The Big Picture |

- Bernanke: Monitoring the Financial System

- More Clueless Stones . . . ?

- Succinct Summation of Week Events (May 10, 2013)

- Witte Lecture Series: Tonite & Tomorrow (May 10/11)

- S&P500 Long Term Breakout?

- 10 Friday AM Reads

- A Few Words About Alan Abelson

- Too Big to Fail too Sweet to Give Up

- The Cave: Plato’s Allegory in Claymation

- David Merkel: On Insurance Investing

| Bernanke: Monitoring the Financial System Posted: 11 May 2013 02:00 AM PDT Monitoring the Financial System

We are now more than four years beyond the most intense phase of the financial crisis, but its legacy remains. Our economy has not yet fully regained the jobs lost in the recession that accompanied the financial near collapse. And our financial system–despite significant healing over the past four years–continues to struggle with the economic, legal, and reputational consequences of the events of 2007 to 2009. The crisis also engendered major shifts in financial regulatory policy and practice. Not since the Great Depression have we seen such extensive changes in financial regulation as those codified in the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) in the United States and, internationally, in the Basel III Accord and a range of other initiatives. This new regulatory framework is still under construction, but the Federal Reserve has already made significant changes to how it conceptualizes and carries out both its regulatory and supervisory role and its responsibility to foster financial stability. In my remarks today I will discuss the Federal Reserve’s efforts in an area that typically gets less attention than the writing and implementation of new rules–namely, our ongoing monitoring of the financial system. Of course, the Fed has always paid close attention to financial markets, for both regulatory and monetary policy purposes. However, in recent years, we have both greatly increased the resources we devote to monitoring and taken a more systematic and intensive approach, led by our Office of Financial Stability Policy and Research and drawing on substantial resources from across the Federal Reserve System. This monitoring informs the policy decisions of both the Federal Reserve Board and the Federal Open Market Committee as well as our work with other agencies. The step-up in our monitoring is motivated importantly by a shift in financial regulation and supervision toward a more macroprudential, or systemic, approach, supplementing our traditional microprudential perspective focused primarily on the health of individual institutions and markets. In the spirit of this more systemic approach to oversight, the Dodd-Frank Act created the Financial Stability Oversight Council (FSOC), which is comprised of the heads of a number of federal and state regulatory agencies. The FSOC has fostered greater interaction among financial regulatory agencies as well as a sense of common responsibility for overall financial stability. Council members regularly discuss risks to financial stability and produce an annual report, which reviews potential risks and recommends ways to mitigate them.1 The Federal Reserve’s broad-based monitoring efforts have been essential for promoting a close and well-informed collaboration with other FSOC members. A Focus on Vulnerabilities Two other related points motivate our increased monitoring. The first is that the financial system is dynamic and evolving not only because of innovation and the changing needs of the economy, but also because financial activities tend to migrate from more-regulated to less-regulated sectors. An innovative feature of the Dodd-Frank Act is that it includes mechanisms to permit the regulatory system, at least in some circumstances, to adapt to such changes. For example, the act gives the FSOC powers to designate systemically important institutions, market utilities, and activities for additional oversight. Such designation is essentially a determination that an institution or activity creates or exacerbates a vulnerability of the financial system, a determination that can only be made with comprehensive monitoring and analysis. The second motivation for more intensive monitoring is the apparent tendency for financial market participants to take greater risks when macro conditions are relatively stable. Indeed, it may be that prolonged economic stability is a double-edged sword. To be sure, a favorable overall environment reduces credit risk and strengthens balance sheets, all else being equal, but it could also reduce the incentives for market participants to take reasonable precautions, which may lead in turn to a buildup of financial vulnerabilities. Probably our best defense against complacency during extended periods of calm is careful monitoring for signs of emerging vulnerabilities and, where appropriate, the development of macroprudential and other policy tools that can be used to address them. The Federal Reserve’s Financial Stability Monitoring Program Systemically Important Financial Institutions Dodd-Frank also establishes a framework for subjecting SIFIs to comprehensive supervisory oversight and enhanced prudential standards. For all such companies, the Federal Reserve will have access to confidential supervisory information and will monitor standard indicators such as regulatory capital, leverage, and funding mix. However, some of these measures, such as regulatory capital ratios, tend to be backward looking and thus may be slow to flag unexpected, rapid changes in the condition of a firm. Accordingly, we supplement the more standard measures with other types of information. One valuable source of supplementary information is stress testing. Regular, comprehensive stress tests are an increasingly important component of the Federal Reserve’s supervisory toolkit, having been used in our assessment of large bank holding companies since 2009.4 To administer a stress test, supervisors first construct a hypothetical scenario that assumes a set of highly adverse economic and financial developments–for example, a deep recession combined with sharp declines in the prices of houses and other assets. The tested firms and their supervisors then independently estimate firms’ projected losses, revenues, and capital under the hypothetical scenario, and the results are publicly disclosed. Firms are evaluated both on their post-stress capital levels and on their ability to analyze their exposures and capital needs. Stress testing provides a number of advantages over more-standard approaches to assessing capital adequacy. First, measures of capital based on stress tests are both more forward looking and more robust to “tail risk”–that is, to extremely adverse developments of the sort most likely to foster broad-based financial instability. Second, because the Federal Reserve conducts stress tests simultaneously on the major institutions it supervises, the results can be used both for comparative analyses across firms and to judge the collective susceptibility of major financial institutions to certain types of shocks. Indeed, comparative reviews of large financial institutions have become an increasingly important part of the Federal Reserve’s supervisory toolkit more generally. Third, the disclosure of stress-test results, which increased investor confidence during the crisis, can also strengthen market discipline in normal times. The stress tests thus provide critical information about key financial institutions while also forcing the firms to improve their ability to measure and manage their risk exposures. Stress-testing techniques can also be used in more-focused assessments of the banking sector’s vulnerability to specific risks not captured in the main scenario, such as liquidity risk or interest rate risk. Like comprehensive stress tests, such focused exercises are an important element of our supervision of SIFIs. For example, supervisors are collecting detailed data on liquidity that help them compare firms’ susceptibilities to various types of funding stresses and to evaluate firms’ strategies for managing their liquidity. Supervisors also are working with firms to assess how profitability and capital would fare under various stressful interest rate scenarios. Federal Reserve staff members supplement supervisory and stress-test information with other measures. For example, though supervisors have long appreciated the value of market-based indicators in evaluating the conditions of systemically important firms (or, indeed, any publicly traded firm), our monitoring program uses market information to a much greater degree than in the past. Thus, in addition to standard indicators–such as stock prices and the prices of credit default swaps, which capture market views about individual firms–we use market-based measures of systemic stability derived from recent research. These measures use correlations of asset prices to capture the market’s perception of a given firm’s potential to destabilize the financial system at a time when the broader financial markets are stressed; other measures estimate the vulnerability of a given firm to disturbances emanating from elsewhere in the system.5 The further development of market-based measures of systemic vulnerabilities and systemic risk is a lively area of research. Network analysis, yet another promising tool under active development, has the potential to help us better monitor the interconnectedness of financial institutions and markets. Interconnectedness can arise from common holdings of assets or through the exposures of firms to their counterparties. Network measures rely on concepts used in engineering, communications, and neuroscience to map linkages among financial firms and market activities. The goals are to identify key nodes or clusters that could destabilize the system and to simulate how a shock, such as the sudden distress of a firm, could be transmitted and amplified through the network. These tools can also be used to analyze the systemic stability effects of a change in the structure of a network. For example, margin rules affect the sensitivity of firms to the conditions of their counterparties; thus, margin rules affect the likelihood of financial contagion through various firms and markets. Shadow Banking As it turned out, the ultimate investors did not fully understand the quality of the assets they were financing. Investors were lulled by triple-A credit ratings and by expected support from sponsoring institutions–support that was, in fact, discretionary and not always provided. When investors lost confidence in the quality of the assets or in the institutions expected to provide support, they ran. Their flight created serious funding pressures throughout the financial system, threatened the solvency of many firms, and inflicted serious damage on the broader economy. Securities broker-dealers play a central role in many aspects of shadow banking as facilitators of market-based intermediation. To finance their own and their clients’ securities holdings, broker-dealers tend to rely on short-term collateralized funding, often in the form of repo agreements with highly risk-averse lenders. The crisis revealed that this funding is potentially quite fragile if lenders have limited capacity to analyze the collateral or counterparty risks associated with short-term secured lending, but rather look at these transactions as nearly risk free. As questions emerged about the nature and value of collateral, worried lenders either greatly increased margin requirements or, more commonly, pulled back entirely. Borrowers unable to meet margin calls and finance their asset holdings were forced to sell, driving down asset prices further and setting off a cycle of deleveraging and further asset liquidation. To monitor intermediation by broker-dealers, the Federal Reserve in 2010 created a quarterly Senior Credit Officer Opinion Survey on Dealer Financing Terms, which asks dealers about the credit they provide.6 Modeled on the long-established Senior Loan Officer Opinion Survey on Bank Lending Practices sent to commercial banks, the survey of senior credit officers at dealers tracks conditions in markets such as those for securities financing, prime brokerage, and derivatives trading.7 The credit officer survey is designed to monitor potential vulnerabilities stemming from the greater use of leverage by investors (particularly through lending backed by less-liquid collateral) or increased volumes of maturity transformation. Before the financial crisis, we had only very limited information regarding such trends. We have other potential sources of information about shadow banking. The Treasury Department’s Office of Financial Research and Federal Reserve staff are collaborating to construct data sets on triparty and bilateral repo transactions, which should facilitate the development of better monitoring metrics for repo activity and improve transparency in these markets. We also talk regularly to market participants about developments, paying particular attention to the creation of new financial vehicles that foster greater maturity transformation outside the regulated sector, provide funding for less-liquid assets, or transform risks from forms that are more easily measured to forms that are more opaque. A fair summary is that, while the shadow banking sector is smaller today than before the crisis and some of its least stable components have either disappeared or been reformed, regulators and the private sector need to address remaining vulnerabilities. For example, although money market funds were strengthened by reforms undertaken by the Securities and Exchange Commission (SEC) in 2010, the possibility of a run on these funds remains–for instance, if a fund should “break the buck,” or report a net asset value below 99.5 cents, as the Reserve Primary Fund did in 2008. The risk is increased by the fact that the Treasury no longer has the power to guarantee investors’ holdings in money funds, an authority that was critical for stopping the 2008 run. In November 2012, the FSOC proposed for public comment some alternative approaches for the reform of money funds. The SEC is currently considering these and other possible steps. With respect to the triparty repo platform, progress has been made in reducing the amount of intraday credit extended by the clearing banks in the course of the daily settlement process, and, as additional enhancements are made, the extension of such credit should be largely eliminated by the end of 2014. However, important risks remain in the short-term wholesale funding markets. One of the key risks is how the system would respond to the failure of a broker-dealer or other major borrower. The Dodd-Frank Act has provided important additional tools to deal with this vulnerability, notably the provisions that facilitate an orderly resolution of a broker-dealer or a broker-dealer holding company whose imminent failure poses a systemic risk. But, as highlighted in the FSOC’s most recent annual report, more work is needed to better prepare investors and other market participants to deal with the potential consequences of a default by a large participant in the repo market.8 Asset Markets Not surprisingly, we try to identify unusual patterns in valuations, such as historically high or low ratios of prices to earnings in equity markets. We use a variety of models and methods; for example, we use empirical models of default risk and risk premiums to analyze credit spreads in corporate bond markets. These assessments are complemented by other information, including measures of volumes, liquidity, and market functioning, as well as intelligence gleaned from market participants and outside analysts. In light of the current low interest rate environment, we are watching particularly closely for instances of “reaching for yield” and other forms of excessive risk-taking, which may affect asset prices and their relationships with fundamentals. It is worth emphasizing that looking for historically unusual patterns or relationships in asset prices can be useful even if you believe that asset markets are generally efficient in setting prices. For the purpose of safeguarding financial stability, we are less concerned about whether a given asset price is justified in some average sense than in the possibility of a sharp move. Asset prices that are far from historically normal levels would seem to be more susceptible to such destabilizing moves. From a financial stability perspective, however, the assessment of asset valuations is only the first step of the analysis. Also to be considered are factors such as the leverage and degree of maturity mismatch being used by the holders of the asset, the liquidity of the asset, and the sensitivity of the asset’s value to changes in broad financial conditions. Differences in these factors help explain why the correction in equity markets in 2000 and 2001 did not induce widespread systemic disruptions, while the collapse in house prices and in the quality of mortgage credit during the 2007-09 crisis had much more far-reaching effects: The losses from the stock market declines in 2000 and 2001 were widely diffused, while mortgage losses were concentrated–and, through various financial instruments, amplified–in critical parts of the financial system, resulting ultimately in panic, asset fire sales, and the collapse of credit markets. Nonfinancial Sector The vulnerabilities of the nonfinancial sector can potentially be captured by both stock measures (such as wealth and leverage) and flow measures (such as the ratio of debt service to income). Sector-wide data are available from a number of sources, importantly the Federal Reserve’s flow of funds accounts, which is a set of aggregate integrated financial accounts that measures sources and uses of funds for major sectors as well as for the economy as a whole.10 These accounts allow us to trace the flow of credit from its sources, such as banks or wholesale funding markets, to the household and business sectors that receive it. The Federal Reserve also now monitors detailed consumer- and business-level data suited for picking up changes in the nature of borrowing and lending, as well as for tracking financial conditions of those most exposed to a cyclical downturn or a reversal of fortunes. For example, during the housing boom, the aggregate data accurately showed the outsized pace of home mortgage borrowing, but it could not reveal the pervasive deterioration in underwriting that implied a substantial increase in the underlying credit risk from that activity.11 More recently, gains in household net worth have been concentrated among wealthier households, while many households in the middle or lower parts of the distribution have experienced declines in wealth since the crisis. Moreover, many homeowners remain “underwater,” with their homes worth less than the principal balances on their mortgages. Thus, more detailed information clarifies that many households remain more financially fragile than might be inferred from the aggregate statistics alone. Conclusion

Other Formats 188 KB PDF 1. For the most recent report, see U.S. Department of the Treasury, Financial Stability Oversight Council (2013), 2013 Annual Report (Washington: Department of the Treasury). Return to text 2. See Ben S. Bernanke (2010), “Causes of the Recent Financial and Economic Crisis,” testimony before the Financial Crisis Inquiry Commission, Washington, September 2; and Ben S. Bernanke (2012), “Some Reflections on the Crisis and the Policy Response,” speech delivered at “Rethinking Finance: Perspectives on the Crisis,” a conference sponsored by the Russell Sage Foundation and The Century Foundation, New York, April 13. Return to text 3. The remainder of my remarks draws heavily on Tobias Adrian, Daniel Covitz, and Nellie Liang (2013), “Financial Stability Monitoring (PDF),” Finance and Economics Discussion Series 2013-21 (Washington: Board of Governors of the Federal Reserve System, April). This paper provides more details on the Federal Reserve’s financial stability monitoring program. I thank the authors for their assistance with these remarks. Return to text 4. The Federal Reserve’s stress-testing program is discussed in Ben S. Bernanke (2013), “Stress Testing Banks: What Have We Learned?” speech delivered at “Maintaining Financial Stability: Holding a Tiger by the Tail,” a financial markets conference sponsored by the Federal Reserve Bank of Atlanta, held in Stone Mountain, Ga., April 8-10. More limited forms of stress testing were used by supervisors before 2009. Return to text 5. For example, conditional value at risk provides an estimate of the systemic importance of a firm at a moment in time, based on how the firm’s equity value and broader equity values co-vary when overall conditions are very adverse; see Tobias Adrian and Markus K. Brunnermeier (2008; revised September 2011), “CoVaR (PDF),” Staff Reports 348 (New York: Federal Reserve Bank of New York, September). The distressed insurance premium uses information from firms’ credit default swap spreads and equity prices to measure the implied cost of insuring a given firm against broader financial distress–an indicator of the vulnerability of the firm to systemic instability; see Xin Huang, Hao Zhou, and Haibin Zhu (2009), “A Framework for Assessing the Systemic Risk of Major Financial Institutions 6. The Senior Credit Officer Opinion Survey on Dealer Financing Terms is available on the Federal Reserve Board’s website. Return to text 7. The Senior Loan Officer Opinion Survey on Bank Lending Practices is available on the Federal Reserve Board’s website. Return to text 8. See Financial Stability Oversight Council, 2013 Annual Report, in note 1. Return to text 9. See, for example, Mathias Drehmann, Claudio Borio, and Kostas Tsatsaronis (2011), “Anchoring Countercyclical Capital Buffers: The Role of Credit Aggregates,” International Journal of Central Banking, vol. 7 (December), pp. 189-240; and Rochelle M. Edge and Ralf R. Meisenzahl (2011), “The Unreliability of Credit-to-GDP Ratio Gaps in Real Time:Implications for Countercyclical Capital Buffers,” International Journal of Central Banking, vol. 7 (December), pp. 261-98. Return to text 10. The flow of funds data are available on the Federal Reserve Board’s website. Return to text 11. See Matthew J. Eichner, Donald L. Kohn, and Michael G. Palumbo (2010), “Financial Statistics for the United States and the Crisis: What Did They Get Right, What Did They Miss, and How Should They Change? (PDF)” Finance and Economics Discussion Series 2010-20 (Washington: Board of Governors of the Federal Reserve System, April). Return to text |

| Posted: 10 May 2013 04:30 PM PDT Check this out: “Mick’s Message to the Bay Area”:

It’s like a bad SNL skit, a bozo politician doing an inadequate job of reading from the Teleprompter. And how about this from the Echoplex: That’s the video on the Stones’ official YouTube page. Listen to Keith’s solo starting around :35, if you’re not laughing, you’re used to hearing your three year old play the guitar. How did they get it so wrong? You know the drill… You play the Super Bowl and you put up the shows the next morning, while the memory is still fresh in the public’s brain, before people forget the hype and excitement of the moment. Hell, I can’t even remember who won last year’s Super Bowl, I’ve just about forgotten “Argo” won Best Picture. We’re inundated with so much information, the news cycle is so fast, that if you don’t capitalize on your fame in days, you’re missing out. So the Stones do their fiftieth anniversary shows last fall. It’s kind of like Zeppelin at the 02. There may never be another show, you’ve got to overpay to go now, to be part of the excitement. And then MONTHS later, when there’s no buzz whatsoever, the band puts up shows at the same inflated ticket prices. Huh? Where’s the manager? There is none. And you need one. An act without a manager is like an attorney representing himself, he’s got a fool for a client. You need a third eye, an opinion from outside the maelstrom, to give you perspective. The entire Rolling Stones YouTube page …was an afterthought. How do I know? Because the views are so low. Remember when the Stones used to premiere videos on TV, how they used to work the public into a frenzy? Now there is no frenzy, there’s no cook creating the perception that if you don’t go, you’re a loser. All you see is greed. And if you’re that damn greedy, do it like the rest of the superstars. Scalp your own tickets. That’s the Michael Cohl model. We pay you a lump sum, and you can’t ask how we got that money. But for prior tours, Cohl had a team of experts, a seamless machine, selling fan club memberships and merch and raking up the capital. This tour is a positively last minute venture with no vision and even poorer execution. 1. Perception Is Everything In The Music Business Yes, the tickets could theoretically be worth $600, but if you ask for that much, you’re separating yourself from your audience. Sell platinum tickets with B.S. perks, a laminate and the ability to meet Ron Wood or some other superfluous member of the band (I’d say Charlie, but I’m not sure he can speak.) You build your fan base not on the rich who can pay anything, but the poor who can’t afford much. Yes, in today’s rich versus poor society, and if you don’t think there’s class warfare, you didn’t notice that Obama got reelected, you have to appear to be one of the people if you want to sell to the people. There are not enough 1%ers to fill arenas at these prices. 2. Ticketmaster The public hates Ticketmaster, even though everybody in the business knows it’s a front for the acts. Yup, those inflated fees go to the promoter, the buildings, on previous tours even to the Stones. You need a scapegoat. But the Stones messed up here, there is no scapegoat, the blame falls squarely on their shoulders. 3. Don’t Be Afraid To Share The Money You pay professional management its commission so you can make more money. It’s kind of like hiring an accountant…they don’t come cheap, but they save you more than their fee, because that’s what they do all day long, taxes. Mick Jagger is hobnobbing with his rich socialite buddies, he’s got no idea what’s going on in the music business, which seemingly changes every six months. He needed fresh, experienced eyes on this. 4. There Are No Secrets The Stones, like Led Zeppelin, were built on mystery. But there is no mystery today. So either you can be like many old farts and restrict taping and photography, which is kind of like telling kids not to have sex, or you can embrace it. If the Stones are crappy live, they should have their official site filled with fan videos, which we all expect to be crappy. We then go to the show to hear the real deal, up close and personal. But when the official videos sound crappy…you think the band is.

5. Social If you don’t embrace it, you can’t energize fans. The Stones are playing to the mainstream press. And although their audience is the last vestige of those who pay attention to it, they should be tweeting and Facebooking to humanize themselves. It speaks to perception. They need to get down in the pit with their audience. 6. Scalping Paperless. Sure, savvy scalpers can elude the system, then again, it would require a drop in ticket prices to generate excitement, and the Stones don’t seem willing to leave a single dollar on the table. 7. People Talk Used to be everything was rumor and innuendo, and you didn’t hear much more than what your neighbors had to say, but now with the Internet people can not only read reports from around the world, they can interact with others. 8. Virality That’s how you sell out a show. By getting everybody talking about it, making them fearful of missing it. There’s no virality here. Hell, look at the YouTube views! 9. Desperation It’s anathema. It’s the same in music as it is in dating. If you need it that bad, we’re turned off. I received the following e-mails: “Another thing that shows what a disaster this tour is/was is that they actually ANNOUNCED their previously secret/surprise special guests early in the day to try and build hype! The stones official account tweeted about Keith Urban and Gwen Stefani’s appearances early in the day. Why in the world would you do this if it was supposed to be a surprise other than to try and scramble to get people to come down? They were just reaching for anything at this point. Today they announced Tom Waits guest appearance for Oakland. What a joke.” And: “Twitter made big bucks last night. The feed was full of Twads and I mean 7-10 in a row time and time again, espousing all their special guests.” It’s supposed to be a SURPRISE! 10. Flex Pricing link: “Rolling Stones Concert Promoter On ‘Flex Pricing’ Ticket Strategy: ‘I Want the Brokers Pissed Off’”: http://bit.ly/1426WgN Let’s assume this was AEG’s plan all along, WHY DIDN’T THEY TELL ANYBODY? This is kind of like paying a grand for an airline ticket the week of and finding out if you’d booked a month in advance, it’d be $350. Don’t create a game without telling us the rules. 11. Lies If you believe there were no $85 customers sitting next to $600 customers, you probably believe everything you read in the newspaper. You can tell the press whatever you want, and the people on the music beat, those who remain, who were not downsized out of existence, will print it. Because they want the access, they want the free tickets. That’s what the entire music press is built upon, access. But if you wouldn’t rather speak to a tech titan than a rocker, you own no smartphone and are unable to cogitate. 12. The Press Read the “New York Times” article wherein it’s stated that Roger Ailes cut Geraldo Rivera’s mic when he was defending Obama on Fox. But it gets better, Benghazi was a big story because Fox hammered it. Read the facts here: “Behind the Scenes at Fox”: http://nyti.ms/18UX7lL Then again, this is long after the fact. And the “Times” story is reporting on a book. Which is why if you want to know what’s going on in music, you go to the web, the one place the Stones forgot to look. 13. “Rolling Stone” Cover Story It’s supposed to come out BEFORE the tour begins. That’s like letting you flip through “Playboy” before asking for payment for the magazine. No, that’s like watching Internet porn, getting off, and then being asked to pay. Music is a sideshow, a carnival, which is why Colonel Tom Parker did so well for Elvis. And yes, he might have ripped Presley off, not gone to Europe for fear of being revealed to be an illegal alien, but Parker made and sustained his career. There’s yet to be a superstar without a great manager. Because performing and managing are two different skills! 14. You Come Out With Both Guns Blazing And Establish Your Narrative The Stones have lost control of their story. Meglen didn’t come out and defend their ticketing practices until days after shows began. 15. Things Change Just because you sold a ton of tickets yesterday, that does not mean you can sell a ton today. Yes, the Stones could have sold out no problem if every ticket was $85, and furthermore, scalpers for superstar shows beget tons of press about how impossible it is to get in, how expensive it is, which only burnishes an act’s image. 16. We All Want What We Can’t Have We should be salivating and unable to get a ticket. Instead, everybody can attend, even up to the very last minute. It’s kind of like queuing up at the Apple Store for the latest product and finding out no one else is in line. Huh? The day one of Apple’s new products falls flat is the day the company’s done. Once again, it all comes down to money. Didn’t used to be that way, it used to be about music. And fame. And sex. You wanted to have sex with Mick Jagger. Do you want to have sex with that emaciated guy in the video above? Eek! Maybe, but only to be able to tell your friends! The eighties were the height of fame, because that’s what TV gives you, ubiquity. Radio can’t compete. And today it’s all about music. If you’re in it for the money, you’re in the wrong business. Follow Bono’s lead, become a venture capitalist. And if you do decide to play music, get a great manager. Gene Simmons likes to bloviate how it’s all about the money, but without Bill Aucoin, he’d have none.

~~~ Visit the archive – |

| Succinct Summation of Week Events (May 10, 2013) Posted: 10 May 2013 12:30 PM PDT Succinct Summations week ending May 10, 2013. Positives:

Negatives:

|

| Witte Lecture Series: Tonite & Tomorrow (May 10/11) Posted: 10 May 2013 11:00 AM PDT Looks like we are just about sold out for this weekend’s lecture at Newport Beach Library in California. This is one of the more fun presentations I do where we reveal I hope it is both informative and amusing !

Click for more information Source: Newport Beach Public Library |

| Posted: 10 May 2013 09:00 AM PDT

The US stock markets continue to rally this week, with the S&P 500 trading up on the week. A longer term look at the S&P 500 since 2000 illustrates both the post dot com comeback and and the post-financial crisis rally. The latest leg of the post-financial crisis rally has the S&P 500 breaking above resistance created by the last two all-time record highs. Ample liquidity, strong profits, and mixed sentiment seem to be the drivers here . . .

|

| Posted: 10 May 2013 07:00 AM PDT My morning reads:

What are you reading?

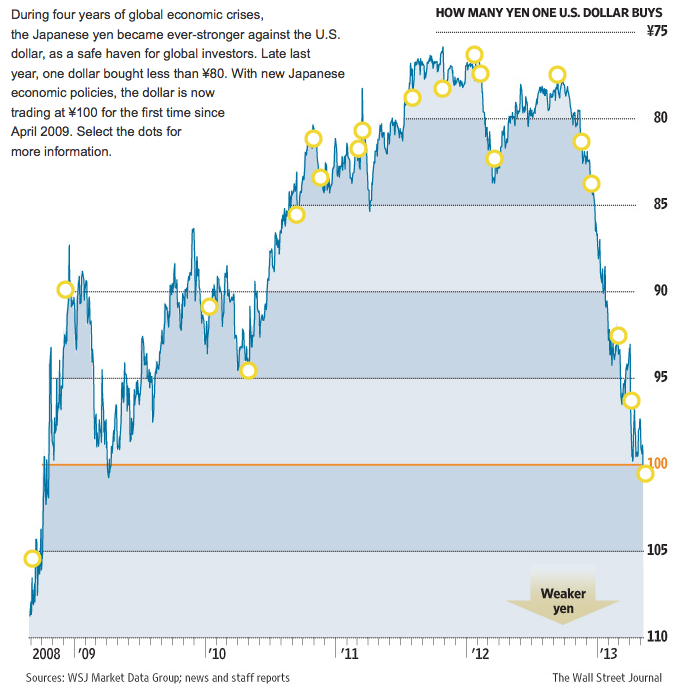

Yen’s Fall Trickles Through Japanese Economy |

| A Few Words About Alan Abelson Posted: 10 May 2013 06:28 AM PDT We learned of the sad news of Alan Abelson’s passing yesterday. I know so many people who have “Abelson stories” — from Doug Kass to Stephanie Pomboy to David Rosenberg to Phillip Dunne. Hopefully, these folks will share some of their memories about the man and the writer in the coming days. (Josh does a nice job here). Ableson’s dry sardonic wit made him everyone’s first read in the weekly, whether it was in print or online. His ability to turn a phrase, capture the zeitgeist in a sentence and then delightfully disembowel it a phrase or two later. CJR notes that Abelson spent 57 years at Barron's, and “started writing his withering Up and Down Wall Street column in 1966 and continued writing through February of this year.” He turned his sharp eye and acid pen on the absurdity of Wall Street, and the systemic ways that financiers labored to separate good people from their money. He was criticized at times for being to bearish — in the late 1990s and again in the mid 2000s — but in each case, he was ultimately proved correct. Besides, a journalist’s job is to shine a light on issues of potential importance — not generate a weekly positive P&L. I recall my first ever mention in his column back in 2004 or 05 — when someone you have admired for so many years says something nice about you (even in passing) it can be overwhelming. At the time I worked at Maxim Group — a sell side firm with about $5B in assets. I remember getting a call from Ed Rose, the firm’s general counsel, at home on the weekend to congratulate me about the mention — which speaks volumes more about Abelson’s stature and influence than anything it says about me. We took in the sad news yesterday, knowing the likes of Abelson will never be replaced. Randall Forsyth has been doing an excellent job handling the column in Abelson’s absence . . . but I do not envy the task that lay before him, for those are some mighty big shoes to fill . . .

Alan Abelson: 1925 to 2013 (Barron’s) |

| Too Big to Fail too Sweet to Give Up Posted: 10 May 2013 05:05 AM PDT |

| The Cave: Plato’s Allegory in Claymation Posted: 10 May 2013 04:00 AM PDT This is a wonderful clay animation adaptation of Plato’s Allegory of the Cave, which dovetails nicely into my Decline of America piece posted yesterday. The video demonstrates simply and briefly how our decline is probable but preventable.

The number of “prisoners” increases daily. My goal is to free as many people from “the cave” as possible. Please share with anyone who may benefit. Hat tip to my friend Ken at Cicero’s Free Citizen Post for making me aware of the video. —————————————————————————————————————– Kent Thune is the blog author of The Financial Philosopher. You can follow Kent on Twitter @ThinkersQuill. |

| David Merkel: On Insurance Investing Posted: 10 May 2013 03:00 AM PDT David Merkel writes: This piece is the sixth out of seven in a series that I have been writing at Aleph Blog. Here are links to the first five pieces:

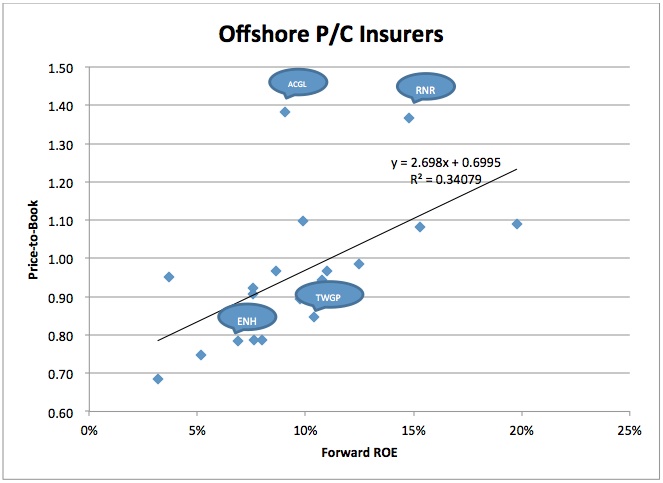

Recently I decided to spend some time analyzing the insurance industry. It's a different place today than when I became a buy-side analyst ten years ago. Why? First, for practical purposes, all of the insurers of credit are gone. Yes, we have Assured Guaranty, and MBIA is limping along. Old Republic still exists. Radian and MGIC exist in reduced states. The rest have disappeared. In one sense, this should not have been a surprise, because the mortgage and credit guaranty businesses never had a scientific model for reserving. I'm not even sure it is possible to have that. Second, the title insurers are diminished. Some, like LandAmerica are gone. Fidelity National seems to be diversifying itself out of insurance, buying up a restaurant chain last year. Third, health insurers face an uncertain future. Obamacare may disappear, or Obamacare could slowly eliminate insurers. It's a mess. Insurers debate to what degree they should compete in insurance exchanges. But beyond all of that, valuations are fair-to-cheap across the insurance industry. Part of that may stem from ETFs. Insurers as a whole are smaller than the banks, but not as much smaller as they used to be. Now, if you are a hedge fund, and you want to short banks, you probably have the best liquidity shorting a basket of financials, which shorts insurers as well. That may be part of the issue. There are other aspects, which I will try to address as I go through subindustries. Offshore By "Offshore" I mean P&C reinsurers and secondarily insurers that do business significantly in the US, and who list primarily on US exchanges, but are not based in the US. Most of them are located in Bermuda. In 2011-2012, many of them were challenged by the high levels of catastrophes globally. But the prices of the reinsurers did not fall because pricing power returned, and investors expect higher future earnings as a result. Before I go on, I need to explain that what I will use to give a rough analysis of value is a Price-to-Book vs Return on Equity analysis [PB-ROE]. For more details, you can read my article here. The short explanation is that companies in the insurance business (and other financials) are constrained by the amount of equity (net worth) that they have. The ability to earn a return as a percentage of the equity [ROE] drives the market valuation as a fraction of the equity [P/B]. Here is a scatterplot for PB-ROE for the Offshore group:

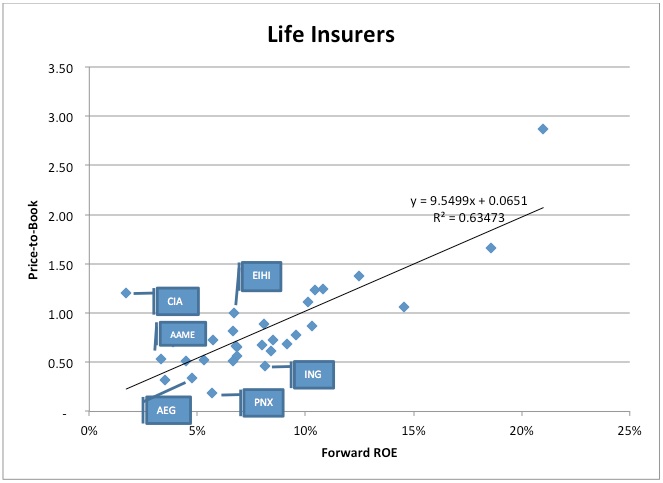

Companies above the line may be overvalued, and companies below the line may be undervalued. ROE is what is expected by analysts for the next fiscal year, not what has been obtained in the past. The fit is fairly tight, and indicates mostly logical valuations for this group. The companies that are possibly overvalued are: Arch Capital [ACGL] and Renaissance Re [RNR]. Possibly undervalued: Tower Group [TWGP] and Endurance Specialty [ENH]. Now, this simple model can fail if you have an intelligent management team that has a better model. Arch Capital and Renaissance Re may be that. But with an expected ROE of less than 20%, it is hard to justify their valuation, when the average stock in this group needs an expected 11% ROE to be valued at book. Why such a high ROE to get book? Earnings quality. Reinsurers have noisy earnings due to catastrophes. You don't give high valuations to companies that run hot or cold. But the trick here is to see who is accumulating book value the fastest – they tend to be the stars over time. Endurance and Arch have been good at that. Life The life insurance business would be simple, if it indeed were only life insurance. Much of the industry is handed over to annuities, and all manner of asset gathering. Even life insurance can be made more complex through variable and variable universal life, where assets are invested in stocks, and do not receive a rate from the company. Part of the trouble is that variable products are not simple, but the insurers offer guarantees for a fee. When I see those products, my reaction is usually, "How do they hedge that?!" Thus I am concerned for insurers that are "equity-sensitive" as I reckon them. Here is the PB-ROE scatterplot:

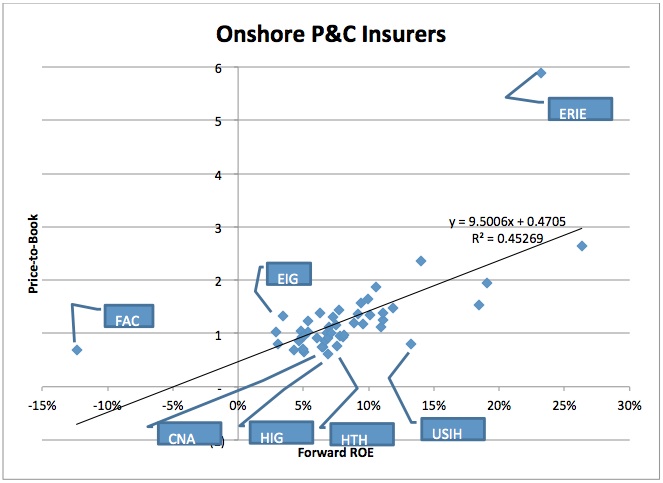

A tight fit. The insurers that are seemingly undervalued are equity-sensitive ones: Phoenix Companies [PNX], Aegon [AEG], and ING [ING]. Those that are overvalued are Citizens [CIA], Eastern Insurance Holdings [EIHI], and Atlantic American [AAME]. For the undervalued companies, I am unlikely to buy because I am skeptical of the accounting. I would look further down the list and consider buying some companies that are more reliable, like Assurant [AIZ], National Western [NWLI], and Fortegra Financial Corp [FRF]. One more note: to get book value in Life Insurance, you need a 9.8% ROE on average. That's high, but I expect that is so because investors are skeptical about the accounting. Property & Casualty This graph gives PB-ROE for the entire onshore P&C insurance industry:

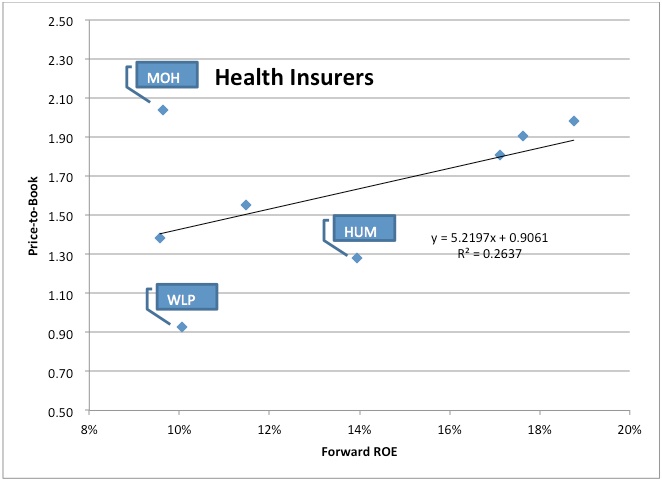

It's a good fit. Again, the casualties of the last year weigh on the property-centric insurers, but for the most part, this is logical. Potential underperformers include First Acceptance [FAC], Employers Holdings [EIG], and Erie Indemnity [ERIE]. Below the line: Hartford Financial Services [HIG], Hilltop Holdings [HTH] Hartford Financial [HIG], and United Insurance Holdings [USIH]. Again, these are only screening tools. Before buying or selling, understanding management and reserving quality, and riskiness of the lines of business makes a considerable difference. Erie Indemnity has an "asset light" model where it manages insurers, but does not bear underwriting risk. Hartford has a significant life insurance and annuity exposure. Models are models, and we have to understand their limitations. Health With Obamacare, I don't know which end is up. It could end up being a giant sop to the health insurers, or it could destroy the health insurers in order to create a government single-payer model, rather than the optimal model for cost reduction, where first parties pay directly, or pay insurers. You want reductions in medical costs, get the government out of healthcare, and that includes the corporate deduction for employee health insurance. My rationale is this: it could mess up the private market enough that the solution reached for is a single payer solution. I've talked with a decent number of health actuaries on this. The ability to price risk is distinctly limited. Young people pay too much, older folks too little. That's a formula for antiselection. I think Obamacare was badly designed. I will not achieve its ends, and when the expenses start coming in, they will be far higher than anticipated. That has been the experience of the government in health care in the US. Utilization is underestimated, the further removed people from feeling its costs. There are many models for profitability here, which makes things complex, but here is the present PB-ROE graph:

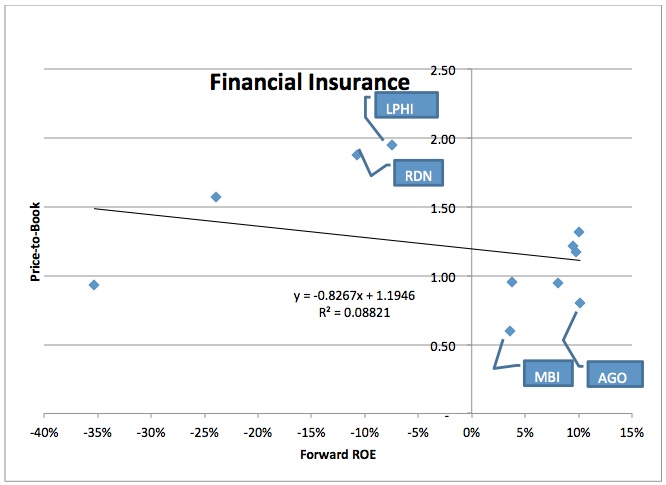

It's an okay fit, with the idea that the following companies might be undervalued: Wellpoint [WLP] and Humana [HUM]. And the following overvalued: Molina Healthcare [MOH]. I don't regard myself as an expert on the health insurance sub-industry, so treat this with skepticism. I include it for completeness, because I think the PB-ROE concept has value in insurance. One more note, the PB-ROE model thinks of this as a safe investment subindustry, because to have a book value valuation, you have to have an ROE of 1.8%. Financial Insurers This group comprises the surviving mortgage, title and financial insurers, and two companies in the ghoulish business of buying life insurance policies from sick people. Here's the PB-ROE graph:

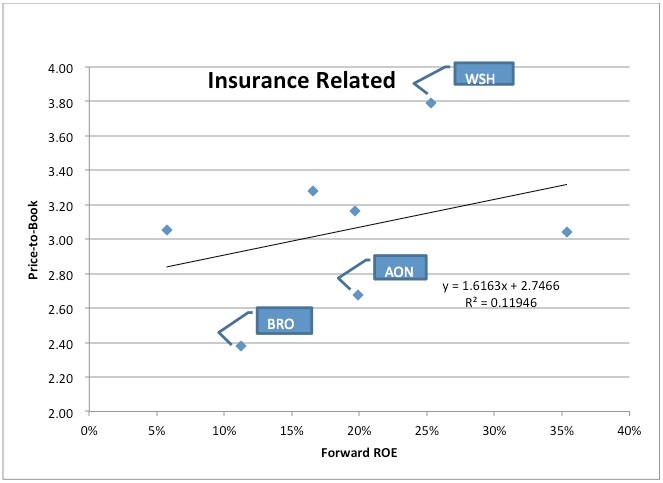

This graph is weird, because it slopes down, and does not have a good fit. That's because we've been through a rough period financially, and in many cases GAAP accounting does not do a good job with these companies that take a lot of credit risk. We can still look for companies that have high price-to-book, and low ROEs – note Life Partners [LPHI] and Radian [RDN] as possible sell candidates. We can also look for companies that have low price-to-book, and high ROEs – note Assured Guaranty [AGO] and MBIA [MBI] as possible buy candidates. This subsector is more difficult than most, because credit is not an underwritable risk. It is feast and famine. We are in a period of feast now, so in some ways what is bad is good. The more risk, the more return. But winter may come soon – who knows what the Fed may do? In general, I avoid this subsector for longs. Insurance-Related Companies This is a group that is a non-group. It comprises brokers and insurance service providers. Here's the PB-ROE graph:

It doesn't look like much of a group. As it is the potential outperformers include Brown & Brown [BRO], and Aon [AON], two leading insurance brokers. A potential underperformer Willis Group [WSH], another leading insurance broker. Summary Insurance is complex, and the accounting is doubly complex, which is a major reason why many stay away from it. But insurers as a group have had reliable and outsized returns over the rememberable past, which should encourage us to do a little kicking of the tires when a decent amount of the industry trades below its net worth and is still earning money with little debt. In my opinion, this is a recipe for earnings in the future, and why I own a lot of insurers for myself, and for clients. In the final part of this series, I will go over some nuances of insurance accounting – I leave it to the end because it is kind of dull, but can make a lot of difference, because some companies look cheap and aren't really cheap. Full disclosure: long AIZ, ENH, NWLI for clients and myself

~~~ David J. Merkel, CFA is Principal of the equity and bond asset management firm Aleph Investments, LLC, and writes The Aleph Blog. Previously, he was the Director of Research for Finacorp Securities, Senior Investment Analyst at Hovde Capital, and a leading commentator at RealMoney.com. |

,” Journal of Banking and Finance, vol. 33 (November), pp. 2036-49. The systemic expected shortfall uses firm equity prices, leverage, and volatility to measure the propensity of a firm to be undercapitalized given a marketwide decline in equity prices; see Viral V. Acharya, Lasse H. Pedersen, Thomas Philippon, and Matthew Richardson (2010), “

,” Journal of Banking and Finance, vol. 33 (November), pp. 2036-49. The systemic expected shortfall uses firm equity prices, leverage, and volatility to measure the propensity of a firm to be undercapitalized given a marketwide decline in equity prices; see Viral V. Acharya, Lasse H. Pedersen, Thomas Philippon, and Matthew Richardson (2010), “

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment