The Big Picture |

- The Recent Boom in House Prices: Why Is This Time Different?

- NSA’s “Lone Wolf” Justification for Mass Spying

- 12/15/13 Week in Review/Preview

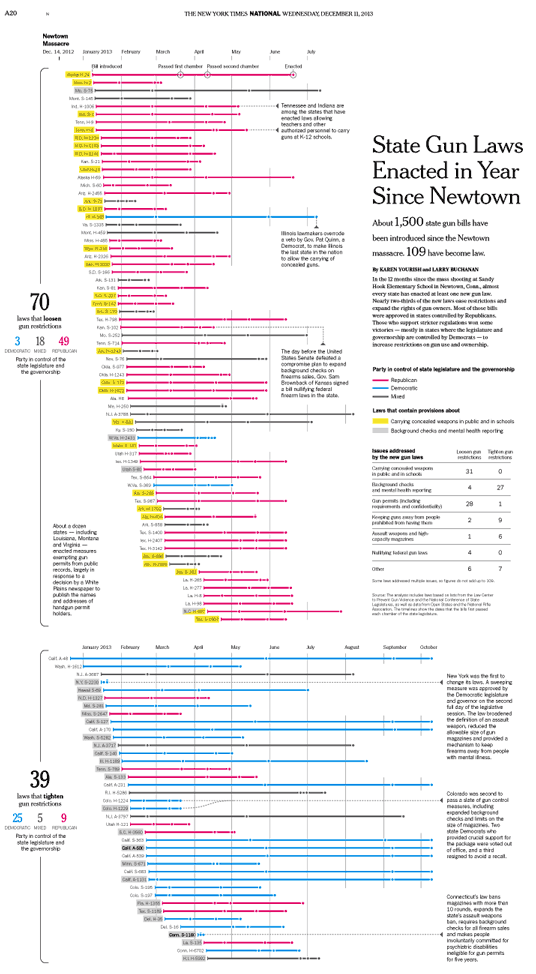

- State Gun Laws Enacted in the Year Since Newton

- What Is the Right Amount of Cash In Your Portfolio?

- 10 Sunday AM Reads

- Carl Zimmer: How did feathers evolve?

- Crowding In – Bond Interest Rates

- Is (Risk) Sharing Always a Virtue?

| The Recent Boom in House Prices: Why Is This Time Different? Posted: 16 Dec 2013 02:00 AM PST |

| NSA’s “Lone Wolf” Justification for Mass Spying Posted: 15 Dec 2013 10:30 PM PST All of the Chairs of the 9/11 Commission and the Congressional Investigation Into 9/11 Say It's "Implausible" that the 9/11 Hijackers Acted Without Government Backing.The NSA's main justification for Constitution-shredding mass surveillance on all Americans is 9/11. In reality:

But we want to focus on another angle: the unspoken assumption by the NSA that we need mass surveillance because "lone wolf" terrorists don't leave as many red flags as governments, so the NSA has to spy on everyone to find the needle in the haystack. But this is nonsense. The 9/11 hijackers were not lone wolves. The former Chair of the Senate Intelligence Committee, outside adviser to the CIA, and Co-Chair of the congressional investigation into 9/11 – Bob Graham – says:

Indeed, Graham – unlike with 9/11 Commissioner and former Senator Bob Kerrey – said in sworn declarations that the Saudi is linked to the 9/11 attacks. They're calling for either a "permanent 9/11 commission" or a new 9/11 investigation to get to the bottom of it. An FBI report implicates the Saudi government. And many other top U.S. counter-terrorism officials say that the government's explanation of the 9/11 hijackers being "lone wolves" connected only to Al Qaeda is ridiculous. See this and this. If this sounds implausible, remember that Saudi Prince Bandar – head of Saudi intelligence – helped to arm the Mujahadeen in Afghanistan, and is now arming Al Qaeda in Syria. (Background). Respected financial writer Ambrose Evans-Pritchard says that Prince Bandar admitted that Saudi Arabia carries out false flag terror. Indeed, the Joint Congressional Inquiry into 9/11 found that the Saudi government supported the 9/11 attacks, but the Bush administration classified the 28 pages of the report which discussed the Saudis. Bipartisan Bill to Publicly Release Report on Saudi Involvement In 9/11A bipartisan bill – introduced by congressmen Walter B. Jones (Republican from North Carolina) and Stephen Lynch (Democrat from Massachusetts) would declassify the 28 pages of the Joint Inquiry which implicate the Saudi government. Some assume that passage of the bill is assured … But both the Bush and Obama administrations have fought to keep Saudi involvement under wraps for more than 10 years. Remember, the U.S. government allowed members of Bin Laden's family – and other suspicious Saudis – hop on airplanes and leave the country right after 9/11 without even interviewing them, even though air traffic was grounded for everyone else. Additionally, a Saudi FBI informant hosted and rented a room to Mihdhar and another 9/11 hijacker in 2000. Investigators for the Congressional Joint Inquiry discovered that an FBI informant had hosted and even rented a room to two hijackers in 2000 and that, when the Inquiry sought to interview the informant, the FBI refused outright, and then hid him in an unknown location, and that a high-level FBI official stated these blocking maneuvers were undertaken under orders from the White House. As the New York Times notes:

The government obstructed the 9/11 Commission in every way possible. During both the Joint Congressional Inquiry into 9/11 and the 9/11 Commission investigation, government "minders" intimidated witnesses and obstructed the investigation. Obama has been no better. Obama's Department of Justice filed an amicus brief in the U.S. Supreme Court arguing that the lawsuit brought by the families of victims killed in the 9/11 attacks against Saudi Arabia should be thrown out of court (it was). And Graham said that he's lobbied Obama for years to release the 28 pages and to reopen the investigation, but Obama has refused. The former Chair of the Senate Intelligence Committee and 9/11 investigator has even resorted to filing Freedom of Information requests to obtain information, but the Obama administration is still stonewalling:

Still Urgent TodayAncient history, you say? Graham notes:

For example, the U.S. might not want to support – let alone launch joint military adventure alongside – a regime which supported the 9/11 hijackers. As Graham told told PBS last year:

And – most importantly – if the entire mass spying program is based on the "lone wolf" theory of 9/11, it is unnecessary and counterproductive. Postscript: Ironically, the U.S. government has in the past alleged state sponsorship of 9/11 when it suited its purposes. Specifically, people may not remember now, but – at the time – the supposed Iraqi state sponsorship of 9/11 was at least as important a justification for the Iraq war as the alleged weapons of mass destruction. This claim that Iraq is linked to 9/11 has since been debunked by the 9/11 Commission, top government officials, and even – long after they alleged such a link – Bush and Cheney themselves. But 70% of the American public believed it at the time, and 85% of U.S. troops believed the U.S. mission in Iraq was "to retaliate for Saddam's role in the 9-11 attacks." |

| 12/15/13 Week in Review/Preview Posted: 15 Dec 2013 02:00 PM PST Set out below is a summary of some of last weeks key events. House and Senate leaders agreed a budget deal which will establish spending levels over the next 2 years. In addition the agreement amends some of the automatic spending cuts caused by the sequester. Whilst the deal was modest in size, it does enable the government to function without the constant political fighting that has been the case recently. The House ratified the deal and the Senate is expected to do so next week. The debt ceiling will have to be increased early in the New Year. US regulators approved the Volcker rule which essentially is designed to prohibit banks from proprietary trading. Banks will still be able to take positions to enable them to carry out their market making activities. CEO's of banks will be more accountable for the banks activities. The key will be the interpretation of the rules by regulators. A number of FED speakers, even those deemed dovish, talked about the tapering programme starting soon. The FED meets next week and a number of analysts believe that it will announce the start of tapering at that time. The size and mix of the tapering programme will be important, with the FED likely to focus more on Treasuries rather than mortgage backed securities, at least initially. In terms of the US economy, retail sales came in better than expected with a rise of +0.7% in November, higher than the upwardly revised +0.6% in October. Core sales, a figure which is used to calculate GDP, were up +0.5%. The buoyant market, combined with lower fuel prices and increased employment has improved confidence of US consumers. Business inventories rose by +0.7% in October, higher than expected. The rise in inventories will ease fears that Q4 GDP will come in much lower, as high inventory levels in Q3 are wound down. Disinflationary forces continue to be evident with producer prices declining by -0.1% in November, lower than the unchanged level expected. The job openings data improved, with vacancies up to a 5 year high. This number is important as it is a data point which the next FED Chairperson, Mrs Yellen looks at. Housing data continues to improve, with foreclosures at a near 8 year low, though I expect that residential home prices will moderate next year. In general, the data confirms that the US economy is improving. Unlike the US, European data was poor. October Industrial output in the eurozone (EZ) came in at -1.1% M/M, much worse than the rise of +0.3% expected. German industrial output declined for the 2nd consecutive month – it was down by -1.2% M/M, worse than the decline of -0.7% expected and the -0.7% in September. French industrial output declined by -0.3%. The only surprise was Italy, which posted an increase of +0.5%. Analysts report that the data implies that Q4 GDP expectations will have to be revised lower to possibly just +0.2%. Over the weekend, SPD members voted overwhelmingly to back a coalition with Mrs Merkel’s CDU party. At least Germany has a new government in place. Importantly. Mr Schauble, will remain as Germany's finance minister. Many have thought that the grand coalition will be more EZ friendly, but comments from the SPD suggest that Germany will continue with its previous policies in respect of the EZ. EU finance ministers announced a series of measures which eventually will lead to a banking union. However, the measures announced are far from ideal. A fund is to be created over a period of 10 years, paid for by levies on banks. However, the use of this fund to provide mutual support for banks is to be phased in over the 10 year period. In the interim, individual countries will continue to responsible for their banks. In other words, the link between the financial sector and the Sovereigns continues. Larger EU countries will have more of a say. Furthermore, the decision making process to deal with problem banks is far from clear cut. Essentially, countries conceded to German demands. The finance ministers also agreed to a common set of rules to deal with failed banks, which will come into effect from 2016, 2 years earlier than planned. Bail-in rules at that time will force bondholders and large depositors to take a hit. The ECB is in the process of conducting an asset quality review and stress tests in respect of the largest banks, with the results due by November next year. Mr Draghi reiterates that the criteria will be credible. Some banks are very likely to fail the tests. How are these banks to be recapitalised?. It is unlikely that the private sector will provide all the funding that will be necessary and the deal agreed by the European finance ministers does not provide the backstop necessary. A number of countries lack the resources to provide the support necessary. Furthermore, members of the ECB have suggested that banks will no longer be able to use cheap funding from the ECB's LTRO operations to buy sovereign bonds. One of the ideas proposed by ECB representatives is that sovereign debt will no longer be treated as zero risk – in other words banks will have to reserve capital against their positions. The logical conclusion is that banks will stop buying and/or reduce their holdings of sovereign bonds, thereby increasing rates. Furthermore, banks will be deleveraging their balance sheets in anticipation of the ECB's stress tests. The net impact is that the availability of credit will be reduced in the EZ and that sovereign yields rise. This is a serious issue and one which could well have a material negative impact on the EZ. To alleviate some of the potential problems, the ECB has stated that it will provide liquidity to banks, in particular to lend to SME's – a funding for lending scheme, as introduced by the Bank of England, may be announced. However, the risks are high, in particular given the weak EZ economy. UK economic data continues to improve. Manufacturing activity has risen, as has construction activity. The services sector, the most important in respect of the UK, remain strong. Unemployment is declining and the market expects interest rates to rise sooner than otherwise thought. The Bank of England (BoE) remains concerned about the increase in property prices, with the house price index rising to the highest in a decade in England and Wales. At some stage, I would not be surprised if the BoE takes measures to try and limit price rises. The British Chamber of Commerce (BCC) has increased its forecast for 2014 GDP to +2.7%, up from +2.2% previously. Importantly, the BCC forecasts that business investment will increase to well over 5.0% in 2014 and 2015 – in the past business investment in the UK has been a problem. The risk to the UK remains the EZ. Japanese calendar Q3 GDP was revised lower to an annualised rate of +1.1%, down from +1.9% previously. Lower investment and inventories were cited as the main reasons. Japan's current a/c declined unexpectedly to a deficit of Yen 127.9bn in October – a surplus of Yen 150bn was expected. Continued current account deficits will pose a serious threat to Japan. Mr Kuroda, the governor of the Bank of Japan (BoJ) stated that the BoJ will continue with its highly expansionary monetary policy until inflation reaches their 2.0% target – the BoJ core inflation rate, which the BoJ targets, is currently +0.9%. However, much of this inflation is due to the increase in Yen terms of imported goods, in particular energy, as the Yen has declined. His comments suggest that the BoJ may well increase its purchases of Japanese bonds and that the ultra easy monetary policy will remain in place for longer than the 2 years initially stated. There is still very little sign that Japanese companies are increasing wages – indeed, the latest data reveals that wages are declining. If this trend continues domestic consumption will decline. I remain highly sceptical of Abenomics and the BoJ policy. Chinese exports rose by +12.7% Y/Y in November, much higher than the rise of +7.0% expected. However, the data is suspect. A number of neighbouring countries reported either flat or marginally lower exports. The much higher than expected export data may actually be capital inflows disguised as exports, as interest rates have increased as a result of actions by the Central Bank (PBoC) and the Yuan has strengthened. Furthermore, industrial production came in marginally lower, which also casts doubt on the export data. Imports rose by just +5.3%, lower than the 7.0% forecast. Inflation was lower than expected at +3.0%, down from 3.2% in October. Retail sales were up +13.7% in November, higher than the +13.3% in October. The PBoC has been trying to limit lending. However, aggregate lending rose by Yuan 1.23 tr, much higher than Octobers Yuan 856.4 bn. Property prices continue to rise, in spite of government policies to limit increases. Recently, the Chinese government announced a number of reforms designed to make the economy more market based. The fear is that a number of vested interests would block these reforms and, in addition, that the Chinese bureaucracy would move very slowly to implement the reforms. As a result, the Chinese government announced that it would withdraw certain powers from a number of central government ministries, including the powerful National Development and Reform Commission. The government also announced that it would strengthen scrutiny of local government financing. In the past local governments have increased spending materially, with the true level of outstanding debt unknown. They added that individuals in local governments would be punished for decisions which resulted in either incurring large losses or for wasting resources or causing environmental damage. The National Audit Office has yet to release details of the level of debt incurred by local governments – some analysts estimate that it could amount to between US$ 2.5tr to US$3.0tr. Over the weekend, the Chinese leadership stated that they would tackle the issue of local government debt next year. Furthermore, there is some speculation that the growth forecast may be reduced to 7.0%, from 7.5%. Overview Whilst the US and UK economies continues to improve, I believe that the EZ and Japan face significant problems next year. For the reasons stated above, the problems in the European banking sector are likely to flare up again. With banks cutting back on lending to meet the ECB's stress tests, credit will be restricted, adding further pressure on the region. Furthermore, inflation in the EZ is likely to remain low and may even drift lower. Indeed, other than in emerging markets, disinflationary forces seem to be continuing. The ECB, at some stage, will have to act. The BoJ's statements suggest an increase in QE next year from its already lofty levels. The risks relating to Japan are rising, in particular if its current account remains in deficit. The Yen and the A$ continue to weaken and I believe that the Yen is likely to depreciate even further. The governor of the Australian Central bank, the RBA, continues to talk down the A$. Recently, he has raised the prospect of intervention and has even suggested that a level of US$0.85 would be more appropriate – the A$ is currently trading at just below US$0.90. The Euro strengthened to around US$1.38, but has declined to closer to US$1.37. I continue to believe that the Euro will have to weaken against the US$ next year – the EZ cannot live with this rate. I remain a US$ bull for next year. I expect that volatility will rise in 2014. The VIX which was trading around 12 has risen to around 15 in just a few weeks. Whilst there may well be the traditional rally into the year end and early next year, I remain cautious. I continue to believe that the risk profile of equity portfolios should be reduced at the very least. Kiron Sarkar |

| State Gun Laws Enacted in the Year Since Newton Posted: 15 Dec 2013 01:00 PM PST

|

| What Is the Right Amount of Cash In Your Portfolio? Posted: 15 Dec 2013 07:00 AM PST

> This is yet another column that looks like its about investing but really is about psychology. As I noted prior, people have been sitting on big piles of cash this entire rally, and missed a huge opportunity to rebuild after the crisis. Here’s an excerpt from the column:

Food for thought . . .

Source: |

| Posted: 15 Dec 2013 05:00 AM PST Good Sunday morning, a kickstarter for your mind while you enjoy that second cup of coffee:

Whats for Brunch?

Women Now Head 4% of Fortune 500 Companies

|

| Carl Zimmer: How did feathers evolve? Posted: 15 Dec 2013 03:30 AM PST To look at the evolution of modern bird feathers, we must start a long time ago, with the dinosaurs from whence they came. We see early incarnations of feathers on dinosaur fossils, and remnants of dinosaurs in a bird’s wish bone. Carl Zimmer explores the stages of evolution and how even the reasons for feathers have evolved over millions of years. How did feathers evolve? – Carl Zimmer Hat tip Brain Pickings |

| Crowding In – Bond Interest Rates Posted: 15 Dec 2013 03:00 AM PST Crowding In – Bond Interest Rates

We are watching bond market volatility as Treasury bonds struggle with questions about what the Fed (Federal Reserve) is going to do. Only the passage of time and improvement of communication from the new Fed leadership will resolve this issue of inadequate clarity and resulting volatility. At the same time, we are aware that the federal deficit is shrinking. The pressure of new Treasury bond issuance is falling all the time. Markets tend to ignore this trend in the short run. In the longer run and in the past, with the federal government "crowding out" other borrowers, having to sell more bonds put more pressure on markets. The fewer bonds there are to be sold, the less pressure there is on markets. This is called "crowding in" and is a characteristic that market agents have forgotten after the recent and long period of high deficits in the United States. In 2014, governmental crowding in has arrived in force. Its influence will be felt in markets. Coupled with restrained state and local budgets, we now have a shrinking federal deficit that is now headed under 3% of GDP and trending lower. This is a very powerful force against rising bond yields. Greg Valliere, an expert observer of Washington, DC, politics and the dynamics of our political system, described the shrinkage of the deficit as follows: "The first two months of the fiscal year look spectacular. Data released yesterday by the Treasury Department show the deficit down by 22% compared to the first two months of last year, with receipts up by 10% to $362 billion. Cynics respond that about $30 billion of that total comes from Fannie and Freddie, which are pumping profits back to the government." When I asked Greg for more detail about the GSE share, Greg offered this addition about "the enormous one-time tax break of about 20 billion that grossly affected the GSE contribution": "Both Fannie and Freddie will continue to contribute to the Treasury, but not at the Oct.-Nov. pace." Many thanks to Greg Valliere for giving us permission to share this insight. We think Greg is right in his assessment that the falling deficit will persist. We believe it will be a force throughout the rest of the Obama term. It is quite possible that the deficit could decisively dip under 3% of GDP and even approach 2% or 2.5% of GDP. That will be a remarkable event. It will happen at the same time that the pressures on the housing agencies and mortgage finance entities are diminishing. All this coincides with rising house prices and the gradual recovery of our economy. As a nation we find ourselves on the benign recovery side of the pain that convulsed the economy during the financial crisis. In sum, the new-issuance pressure of bonded indebtedness at all government levels is not intense and not of the nature to drive up interest rates. Instead we have crowding in, not crowding out. Meanwhile, the issue of inflation is being ignored by bond investors. The headline personal consumption expenditure deflator is falling. Market-based priced Core PCE is falling even more. It is trending under 1%. Core CPI is also falling. Producer Price inflation is trending at about 1%. In fact, the case can be made that the collective indicators of price level changes could all trend under at or near 1% sometime in 2014. The real interest rate in the bond market (after inflation is removed from the calculation) rises when the anticipated or measured rate of inflation falls. As we know, over time, it is the real interest rate that counts. Rising real interest rates have a slowing effect on economic activity. Falling or lower real interest rates spur economic activity. Presently, with inflation rates not widely accepted as accurate by market players but trending lower and bond interest rates not widely accepted as bargains by market players but trending higher, a possible collision course or tension between the two indicators results. That tension could slow the pace of economic growth, and any such slowing could and would lead to a subsequent robust rally in bonds. What bonds to buy, what bonds to hold, and what bonds to sell? When should they be swapped? These are the conundrums investors face. Fortunately, there are good answers to be found. We have long said that the tax-free, high-grade bond sector is cheap relative to other bonds. It still is. Sectors of the bond markets that are yielding real tax-free returns of 3% and even 4% are very attractive. One can get those returns without taking a lot of credit risk. We are not talking about Detroit, Puerto Rico, or other credits in the municipal bond space that are questionable, facing bankruptcy, in bankruptcy, or otherwise under pressure. We are talking about the highest-quality credits that are available at bargain real yields and bargain relative nominal yields. Build America Bonds, the taxable cousins in Muniland, also remain cheap. Lastly, the disposition of investors to run from the bond market continues to intensify. We see evidence week after week of liquidation of mutual fund shares. This has been going on for six months. Credit Suisse recently created an analysis of various fund flows (December 10, 2013). They ask the question, "What's all the fuss about fund flows about?" They then dissect the various measures of fund flows. The conclusion is fairly clear. The flight from bonds has forced mutual funds to sell. They are selling as a class. That means when Fidelity sells, it has to sell its bonds, and Vanguard is not able to buy because they have to sell bonds as well. As in an earlier period of intense liquidation, the liquidation of bonds now underway works to create bargains in the bond space as sequential investors capitulate due to fear. They extract money from the bond side and place it elsewhere. Then they wonder and second guess their actions. Has anyone thought that the bond sell-off might be overdone? The economy and its recovery are not so robust and not so impacted by rising inflation pressures as to cause bond interest rates to spike higher. Maybe, just maybe, we will have low inflation, lower interest rates, and gradual economic recovery that will persist for quite some time. Maybe, just maybe, the backup in home mortgage interest rates will slow the housing recovery so that it will not be robust. The recovery in the labor market may also persist slowly, as the evidence seems to show. We are approaching the end of the year in managed bond accounts. That is a big piece of Cumberland's activity. We resist this notion that the bond market is headed for an absolute debacle in 2014. We particularly favor the tax-free municipal bond. Where appropriate, we recommend tactical hedging as a method of dampening overall bond portfolio volatility. At Cumberland, we do not view the world as coming to an end in bond land. When a high-grade, long-term tax-free yield of 5% is obtainable in a very low-inflation environment, we think that bond investors who run from bonds and liquidate them will look back, regret the opportunities they missed, and wonder why they did it. ~~~ David R. Kotok, Chairman and Chief Investment Officer |

| Is (Risk) Sharing Always a Virtue? Posted: 15 Dec 2013 02:30 AM PST Is (Risk) Sharing Always a Virtue?

The financial system cannot be made completely safe because it exists to allocate funds to inherently risky projects in the real economy. Thus, an important question for policymakers is how best to structure the financial system to absorb these losses while minimizing the risk that financial sector failures will impair the real economy. Standard theories would predict that one good way of reducing financial sector risk is diversification. For example, the financial system could be structured to facilitate the development of large banks, a point often made by advocates for big banks such as Steve Bartlett. Another, not mutually exclusive, way of enhancing diversification is to create a system that shares risks across banks. An example is the Dodd-Frank Act mandate requiring formerly over-the-counter derivatives transactions to be centrally cleared. However, do these conclusions based on individual bank stability necessarily imply that risk sharing will make the financial system safer? Is it even relevant to the principal risks facing the financial system? Some of the papers presented at the recent Atlanta Fed conference, “Indices of Riskiness: Management and Regulatory Implications,” broadly addressed these questions and others. Other papers discuss the impact of bank distress on local economies, methods of predicting bank failure, and various aspects of incentive compensation paid to bankers (which I discuss in a recent Notes from the Vault). The stability implications of greater risk sharing across banks are explored in “Systemic Risk and Stability in Financial Networks” by Daron Acemoglu, Asuman Ozdaglar, and Alireza Tahbaz-Salehi. They develop a theoretical model of risk sharing in networks of banks. The most relevant comparison they draw is between what they call a “complete financial network” (maximum possible diversification) and a “weakly connected” network in which there is substantial risk sharing between pairs of banks but very little risk sharing outside the individual pairs. Consistent with the standard view of diversification, the complete networks experience few, if any, failures when individual banks are subject to small shocks, but some pairs of banks do fail in the weakly connected networks. However, at some point the losses become so large that the complete network undergoes a phase transition, spreading the losses in a way that causes the failure of more banks than would have occurred with less risk sharing. Extrapolating from this paper, one could imagine that risk sharing could induce a false sense of security that would ultimately make a financial system substantially less stable. At first a more interconnected system shrugs off smaller shocks with seemingly no adverse impact. This leads bankers and policymakers to believe that the system can handle even more risk because it has become more stable. However, at some point the increased risk taking leads to losses sufficiently large to trigger a phase transition, and the system proves to be even less stable than it was with weaker interconnections. While interconnections between financial firms are a theoretically important determinant of contagion, how important are these connections in practice? “Financial Firm Bankruptcy and Contagion,” by Jean Helwege and Gaiyan Zhang, analyzes the spillovers from distressed and failing financial firms from 1980 to 2010. Looking at the financial firms that failed, they find that counterparty risk exposure (the interconnections) tend to be small, with no single exposure above $2 billion and the average a mere $53.4 million. They note that these small exposures are consistent with regulations that limit banks’ exposure to any single counterparty. They then look at information contagion, in which the disclosure of distress at one financial firm may signal adverse information about the quality of a rival’s assets. They find that the effect of these signals is comparable to that found for direct credit exposure. Helwege and Zhang’s results suggest that we should be at least as concerned about separate banks’ exposure to an adverse shock that hits all of their assets as we should be about losses that are shared through bank networks. One possible common shock is the likely increase in the level and slope of the term structure as the Federal Reserve begins tapering its asset purchases and starts a process ultimately leading to the normalization of short-term interest rate setting. Although historical data cannot directly address banks’ current exposure to such shocks, such data can provide evidence on banks’ past exposure. William B. English, Skander J. Van den Heuvel, and Egon Zakrajšek presented evidence on this exposure in the paper “Interest Rate Risk and Bank Equity Valuations.” They find a significant decrease in bank stock prices in response to an unexpected increase in the level or slope of the term structure. The response to slope increases (likely the primary effect of tapering) is somewhat attenuated at banks with large maturity gaps. One explanation for this finding is that these banks may partially recover their current losses with gains they will accrue when booking new assets (funded by shorter-term liabilities). Overall, the papers presented in this part of the conference suggest that more risk sharing among financial institutions is not necessarily always better. Even though it may provide the appearance of increased stability in response to small shocks, the system is becoming less robust to larger shocks. However, it also suggests that shared exposures to a common risk are likely to present at least as an important a threat to financial stability as interconnections among financial firms, especially as the term structure and the overall economy respond to the eventual return to normal monetary policy. Along these lines, I recently offered some thoughts on how to reduce the risk of large widespread losses due to exposures to a common (credit) risk factor.

Note: The conference “Indices of Riskiness: Management and Regulatory Implications” was organized by Glenn Harrison (Georgia State University’s Center for the Economic Analysis of Risk), Jean-Charles Rochet, (University of Zurich), Markus Sticker, Dirk Tasche (Bank of England, Prudential Regulatory Authority), and Larry Wall (the Atlanta Fed’s Center for Financial Innovation and Stability). |

By

By | You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment