The Big Picture |

- The Behavioral Experts on Wealth Management

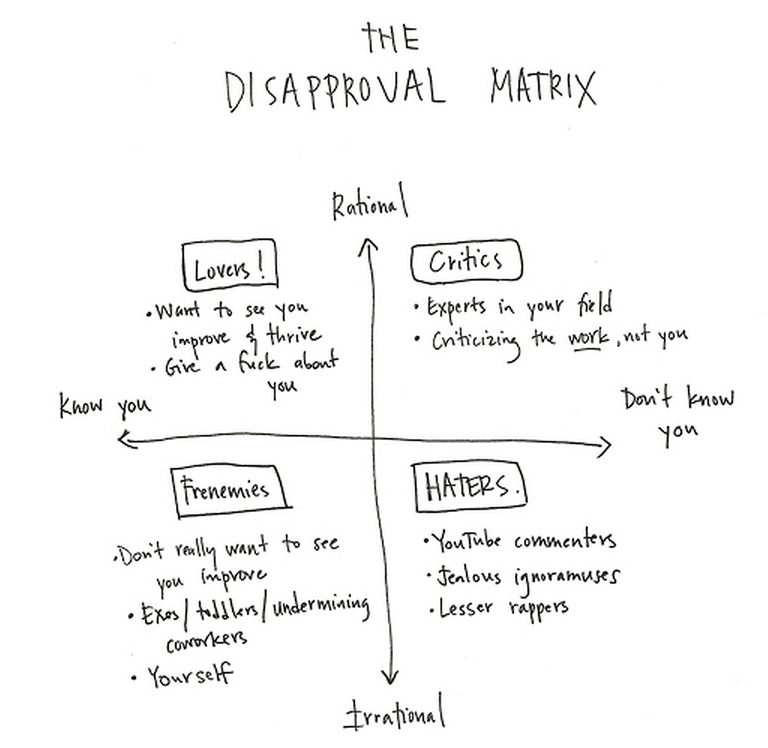

- The Disapproval Matrix

- What You Need To Know

- How Corporate Logos Evolve

- How Money Walks

- America’s Inevitable, Yet Preventable, Decline

- Reminder: Meet Up L.A. Today

- 10 Thursday AM Reads

- QOTD: 8,000 Points Later . . .

- Is Abenomics Going to Put Japan Back on the Map?

- Are Stocks Cheap? A Review of the Evidence

| The Behavioral Experts on Wealth Management Posted: 10 May 2013 02:00 AM PDT Click for Video |

| Posted: 09 May 2013 04:30 PM PDT |

| Posted: 09 May 2013 01:30 PM PDT 1. Fame is fleeting. Used to be very few could get through the sieve, now with fame up for grabs, from reality TV to YouTube, it’s easy to break through, but nearly impossible to sustain. 2. Quality counts. If you want to have longevity. It’s too hard to game the system, too hard to stay on top, in the public eye, your best bet is to focus on the work. 3. Talent is not god-given. You have to do the work, there’s no way around it. You can spearhead the production of the usual suspects, in other words, Max Martin and Dr. Luke can make you a star, but they can’t keep you there, hell, they’re doing their best to stay on top themselves, because almost no one does, from Giorgio Moroder to Mike Chapman to Scott Storch hitmakers have their time and then it ends. Fashion changes, tastes change, generations change. Instead of getting plastic surgery and playing to the young ‘uns, it’s best to cater to your core audience, which will spread the word for you. Yes, parents turn their kids on to their favorite acts, and these are never one hit wonders, but those who have longevity. 4. Spamming is irrelevant. It makes you feel good to get the message out, but no one is paying attention. It is not a numbers game. It’s all about being personal. One personal e-mail to a tastemaker is more important than a generic press release sent to a hundred people from a list you found online. The personal touch is everything. And in this era, the written word is everything. First, know how to type. Second, know how to spell. Third, know grammar. Fourth, be able to tell a story. Fifth, don’t get frustrated when you get no response. People remember personal e-mails, they can pay dividends down the line. But it’s always best to focus on the work more than the marketing. And if you don’t know how to use spellcheck, if you haven’t got the time for spellcheck, tastemakers have no time for you. Hell, I know people who pick online dates based on the spelling errors. Yup, you can have a great picture, but if you don’t know how to spell, these women want nothing to do with you. In other words, school is not for pussies. And if your educational institution isn’t living up to your needs, 5. Don’t chase trends. What’s here today may be gone tomorrow. 6. Ignore the haters. Easier said than done. But you know when criticism resonates. None of us are perfect, we can all improve, we all make mistakes. But let me be clear, ignore the haters, ignore advice unless you’re asking for it. If you ask for someone’s time and you hate on them because they don’t love your production, you’re missing the point. If you don’t have enough confidence in your work to ignore the critics, you’re going to have a very rough road. This does not mean your stuff is good. I’m just saying breakthrough work is usually rejected at first. But there’s very little mainstream breakthrough work out there. 7. The news cycle is 24/7. You’ve got one shot at publicity, then you’re history. So if you’re relying on publicity, your odds are low. You want to bubble up from the bottom, not float down from the top. 8. True fans are worth more than news coverage. You can show your mother you’re in the paper, but most people reading about you, if they do at all, just don’t care. You want active users, not passive people. You want fans who embrace and champion you. 9. Just because you made it, don’t assume anyone is interested in it. Don’t be a child showing his parent his feces. Your work is not that important, we’re all on the planet trying to get along. Push is dead, you want pull. You want to create something so good it sells itself. Which I know is almost impossible, but those are the odds you’re up against. 10. Money comes late. Success is slow. And when you get it, if you overcharge, you shorten your career. There’s plenty of money to be made in the long run if you don’t make money your number one priority. 11. Major labels want radio hits. They want the easy sell. Unless you can get on radio, immediately, the major label doesn’t want you. Period. 12. You need hits. A hit is something so entrancing, so catchy, it ripples through the public. Just because your music does not fit the format, that does not mean it can’t go viral. That’s the essence of PSY’s “Gangnam Style.” 13. Me-too. There’s an audience for me-too, but you want to be me-first. That’s why the classic rock era was so classic, none of the bands sounded alike. That’s one thing wrong with the younger generation, they date in groups, they want to be a member of the club, individuality is shunned. But when it comes to lasting art, individuality is key.

~~~ Visit the archive – |

| Posted: 09 May 2013 11:30 AM PDT click for complete graphic with more examples Hat tip Josh

An illustration by the team at The Logo Company

|

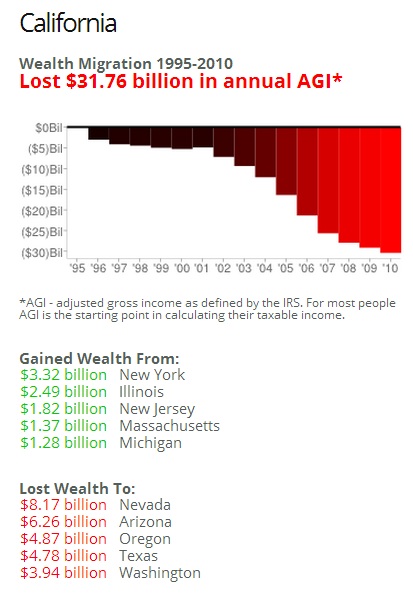

| Posted: 09 May 2013 09:30 AM PDT Fascinating interactive maps at How Money Walks shows where the tax flows int he United States are — both nationally from State to State and Intra-State from County to County.

Click for interactive experience

Since I am on the Left Coast, let’s use California as a sample: California Here is how cash migrated to and from other states:

You can see any inflow or outflow of any state, as well as the intra-state movement.

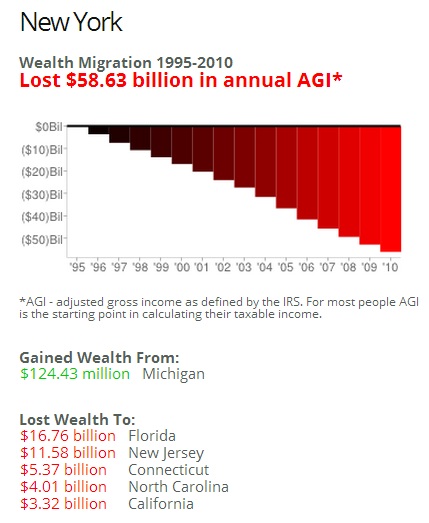

New York after the jump

New York State ~~~ Source: How Money Walks |

| America’s Inevitable, Yet Preventable, Decline Posted: 09 May 2013 09:30 AM PDT “It is no measure of health to be well-adjusted to a sick society.” ~ Jiddu Krishnamurti Much has been said on the topic of America's rise and its inevitable, although preventable, decline. But most of what has been said or written uses empirical evidence, specifically historical observations, of the rise and fall of empires, most notably the Roman Empire. Here on TBP, the Washington Blog recently published a post, called All Empires Crash Soon After They Reach Their Peak. The post notes several common symptoms of empires on the verge of collapse:

These are interesting and important observations that can use a few more thoughts. For disclosure, I'm not a scientist, nor am I a historian or empiricist; I'm a philosopher. Therefore I don't care to make prognostications based upon observations of history, where I am most likely to arrive at only correlations. I like to search for causation by non-scientific means. I’ve provided my own thoughts in The Decline of America Part I: What Consumes the Consumers? Philosophy does not begin with Knowing (at least not from the Rationalist view, ala Plato, and most of Eastern Philosophy, such as Taoism and Buddhism); it begins with Being; before you discover, you must uncover. It is only then that you may recover. But much of Western Philosophy is obsessed with Knowing and thus Being is covered. With regard to the decline of America, one can easily find correlations to past empires that rose and fell spectacularly. But what is the causation? To begin with Being, consider the meta-physics, not the physics:

The primary theme here is not deterministic nor is it anti-American; we do have the capacity to save ourselves but we won't. In the so-called free society, individuals have the ability to succeed wonderfully but there is also equal potential to fail miserably. At our fingertips we have the capacity to learn all the teachings of Socrates, Plato, Aristotle, Buddha, Nietzsche, Kierkegaard, Jung, Freud and Maslow. But there is no demand for depth; all is superficial; there is no Being; there is only Knowing. There is greater demand for escaping into the self-created reality with Facebook and the ironically named “reality television.”

In philosophical terms, individualism consumes itself. The health of the social organism is a total measure of the lower parts of the organism, which will continue to erode as awareness and attention disappear. There is no incentive to change course. The means to escape is in high demand and thus the incentive create more means to escape persists. As Jiddu Krishnamurti taught, attention is everything. Without attention, we are not ourselves; it is where all of our energy comes from. The Roman Empire did not decline this way. However, like all declines of nations, societies and civilizations, are preventable. —————————————————————————- Kent Thune is the blog author of The Financial Philosopher. You can follow Kent on Twitter @ThinkersQuill. |

| Posted: 09 May 2013 08:30 AM PDT

I am in Los Angeles for a few meetings and events this week. If anyone is game for drinks, we will be getting together at the Palomar Hotel Bar & Lounge Blvd 16 from 5:15-7pm today (May 9th). Go in through the lobby, Blvd 16 door on your right (before elevators). Please tweet me @Ritholtz if you plan to show. See you there!

|

| Posted: 09 May 2013 07:00 AM PDT My morning reads:

What are you reading?

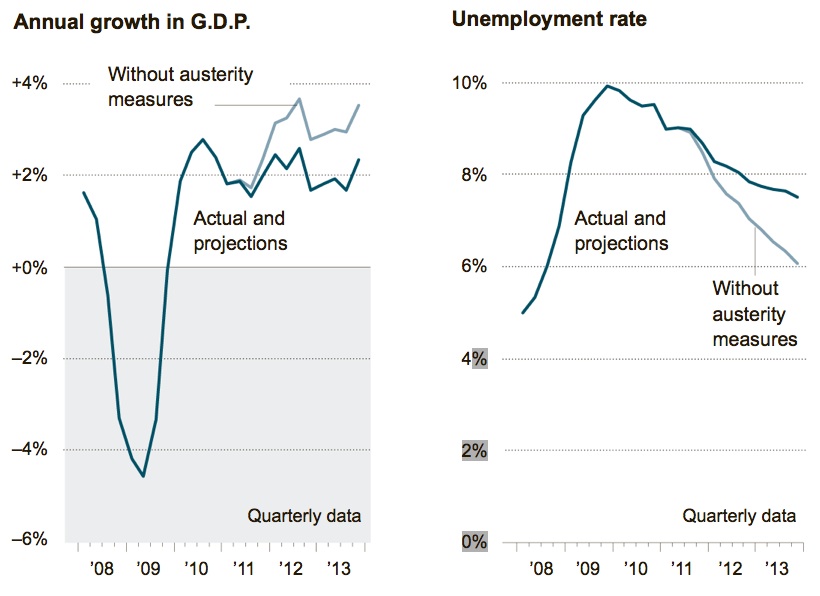

Fiscal Policies Take a Toll |

| QOTD: 8,000 Points Later . . . Posted: 09 May 2013 05:30 AM PDT Josh calls out those who have dug their heels in and fought the tape the whole way up. Are these folks part of your daily media diet? He notes:

The people who have been consistently forecasting the future (as opposed to analyzing the present) have, not surprisingly been getting it wrong. What is surprising is their lack of error correction method. We expect to be wrong, have built in a recognition and admission process that prevents us from staying wrong. This is not to suggest the world is hunky dory and there is nothing to be concerned about. However, there is an issue with those who philosophically cannot wrap their heads around equity markets going up. I am not suggesting that you need to be sanguine all the time — but your methodology has to be more than cherry picking the worst headlines and positioning your portfolio for the next crash, year after year. There are plenty of things to be concerned about — but there always are. The recession porn crowd’s constant warning of impending doom has not exactly been adding value to your media diet — or your portfolio. Instead, try watching inputs and data instead of headlines. Consider signals like the A/D line, equity valuations and trend. I find that is a more productive use of my time than indulging in recession port and fighting the tape the whole way up. As we have discussed repeatedly, what you read and who you listen to can have a significant impact on your net wealth. Choose your Yodas wisely. After a recession, the least rational rise (temporarily) to prominence. Ignore them. (June 4, 2011) |

| Is Abenomics Going to Put Japan Back on the Map? Posted: 09 May 2013 05:00 AM PDT Is Abenomics Going to Put Japan Back on the Map?

In a special Outside the Box today, Keith Fitz-Gerald, Chief Investment Strategist for Money Morning, dissects “Abenomics,” the radical, not to say outlandish, fiscal moves that the newly installed government of Japan is making. And Keith has a ringside seat: he spends much of each year in Japan. In an attempt to cut the Japanese a little slack, Keith comes up with four things that will have to happen for Abenomics to work – but when all is said and done, he says, Abenomics is a recipe for disaster. That does not mean, however, that there is not plenty of opportunity here for short-term profit, and Keith offers a play that is a potential money maker in this volatile Japanese environment. For a limited time, Outside the Box readers can receive a 60% discount when they subscribe to Keith’s Money Map Report. You can check it out here. Have a great week.Your up to my eyeballs in information analyst, John Mauldin, Editor Is Abenomics Going to Put Japan Back on the Map?By Keith Fitz-Gerald On the surface, Abenomics – the radical unlimited stimulus plan put in place by newly elected Japanese PM Shinzo Abe – appears to be working. The Nikkei is up 68% since July, 2012, the yen has weakened by 26% over the same time frame, and Japanese consumer confidence is up sharply to the highest levels in six years. The theory behind Abenomics is that the rising stock market will create capital, and the falling yen will make Japan's export-based economy more competitive in global markets, while newly profitable companies will hire more workers. Don't hold your breath. As I noted during a recent interview on NHK, Japan's national public broadcasting network, the beleaguered island nation faces significant challenges:

The bottom line? Japan is making the same mistakes we're making … or we're making the same mistakes they've already made – it's hard to tell. Either way, the bottom line is pretty simple: You give me a trillion yen and I'll give you a good time, too. In order for Abenomics to work, four things have to happen:

Longer-term, Abenomics is a recipe for disaster – have no illusions about that. Japan, as John Mauldin likes to say, is a bug in search of a windshield. No nation in the history of mankind has ever bailed itself out on anything more than a short-term basis by pursuing a course like Japan's. But short-term … that's another matter entirely, and therein lies opportunity. Historically, every 10% drop in the yen versus the dollar has translated to a 0.3% rise in Japanese GDP the following year, noted Kiichi Murashima, chief economist at Citi in an FT interview. You cannot say the same thing about Japanese stocks. Since the Japanese market's initially collapse in 1991, the world has watched with bated breath as the Nikkei has risen … and plunged with alarming regularity. If you're going to buy and sell like a trader and you're nimble, you can ride the Japanese equity bull – pun absolutely intended. Most investors aren't so equipped, though, -and so the "buy and hope" approach they favor is far more likely to leave them disappointed than profitable. Japanese bonds are probably of dubious value, too. So far they've been stable, because Japan has been able to issue mountains of debt to its own dutiful citizens. The cost of debt service has been negligible, because nearly all of it was held domestically. Now, however, Japan has got a very different situation on its hands. Any rise in long-term rates, let alone a significant one like Kuroda is planning, is going to dramatically hike the cost of debt service to unsustainable levels. Factor in Japan's rapidly aging population and dwindling workforce, and you're looking at a far smaller pool of bond buyers. My expectation is that Japan will be forced into international bond markets no later than 2015, which will effectively double their capital costs. Without meaningful social security reform and spending cuts, that's going to really impact things. That's why I'd rather short the Japanese yen. Stocks are fickle. Abe doesn't care whether they go up or down. Bonds are a part of Kuroda's repurchasing agenda, so those are covered, too. But the yen stands on its own. In that sense, it's the key to the proverbial castle. In order to conduct any sort of serious financial reform, Abe is going to have to move the yen's needle. Everything in corporate Japan depends on it. Since I first brought this trade to everybody's attention in Money Morning in February, 2012, the yen has dropped by 30%, and the investment vehicle I recommended, the ProShares UltraShort Yen Fund, is up more than 60% as it flirts with the psychologically important ¥100/$1USD level. Now, having come close enough to that target for government work, I think the next stop is ¥125 to the dollar, which means that even if you missed the first part of this trade, it's not too late to get on board. And if you're already holding Japanese equities? Don't look a gift horse in the mouth. Hedge the snot out of them or sell into strength – equity markets are not as directly connected to central banking stimulus efforts. But they are absolutely linked to traders’ expectations, which can and do change all too frequently on nothing more than a whim or an errant "tweet," as we have recently seen. You don't want to be left holding the bag. ____________ For a limited time, Outside the Box readers can receive a 60% discount when they subscribe to Keith Fitz-Gerald’s Money Map Report. Check it out here. About the Author: Keith Fitz-Gerald is a seasoned analyst, expert media contributor, and futurist with decades of experience in global markets. In his capacity as Chief Investment Strategist for Money Morning and Chairman of the Fitz-Gerald Group, he appears regularly on financial television programs around the world on the Fox Business Network, CNBC Asia, NHK, BNN, and more. He's been called on for his extraordinary ability to see future trends in such publications as Wired UK and the Wall Street Journal. Forbes.com labeled him a "Business Visionary." Even Mensa has called him to their stage. Mr. Fitz-Gerald splits his time between homes in Oregon and Japan, with his wife and two boys. He travels the world extensively in search of investment opportunities others don't yet see or recognize. |

| Are Stocks Cheap? A Review of the Evidence Posted: 09 May 2013 03:00 AM PDT Are Stocks Cheap? A Review of the Evidence

We surveyed banks, we combed the academic literature, we asked economists at central banks. It turns out that most of their models predict that we will enjoy historically high excess returns for the S&P 500 for the next five years. But how do they reach this conclusion? Why is it that the equity premium is so high? And more importantly: Can we trust their models? The equity risk premium is the expected future return of stocks minus the risk-free rate over some investment horizon. Because we don't directly observe market expectations of future returns, we need a way to figure them out indirectly. That's where the models come in. In this post, we analyze twenty-nine of the most popular and widely used models to compute the equity risk premium over the last fifty years. They include surveys, dividend-discount models, cross-sectional regressions, and time-series regressions, which together use more than thirty different variables as predictors, ranging from price-dividend ratios to inflation. Our calculations rely on real-time information to avoid any look-ahead bias. So, to compute the equity risk premium in, say, January 1970, we only use data that was available in December 1969. Let's now take a look at the facts. The chart below shows the weighted average of the twenty-nine models for the one-month-ahead equity risk premium, with the weights selected so that this single measure explains as much of the variability across models as possible (for the geeks: it is the first principal component). The value of 5.4 percent for December 2012 is about as high as it's ever been. The previous two peaks correspond to November 1974 and January 2009. Those were dicey times. By the end of 1974, we had just experienced the collapse of the Bretton Woods system and had a terrible case of stagflation. January 2009 is fresher in our memory. Following the collapse of Lehman Brothers and the upheaval in financial markets, the economy had just shed almost 600,000 jobs in one month and was in its deepest recession since the 1930s. It is difficult to argue that we're living in rosy times, but we are surely in better shape now than then.

The next chart shows a comparison between those two episodes and today. For 1974 and 2009, the green and red lines show that the equity risk premium was high at the one-month horizon, but was decreasing at longer and longer horizons. Market expectations were that at a four-year horizon the equity risk premium would return to its usual level (the black line displays the average levels over the last fifty years). In contrast, the blue line shows that the equity risk premium today is high irrespective of investment horizon.

Why is the equity premium so high right now? And why is it high at all horizons? There are two possible reasons: low discount rates (that is, low Treasury yields) and/or high current or future expected dividends. We can figure out which factor is more important by comparing the twenty-nine models with one another. This strategy works because some models emphasize changes in dividends, while others emphasize changes in risk-free rates. We find that the equity risk premium is high mainly due to exceptionally low Treasury yields at all foreseeable horizons. In contrast, the current level of dividends is roughly at its historical average and future dividends are expected to grow only modestly above average in the coming years. In the next chart we show, in an admittedly crude way, the impact that low Treasury yields have on the equity risk premium. The blue and black lines reproduce the lines from the previous chart: the blue is today's equity risk premium at different horizons and the black is the average over the last fifty years. The new purple line is a counterfactual: it shows what the equity premium would be today if nominal Treasury yields were at their average historical levels instead of their current low levels. The figure makes clear that exceptionally low yields are more than enough to justify a risk premium that is highly elevated by historical standards.

But none of this analysis matters if excess returns are unpredictable because the equity risk premium is all about expected returns. So…are returns predictable? The jury is still out on this one, and the debate among academics and practitioners is alive and well. The simplest predictive method is to assume that future returns will be equal to the average of all past returns. It turns out that it is remarkably tricky to improve upon this simple method. However, with so many models at hand, we couldn't help but ask if any of them can, in fact, do better. The table below gives the extra returns that investors could have earned by using the models instead of the historical mean to predict future returns. For investment horizons of one month, one year, and five years, we pick the best model in each of the four classes we consider together with the weighted average of all twenty-nine models. We compute these numbers by assuming that investors can allocate their wealth in stocks or bonds, and that they are not too risk-averse (for the geeks again, we solved a Merton portfolio problem in real time assuming that the coefficient of relative risk aversion is equal to one). The table shows positive extra returns for most of the models, especially at long horizons. At face value, this result means that the models are actually helpful in forecasting returns. However, we should keep in mind some of the limitations of our analysis. First, we have not shown confidence intervals or error bars. In practice, those are quite large, so even if we could have earned extra returns by using the models, it may have been solely due to luck. Second, we have selected models that have performed well in the past, so there is some selection bias. And of course, past performance is no guarantee of future performance. Disclaimer

|

Source:

Source:

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment