The Big Picture |

- Juliette Valduriez, Shredder Extraordinaire

- U.S. Equity Sector ETF Performance/Week Ending December 28

- John Cleese – a lecture on Creativity

- Ritholtz’s Dozen Rules for Investors

- How to separate fact and fiction online

- Falling Off the Fiscal Cliff

- 10 Sunday AM Reads

- Montier: Strategic Asset Allocation ≠ Static Asset Allocation

- The Properties of Income Risk in Privately Held Businesses

| Juliette Valduriez, Shredder Extraordinaire Posted: 30 Dec 2012 02:00 PM PST On the Adrian Belew post yesterday, Clay pointed us to this 24 year girl who lives in Paris. She shreds the hell out of a number of classic rock tunes:

Lost Paradise – Juliette Valduriez More videos after the jump ~~~ Comfortably Numb – Pink Floyd | ||||

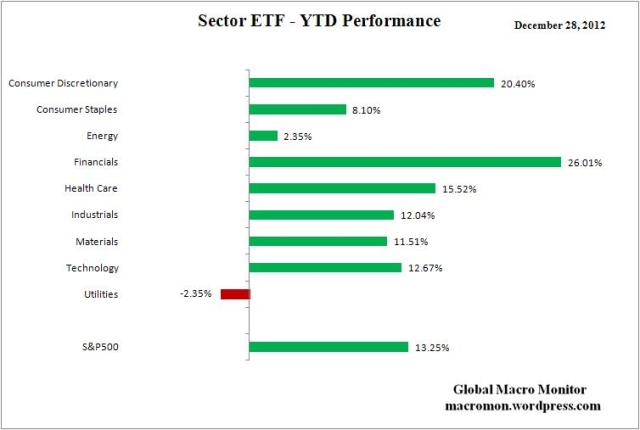

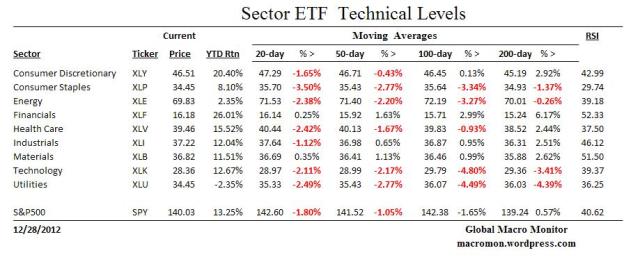

| U.S. Equity Sector ETF Performance/Week Ending December 28 Posted: 30 Dec 2012 01:00 PM PST | ||||

| John Cleese – a lecture on Creativity Posted: 30 Dec 2012 08:30 AM PST

-John Marwood Cleese (/ˈkliːz/; born 27 October 1939) is an English actor, comedian, writer and film producer. He achieved success at the Edinburgh Festival Fringe and as a scriptwriter and performer on The Frost Report. In the late 1960s he became a member of Monty Python, the comedy troupe responsible for the sketch show Monty Python’s Flying Circus and the four Monty Python films: And Now for Something Completely Different, The Holy Grail, Life of Brian and The Meaning of Life. (Continues after video)

Previously: John Cleese on the Origin of Creativity

In the mid 1970s, Cleese and his first wife, Connie Booth, co-wrote and starred in the British sitcom Fawlty Towers. Later, he co-starred with Kevin Kline, Jamie Lee Curtis and former Python colleague Michael Palin in A Fish Called Wanda and Fierce Creatures. He also starred in Clockwise, and has appeared in many other films, including two James Bond films as Q, two Harry Potter films, and three Shrek films. With Yes Minister writer Antony Jay he co-founded Video Arts, a production company making entertaining training films. It was founded in 1972 by John Cleese, Sir Antony Jay, and a group of other television professionals. The videos feature well known British actors, and humorously explain business concepts. Productions include Meetings, Bloody Meetings and More Bloody Meetings, and have featured Cleese, Dawn French, Prunella Scales, Hugh Laurie, and Robert Hardy. In December 1977, Cleese appeared as a guest star on The Muppet Show. Cleese was a fan of the show, and co-wrote much of the episode. He appears in a “Pigs in Space” segment as a pirate trying to hijack the spaceship Swinetrek, and also helps Gonzo restore his arms to “normal” size after Gonzo’s cannonball catching act goes wrong. During the show’s closing number, Cleese refuses to sing the famous show tune from Man of La Mancha, “The Impossible Dream”. Kermit the Frog apologises and the curtain re-opens with Cleese now costumed as a Viking trying some Wagnerian opera as part of a duet with Sweetums. Once again, Cleese protests to Kermit, and gives the frog one more chance. This time, he is costumed as a Mexican maraca soloist. He has finally had enough and protests that he is leaving the show, saying “You were supposed to be my host. How can you do this to me? Kermit — I am your guest!”. The cast joins in with their parody of “The Impossible Dream”, singing “This is your guest, to follow that star…”. During the crowd’s applause that follows the song, he pretends to strangle Kermit until he realises the crowd loves him and accepts the accolades. During the show’s finale, as Kermit thanks him, he shows up with a fictional album, his own new vocal record John Cleese: A Man & His Music, and encourages everyone to buy a copy. This would not be Cleese’s final appearance with the Muppets. In their 1981 film The Great Muppet Caper, Cleese does a cameo appearance as Neville, a local homeowner. As part of the appearance, Miss Piggy borrows his house as a way to impress Kermit the Frog. Cleese won the TV Times award for Funniest Man On TV — 1978-79. Many people think you are either born with creativity or you aren’t. But John Cleese explains how to become creative. John Cleese – a lecture on Creativity: In the video, he talks about such thing as the unconscious mind. | ||||

| Ritholtz’s Dozen Rules for Investors Posted: 30 Dec 2012 08:15 AM PST These were my rules I pulled together for the Washington Post:

The first half is here, second half here. | ||||

| How to separate fact and fiction online Posted: 30 Dec 2012 05:59 AM PST

By the end of this talk, there will be 864 more hours of video on YouTube and 2.5 million more photos on Facebook and Instagram. So how do we sort through the deluge? At the TEDSalon in London, Markham Nolan shares the investigative techniques he and his team use to verify information in real-time, to let you know if that Statue of Liberty image has been doctored or if that video leaked from Syria is legitimate. The managing editor of Storyful.com, Markham Nolan has watched journalism evolve from the pursuit of finding facts to the act of verifying those floating in the ether.

Markham Nolan: How to separate fact and fiction online | ||||

| Posted: 30 Dec 2012 05:55 AM PST Falling Off the Fiscal Cliff

Rarely has a Federal Reserve chairman spoken of an event in more ominous terms. Falling off the "fiscal cliff," a phrase coined by Ben Bernanke to describe a massive and abrupt shift in federal taxes and spending, may accompany the last words of "Auld Lang Syne" to begin 2013. Commentators spanning the ideological spectrum have pronounced an economic apocalypse of varying proportions. Some have forecast that the country will slide into recession for at least two quarters and possibly all of 2013, that consumers will become even more reluctant to spend and that the international economy will suffer. The Group of 20—a collection of industrialized nations whose members (including Japan and much of Europe) face their own economic challenges—pegged the cliff as the single most significant threat to global economic growth in 2013. These are serious claims, with wide-ranging implications not only on Capitol Hill but also for monetary policymakers. As such, it's important to better understand the fiscal cliff and its overall economic implications, examining key components, their size and how they interact. Assessments of the fiscal cliff are complicated by the nation's high unemployment rate and slow growth in the three-and-a-half years following the end of the last recession. Most macroeconomic analyses of a fall from the cliff indicate a large hit to gross domestic product (GDP), at least in the short run. Some suggest the best alternative strategy may be to combine short-term spending with longer-term fiscal consolidation—though such a strategy may be easier said than done. Fiscal Cliff ComponentsWhile many people view the fiscal cliff as a monolithic entity, it's actually a collection of six major provisions that happen to occur at about the same time, involving: income taxes, the alternative minimum tax, labor-market support, health care taxes, Medicare reimbursement reductions and across-the-board spending cuts. The first and among the largest of these are income tax provisions contained in the Economic Growth and Tax Relief Reconciliation Act of 2001 and companion legislation passed in 2003. Better known as the "Bush tax cuts," the legislation included lower marginal rates on income, capital gains and dividends; a smaller "marriage penalty"; larger child tax credits; and gradual elimination of the estate tax. Extending these tax provisions would cost the government $110 billion in fiscal year 2013. The second category concerns a design flaw in the alternative minimum tax (AMT)—a tax intended to ensure payments by high-income earners—that has increasingly ensnared middle-income earners. The AMT's brackets are not indexed to inflation, causing an ever-deeper dip into the ranks of the middle class. For budgetary reasons, lawmakers adopted a series of patches rather than a permanent fix for this glitch. Another patch would cost $90 billion in fiscal 2013. Just how many Americans are shielded by these patches? Roughly 4 million taxpayers were subject to the AMT in tax year 2011 (Chart 1). Without a new patch, that number would immediately rise to 30 million and would escalate, possibly reaching 66 million over the next decade. Not included in the AMT figure is an interactive effect with the 2001/03 Bush tax cuts. Because the AMT acts as a floor on how much income tax households pay, reductions in ordinary income tax rates increase AMT coverage, inadvertently broadening the AMT's reach. This effect makes patching the AMT a more expensive proposition when accompanied by extension of the Bush tax cuts. The cost—$35 billion in fiscal 2013—also increases over time. The third category, labor-market support, encompasses unemployment insurance extensions and a payroll tax cut of 2 percentage points that were enacted as part of the Job Creation Act of 2010. Studies suggest these measures have significant stimulative macroeconomic effects over the short term. However, some analysts believe further unemployment extensions may discourage job-seeking, while the payroll tax cut may have troubling implications for the solvency of entitlement programs such as Social Security over the longer term. Extending the labor-market support package would cost $115 billion in fiscal 2013. The fourth category includes tax increases adopted under the Affordable Care Act of 2010. Principal among them is a 0.9 percent Medicare payroll-tax increase for upper-income workers and an accompanying 3.8 percent "payroll tax" applied to the investment income of high-income households. Also included are new taxes on specific manufacturers, such as medical device makers. Postponing these taxes would cost $25 billion in fiscal 2013. The fifth category includes currently scheduled reductions in Medicare payments to doctors, hospitals and other health care providers. In the late 1990s, Congress examined Medicare reimbursements and concluded that a slower, sustainable growth rate in payouts to doctors and hospitals was needed to help safeguard Medicare's long-run solvency. As soon as those limits began to bite, providers persuaded policymakers in 1997 to temporarily waive them, a reprieve that has continued through this year even as the gap between sustainable spending and actual reimbursements swelled to almost 30 percent. Continuing those waivers—the so-called "docfix"—would cost an estimated $10 billion in fiscal 2013. The last component, across-the-board spending cuts, became a factor only last year. As part of the debt-limit agreement that narrowly averted a U.S. debt default in August 2011, lawmakers vowed to reach consensus on a $1.2 trillion "down payment" on deficit reduction over the next 10 years or submit to a "sequester," automatic spending cuts that would fall equally on defense and nondefense portions of the budget beginning in 2013. Canceling the sequester would raise the deficit by $65 billion in fiscal 2013. With these components and an "other" category that encompasses smaller provisions and feedback effects, fiscal cliff consolidation amounts to $560 billion in fiscal 2013 alone (Chart 2). Short-Term Economic ImpactTo understand the economic impact of the fiscal cliff, it's important to understand the logic underlying the models agencies use to assess the macroeconomic impact of government policy. It's assumed that as higher income tax rates and smaller government "transfer" payments for social programs take effect, individuals find themselves with less disposable income and respond by purchasing fewer goods and services. As businesses feel the effects of this adverse shift in aggregate demand, they scale back output—and employment. In this way, contractionary fiscal policy has a negative impact on the economy in the short run (though not necessarily over the long run). The Congressional Budget Office (CBO) found that the negative economic impact of going over the fiscal cliff would be heavily concentrated in the first half of the year, with a reduction in growth of 3 percentage points.[1] Importantly, this implies the fiscal cliff would be stout enough to briefly take the country into recession, though it would likely emerge in the second half—unless the economy were hit by further headwinds. Employment over the year would be about 2 million behind where it would have been if the cliff had been addressed. The Tax Policy Center (a joint venture of the Urban Institute and the Brookings Institution) found that disposable income would fall 4.4 percent for the middle 20 percent of households if the fiscal cliff occurred in its entirety (Chart 3). Higher-income households would be hit harder by the cliff, suffering a 7.7 percent decline, primarily because the 2001/03 tax cuts disproportionately—though not exclusively—benefit high earners. The bottom 20 percent of households would suffer the smallest decline, 3.7 percent, because several significant chunks of the cliff bypass them.[2] Interestingly, the various components of the fiscal cliff don't contribute equally to these negative economic impacts. For example, it might appear that letting the 2001/03 tax cuts expire would have a large impact because this component is among the biggest fiscal cliff budget items, as detailed in Chart 2. However, the cuts are estimated to have the fourth-largest impact, behind the sequester, labor-market provisions and AMT patch. The reason is that, in the short run, different fiscal policies can have a very different "bang for the buck" (often referred to in economic shorthand as a fiscal "multiplier"). When the government reduces its purchases and lays off workers, as would occur under the sequester, there is an immediate and sizable reduction in demand that feeds back into the overall economy—that's why the impact of the sequester on GDP is so large. Marginal rate cuts have the smallest multiplier because they flow disproportionately to higher-income individuals, who make the "wrong" choice from a short-run point of view and save those funds instead of spending and pumping them back into the broader economy.[3] Longer-Run FactorsIf averting the fiscal cliff has such large positive effects on GDP growth in the short run, why not avert it permanently and enjoy those effects not only in 2013 but every year thereafter? The answer boils down to one word: debt. In the short run, most economists agree that spending borrowed funds can stimulate the economy. But over the longer term, debt incurred from these programs reduces future generations' standard of living several ways:

No matter how things shake out, deficits will remain—but they'll be a lot larger under some circumstances than others. If none of the expiring fiscal cliff provisions were extended past 2012, the CBO estimates that deficits would gradually fall to 1.2 percent of GDP and remain there for the next decade (Chart 4). If the fiscal cliff and smaller "fiscal clifflets" later in the decade were deferred in perpetuity, however, annual deficits would never fall below 4 percent of GDP and would reach 5.5 percent by 2022—leaving the U.S. poorly positioned to cope with the fiscal challenges of expected Social Security and Medicare shortfalls. In fiscal policy as in monetary policy, it's necessary to carefully weigh short-term gain against long-term pain, often when no unambiguously optimal options are available. Many have suggested that the best strategy may be visible, loose fiscal policy today, coupled with strongly worded promises to embark upon fiscal consolidation as soon as it becomes reasonable to do so. But what's reasonable is not always apparent, making such proposals easier said than done. Perhaps the real question today is whether we have entered an era of permanently greater polarization in Congress and permanently higher fiscal policy uncertainty. If that's the case, today's fiscal cliff may be a harbinger of what's to come.

_______ Notes

| ||||

| Posted: 30 Dec 2012 05:30 AM PST My Sunday morning reads:

What are you doing this New Year’s Eve?

Chinese growth faces a more sober economy in 2013 | ||||

| Montier: Strategic Asset Allocation ≠ Static Asset Allocation Posted: 30 Dec 2012 05:30 AM PST | ||||

| The Properties of Income Risk in Privately Held Businesses Posted: 30 Dec 2012 03:00 AM PST |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |