The Big Picture |

- Global Trend Indicators

- Here’s the Thing: Peter Frampton

- Uh-Oh: NYT’s Front Page Cover Indicator

- My Hometown

- Prisoner of the Bureaucracy

- Your Three Investing Opponents

- Tea Party Membership Cards

- Shiller: U.S. Housing Decline `Could Go On’

- 10 Weekend Reads

- Cost of Borrowing Shocks and Fiscal Adjustment

| Posted: 26 Jan 2013 04:00 PM PST |

| Here’s the Thing: Peter Frampton Posted: 26 Jan 2013 03:00 PM PST This week on Here's the Thing, Alec talks with Grammy-winning guitarist Peter Frampton. "Sound is very inspirational to me," explains Frampton – and it always has been: he started playing guitar before he was 8 years old. Frampton talks about his musical roots in England, playing in bands like The Preachers and The Herd. At age 14 he was playing at a recording session produced by Bill Wyman, who he says is "sort of like my mentor, my older brother." Eleven years later, Frampton was on stage in San Francisco, recording “Frampton Comes Alive,” one of the biggest selling live albums of all times. Frampton also talks about the challenges of his extraordinary success: "I don't think anybody can be ready for that kind of success," explains Frampton. Peter Frampton recently completed a 35th anniversary tour of Frampton Comes Alive – a DVD will be available later this year. Peter Frampton |

| Uh-Oh: NYT’s Front Page Cover Indicator Posted: 26 Jan 2013 12:00 PM PST

The rest of the article is just as bullish:

To be sure, there are some caveats throughout:

But overall, there is no escaping the sentiment of either the headline of that first sentence or the gist of the entire column. Stocks are back, baby! Now is the time to jump onboard. I have been fairly selective as to what qualifies as a magazine cover indicator and what is merely media noise. Let us look at the details of this one:

That is how I determine when the magazine cover has been initiated. I cannot think of any reason why this one does not qualify. This chart accompanied the article: A Steady Ascent

Previously: Source: |

| Posted: 26 Jan 2013 10:00 AM PST My mother had a two-tone Maxima, light and dark blue. It replaced the five cylinder Audi which was a great car when it ran right, which was rarely. Only buy Japanese cars. Unless you’re rich, or leasing, or both. And it was in this car I found myself driving on Route 7 from Middlebury to Rutland on one of those days when it’s not sure whether it wants to rain or snow. When the temperature is hovering around thirty two degrees and God can’t decide whether to add to the snowpack or deplete it. And on the radio I heard “My Hometown.” It used to be a boonie ritual. Driving with one hand on the steering wheel and the other on the radio knob, trying to pull in a station. You’d get the farm report, some country music, the real, twangy stuff, not the faux rock and roll of today, and if you were lucky something you wanted to hear on a Top Forty station. This was back when our relationship was teetering. A year and a half after we got married. And when things are going south you know it because of the silence. Suddenly there’s nothing to say. And if you venture a few words you get no response, except maybe a guttural “um” or “mm.” And the song keeps playing on the radio and you keep listening and your whole life plays out in your brain as you stare at the highway.

My father loved his hometown. He took pride in the location of our domicile, just a block from the main drag, where we could get a quart of milk or a loaf of bread whenever we wanted. The upwardly mobile moved to Skytop Drive, but things were good down on Black Rock Turnpike, where we had Richelsoph’s Bakery. Where they sliced the rye after you bought it and it was still warm and if your mother didn’t restrict your grabbing you could eat half of the loaf before you got home. But my dad never put me on his lap to drive. He was a safety bug. Nothing untoward was ever done. But the cancer got him anyway. He died five years after the purchase of that Maxima. I told my mother to give it to my little sister when he passed. They trucked it to Minnesota where it never died, but was replaced when my brother-in-law’s career floated upwards in the boom of the last decade.

Big Al struck it rich and bought a barn in Newtown. He died in a hotel in New York, his Parkinson’s felled him while he was waiting for the elevator. But back in the seventies, we used to drive over and play tennis, badly, during the boom, when it caught the national mood. This was after the sixties, when every year someone got assassinated and everybody was fighting for his rights, when the youth took the country from the old men, when we were all in it together. Before greed and income inequality created a gap so wide in my hometown the poor don’t interact with the rich unless they’re bused in to clean.

They never made much in my hometown, but I know too many people who lost their job and their house and are struggling. As we get older every day. We assumed our kids would do better than us. We no longer believe that.

I got out. I saw Los Angeles on television, I listened to the Beach Boys & Jan and Dean sing about a happy, carefree life and when I graduated from college I moved. And it is better. But now I’m approaching sixty and I’ve got no kids and instead of worrying about finding a station on the radio I’m overwhelmed with input. I’ve got AM, FM, XM, iPod, iPhone, Internet…and we’re all closer together, just an e-mail or a text away, but we’ve all retreated into our niches, we’ve lost our cohesiveness. We’re no longer all in it together, we’re doing our own thing. And when you take a break and look up and realize no one’s around you wonder…are we better off? “My Hometown”: http://spoti.fi/Jhc5p4 ~~~ If you would like to subscribe to the LefsetzLetter |

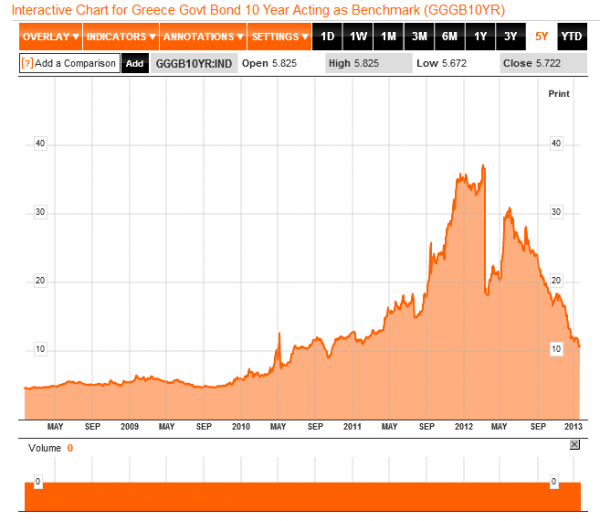

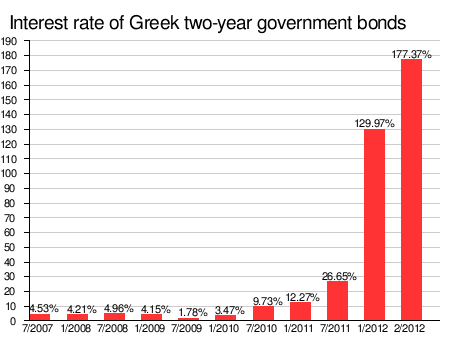

| Posted: 26 Jan 2013 09:00 AM PST Prisoner of the Bureaucracy

Greece Must Stay in the Euro |

| Your Three Investing Opponents Posted: 26 Jan 2013 07:00 AM PST "Tough Year!" We hear that around the office nearly every day – from professional traders to money managers to even the 'most-hedged' of the hedge fund community. This year's markets have perplexed the best of them. Each week brings another event that sets up some confusing crosscurrent: call them reversals or head fakes or bear traps or (my personal favorite) the "fake-out break-out" – this is a volatile, trendless market has been unkind to Wall Street pros and Main Street investors alike. Indeed, buy & hold investors have had more ups and downs this year than your average rollercoaster. The third and fourth quarters alone had more than a dozen market swings, ranging from 5 percent to more than 20 percent. Despite all of that action, the S&P 500 is essentially unchanged year-to-date. It doesn't take much to push portfolios into the red these days. Three Opponents in Investing With markets more challenging than ever, individual investors need to understand exactly whom they are going up against when they step onto the field of battle. You have three opponents to consider whenever you invest. The first is Mr. Market himself. He is, as Benjamin Graham described him, your eternal partner in investing. He is a patient if somewhat bipolar fellow. Subject to wild mood swings, he is always willing to offer you a bid or an ask. If you are a buyer, he is a seller – and vice versa. But do not mistake this for generosity: he is your opponent. He likes to make you look a fool. Sell him shares at a nice profit, and he happily takes their prices so much higher you are embarrassed to even mention them again. Buy something from him on the cheap, and he will show you exactly what cheap is. And perhaps most frustrating of all, Mr. Market has no ego – he does not care about being right or wrong; he only exists to separate the rubes from their money. Institutional Competitors Yes, Mr. Market is a difficult opponent. But your next rivals are nearly as tough: They are everyone else buying or selling stocks. Recall what Charles Ellis said when he was overseeing the $15-billion endowment fund at Yale University:

Ellis lays out the brutal truth: investing is a rough and tumble business. It doesn't matter where these traders work – they may be on prop desks, mutual funds, hedge funds, or HFT shops – they employ an array of professional staff and technological tools to give themselves a significant edge. With billions at risk, they deploy anything that gives them even a slight advantage. These are who individuals are doing battle with. Armed only with a PC, an internet connection, and CNBC muted in the background, investors face daunting odds. They are at a tactical disadvantage, outmanned and outgunned. We Have Met the Enemy and They Is Us That is even before we meet your third opponent, perhaps the most difficult one to conquer of all: You. You are your own third opponent. And, you may be the opponent you understand the least of all three. It is more than time constraints, lack of discipline, and asymmetrical information that challenges you. The biggest disadvantage you have is that melon perched atop your 3rd opponent's neck. It is your big ole brain, and unless you do something about it, it is going to lose all of your money for you. See it? There. Sitting right behind your eyes and between your ears. That "thing" you hardly pay any attention to. You just assume it knows what it's doing, works properly, doesn't make too many mistakes. I hate to disabuse you of those lovely notions; but no, sorry, it does not work nearly as well as you assume. At least, not when it comes to investing. The wiring is an historical remnant, hardly functional for modern living. It is overrun with desires, emotions, and blind spots. Its capacity for cognitive error is nearly endless. It was originally developed for entirely other purposes than risk assessment in capital markets. Indeed, when it comes to money, the way most investors use those 100 billion neurons or so of grey matter, they might as well not even bother using their brains at all. Let me give you an example. Think of any year from 1990-2005. Off of the top of your head, take a guess how well your portfolio did that year. Write it down – this is important (that big dumb brain of yours cannot be trusted to be honest with itself). Now, pull your statement from that year and calculate your gains or losses. How'd you do? Was the reality as good as you remembered? This is a phenomenon called selective retention. When it comes to details like this, you actually remember what you want to, not what factually occurred. Try it again. Only this time, do it for this year – 2011. Write it down. Go pull up your YTD performance online. We'll wait. Well, how did you do? Not nearly as well as you imagined, right? Welcome to the human race. (Despite having taken numerous high-performance driving courses and spending a lot of time on various race tracks, I am only an average driver. I know this because my wife reminds me constantly.) As it turns out, there is a simple reason for this. The worse we are at any specific skill set, the harder it is for us to evaluate our own competency at it. This is called the Dunning–Kruger effect. This precise sort of cognitive deficit means that areas we are least skilled at – let's use investing decisions as an example – also means we lack the ability to identify any investing shortcomings. As it turns out, the same skill set needed to be an outstanding investor is also necessary to have "metacognition" – the ability to objectively evaluate one's own abilities. (This is also true in all other professions.) Unlike Garrison Keillor's Lake Wobegon, where all of the children are above average, the bell curve in investing is quite damning. By definition, all investors cannot be above average. Indeed, the odds are high that, like most investors, you will underperform the broad market this year. But it is more than just this year – "underperformance" is not merely a 2011 phenomenon. The statistics suggest that 4 out of 5 of you underperformed last year, and the same number will underperform next year, too. Underperformance is not a disease suffered only by retail investors – the pros succumb as well. In fact, about 4 out of 5 mutual fund managers underperform their benchmarks every year. These managers engage in many of the same errors that Main Street investors make. They overtrade, they engage in "groupthink," they freeze up, some have been even known to sell in a panic. (Do any of these sound familiar to you?) These kinds of errors seem to be hardwired in us. Humans have evolved to survive in competitive conditions. We developed instincts and survival skills, and passed those on to our descendants. The genetic makeup of our species contains all sorts of elements that were honed over millions of years to give us an edge in surviving long enough to procreate and pass our genes along to our progeny. Our automatic reactions in times of panic are a result of that development arc. This leads to a variety of problems when it comes to investing in equities: our instincts often betray us. To do well in the capital markets requires developing skills that very often are the opposite of what our survival instincts are telling us. Our emotions compound the problem, often compelling us to make changes at the worst possible times. The panic selling at market lows and greedy chasing as we head into tops are a reflection of these factors. The sort of grinding market we had in 2011 only exacerbates investor aggravation, and therefore increases poor decision making. Facts and logic go out the window, and thinking gets replaced with naked emotions. We get annoyed, angry, frightened, frustrated – and that does not help returns. Indeed, our evolutionary "flight or fight" response developed for a reason – it helped keep us alive out on the savannah. But the adrenaline necessary to fight a Cro-Magnon or flee from a sabre-toothed tiger does not help us in the capital markets. Indeed, study after study suggests our own wetware works against us; the emotions that helped keep us alive on the plains now hinder our investment performance. The problem, as it turns out, lies primarily in those large mammalian brains of ours. Our wiring evolved for a specific set of survival challenges, most of which no longer exist. We have cognitive deficits that are by-products of that. Much of our decision making comes with cognitive errors "secretly" built in. We are often unaware we even have these (for lack of a better word) defects. These cognitive foibles are one of the main reasons that, when it comes to investing, we humans just ain't built for it. We Are Tool Makers But we are not helpless. These large mammalian brains of ours can do a whole lot more than merely overreact to stimulus. We think up new ideas, ponder new tools, and create new technologies. Indeed, our ability to innovate is one of the factors that separates us from the rest of the animal kingdom. As investors, we can use our big brains to compensate for our known limitations. This means creating tools to help us make better decisions. When battling Mr. Market – as tough as any Cro-Magnon or sabre-toothed tiger – it helps to be able to make informed decisions coolly and objectively. If we can manage our emotions and prevent them from causing us to make decisions out of panic or greed, then our investing results will improve dramatically. So stop being your own third opponent. Jiu jitsu yourself, and learn how to outwit your evolutionary legacy. Use that big ole melon for a change. You just might see some improvement in your portfolio performance. Individual Investors Have Certain Advantages Over Institutions One final thought. Smaller investors do not realize that they possess quite a few strategic advantages – if only they would take advantage of them. Consider these small-investor pluses:

And with those thoughts, good luck and good trading in 2012! ~~~ This was originally published as part of a longer piece in Thoughts from the Frontline exactly one year ago, on January 25, 2012.

|

| Posted: 26 Jan 2013 05:00 AM PST

|

| Shiller: U.S. Housing Decline `Could Go On’ Posted: 26 Jan 2013 04:39 AM PST Robert Shiller, a professor at Yale University and co-creator of the S&P/Case-Shiller index of property values, talks about the global economy and the U.S. housing market. He speaks with Tom Keene on Bloomberg Television’s “Surveillance” on the sidelines of the World Economic Forum in Davos, Switzerland. (Source: Bloomberg)

|

| Posted: 26 Jan 2013 04:00 AM PST Ahhh, good to be back. Here are my long form pieces of journalism to start your snowy weekend:

What’s up for the weekend?

Bull Market Winding Down. Don’t Panic |

| Cost of Borrowing Shocks and Fiscal Adjustment Posted: 26 Jan 2013 03:00 AM PST |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment