The Big Picture |

- Weekly Eurozone Watch 12.21.12

- Somebody That I Used to Know

- ‘Tis four days before Christmas

- Succinct Summation of Week’s Events (12/21/2012)

- What going over the ‘fiscal cliff’ means . . .

- Quote of the Day: On Pledges

- Durable goods orders surprise to upside / Income

- 10 Friday AM Reads

- Mandelbrot: Fractals, Chaos and Other Mathematical Visions

- Boehner’s Plan B fails

- ACME Corporation: 126 Coyote Endorsed Products

- The Sequestration Vote Is Nothing Like the TARP Vote

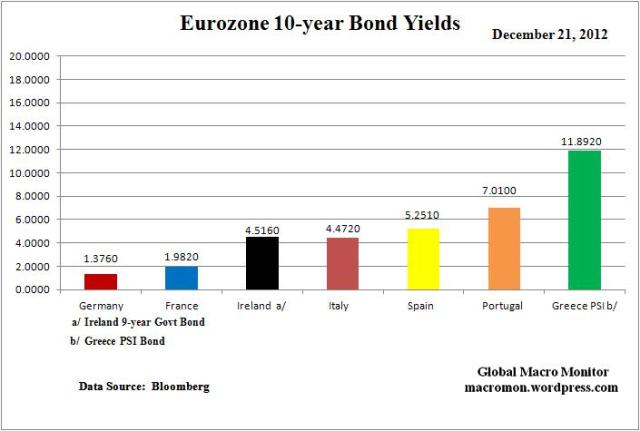

| Weekly Eurozone Watch 12.21.12 Posted: 21 Dec 2012 03:21 PM PST Key Data Points Comments Source: Guardian and Telegraph

(click here if charts are not observable)

|

| Posted: 21 Dec 2012 02:00 PM PST I know this Gotye Cover was played relentlessly this past year, but they do such a killer job on this, including 5 people playing the same guitar. Sure, its schtick, but its so well done I cannot help myself:

|

| ‘Tis four days before Christmas Posted: 21 Dec 2012 01:30 PM PST ‘Tis four days before Christmas

'Tis four days before Christmas Down on the Exchange The Fed struggled and twisted

In sports it was Giants The Mayans once told us Lady Gaga bulked up A cruise ship keeled over At the movie box office There was flooding and riots So stop looking backwards And amidst all the trading And Monday they'll pause Don't let this year's problems And resist ye Grinch feelings So count up your blessings And think ye of wonders So play ye a carol Hanukkah's just ended Whatever your feast is Monday, as the bell rings

|

| Succinct Summation of Week’s Events (12/21/2012) Posted: 21 Dec 2012 12:00 PM PST Succinct summation of week’s events: Positives:

Negatives:

|

| What going over the ‘fiscal cliff’ means . . . Posted: 21 Dec 2012 09:30 AM PST What going over the ‘fiscal cliff’ would mean . . . |

| Posted: 21 Dec 2012 07:48 AM PST From Jim Welsh, whose MacroTides have graced the Think Tank for several years now. Jim wrote this last night:

Nicely said . . . |

| Durable goods orders surprise to upside / Income Posted: 21 Dec 2012 07:15 AM PST Durable Goods orders in Nov were better than forecasted up .7% headline, 1.6% ex transports and 2.7% for non defense capital goods ex aircraft vs expectations of up .3%, down .2% and flat respectively. Also positively, Oct was revised higher. Putting into perspective though, headline orders are up just .5% y/o/y, flat ex transports and up only .3% at the core cap ex level. Within the details, vehicle/parts orders rose 3.5% more than offset by a 13.9% in nondefense aircraft. Order gains were seen in metals, machinery, electrical equipment and a tiny gain for computers/electronics. Shipments, which go right into GDP, were up 1.5% after a .1% gain in Oct and because inventories were up just .2%, the I/S ratio fell to 1.65 from 1.67. Backlogs rose .1%. Bottom line, after weakness seen in the June thru Sept timeframe where core cap ex orders fell to the lowest since Feb ’11, they have bounced back over the past two months to the most since June notwithstanding the cloudy visibility seen in economy’s overseas and with our own political process. Cap ex has been a drag on economic growth during 2012 and we’ll see if the uptick in the past few months is sustainable into 2013. ~~~ Personal Income in Nov rose .6% m/o/m, twice expectations while Spending was up .4%, in line with estimates. Because the headline PCE inflation deflator was down .2% m/o/m, REAL income was up .8% and REAL spending was up by .6%. Core PCE was flat and the y/o/y gains are 1.4% headline and 1.5% core. The PCE is now the preferred inflation gauge of the Fed because I guess they don’t like the more housing heavy CPI which has been more elevated than PCE because of rising rents. The income bounce in Nov follows the Oct decrease in wages and salaries which “reflected work interruptions caused by Hurricane Sandy” according to the BEA. The y/o/y gain in wage and salary is 3.6% with a 4.1% rise in overall income. It’s an improvement to the best since Oct ’11 but still below the average in the 20 yrs into Sept ’08 of 5.6%. The Savings Rate rose to 3.6% from 3.4%. Bottom line, with revolving consumer credit outstanding hovering around the lowest since late ’05 and the consumer’s desire to further deleverage, income growth is the important statistic in leading consumer spending higher as more production and eventually more hiring will follow that. The Savings Rate at 3.6% remains well below the average since data going back to 1959 of 6.9% and the more limited access and desire for credit must be offset by higher income and savings. The savings part is being made much more difficult by the Fed of course. There is more than $8T of national savings yielding almost nothing where just a 1% fed funds rate would be $80b+ extra into the hands of savers. |

| Posted: 21 Dec 2012 07:00 AM PST My morning reads:

What are you reading?

Fed's $4 Trillion Rescue Helps Hedge Fund as Savers Hurt |

| Mandelbrot: Fractals, Chaos and Other Mathematical Visions Posted: 21 Dec 2012 06:45 AM PST

|

| Posted: 21 Dec 2012 06:35 AM PST Foreign ownership in Japanese debt has increased 11% YoY, with total debt held outside Japan rising to a record 9.1% (US$ 1tr) as at 30th September. However, I would guess that the percentage ownership will be lower at the end of this year. It is broadly accepted that Japan’s disproportionate local holding of its debt protects it from adverse fluctuations by international markets and that increasing foreign ownership may pose risks for this stability. The BoJ owns roughly 11.1% of outstanding Japanese government debt. (Source – Financial Times/Bloomberg); Mr Narendra Modi has won a landslide victory in the western Indian state of Gujarat. Modi has been tipped to be BJP's candidate for PM at the elections in 2014. Modi is seen as a Hindu nationalist, whereas the Congress Party maintains an inclusive multi denominational perspective.

German January Consumer Confidence (GfK survey) came in at 5.6 M/M, slightly lower than the 5.9 expected and the revised 5.8 in December; French business confidence indicator came in at 89 M/M, in line with expectations and 88 in November. The outlook indicator improved marginally to -38 M/M, better than the -42 expected and -42 in November; Eurozone Consumer Confidence (December) came in at -26.6 in line with expectations of -26.5 (prev -26.9). Final UK Q3 GDP came in at +0.9% Q/Q, marginally lower than the +1.0% previously. Y/Y, GDP was flat, marginally better than the -0.1% expected. The Philly Fed Index rose materially to +8.1 (Exp -3.0) in December from -10.7 in November. The new orders component surged to +10.7, from -4.6 in November, with employment up to +3.6, from -6.8. Prices paid was relatively unchanged at +27.8, from +27.9 in November. Importantly, the expectations component (looking 6 months ahead) rose to 30.9, from 20.0. Certainly a very good piece of data, though probably reflecting the recovery post Hurricane Sandy; US existing home sales rose by +5.9% to 5.04mn homes at an annual rate, the most in 3 years and above expectations of a rise of +2.3% to an annualised rate of 4.9mn homes. I will repeat – housing will make a material positive contribution to US GDP next year, which suggests to little old me that current US GDP forecasts need to be revised higher; Mr Boehner, the House Speaker called off a vote on his Plan B last night, as he did not have enough support from his colleagues to pass the bill which, in any event, was not going to pass the Senate. Seems to have been a crazy tactic and could jeopardise his position early in the New Year. It looks as if the resolution of the fiscal cliff will carry over into the New Year, with President Obama proposing a tax cut on most Americans – probably for those earning up to US$500k. Its all politics, but the markets have reacted negatively; US personal income rose by +0.6% more than the +0.3% expected and a flat reading previously. Consumer spending was up 0.4% (prev -0.1%) in line with expectations but the largest rise since February 2012. Durable goods orders rose by 0.7%, higher than the expected 0.3% (prev 1.1%); The Brazilian Central Bank has forecast growth of 1% next year. In efforts to encourage investment, Brazil has sanctioned the privatisation of the upgrade and management of Brazil’s public airports, including Galeao in Rio. The Central Bank also increased their gold holding to 67.2 tonnes and is at the highest since August 2000. Outlook Asian markets closed lower following the withdrawal by Mr Boehner of his Plan B. European markets are around -0.5% lower, with US futures over -1.0% down. Spot gold is trading around US$1650, with February Brent at US$109.79. The Euro is trading at US$1.3215, with the Yen slightly stronger at Yen 84.10 against the US$. I continue to add to my equity holdings. Kiron Sarkar 21st December 2012 |

| ACME Corporation: 126 Coyote Endorsed Products Posted: 21 Dec 2012 05:00 AM PST Rob Loukotka watched every Coyote & Road Runner episode, then hand drew all 126 gadgets, explosives, and items that appeared in the cartoons, pulling them into a giant poster.

click for giant poster How amazing would it be if The ACME Corporation were real? That’s why Rob made this poster, funding it via Kickstarter. Only a giant 24×36″ poster can capture the incredible detail of these fun items. The posters will be beautifully screen printed on thick ‘Wild Cherry Red’ French Paper, signed and numbered by me. One poster is $30 and includes shipping anywhere in the US; $40 for anywhere else in the world.

Source: |

| The Sequestration Vote Is Nothing Like the TARP Vote Posted: 21 Dec 2012 04:20 AM PST The ongoing fiscal cliff foolishness continues to be a parade of bad data, ignorant commentary and media hype. The latest silliness: THIS IS JUST LIKE TARP. Only its nothing like TARP. Indeed, in nearly every significant way that we can c0mpare the two, they have almost no similarities:

Let’s see, 3% tax bump versus Martial Law: Yeah the Sequestration is exactly like TARP. The best part about the fiscal cliff is how revealing it is of the scaremongers, fools and charlatans, Make your list of fools now, and save it for a future date. You may find it productive.

Previously: Apprenticed Investor: Lose the News (The Street.com, 06/16/05) |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment