The Big Picture |

- Why We Are In a Perpetual Series of Wars …

- Weekly Eurozone Watch: Spread Compression Continues (1/4/12)

- Top Ten Issues in the Music Industry

- Rick Santelli’s First Insane Rant of 2013

- 2013 Outlook & Forecast

- Employment/Unemployment Pictures

- Cosmic Collision

- 10 Weekend Reads

| Why We Are In a Perpetual Series of Wars … Posted: 05 Jan 2013 10:30 PM PST Endless War Is a Feature – Not a Bug – of U.S. PolicyWe are in the middle of a perpetual series of wars. See this, this, this and this. As just one example, in 2010 the war in Afghanistan became the longest war in U.S. history. But – no matter what you've heard – there are no plans to get out any time soon. As Glenn Greenwald notes today:

Why is the war of terror being waged indefinitely? Many have said that "war is the health of the state", and Thomas Paine wrote in the Rights of Man:

George Washington – in his farewell address of 1796 – said:

James Madison said:

Madison also noted that never-ending war tends to destroy both liberty and prosperity:

Greenwald noted in October:

Indeed, top American military officials and national defense experts say that our specific actions in the "war on terror" are creating more terrorists and more war. As Greenwald points out today, the endless nature of the war on terror is a feature, not a bug:

Indeed, the American government has directly been supporting Al Qaeda and other terrorist groups for the last decade. See this, this, this, this and this. (Remember, if there aren't scary enough enemies in real life, we've got to create them. Oops … did I say that out loud?) And the American government lies – and even kills its own – to justify new wars. Top American economists say that endless war has ruined our economy. It benefits a handful of elites, while levying a tax on the vast majority of Americans. Congress members – part of the super-elite which has made money hand over fist during this economic downturn – are heavily invested in the war industry, and routinely trade on inside information … perhaps even including planned military actions. No wonder the American government is making the state of war permanent, and planning to unleash new, widespread wars in the near future. Postscript: Under Bush, it was the "war on terror". Obama has re-branded the perpetual fighting as "humanitarian war". But - underneath the ever-changing marketing and branding campaign – it's really just the good 'ole military-industrial-and-banking complex consolidating their power and making money hand over fist. |

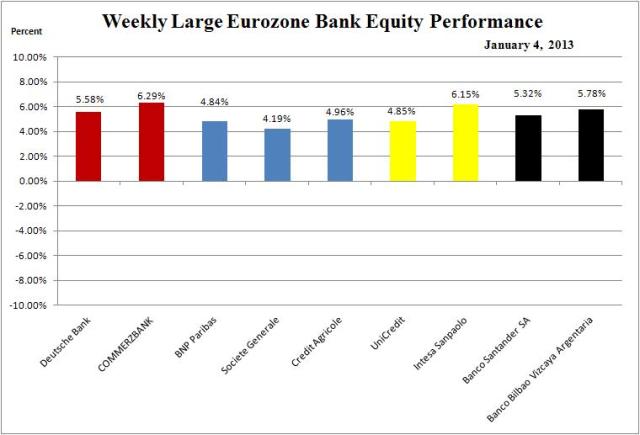

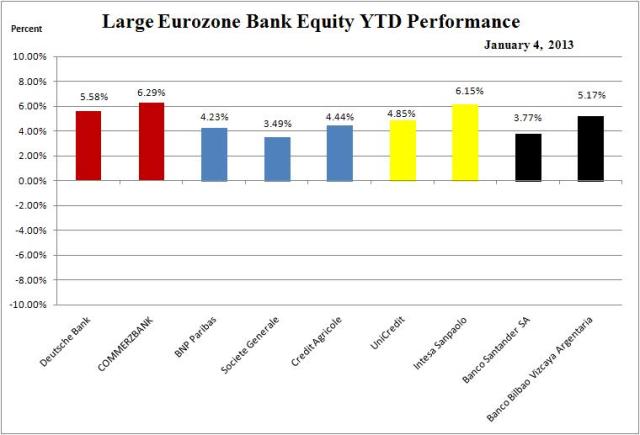

| Weekly Eurozone Watch: Spread Compression Continues (1/4/12) Posted: 05 Jan 2013 02:00 PM PST Key Data Points Comments

|

| Top Ten Issues in the Music Industry Posted: 05 Jan 2013 12:00 PM PST Problems: 1. Filter People don’t know what to listen to. You can’t trust the radio, you can only trust your friends, and who’s to say your friends have the same taste as you? He who tells us what to listen to will have all the power in the future. It will not be an algorithm. If you think Pandora has great recommendations, you’ve got no taste. If that’s the future of radio, I want no part.

2. Money Trumps Art Everyone’s trying to get rich, or bitching that they’re poor. People no longer discuss music, but their financial stability. Furthermore, money is the ultimate arbiter. If someone sells a lot of tickets or a lot of tracks you can’t say a negative thing about them. This coarsens our society. Critical thinking is crucial to a healthy arts scene. Something can be successful and suck. Conversely, it can be obscure and great. If your first question is how do I make money, you shouldn’t be in music.

3. Everybody Thinks They’re A Star We’re only interested in the exceptional. It’s kind of like the Olympics, if you don’t medal, we don’t know your name. In the old days, with a limited universe, mediocre, with exposure and promotion, could make it. Today, you’ve got to be positively A-team. Or, the beneficiary of A-team marketing and promotion. But if your music doesn’t sell itself, your career will be very brief.

4. You Can’t Get A Good Ticket At A Fair Price Therefore people don’t even try to buy. For all the bitching from people who overpay or sit in the cheap seats there are legions who’ve opted out of live music. This is the industry’s problem. With no one leading the charge against it. It’s easy to fall out of the habit of going to the show.

5. Greed This is just how the rich like it. The hoi polloi fighting amongst themselves, oblivious to the true enemy. The acts and executives, the agents and the promoters, they’re fighting over a tiny pot.

6. Con Artists You know, the websites that give you advice and hope, and charge you for the privilege. Not everybody can work in the music business, not everybody can be a star. If you’re paying someone to host your stuff, to get you gigs, you’re either not good or delusional or both.

7. Classic Rock It was too good. Just because the kids like something that does not make it good. Come on, all you trumpeting the Jonas Brothers, name one of their songs… Until modern acts truly reach the brass ring, the whole sphere will suffer. As for those saying today’s music is just as good as yesteryear’s…you don’t have ears.

8. Old Media From radio to newspapers to movies it’s old world thinking, a circle jerk trying to perpetuate something that’s dead. The sooner old media dies, the clearer the landscape will be. Radio is not coming back. Newspapers will not survive in print, and most won’t survive at all. And while we’re at it, CDs are history and physical books are goners. The fact that something still exists does not mean it isn’t over. If you’re discussing piracy, the death of the CD, singles and streaming, you’re wasting your breath. The modern music world is not like Congress, there’s no consensus amongst an elite. Instead modernity is an endless rushing river controlled by nobody. If you’re doubling down on old media, you’re probably investing in the PC business and feature phones.

9. Working The Numbers Whether it be authors scamming Amazon reviews or record companies garnering fake YouTube plays you can no longer trust statistics and reviews. Everybody’s a scumbag. Trying to game the system. And it’ll only go away when e-mail spam is eradicated. Which probably won’t be in my lifetime.

10. Lack Of Knowledge No one knows history. Before you sit down to write your song, listen to the Beatles catalog, learn about a bridge, learn about harmony. You can’t break every rule and be successful. If you’re familiar with the basic building blocks, you’ve got a chance of making it.

NOT A PROBLEM 1. Peer To Peer File-Sharing It’s declining. Everything’s free on YouTube anyway. To worry about piracy is to be shortsighted. If you don’t want people to trade your music you’re living in the last century. Your enemy is not piracy, but obscurity. Just because the RIAA controls the media discussion, that doesn’t mean you should pay attention. Focus on your career. Focus on being great. There’s plenty of money to be made if you are. Not as much as being a banker, but that’s got more to do with the meshuggeneh country we live in and its flawed economic policies than piracy.

2. Sound Quality The baby boomers listened to 45s on some of the worst systems imaginable. If it’s a hit song, it sounds good on anything. Yes, a hi-fi boom would lift all boats, but it won’t happen by badgering people their sound sucks, but creating stuff so marvelous you want to hear it at a high level, which is not today’s compressed, loudness wars crap.

3. Electronic Music You didn’t understand rap, does your opinion on EDM count?

4. Texting & Shooting Photos At Gigs People live to communicate, it’s human nature. Maybe they’ll communicate about you! The best way to combat social media at a show is to be absolutely riveting. But even that won’t work…people live to connect. And at these prices do you blame them?

5. Information Google yourself. You’ll find the bread crumbs of your life. You never know when someone will decide to check you out. If you’ve got no online presence, you will have no success. The first thing someone does when they’re interested is read your Wikipedia page. And they can tell if you wrote it yourself, they laugh behind your back. If someone can’t research your history and find out almost everything about you, you’re doing it wrong. Don’t think campaign, think land mine. People will find you when they’re good and ready.

~~~ – |

| Rick Santelli’s First Insane Rant of 2013 Posted: 05 Jan 2013 10:04 AM PST |

| Posted: 05 Jan 2013 09:14 AM PST I believe that the current year should be positive for equity markets, in particular in H2 2013, subject to adverse geopolitical issues. US The US, as the market expected, cobbled together a "deal" on the fiscal cliff. Taxes will rise on individuals and couples earning over US$400k and US$450k respectively, as will capital gains taxes on such individuals, together with estate-tax rates. Furthermore, the value of personal exemptions will be limited for the better off. In addition, the decision on approx US$110 bn of automatic spending cuts will be deferred for 2 months. The elimination of a 2.0% payroll tax cut will impact all US citizens and will take its toll on US GDP this year, in particular on Q1 2013 GDP, with GDP declining to below Q4 2012 levels. In aggregate, tax revenues will rise by US$600bn over the next 10 years. The measures, will reduce the US budget deficit this year. Negotiations over further spending cuts, over the next couple of months, will reduce the budget deficit further. However, the next phase (over the next 2 months) will have to deal with the much more contentious issue of additional spending cuts and the governments need to increase the debt ceiling. Expect a renewed fight, which will prove much tougher to resolve than the partial agreement which has been achieved in respect of the "fiscal cliff". Nevertheless, the deal over the fiscal cliff was greeted with relief, with markets rising materially following the announcement. However, with the next set of negotiations likely to be far more fraught, markets may well react negatively, as the intensity of the debate reaches levels unseen to date. Whilst a number of analysts expect a continuing weak recovery in the US, I believe that the US will grow far faster than current expectations, in particular in H2 this year. I have assumed that the forthcoming spending cuts/debt ceiling negotiations are ultimately resolved, which I believe will be the case, though it is no shoe-in, I must admit. Recent US economic data has been better than expected and whilst growth in Q4 2012/Q1 2013 will be subdued, with GDP of around +1.75% and sharply lower to just +0.75% or lower (impact of the payroll tax rise, in particular) respectively (much lower than the +3.1% Q/Q in Q3 2012), GDP should start to rise in Q2 2013, with further material increases through H2. The most recent ISM non-manufacturing data pointed to a strong rebound, particularly in employment. I would not be surprised if US 2013 GDP increases by at least +2.25% to +2.50%, with Q4 annualised GDP quite possibly over +3.5%, as the real improvement comes through in H2 this year. I appreciate that the deal on the fiscal cliff, combined with the impending negotiations on spending cuts, could translate into a fiscal drag of between 1.25% to 1.50% this year. However, there are a number of latent growth drivers which I believe will more than counteract this fiscal drag. Importantly, an analysis of final Q3 GDP data revealed that corporate profits across the whole economy came in higher than expected. That bodes well for the current year. Towards the end of 2012, US businesses stopped spending, due to uncertainties relating to the Presidential elections and concerns over the fiscal cliff. That will reverse, starting in Q2, but mainly in H2 2013, once agreement over spending cuts and the debt ceiling has been "resolved". Residential housing, which has been a drag on the economy, will continue to improve and will make a meaningful contribution to GDP this year, with employment in the sector rising. A better housing market is a key factor for an improvement in the US economy. Last year, US residential home prices recorded their first price increase since 2006, a trend I expect will continue this year, helping to reduce negative equity. As the housing sector and the economy improves, the banking sector should benefit. In particular, I believe that banks will ease their strict lending standards, increasing the number of mortgages issued, together with credit to businesses and consumers generally, which will be supportive of the US housing market, consumption, smaller businesses and, as a result, US GDP. Indeed, the CEO of BoA has stated that his bank will increase the flow of credit, a policy which will be followed up by other banks. Mortgage rates will rise from current record lows however, as bond yields increase, suggesting that the number of home purchases could rise materially in coming months, as people rush to obtain cheaper mortgages. December NFP's data reported an increase of 155k jobs, slightly better than forecast, with the prior month revised higher. In addition, private sector payrolls came in stronger than expected at +168k, as compared with +155k expected. I expect that this years NFP data will be much more positive, in particular in H2. I would not be surprised if the unemployment rate declines to closer to (or below?) 7.0% by the year end, resulting in improving sentiment, leading to higher consumption. For US unemployment to decline to 7.0%, a net 200k jobs per month needs to be created this year, according to a calculator produced by the Atlanta FED. Whilst above the long term average, its not at all impossible in my humble view, given the pent up demand in the economy. The US is and will increasingly benefit for a rise in domestic energy production, a truly transformational event in coming years. The competitive advantage of lower US energy costs will enable energy intensive industries to thrive and will act as a further stimulus for the US economy. Admittedly, the material benefits of these new energy sources will take some years to flow through, through capex spending related to this sector (both in terms of production and use by energy intensive related businesses) will increase, as will employment, providing yet another boost to the US economy. I do not believe that the full extent of this factor has been fully appreciated by the markets. With the FED’s QE programme in place, monetary stimulus should cement the US recovery, with unemployment declining faster than expected. Rising GDP may well force the FED to reduce the size of its QE programme (currently US$85bn per month) in H2. Indeed, the recent FED minutes suggested that Committee members were thinking of slowing or even ending the FED's asset purchase programme in H2 this year. With the FED on hold in terms of interest rate increases, until employment declines to 6.5% or inflation rises to +2.5% (unlikely this year), interest rates will remain on hold. Furthermore, with an elevated unemployment rate and with discouraged workers returning to the labour force as the economy improves, wages and salaries increases will be constrained, benefiting corporate earnings, whilst keeping inflation constrained. The S&P closed over +13% higher in 2012 and I remain positive, indeed bullish on US equity markets, this year. In particular, I like the financials, tech, building materials, property and industrial sectors. Businesses associated with the new energy sources (both oil and gas) in the US should also benefit, as will retailers, given increased consumer spending. Cheaper energy will also help limit pressure on corporate margins and inflation. Europe This year, I believe that the EZ will relax its austerity policy, as Mrs Merkel faces a general elections in September, which she is expected to win. The most recent poll reports that her CDU party has support of 41% of the population, as opposed to just 27% for the SPD, with the Greens on 13%. She will need to find a new coalition partner. In particular, Mrs Merkel will want to avoid a crisis in the EZ, given her upcoming general election. Indeed, she may “approve” or at least not oppose (more likely) some growth policy measures. In addition, I sense that EZ policy makers are beginning to understand the negative impact of austerity measures (spending cuts, combined with tax increases), which has increased the fiscal multiplier to above 1 for a number of countries. Essentially, if the fiscal multiplier for a particular country rises above 1, further austerity measures will worsen the fiscal, economic and unemployment situation for countries, including Greece, Portugal and Spain and arguably France and Italy, rather than improve the situation. The consequence of this absurd policy has been to reduce growth and, as a result, tax revenue, which, in turn, increases debt to GDP – precisely the opposite of what the policy was intended to achieve. As you know, I have been banging on about this issue for quite a few months. The IMF's chief economist no less, Mr Olivier Blanchard has just published a paper admitting that the IMF misjudged the negative impact that significant austerity measures would have on a number of EZ countries, given the impact of the fiscal multiplier. Yes, Spain, Portugal, Italy and France will all fail to meet their fiscal targets this year, but I believe that the EU (and Germany) will be more tolerant of countries that miss their targets. However, I remain convinced that Portugal and Spain will have to restructure their debts – their current levels of debt are unsustainable. In addition, I believe that Ireland will eventually be offered a deal in respect of its bank related debt, allowing the country to exit its bailout programme this year. The EZ needs a success story and the only candidate is Ireland. In addition, the materially better deal offered to Greece will result in other peripheral EZ countries demanding better terms than at present. The ECB’s OMT programme is a major deterrent to those who wish to short peripheral EZ bonds, though I do believe that Spain will have to seek assistance sometime this year, in spite of continued dithering by its PM and a reluctance by Germany for Spain to seek assistance, ahead of their September general election. Spain cannot afford to borrow even at current rates, as Spanish GDP is negative and further borrowing merely raises the level of debt to GDP to even more unsustainable levels. Furthermore, Spain, whose GDP was dependent, inter alia, on consumption and construction (both dead in the water), will find it difficult to rebalance its economy. A further credit downgrade for the country is likely. 2013 German GDP forecasts are, I believe, unduly pessimistic. Yes, Germany will contract in Q4 2012 and Q1 2013 GDP growth will be flat. However, Germany is refocusing its exports away from the EZ and towards emerging markets, whilst exports to the US are rising. Domestic consumption remains robust and whilst unemployment may creep up in Q1/H1, it should stabilise and indeed improve in H2, in particular. Consumer, industry and investor confidence remains high and, indeed, is improving. A recent Ernst & Young poll reports that 78% of Germans were optimistic on the future and confidence has improved over the last 3 months. As a result, I believe that German GDP may grow by more than +1.25% this year (the Bundesbank forecast is just +0.4%), well above analyst expectations of less than half that number. Following the September general elections, I believe that Germany will be willing to embark on banking, fiscal and, in addition, a transfer union, in addition to the existing monetary union, though such measures will be introduced cautiously and mainly from 2014 onwards. Such policies will have a profound and positive impact on the EZ in due course, though treaty changes will be necessary and EZ countries will have to agree to a centralised budget mechanism. However, these policy initiatives will require the approval of the German Constitutional Court – no easy task, I must admit. In addition, the cost of partially "bailing out" the EZ will negatively impact Germany in coming years. Germany's industrial companies should benefit from stronger global growth, resulting in higher exports, in particular to the US and EM's. Whilst EZ Q4 2012 GDP may be around -0.4%/-0.5% lower, with Q1 2013 GDP negative as well, I believe that the EZ economy will stabilise in H2. However, GDP for the 17 countries in the EZ may come in better, around flat for the year – the ECB forecast is -0.3%. Importantly, due to base effects, year on year economic comparisons within the EZ will get easier, in particular in H2 this year. Essentially, I believe that the EZ economy will stabilise in the next 3 to 6 months, with the data improving thereafter, though admittedly off a particularly weak base. However, stabilisation, followed by marginally better data, will be positive for EZ equity markets. There are risks, however. In the near term, impending elections in Italy could create political uncertainty, though I do not believe that Mr Berlusconi will return to power. Furthermore, social tensions and civil disorder within the EZ could resurface, as the weather improves in spring. I continue to believe that France will pose the most significant problem for the EZ. The government's pursuit of failed economic policies (including increased taxation, higher government spending, inability to introduce labour reforms, etc, etc) is such that the country will remain a major threat to the EZ. French unemployment continues to rise, with the the number out of work rising by +0.9% M/M to 3.132mn in November, the 19th consecutive monthly increase. Final Q3 GDP came in at just +0.1% and Q4 2012/Q1 2013 do not look promising either – a contraction is likely. French December retail PMI declined to 46.8, down from 48.8 in November, which is clearly negative for a country whose GDP is materially dependent on consumption. The other main drivers of the French economy, namely defence and autos look weak as well. With debt to GDP around 90% and unlikely to meet its 3.0% budget deficit target this year, combined with questionable policies and opposition to much needed changes, France's problems look near impossible to resolve. President Hollande's relationship with Mrs Merkel continues to worsen, with France joining the Mediterranean club of Spain, Italy and Greece, rather than the core Northern European EZ countries. Essentially, Germany increasingly is ignoring France. To date, French bond yields have not widened materially. However, this year, I believe that the honeymoon period for France will be over, with yields moving towards Spanish and Italian levels, rather than declining towards German yields – a major problem for the country. However, the problems in France will just highlight the need to implement growth policies within the EZ. In addition, we all know, that Greece’s fiscal position is unsustainable and a further haircut will be necessary. However, they have been provided a lifeline, which further aid likely if they come even close to meeting their commitments, though the risks of another political/economic/social crisis in Greece remain. Businesses in the EZ are becoming more efficient (they have no choice) and the benefits should flow through to earnings towards the end of this year and, in particular, over coming years – once again, materially positive. I would not be surprised to see the peripheral EZ markets outperform the core countries, but I will continue to invest in Germany and possibly Holland (even though Holland is likely to lose its AAA rating), whilst avoiding France. I really don’t know how France gets itself out of its problems and a further credit downgrade is likely this year. Less bad news from the EZ as the year continues, together with faster growth in the US and EM's, should help the UK, though the country is likely to lose its AAA credit rating this year. However, given the weightings of the FTSE 100 (50% by market value is made up of mining, energy and financials sectors), I expect the FTSE 100 to outperform other European markets as recovery takes hold globally, in particular in H2. Furthermore, anecdotal data suggests that the UK economy is performing better than official statistics would suggest. I remain positive on UK equities. Japan Mr Abe wants the BoJ to increase inflation to a target of 2.0% and has threatened to introduce legislation to curtail the independence of the BoJ, unless they respond ahead of, or at least at, the 21/22nd January meeting. The Governor of the BoJ, Mr Shirakawa, who has proved to be particularly cautious in the past (his recent comments have been confusing), retires on the 8th April, as do two other hawkish board members on the 19th March. At present, the 9 member board comprises just two members, who are deemed "dovish". However, with three other replacements in due course (making a majority of five out of nine BoJ members by April, including a more sympathetic governor), the BoJ should, as is the case in the US, EZ, UK etc, embark on a more accommodative monetary policy, to accompany the expected major fiscal stimulus programme which the government will introduce. However, appointments to the BoJ board require the approval of the opposition controlled Upper House. Elections for half of the seats in the Upper House are due in July this year and gaining a majority in the Upper House will be no easy task for Mr Abe's LDP coalition. A policy to increase inflation and, as a result, interest rates in a highly indebted country such as Japan is a high risk policy, in particular, as the country suffers from a huge budget deficit, combined with a trade deficit and recently, most importantly, a current account deficit. If Japan, in coming years, has to rely on external financing to finance its budget deficit, assuming the current account deficit continues, the negative impact on the Yen will be material. Yes, a weaker Yen will help Japanese companies export more, though as recent results have proven, Japanese industries (particularly the electronics sector) seem to have lost their way and with competition from China, Korea and Taiwan, together with Germany and the US, an improvement of Japanese industry will take time, at the very least. Industrial production was -1.7% lower M/M in November, far worse than the -0.5% expected. Furthermore, workers earnings were -1.1% lower Y//Y, much weaker than the -0.4% forecast. The new Finance Minister Mr Aso will not limit new bond issuance to Yen 44tr per year, a policy instituted by the former administration. Increasing the level of government debt will increase Japanese bond yields, a particularly significant problem for the country, as Japanese debt (US$14.6 tr) to GDP exceeds 220%. Furthermore, who are the prospective buyers of such debt. In the past, Japanese financial institutions have been. However, with a weaker Yen, enormous existing holdings and the prospect of higher rates, the Japanese financial sector will be a less willing buyer (other than short term securities), preferring foreign assets, even though they are unlikely to be major sellers of JGB's, as they will not want to undermine the market. I believe that this issue will prove to be a major problem for the Japanese authorities later this year. A credit downgrade for the country is very likely, as well. Whilst politically difficult, the LDP (less so their coalition partner) have indicated that they will restart the nuclear electricity programme, subject to the relevant reactors being deemed safe. A restart of Japan’s nuclear programme will reduce Japan’s trade deficit materially and likely result in Japan producing a current account surplus – clearly Yen positive. In addition, a nuclear restart will reduce fossil fuel based energy demand globally, which is bearish for energy, including oil and LNG. However, such measures if implemented, will be phased in over 3 years, assuming a safety report, due in June/July this year, suggests that a restart of Japan's nuclear power stations is “safe”. However, Japan like France, remains one of the most problematical of the major economies and is likely to remain so for years to come. Furthermore, a continuing decline and, indeed, aging population in Japan (the population declined by 212k last year, the 6th consecutive annual decline and will decline even faster in coming years), will limit the country's growth prospects. A number of analysts are particularly bullish on Japan. Whilst the short term rationale may be persuasive, I fear that such sentiment will prove to be relatively short lived. Japanese equity markets may outperform in the short term, though as we progress into H2 and as bond yields rise, (unless the BoJ truly buys a massive amount of bonds), well………. BRIC’s The Chinese services sector is also improving, coming in at 56.1 M/M in December, up from 55.6 in November. With a new regime in place and eager to achieve success, the Chinese economy should improve this year, which I believe will be reflected in their equity markets. Having been lower for most of last year, Chinese markets have rallied by over 15% over the last month or so, closing some 3.0%+ higher for 2012. I would not be surprised if the Shanghai Composite rallies by over 25% this year. Official GDP growth is forecast to increase above +8.0% this year. I have long dismissed official Chinese data – it simply cannot be accurate, as economic data, once announced, is never revised, which clearly is impossible. The short term trend, however, is certainly positive, as can be seen from the improvement in the residential housing market, both in terms of volume of sales and prices. I continue to believe that the Chinese economy is uncoordinated, unbalanced and unsustainable, as Premier Wen has admitted, in particular, in the medium to longer term. Until the last few months, I have been bearish of the Chinese economy for some 3 years and in due course, will continue to be. However, for the moment, I remain positive – the miners and US based China ETF’s are the way I play China. Political risks associated with territorial disputes in the South China Seas should not be ignored. In addition, there are some signs that the proliferation of “wealth management products”, sold to Chinese investors seeking higher yields could well prove a major problem – this practice could well be described as a major Ponzi scheme. In addition, the non-bank financial market, which is lightly regulated at present, poses serious risks. Chinese markets are driven more by political and policy issues and I will watch for any developments which could curtail the current positive market sentiment. In addition, inflation is at its lows and will rise in coming months. However, for the moment, I remain positive on China. India is facing an increasing budget, fiscal and current account deficit. Indeed, the current account deficit for the quarter ended 30th September 2012 came in at -5.4% of GDP, the highest for over 50 years. With general elections due next year, the new finance minister has introduced economic reforms which should help, but far, far more is necessary. At some stage this year, India is likely to lose its investment grade rating, a major problem for the country. For the moment however, foreign investment into Indian equity markets should continue, which suggests that the equity rally (currency hedged) should continue for a while longer. Inflation should decline from recent highs, as food and energy prices have a more benign effect, though I expect that the decline will prove to be temporary. Russia, well like all EM’s, the country is susceptible, in particular, to political and policy issues. Mr Putin has imposed further restrictions on his people in an attempt to curb opposition to his regime. These measures may work in the short term, but are unlikely to be successful in the medium, let alone the longer term. Yes Russian markets are extremely cheap, though in spite of not being totally energy based, move largely in relation to energy prices. Essentially, there are far more interesting opportunities around globally and I will continue to avoid Russia. Brazil, well the country faces increasing problems, due to being fundamentally uncompetitive. The Central Bank has cut interest rates to historic lows, which in my opinion is unsustainable, as inflation looks set to rise. Recent government policy measures suggest that the authorities are worried about growth, which has slumped to just around +1.0% recently – not at all great for an EM. The Real is looking fragile to say the least and the authorities have been supporting the currency to avoid an uncontrolled free fall. I believe that there are better opportunities elsewhere. Inflation Interest rates Market Outcome Equities Whilst, the recent strength of Japanese markets (currency hedged) should continue into Q1 and possibly H1 this year, I believe that Japanese markets will could well face headwinds as the year progresses. Of the BRIC's, I favour China and possibly India, certainly in the shorter term, and will avoid Russia and Brazil. In terms of sectors, my current views are as follows: I continue to like the US/UK financials, in particular, as I believe that the yield curve will steepen in both countries. Financials with investment banking exposure, in particular in the US, should outperform, as markets improve; Bonds However, post resolution of the US spending cuts/debt ceiling issue and the Italian elections, I believe that funds will start to rotate out of bond markets and into equities – indeed, there is a risk that they will do so earlier earlier. I am bearish on bonds. I will look to short US, UK, German and Japanese bonds this year, in particular, at the the longer end. French longer term bonds also look vulnerable, given the serious economic problems facing the country. Whilst the German economy will rebound, as will the US and the UK, Germany increasingly will have to share some of the burden facing the other EZ peripheral countries, in particular following the September general elections, suggesting that German yields will rise. Improving equity markets are also bond negative. Corporate debt in EM's look particularly vulnerable. Currencies Based on current and expected policies, the Yen looks like a continuing currency short in 2013, especially against the US$. Investors are likely to use the Yen as a funding currency (the Yen carry trade), which will weaken it even further. I would not be surprised if the Yen weakens to Yen 95 (quite possibly over Yen 100) against the US$ this year. US bond yields are set to rise, increasing the yield differential between US treasuries and JGB's. However, a restart of Japan's nuclear programme, together with a failure to force the BoJ to become more accommodative at its next policy meeting on the 22nd January, accompanied by the inability to appoint more dovish members onto the BOJ board, due to opposition by the Upper House, could limit the Yen's decline, I must admit – though such events look unlikely, in the main. A weaker Yen is the most likely outcome and will create material tensions in Asia, with a number of countries trying to devalue their currencies to compete. Korea's outperformance looks as if it will end. I have been amazed as to the performance of the A$ last year. Indeed, it was nearly the one currency that I lost money on during 2012. Fortunately I managed to close at break even, more by luck, following Mr Boehner’s failure of his plan B, which strengthened the US$ against the A$. The Australian authorities have abandoned their policy of achieving a balanced budget. The RBA, which has been particularly slow in easing, should continue to cut interest rates by up to 100 bps this year – most likely between 50 bps to 75 bps. Investment into the mining sector has peaked, as will employment in coming months, though base metal prices have risen in the last few months admittedly and there is some evidence that recent capex cutbacks will be reversed. China will grow, but the previous obsession with fixed asset investment will be limited. The strong A$ is hurting the non mining side of the Australian economy, which shows continued signs of contraction. I remain bearish of the A$ and believe that it will depreciate to A$0.95 or below to the US$ during the year, though in the short term, the A$ could well rise to US$1.06 to US$1.08. Essentially, I believe that 2013 will be the year for US$ outperformance against virtually every currency. Commodities I must admit that I have always been far too bearish on oil prices in the past. Brent has been remarkably resilient, trading around US$110 in recent months, though (ex geopolitical issues) I believe that Brent will will decline to between US$100 to US$105 over the next few months. The risks however are that prices will rise to closer to US$110 to US$115 in H2 this year, as the global economy improves. Indications that Japan could restart its nuclear programme (the report from the safety committee is due in June) may prove constraint on oil prices, however. Base metal prices (iron ore) are up over 50% in the last 3 to 4 months, a move which has gone largely unnoticed. Indeed, an Australian mining company (Fortescue) has resurrected its previously postponed capex programme. I have been long the base metal miners (closed just recently), though am likely to reinvest in the sector this year. However, the rise in iron ore prices seems overdone and normally a stronger US$ is negative. I do not believe that inflation will be a problem, especially in H1 of this year and, in particular, in DM’s. As a result, with improving growth in DM’s, I really do not see gold prices rising, ex any geo political issues. Furthermore, the latest FED minutes, which suggest that QE could be reduced, indeed stopped, in H2 this year is US$ positive, which generally is negative for gold. However, I have never understood or, indeed, really ever traded gold. Risks The new Japanese government is pressing the BoJ to increase its inflation target to 2.0%, whilst it will increase fiscal stimulus. At present, Japanese equity markets (on a currency hedged basis) have responded positively to the policy measures announced and should continue to do so. However, with debt to GDP of over 220%, higher inflation will increase interest rates, which Japan can ill afford. Sure, the Central Bank will buy more Japanese bonds, quite probably of longer maturities, which could temper the rise in yields. However, with a massive budget deficit, which will increase due the proposed fiscal stimulus, yields on longer dated bonds, in particular, should rise. Japanese investors (in particular financial institutions) have been major purchasers of Japanese bonds in the past – will they in the future?, in particular given their massive existing holdings – I have my doubts. Who will finance Japanese borrowing requirements, especially as Japan is facing a current account deficit? Outlook Markets globally closed 2012, with respectable gains. Negotiations over spending cuts/raising the debt ceiling in the US, over the next 2 months, could well impact markets negatively. However, on balance, I remain positive on equity markets for 2013 and will want to be long, though short term may well take profits, ahead of what is likely to be a particularly tough and noisy public squabble between Republicans and the Democrats over spending cuts and the need to raise the debt ceiling. Experience has taught me to never underestimate the ability of politicians to create problems. Given the significant level of cash held by companies at present, M&A activity should pick up this year and corporate buybacks should increase. Both market supportive. Better markets may also result in companies seeking to raise equity capital, in particular in H2 this year. Above all, I believe that there will be a rotation out of bonds and into equity markets this year. In addition, I believe that the US$ will strengthen against all the major currencies this year. As the year progresses I will continue to favour the financials (US/UK), base metal miners (UK/US), builders (UK) and building materials (US/UK), industrials (German/US), IT/technology (US), property companies (US/UK – London based) and China (US ETF). However, in the shorter term, I will look to reduce my equity exposure, given the likely political problems in the US in respect of the spending cuts/debt ceiling issues. In due course, I may look at the energy sector, (which I am not convinced about at present) and retail, which I believe has greater potential. I remain of the view that these are trading, rather than buy and hold, markets. Kiron Sarkar 5th January 2013 |

| Employment/Unemployment Pictures Posted: 05 Jan 2013 08:00 AM PST click for larger graphics All charts courtesy of Bianco Research except as noted

Source: Bianco Research |

| Posted: 05 Jan 2013 05:00 AM PST

The unusual form seen here is the result of a cosmic collision with a smaller galaxy which plunged right through the heart of the larger and shot out the other side. As the smaller galaxy passed through the middle it set up gravitational ripples that disrupted the clouds of gas and triggered the formation of new stars whose radiation then lit up the remaining gas. Source: hubblesite.org via Buzzfeed |

| Posted: 05 Jan 2013 04:00 AM PST Welcome to the first weekend reads of the new year — these are our favorite longer form reads from over the past week (or so). Pour a cup of coffee, settle into the comfy couch, and enjoy:

What are you up to this weekend?

How Much Will Your Taxes Jump? |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment