007 and 2010. The 1.5 million increase in the number of additional adults aged 25 to 34 accounted for about 45 percent of the total increase in additional adults during the period.” At some point, should this economy ever truly gain some traction and hit escape velocity, I’ve got to believe these interlopers are going to head for the exits of the homes in which they’re now doubled up, and that could be a decent tailwind for an improving housing market. On Bernanke watch, the Fed’s “central tendency” forecast for the unemployment rate in 2014, released on Wednesday after the FOMC decision, showed them ratcheting up from a range of 6.7 – 7.4 percent to 7.0 – 7.7 percent. The Fed has consistently issued rosy forecast after rosy forecast, only to have to downgrade them at a later date. Given the repeated downgrades, it is shameful that they are not doing more. And at this point, as we draw ever nearer to the election, any further action will draw shrill cries of an attempt to help Obama’s reelection chances. So as not to heap all the blame on Bernanke, I’ve rarely – if ever – seen a more useless group of people than our Congress. Though I don’t think Bernanke’s done enough, he looks downright heroic compared to our do-nothing Congress, which has done exactly zero. And that is simply unforgivable. The Fed’s toolbox is limited to whatever monetary tricks Bernanke can pull out of it. Congress could, if anyone ever found a spine, complement Bernanke’s actions with some growth-promoting legislation. And Mila Kunis is going to fall madly in love with me. @TBPInvictus Adding: I’m fascinated that everyone seems to want to jump on the Laffer/Moore graph and my comments about it. That part of the post was almost an afterthought. I’m surprised – though I guess I shouldn’t be – that no one seems to want to tackle the meat of the issue here which is, of course, the first chart of State/Local employment vs. private sector. Then again, what is there to say? |

| Deep economic collapses are dangerous – Martin Wolf of the FT Posted: 23 Jun 2012 06:00 AM PDT Bloomberg reports that officials are in the process of drawing up plans which would result in shareholders and junior bondholders in Spanish banks facing losses, prior to any bail out. Not before time. At least the EU is finally (partially) getting it, though senior bond holders look as if they will be made whole – why?. There are certain issues, I accept, but senior bondholders were not investing in guaranteed bonds; Spain is expected to make a formal request to the EU for funds to bail out its banks on Monday. The IMF (indeed in non diplomatic language), supported by many in the EZ, want the funds injected directly into the banks, rather than through the FROB, (Spain’s bank restructuring agency) as it will not increase Spanish debt to GDP – to approximately 90% by end 2012. Furthermore, EZ finance ministers failed to agree whether the E100bn of loans would rank senior to existing privately held debt, a key issue. Germany has refused to concede, though there are (some?) signs that Mrs Merkel will do so at the heads of state meeting on 28/29th June, in return for EZ countries agreeing to measures to enforce strict fiscal discipline. Interestingly, Spanish 10 year yields fell 97bps from the previous weeks highs to close at 6.34% on Friday; Portugal’s budget deficit rose by 35% in the 1st 5 months of the year, to E2.72bn (E2.02bn previously). Revenues declined by -2.3% to E14.82bn, whilst spending rose to E17.54bn. The data casts doubt on Portugal’s ability to reach their targeted budget deficit of 4.5% this year, especially as May’s revenues came in significantly below expectations and the decline in revenues continues into June. Last years budget deficit was achieved by a one-off transfer of bank pension funds. In spite of repeated denials, Portugal will need another bail out in the next couple of months. Having said that Portuguese 10 year bond yields declined by around 100bps last week; EU finance ministers failed to agree an EU wide financial tax. Some countries, including proponents of the tax such as Germany, Austria and France will attempt to reach agreement with at least 9 EU countries to introduce such a tax, essentially some form of stamp duty, though set at less than the 0.5% currently applicable in the UK. The EU reports than 11 (out of 27) EU countries would support such a tax; Germany (Mrs Merkel) agreed to a E130bn plan to stimulate growth, which has been pressed by Italy, France and Spain – no significant development. Her opposition parties supported the move. No other material agreements were achieved at the meeting in Rome yesterday, which by all accounts pitted the 3 leaders of France, Italy and Spain against Mrs Merkel; A recent poll (Infratest survey for ARD public TV) suggests that 55% of Germans want the Deutschmark back, up 9% on the previous month. This is getting serious, but the real problem is that German politicians have not explained the consequences of such a move (the DM would become a supercharged Swissy) to their public. 62% of Germans supported Mrs Merkel’s insistence on imposing austerity measures. Support for Greece was ebbing fast. (Source FT); Questions are being raised as to whether the ESM can raise the full amount of E500bn. Portugal, Ireland, Spain and Greece (and Cyprus soon) are due to contribute just above 19% of the E500bn, which must be considered uncertain. If Italy faces a problem, another 18% would disappear. It does not look as if the EZ leaders will agree to granting the ESM a banking licence at the 28/29th meeting, in part due to the recent German Constitutional court issues. However, as the size will prove insufficient, it is a near certainty that the ESM will have to be granted a banking licence in due course. Martin Wolf of the FT responds to a letter from a senior official in the German finance Ministry, Mr Ludger Schknecht, who replied to an op ed written by Mr Wolf. You really should read it. However, I will just focus on one point, namely that the rise of Adolf Hitler in Germany was not due to high inflation in Germany – indeed, it was due to the depression/deflationary environment, following the austerity programme introduced by Mr Heinrich Brunning. This issue is widely misunderstood in Germany – time to suggest that its critical to “do your homework?” do you think. Mr Wolf concludes that “Deep economic collapses are dangerous”. Absolutely right. There are mounting (extremist) political challenges in the EZ – in France, Greece, Holland, etc, etc. Time to understand the issues Mr Schknecht; US 30 year mortgage rates hit a record low of 3.66%, down from 4.5% the same time last year. A number of mortgage holders will refi given the much lower rates, increasing disposable income. The FHFA house price index rose by +0.8% in April MoM and +3.0% YoY; Goldman’s suggest that the FED will have to push forward guidance for its 1st rate increase further into the future and, in addition, do another QE programme, as unemployment remains a problem and inflation declines. Sounds right to me; Brazil’s Petrobras has been granted permission to raise petrol prices for the 1st time in 9 years. Petrobras should be amongst the best performing energy companies worldwide, though government policy (actually massive interference) has neutered the business. Is this the beginning of a change – well, history suggests that investors should remain cautious for a while at least; Really on hold and awaiting developments arising from the EU heads of state meeting. At present, it looks pretty bleak, I must admit. A failure will be disastrous for markets. Need to watch this one carefully. I will be trying to read the tea leaves next week. Have a great weekend. Kiron Sarkar 23rd June 2012 |

| Larry Ellison to Buy Hawaiian Island Posted: 23 Jun 2012 05:00 AM PDT Larry Ellison, the billionaire CEO of Oracle, has struck a deal to buy the bulk of the Hawaiian island of Lanai. Ben Worthen reports on digits. |

| Posted: 23 Jun 2012 03:30 AM PDT Some longer form reads for your weekend pleasure:

What are you mulling over this weekend?

2012 Forecasted Debt to GDP Ratio |

| The Federal Reserve Extends Operation Twist Posted: 23 Jun 2012 03:00 AM PDT The Wall Street Journal – Fed Extends Operation Twist Bloomberg.com – Caroline Baum: The Fed Is Running Out of Room to Twist The Financial Times – Mohamed El-Erian: The Fed's second best solution Comment Yesterday we argued that the Federal Reserve would not extend Operation Twist because the $175 billion in 0- to 3-year securities on their balance sheet was not enough to implement a meaningful operation. Despite this, Bernanke extended Operation Twist through the end of 2012 for an additional $267 billion. So, how can the Federal Reserve sell $267 billion of 0 to 3 year securities when they only own $175 billion? It depends on how you define "three-year securities." What Is A Three-Year Security? We defined 0- to 3-year securities as all securities maturing before June 30, 2015. Using this definition, the Federal Reserve was expected to have $175 billion of securities between 3 months and 3 years on June 30. Since the Federal Reserve extended Twist until December 2012, they must be defining a "three-year note" as any security that has a maturity of three years or less as of December 31, 2012 . Under this definition, the Federal Reserve would have about $295 billion of Treasuries less $30 billion of securities that mature before December 30, 2012. Net them together and the Federal Reserve would have $265 billion of securities they can sell before December 31. This is a rounding error difference from the Federal Reserve's $267 billion estimate. This also means when Operation Twist is done, the Federal Reserve will have no Treasuries that mature before 2016. Will The Market Have A Plumbing Problem? When Operation Twist is over and the Federal Reserve owns no securities that mature in less than three years, the market could have a plumbing problem. The next story explains it well. Liquidity Problems Likely in Twist Extension: Cloherty June 21 (Bloomberg) — Fed is likely to have to "adjust the mix of its purchases well before the end of the year, possibly by adding MBS to the purchase mix," RBC strategist Michael Cloherty said in an emailed response to questions. * Recent offer-to-cover ratios in 8-to-10-yr and 10-to-20-yr purchase operations have been low Source: Bianco Research |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment