The Big Picture |

- Succinct Summations of the Week (10/18/13)

- Shiller: U.S. Stocks Are ‘Highly Priced’

- A Wonderful Circus

- 10 Friday AM Reads

- Updated Schedule of BLS News Releases

- Tax Rates, Inequality, and US Deficits

- IMF Fiscal Monitor: Taxing Times

- Art of the Automobile

- Puerto Rico

| Succinct Summations of the Week (10/18/13) Posted: 18 Oct 2013 12:30 PM PDT Succinct Summations week ending October 18, 2013. Positives:

Negatives:

Thanks, Batman |

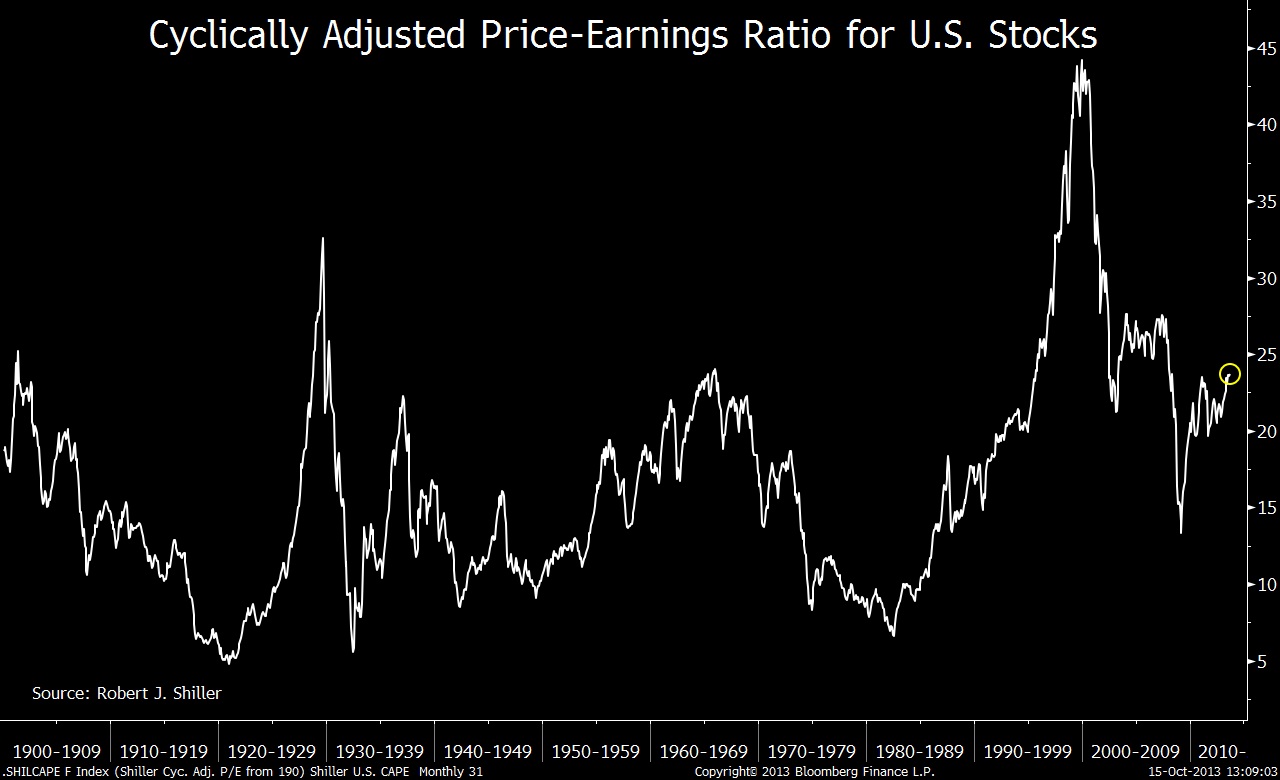

| Shiller: U.S. Stocks Are ‘Highly Priced’ Posted: 18 Oct 2013 10:00 AM PDT Shiller's cyclically adjusted price-earnings ratio

Robert J. Shiller, a co-winner of this year's Nobel Prize in Economic Sciences says US stocks are expensive. They are the most expensive relative to earnings they have been in more than five years — since the lows follwoing the great collapse of 2007-09. Shiller's CAPE ratio — the cyclically adjusted price-earnings ratio — compares the Standard & Poor's 500 Index with companies' average profits over the prior decade. The ratio ended last month at 23.7, the highest since January 2008, according to data available from his website. Bloomberg notes that “the September ratio was lower than a peak of 27.5 in May 2007 — and even further below a record of 44.2, set in December 1999.” Date for Shiller's price-earnings figures go all the way back to 1881 (above chart 1900 – present). Shiller made several other comments on equities:

A far cry from his prior warnings of dot com stocks in 1999 and housing in 2006. The CAPE ratio was developed by Shiller and Harvard University professor, John Y. Campbell.

Source: |

| Posted: 18 Oct 2013 09:00 AM PDT Thats how the FT’s delightful Martin Wolf described the recent silliness in Washington DC:

Click for video |

| Posted: 18 Oct 2013 07:00 AM PDT My morning reading:

What are you reading?

Abe gets ready to start “naming and shaming” |

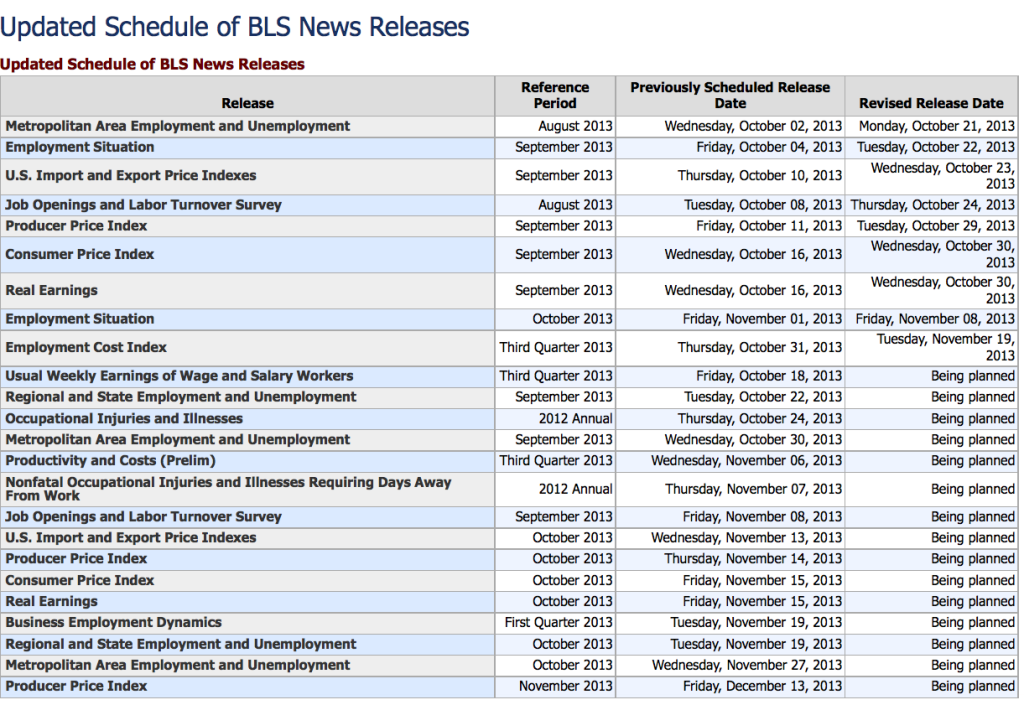

| Updated Schedule of BLS News Releases Posted: 18 Oct 2013 06:00 AM PDT The shutdown is over. Now BLS can back to the business of releasing data that I will mostly ignore.

click for updated release schedule

|

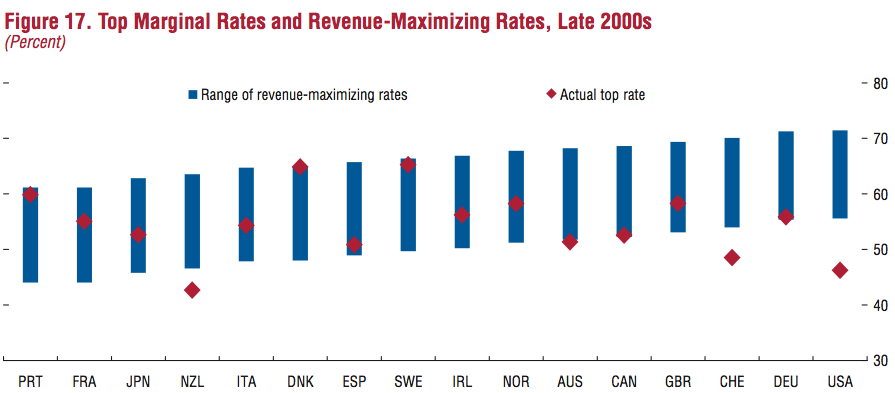

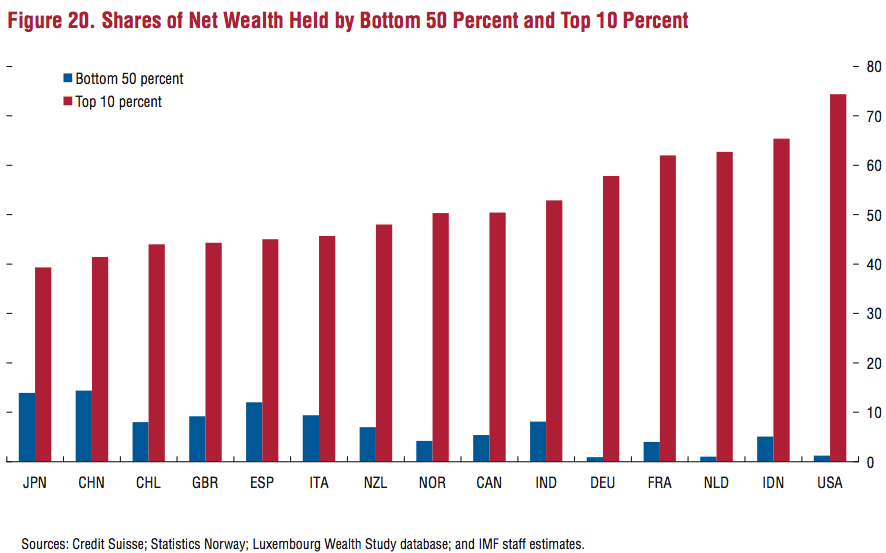

| Tax Rates, Inequality, and US Deficits Posted: 18 Oct 2013 04:45 AM PDT Its Friday, after what was for me a long and annoying 17 days. But the shutdown is over, US markets are at all time highs, and Bob Shiller got his Nobel (more on this tomorrow). You might think that I would be at peace with the current state of the world, but life is never that simple. You see, I have assumed the task of explaining things which require explaining. By some quirk of fate and an odd academic background, I find myself with skills in simplifying complex matters. Whether OCD or over-compensation for some other defect, this is my lot in life. (I made peace with it long ago). As we discussed yesterday, amongst all of the background nonsense since October 1, the noise about the deficits was not really about budget deficits at all. Rather, it was about a decidedly narrow ideology held by a small percentage of Americans. Their belief is that government should be much smaller. This is a legitimate political ideology, one that has persisted over the centuries. Their approach to this philosophy, however, is far less intellectually honest. Rather than having a full on debate on that subject — a debate they are likely to lose — they have chosen a very different approach. This time around, they made the deficit a proxy. Because of what I do for a living, I found this offensive. Deficits impact fixed income, an important part of portfolio planning. They impact available credit, capital for investment, in a broad and varied way. Hence, the deficit is a genuine issue, a real problem that should be addressed in a mature and responsible way. It can be easily solved using intelligent solutions, but for the ideologues in Washington DC (and elsewhere) who refuse to treat it as the basic mathematics and accounting problem it actually is. The way the Tea Party and others have treated the deficit reminds me of the approach Meredith Whitney took to Municipal Debt. Both groups are stunningly ignorant about their subjects, while possessing the skills to allow them to exploit the topic, hog the spotlight for themselves and other tangential pet issues. The Tea Party, like Whitney, turned an important question of debt and credit and solvency into one giant PR clusterfuck. Back to our issue of taxes (next week, I will address spending). Amongst Industrialized Nations, the United States has amongst the lowest tax rates in the world, especially for those folks (like myself) who reside at the top of the income scale. To demonstrate this, I want to point to the IMF’s World Economic and Financial Surveys: Taxing Times. It is chock full f great charts and data and other interesting results of the IMF survey. The two below caught my eye. They are rather instructive for our discussion of taxes and deficits in the US. The first looks at major industrial nations, and compares what the IMF calls their Revenue-Maximizing Tax Rates (blue line) versus their actual top rate (red dot). As you can see, some countries — Denmark and Sweden — are at the top of the revenue maximizing ranges. Other countries — Canada and Germany — are at the bottom of their revenue maximizing ranges. Then there is the United States, which is simply far off the scale, way below the bottom of its revenue maximizing range. If your concern is deficits, than you must take notice of how much money the USA is leaving on the table. I am not suggesting that the role of government should be to maximize their tax revenues, but rather to suggest that if you want to close the deficit, you need to at least be in a defendable range. The US is not.

Not coincidentally, when we look at shares of Net Wealth held by the bottom 50% of he population versus the top 10%, the United States is off the scale. We are the most unequal nation in the world.

The inescapable conclusion presented to us by this data is that our tax policy is responsible for both the world’s greatest inequality among developed nations, and our ongoing deficits. If you have a better explanation for our current conditions, or the net results of our tax policies, I would love to hear it.

Source: |

| IMF Fiscal Monitor: Taxing Times Posted: 18 Oct 2013 04:00 AM PDT World Economic and Financial Surveys

Persistently high debt ratios in advanced economies and emerging fragilities in the developing world cast clouds on the global fiscal landscape. In advanced economies, with narrowing budget deficits, the average public debt ratio is expected to stabilize in 2013–14—but it will be at a historic peak. At the same time, fiscal vulnerabilities are on the rise in emerging market economies and low-income countries—on the back, in emerging market economies, of heightened financial volatility and downward revisions to potential growth, and in low-income countries, of possible shortfalls in commodity prices and aid. Strengthening fiscal balances and buttressing confidence thus remain at the top of the policy agenda. Against that backdrop, this issue explores whether and how tax reform can help strengthen public finances. Taxation is always a sensitive topic and is now more than ever at the center of policy debates around the world. Can countries tax more, better, more fairly? Results reported in this issue show that the scope to raise more revenue is limited in many advanced economies and, where tax ratios are already high, the bulk of the necessary adjustment will have to fall on spending. In emerging market economies and low-income countries, where the potential for raising revenue is often substantial, improving compliance remains a central challenge. |

| Posted: 18 Oct 2013 03:00 AM PDT Art of the Automobile : 21 November 2013 RM Auctions in association with Sotheby's will present a select offering of motor cars to celebrate the historic importance of the automobile—a singular achievement at the crossroads of art, technology, and innovation. Click to enlarge

Source: RM Auctions |

| Posted: 18 Oct 2013 02:00 AM PDT Puerto Rico

Some readers saw the Barron’s front-page article on Puerto Rico and its financial problems. The details of the debt burdens of Puerto Rico make for an ugly picture. Puerto Rico bonds are ubiquitous. They are tax-free in all state jurisdictions because of the particular nature of Puerto Rico’s territorial commonwealth status. Many mutual funds hold (or held) them because they can be placed in state-specific funds and in more general funds. We have seen five months of mutual fund liquidation pressure, which originated in part with Puerto Rico credit risk. The pressure was exacerbated by tapering talk from the Federal Reserve and again intensified with the federal political impasse. Other credit-related events such as Detroit’s bankruptcy added fuel to the liquidation fire. Where do we stand now? The Puerto Rico Commonwealth debt obligations are rated Baa3 by Moody’s, BBB- by Standard & Poor’s, and BBB- by Fitch. Some other securities issued by Puerto Rican agencies are below investment grade. The ratings just recited are the lowest of the low investment grades. Market-based pricing in Puerto Rico debt reflects market perceptions of imminent cash exhaustion. We see PR bonds that are backed by Assured Guaranty, the US bond insurer, trading at yields close to 7%. We see uninsured, unenhanced Puerto Rico credits trading at double-digit yields. And we see short-term Puerto Rico debt trading at annualized yields well into double digits. The market is saying that Puerto Rico could run out of cash. This market-based pricing suggests that Puerto Rico could default, declare some legal action, or otherwise jeopardize the payment stream to bond holders. We think that is a very serious risk. Market based pricing suggests that PR will not easily "roll" its maturing debt. The political questions surrounding Puerto Rico are equally complex. Puerto Rico is a sovereign commonwealth; it is not a state or city. It has never held a vote to support an application for statehood in the US. Puerto Rican residents do have US citizenship status. If Puerto Rico were to bankrupt or default and then try to achieve statehood in the US, would it be accepted? There is no reference in American history regarding the legal status of a territorial jurisdiction like Puerto Rico seeking direct assistance and federal guarantees under conditions like these. PR has benefitted by many special tax treatment related subsidies in the IRS code. Additional serious political questions arise out of the imbroglio currently playing out in Washington, DC. If the federal government does not inject money into a city like Detroit, Harrisburg, or Stockton, would that same federal government use the US credit to support the refinancing of Puerto Rican debt? All of the political questions involving Puerto Rico are profound and their answers highly uncertain, but we believe that a bailout of Puerto Rico is unlikely in the present political environment in Washington. Cumberland has not taken any positions in Puerto Rico that are in unenhanced credits. We have avoided them. When clients hold them in accounts that come in, we attempt to sell them, and those sales are increasingly difficult. We have held Puerto Rico bonds that are pre-refunded: that means they are secured by an escrow of US Treasury obligations. And we have held bonds that are guaranteed by Assured Guaranty, Inc. AG is rated favorably by both Moody’s and Standard & Poor’s. Would we buy new bonds in Puerto Rico if they were insured? The answer is, probably not. And we doubt that insurers would take on more PR risk. Would we buy any of the unenhanced Puerto Rican debt or standalone credit? The answer is, definitely not. In contrast to a separate-account manager such as Cumberland Advisors, the mutual fund manager faces an acute difficulty. Let me describe it in the following way. A mutual fund manager has a collective fund of tax-free bonds and may be facing shareholder redemptions. That means the manager must sell, raise cash, and pay the shareholders on demand. If the manager owns some Puerto Rico debt and must sell it, enormous losses will be taken, because the pricing of that debt is as I have described. There is no longer the ability to easily sell Puerto Rico debt. So what can be sold by the fund manager instead? The highest-grade, most liquid, and easily traded securities can be sold. However, if mutual fund A is facing redemptions, it is likely that mutual funds B, C, D, and E are also facing them. So the natural buyers for the bonds held by A become sellers instead, just like manager A is a seller. The end result is wholesale selling, and the selling by mutual funds is across the board, not idiosyncratic to one fund. Who is on the buy side? Only separate-account managers who can cherry pick the offerings. That is what we do. We look at bid-wanted lists. The bids we give are bids that we think are bargain bids for bonds that we know we want to buy for our clients. Do we see Puerto Rico bonds offered? Yes, of course. They are distressed sales coming from institutions that are under pressure. That is the time when a separate account can be opportunistic. Taking advantage of opportunities is what we try to do, but only when we believe those opportunities will pan out. We seriously question whether Puerto Rico can make it. There are arguments being put forth about using casino revenues, sales tax revenue, and other collateral to secure financing. We are skeptical. We think the commonwealth is facing huge difficulty in rolling over their maturing debt. The climactic Puerto Rico chapters of the municipal bond book are being written now. We advise reading and watching with professional interest. But we do not advise owning Puerto Rico. We want to offer some special thanks to Natalie Cohen, Head of Municipal Research at Wells Fargo Securities, for her excellent work in the municipal bond arena and specifically on Puerto Rico. We also want to note that the slides and presentations made at the October 10-11, 2013, Global Interdependence Center conference in Bermuda are now posted on the GIC website, www.interdependence.org. Included in those presentations and slides is an entire section on municipal debt. It includes comments about Detroit, among other jurisdictions, and references Puerto Rico. The participants in the first session on cities were Peter Gold of the Peter Gold Group, Mary Francoeur of Assured Guaranty, and Dennis Archer, former mayor of Detroit. The second session was moderated by my colleague John Mousseau and included presentations by Catherine Mann of Brandeis University and Robert Kurtter of Moody’s Investors Service. Those presentations focused on municipal credit and the issues of cities – whether they can be saved, how they can be saved, and the mechanics of municipal finance. I can report to you that during those two sessions that morning, the attendees were very attentive and strongly responsive to the information that was presented. In fact, I would say that people were riveted. We encourage readers to view those presentations. In some cases, new data was presented that had not previously been broadly shared in an open-forum conference. ~~~ David R. Kotok, Chairman and Chief Investment Officer, Cumberland Advisors Cumberland Advisors |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment