The Big Picture |

- Nonlinear Thinking: Wireless Doctors

- Weekly Eurozone Watch: November 30, 2012

- David Angelo Explains Gas Prices & Taxes

- Succinct summation of week’s events (11.30.12)

- Ghost Exchange: The Movie

- Rolling Stones 50th Anniversary Tour Set List

- German Bundestag Approves Greek “Deal”

- Real Median Household Income in the 21st Century

- 10 Friday AM Reads

- “If you give a mouse a cookie…”

- Idiosyncratic vs. Systemic: California Cities, A Case Study

- Seinfeld Reunion on Curb Your Enthusiasm

| Nonlinear Thinking: Wireless Doctors Posted: 30 Nov 2012 10:30 PM PST The wireless revolution in the delivery of health care services is coming, folks. We've been all over this story. Click here, here, and here. Scanadu is a new company with a mission to give consumers affordable medical care alternatives and to take more control of their own health. The company is about to unveil three new products: 1) the Scout is a device that you hold up to touch the electrodes to your temple to take vital signs and sends the data to a smartphone; 2) ScanaFlo acts as a urine analysis reader; and 3) ScanaFlu is a low-cost disposable cartridge that can test for cold and flu symptoms though testing a person's saliva. Here's Forbes on Scanadu,

(click here if picture and video are not observable) Incredible stuff. Beam me up, Scotty! |

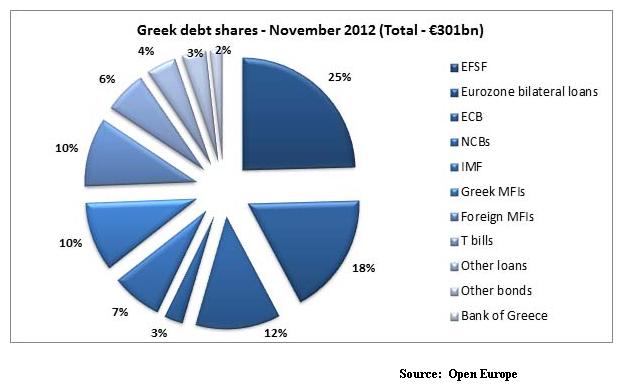

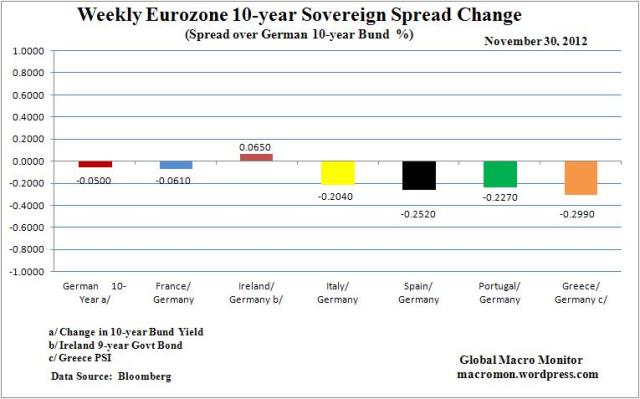

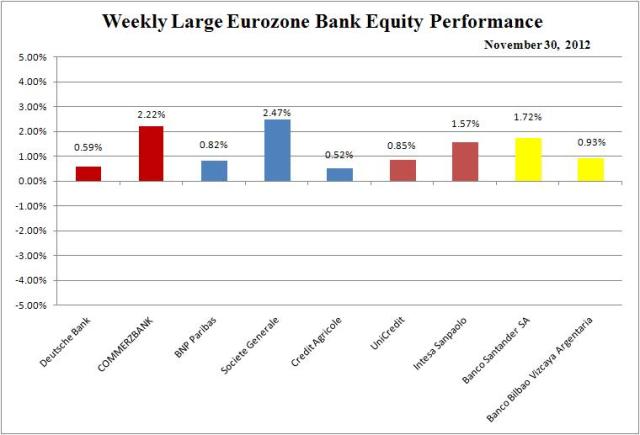

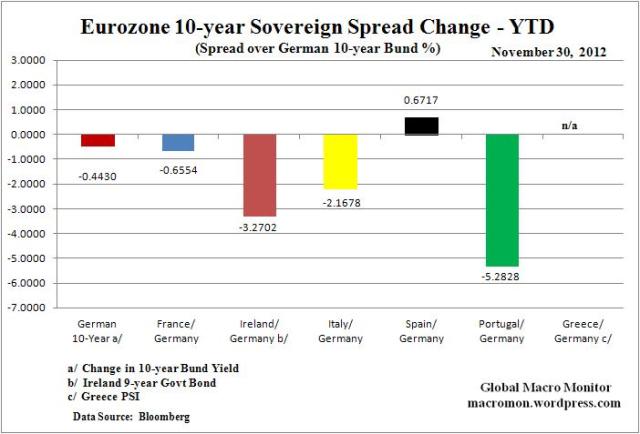

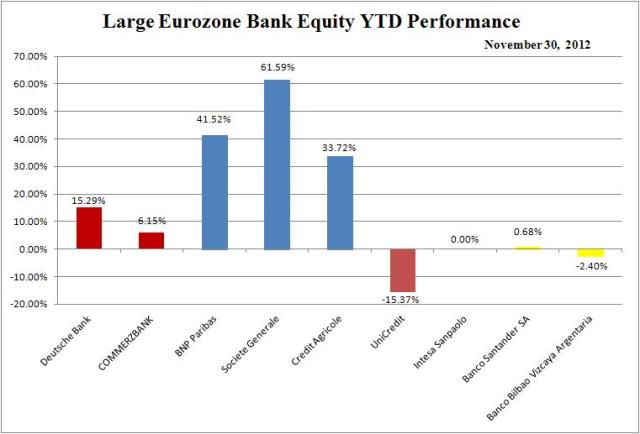

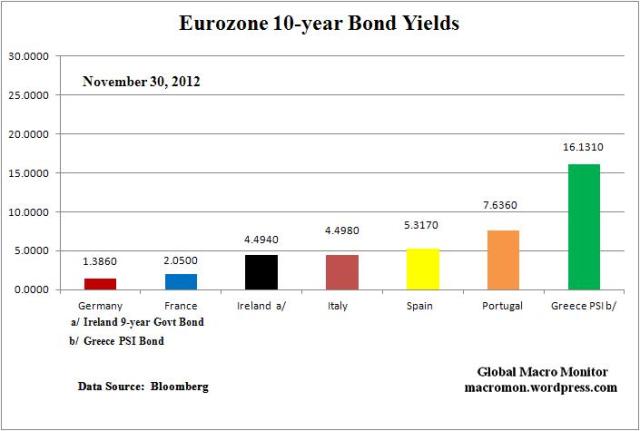

| Weekly Eurozone Watch: November 30, 2012 Posted: 30 Nov 2012 02:30 PM PST Key Data Points1 Comments

(click here if charts are not observable) |

| David Angelo Explains Gas Prices & Taxes Posted: 30 Nov 2012 12:45 PM PST David Angelo explains rising gas prices with Deadpan Hilarity: Gas Prices ~~~ Gas Taxes Hat tip Economic Thought |

| Succinct summation of week’s events (11.30.12) Posted: 30 Nov 2012 12:30 PM PST Succinct summation of week’s events: Positives

Negatives

|

| Posted: 30 Nov 2012 11:00 AM PST |

| Rolling Stones 50th Anniversary Tour Set List Posted: 30 Nov 2012 10:00 AM PST Here are the songs the Stones are performing this tour:

Sources: Stones, Rolling Stone

The Rolling Stones 50th Anniversary Tour Tickets Out-Price Them All |

| German Bundestag Approves Greek “Deal” Posted: 30 Nov 2012 09:30 AM PST Japanese consumer prices, excluding fresh food, were unchanged in October Y/Y, somewhat higher than the decline of -0.1% in September. The Japanese government has approved a 2nd round of stimulus in just over 1 month amounting to Y880bn (US$10.6bn), including capex programmes, employment measures and aid to small businesses. Industrial output rose unexpectedly by +1.8% in October M/M, much better than the -2.0% expected and -4.1% in September – mainly due to Apple related products. I continue to believe that the Yen will weaken further into and after the elections, assuming the LDP party comes in as the largest party with Mr Abe as PM. At present, the LDP is leading in the polls with 23% support, followed by its likely partner, the Japan Restoration Party (15%), with the current PM’s party (the DPJ) lagging at 13%. Mr Abe beat the nationalist drum today, which in due course is going to add to the friction with China, in particular.The Yen continues to weaken. Please note, I remain short the Yen; Indian GDP declined to +5.3%, in Q3, down from +5.5% in Q2, though in line with estimates – matching a 3 year low. Previous growth levels have been around 8.0%. The government has announced a number of economic reforms, with a (no-binding) Parliamentary vote on the politically sensitive plan to allow foreign investors to take a majority stake in multi-brand retail operations due shortly. Structural reforms are much needed, though opposition by vested interests, combined with bureaucratic delays and corruption have stifled the Indian economy – however, some changes are expected, which clearly are much needed. Having said that the Indian markets continue to rise, in anticipation of structural reforms The Indian Central Bank, the RBI meets on the 18th December, though is unlikely to cut rates. However, a rate cut in Q1 next year is pretty likely; Italian provisional seasonally adjusted October unemployment came in at 11.1% M/M, higher than expectations of 10.9%, and 10.8% previously. There were hopes that Italy was stabilising, but recent data has been weaker than expected; German October retail sales declined -2.8% M/M, much worse than the -0.4% expected and the downwardly revised +0.5% in September. Y/Y, October retail sales declined by -0.8%, much worse than the -0.3% expected. Construction and consumption was supposed to keep the German economy ticking over – I don’t think so; As expected, the Bundestag approved the “deal” on Greece by 473, out of 584 Bundesatag members who voted. However, Mrs Merkel failed to secure an absolute majority from her own coalition, having to rely on the opposition to secure the approval. The opposition parties, however, accused Ms Merkel of not telling the German public the truth. Importantly, dissent amongst Mrs Merkels coalition is not increasing; French October consumer spending came in -0.2% M/M, in line with expectations and a downwardly revised unchanged reading in September. Y/Y, consumer spending is -0.5% lower, bad news as the French economy is relatively dependent on consumption; EZ estimated inflation declined to +2.2% in November, from +2.5% in October and lower than the +2.4% expected. It was the lowest reading since December 2010. Inflation should decline further. The ECB is likely to cut interest rates, the question is this year or 1st Q 2013 – I would go for next 1st Q 2013; UK November consumer confidence in the UK, whilst negative at -22, was much better than the -30 expected and an 18 month high. UK economic data is all over the place, though I believe that the UK economy is performing better than believed; The UK BoE has warned UK banks that they need to raise between £20bn and £50bn in equity to strengthen their balance sheets, as they have not written off enough in respect of their “assets” and had not made sufficient provisions for the recent scandals eg LIBOR . Well, no great surprise, as a number of European banks have exaggerated asset values; US consumer spending declined by -0.2% in October, lower than the +0.8% in September and the unchanged expected, the 1st decline since May. Personal income was unchanged in October, lower than the +0.4% gain in September and +0.2% expected. The savings rate rose to +3.4% from +3.3% in September; The numbers were affected by Hurricane Sandy; US October PCE deflator came in at +0.1% M/M, in line with expectations and +0.3% in September. Core PCE came in at +0.1% M/M, lower than the +0.2% expected and +0.1% in September; Chicago November PMI came in at 50.4, as opposed to 50.5 expected and 49.9 in October. Whilst it was the 1st above 50 reading, new orders declined materially (to the lowest since June 2009), and prices paid surged (to the highest since March). However, the employment component was better; Brazilian GDP rose by just +0.6% in Q3 Q/Q, about half the rate expected. Y/Y GDP rose by just +0.9%, well below the +1.9% expected. A very definite Oops, given the recent rhetoric by the finance minister; Outlook Asian markets closed higher, including China. European markets are marginally higher, with US markets flat to lower. The Euro has bounced back up to US$1.3009 against the US$ (will still wait before I short), with the Yen at 82.52 against the US$. Gold is off, currently trading at US$1712, with January Brent at US$110.62 – still remain bemused at the strength of Brent. Usual politicking in the US re the fiscal cliff, though most (including myself) expect a deal to be done, though quite possibly just after 31st December 2012. Markets are taking a pause – still feel that there will be time to buy the markets in due course. Have a great weekend. Source: |

| Real Median Household Income in the 21st Century Posted: 30 Nov 2012 09:00 AM PST

Source: Advisor Perspectives

Courtesy of Doug Short, we see from the above that the past decade has seen no gains in real median household incomes. Indeed, the free fall began in earnest in 2008, and now reflects an 8.1% decrease in real buying power. This is for the median household — we know from Fed and IRS data that the past decade has seen a modest gains in the top 30% of all earners, bigger gains in the top 10%, very significant increases in the top 1.0%, and enormous gains in the top 0.1%. If you combine the real median income chart above with knowledge of an how US income distribution is skewed, you get a much into starker context for median income changes. It implies that the bottom 70% has done far worse than the minus 8% of this chart. |

| Posted: 30 Nov 2012 06:40 AM PST My morning reads:

What are you reading?

Investors Warm to Spanish, Italian Debt |

| “If you give a mouse a cookie…” Posted: 30 Nov 2012 06:16 AM PST “If you give a mouse a cookie, he’s going to ask for a glass of milk. When you give him the milk, he’ll probably ask you for a straw. When he’s finished, he’ll ask for a nampkin…” This children’s book which I read to my son about hundred times years back now reminds me of the new Tim Geithner fiscal plan which we got a whiff of a few weeks ago. Republicans finally decide to give in on about $800b in tax increases and the Obama administration says they want $1.6T of taxes with spending cuts to be determined later. Any economic credibility that Geithner professed to have is out the window. The US economy is growing no more than 2% and his plan is to take 1% of GDP right out of the private sector per year. While this could be just awful DC negotiating, the optics now look like a giant money grab where the income of the top 2% is just a cookie jar for others to stick their hands in to eat as many as they want. |

| Idiosyncratic vs. Systemic: California Cities, A Case Study Posted: 30 Nov 2012 05:30 AM PST Idiosyncratic vs. Systemic:

~~~

We thank readers and media friends for the quotes originating at the Bloomberg State and Municipal Finance Conference held on October 3, 2012, in New York. We also thank Bloomberg’s Kathleen Hayes, our panel moderator, who gave me a few minutes to make the distinction between idiosyncratic and systemic issues. In our presentation, we discussed several California cities. The first mentioned was Vallejo, California, a city of 116,000 at the north end of the Bay Area. (You can take a ferry ride from San Francisco to get there.) Vallejo enlarged its municipal budget by giving raises to its municipal workers and subsequently ran out of money. Hat in hand, it went to the State of California looking for a bailout. California said it did not have any money, either, and would not be providing assistance. Vallejo provoked a fight. It sought Chapter 9 bankruptcy protection under California law. The first result was the squandering of ten million dollars in legal fees and costs. Vallejo was able to break and redo the labor contracts with its municipal workers who had achieved huge raises. But by 2011, salaries and benefits were 80% of the general fund budget. The potholes in Vallejo were not fixed. The old political regime was kicked out, and the new political regime has inherited a mess. The second result for Vallejo was that the bondholders did not get “stiffed.” But the city tried to get them. Senior bondholders were repaid in full. The COP holders recovered only 65 percent of principal. COP means Certificate of Participation and is a weaker credit claim. Fast-forward to the important question. Is this an idiosyncratic event, or is it the first in a string of systemic events? That question was discussed at the Bloomberg conference. At the time of Vallejo it was viewed as idiosyncratic. This seemed to be a “one-off” event. What do we do when we want to find the signs of “morphing” from idiosyncratic to systemic? The earlier an investor, professional, or analyst can see the signs, the faster they can move to protect their portfolios, strategies, and implementation options. In California, Vallejo has been followed by Mammoth Lakes, Stockton, San Bernardino, and Atwater. At the bottom of this commentary, my colleague Michael Comes, Vice President of Research at Cumberland Advisors, will provide a summary of each of these credits. For us, as a Muni sector manager, the question is, how do we see the transition? Where do we determine whether there is more than one cockroach in the nest? Now, we know there is an infestation of cockroaches in California, and we find them turning up in its cities. In the argument we summarized at the Bloomberg conference, we made the case that cities in California have a systemic problem. This is not a “one-off.” It is not idiosyncratic. The systemic issue is now statewide and is a heavy load for the state of California. It piles onto other problems in California. These include underfunded pension systems, inadequately funded post-retirement health-care benefits, and high taxation (which is driving marginal taxpayers out of the state to other jurisdictions). At Cumberland, we are worried about some aspects of California debt. We are on the side of selling or under-weighting California debt and restricting and limiting our California credit exposure. There are two reasons. The first is headline risk. The second is default risk. There is headline risk that hurts the credit, injures the state’s debt-trading characteristic, and causes the pricing of bonds to be weak in a relative sense. That does not mean California will or will not default. It does mean that if you have to sell your bond into a weak market, you have no choice but to accept a price that is lower than you would otherwise get if the markets were clearing without adverse news flow to hurt them. Headline risk is important: it is necessary to review it, discuss it, and price it because it can affect the contingent sale of a bond. When you have to sell a bond because you need the money, you have to go into the market at the time of the sale, regardless of the efficiency or inefficiency of the pricing. Headline risk means a sale under duress will get a poor price. The other side of this question is default risk. So far, California courts have upheld the rights of the bondholders to get paid. These courts have rejected each of the arguments to place the claims of the specific city ahead of the claims of the bondholder. The bondholders have been paid in Vallejo (except for COPs), San Bernardino, Atwater, Mammoth Lakes, and Stockton. In his summary, Michael Comes will have a quick comment about the credits of these cities and the status of those bonds. We know something else about the California cities. The rating agencies are now out with extensive municipal questionnaires. Cumberland Advisors consults for some municipalities, and we have seen these questionnaires. Our expectation is that the cities in California are under scrutiny by rating agencies. The likely outcome will be warnings about credit deterioration or downgrades (see Moody's news above). We see little likelihood of credit upgrades. In other words, the credit picture of the troubled California city is asymmetrical. It is more likely to go down than up. It is more likely to deteriorate than improve. The pressures in California have not been resolved. Below you will find the city-by-city summary. We thank Michael Comes for preparing it. We thank readers and participants at the Bloomberg conference for their emails and comments. At Cumberland, we look at California as a troubled state. We look at the cities within California as troubled municipal credits. Cumberland Advisors does not hold positions in those troubled California cities. You can own plenty of bonds in California that are amply protected with senior claims on revenues and structure. A bond investor does not have to gamble on a deteriorating credit in California. Michael Comes’ research notes follow. ATWATER, CA. A typical agricultural community located in the central San Joaquin Valley with a population of 28,000, Atwater declared fiscal emergency on Wednesday as a result of financial uncertainty built up during the past three years. The city has roughly $82 million in debt outstanding across government and business-type activities, all of which the city is on the hook for. Declining property taxes from lower home values, a new wastewater treatment plant, and lack of willingness to reduce personnel costs have created structural imbalances in the city’s budget that have significantly reduced municipal cash balances and ability to remain solvent. As a result, the city has been forced to increase debt issuance to fund deficits, transfer restricted funds from its water and sewer entities to pay debt service in the general fund, and increase rates on city-provided services to levels substantially higher than those of surrounding communities. The city’s ability to pay debt service has been reduced to barely sum-sufficient levels. We view declaration of fiscal emergency as the inevitable path toward any sort of restructuring because of the city’s lack of leadership in controlling its finances and protecting bondholders. Fortunately for bondholders, the declaration will allow the city to lay off personnel, restructure labor contracts, and reduce benefits without negotiations. VALLEJO, CA. Four years before Atwater, the city of Vallejo filed a Chapter 9 petition on $53 million of general-obligation debt before the start of FY08-09, when it otherwise would have been insolvent. Vallejo is extremely important in our analysis, because it set the precedent. Before Vallejo, the need for Chapter 9 relief usually arose from a one-time, idiosyncratic catastrophe, most of the time against a small city (think Mammoth Lakes). Rarely was there a large entity filing as a result of something like a legal judgment (Orange County). Vallejo was the first major city to file for bankruptcy because it had become structurally insolvent due to systematic factors such as the combined impacts of the housing, economic, and banking crises. The city’s structural insolvency came as a result of its unsustainable expenses and stalled revenues as it ate through all its reserves, and its budget could not be balanced without relief. Vallejo’s experience highlights positive and negative aspects of a bankruptcy. On the positive side, Vallejo was able to restructure labor and debt contracts deemed otherwise unsustainable, to the tune of over $100 million. On the other hand, the bankruptcy was very expensive, costing over $10 million – largely because of its long length and the litigation of new issues. MAMMOTH LAKES, CA. On Monday July 2 the city declared bankruptcy to seek legal protection against having to pay a legal judgment equal to 2.1 times its annual operating budget. This city of 8200 residents, located 300 miles north of Los Angeles, has $2.678 million in Certificates of Participation (debt with interest backed by lease payments) outstanding, issued for capital projects in 2000. In 1997, the town entered a development agreement that required real estate developer Terrance Ballas to construct retail and residential buildings near the Mammoth Yosemite Airport. In return, Ballas would receive rights to develop a $400 million hotel project on 25 acres of airport land and an option to buy the land. The town backed out of the deal because it wanted to use the land to extend the airport’s runway to allow larger jets to land. In 2006, the developer, through its closely held company, Mammoth Lakes Land Acquisition, sued the town for breach of contract and was awarded a $30 million judgment against the town. The judgment accrued interest at 7% and grew to $43 million, up until August of this year, when the city settled out of court with the developer. The town’s bankruptcy plan does not allow restructuring lease payments on its $2.678mm in outstanding debt, which amount to 1.2% of its general-fund expenditures. It is unclear how the bankruptcy filling will affect future debt-service payments; however the bonds continue to be paid in full. SAN BERNARDINO, CA. The commonly held belief about Chapter 9 is that it is a remedy of last resort for cities that, after attempting to do so in good faith, cannot repay or renegotiate their debts as they come due. San Bernardino’s use of Chapter 9 is an exception to this rule. Over the course of the last decade, personnel expenses for public safety increased 350%. Reserves in the general fund were depleted years ago, and the city encumbered itself with debt-service obligations and labor agreements that put large risks on the general fund. The city reached a breaking point in June of this year when the city council came to the realization that the resources on hand were insufficient to make August debt service and other contractual obligations – this after a decade of fiscal mismanagement and structural budget imbalances. California law AB506 allows debtors to bypass private 30-day negotiations with creditors if it is determined the city will be insolvent before the 30 days have elapsed. To remedy that issue, it was more convenient for the city to declare, eventually allowing it to pass an emergency budget (after a month of wrangling) that included no general-fund payments toward its $50 million POBs (pension obligation bonds), out of a total $233 million in outstanding debt. STOCKTON, CA. On June 28th of this year, about sixty miles northwest of Atwater, Stockton became the first – and by far the largest – California city to seek relief under bankruptcy, after failed AB506 negotiations with its creditors. The negotiations failed to achieve a negotiated settlement that would allow the city to adopt a balanced budget for FY12-13, as required by law. A pendency plan submitted by the city during the AB506 process – essentially a budget for the city under Chapter 9 protection – did not include payments for debt service on $350 million out of $702 million of debt, and also reduced costs for labor, retirees, and long-term healthcare obligations. As in the other bankrupt inland cities in the state of California, the bankruptcy code is being used as a last resort, enabling Stockton to continue general-fund operations while giving the city time to negotiate settlements with creditors, thus providing long-term stability. In this time of uncertainty, bankruptcy has looked increasingly attractive. Revenue increases, except in certain instances, require voter approval; and specific taxes (e.g., a tax on a certain good) require a 2/3 vote by town residents. A “typical” tax-plan increase such as a sales or utility tax hike could erase deficits and maintain debt-service coverage levels. But will electorates support new taxes, given the risks to municipalities of litigation and escalating costs? Probably not, until the city council can regain the trust of its citizens. We use as an example the city of Vallejo, which, once it got its fiscal affairs in order and regained the trust of its citizens, saw its citizens approve a tax increase. Now, the city is a model of austerity in the deleveraging world in which we find ourselves. At a minimum, a restructuring of contracts relating to labor, retirees, debt, etc. is required to regain fiscal sustainability. Unfortunately, given the failures we’ve seen with AB506, bankruptcy is looking like the only way to attain this. The long-term budget forecasts we’ve seen show the problems facing these California municipalities are so severe that aggressive tax hikes or cutting services are not enough to make them viable. Revenues and expenditures are only one source of the problem: debt and contractual liabilities, which can only be addressed through AB506 or Chapter 9 bankruptcy, must be restructured. Source: Cumberland Advisors |

| Seinfeld Reunion on Curb Your Enthusiasm Posted: 30 Nov 2012 05:00 AM PST Some Friday humor to end your week: This video is only a small piece of Curb Your Enthusiasm’s seventh season. (Note: the Curb Your Enthusiasm footage has been edited out to better present the reunion’s storyline and plot). There are some instances in which editing out Larry’s shiny head and the Curb characters would have subtracted significant dialogue or plot points, so they were left in. As for Larry’s hilarious but pathetic attempt to play George Constanza, it has been completely omitted to spare unsuspecting Seinfeld fans the horror, shock and pain of the unfortunate footage.

|

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment