The Big Picture |

- 10 Monday PM Reads

- Fisher on “Feral Hogs”

- World’s Shortest Analyst Report

- A Commotion to Wake the Dead

- 10 Monday AM Reads

- Look Out Below, Sell Off Continuation Edition

- How Jeff Gundlach Made His Financial Mark

- Hilsenrath: Markets Misreading Fed’s Messages

| Posted: 24 Jun 2013 01:30 PM PDT My afternoon train reads:

What are you reading?

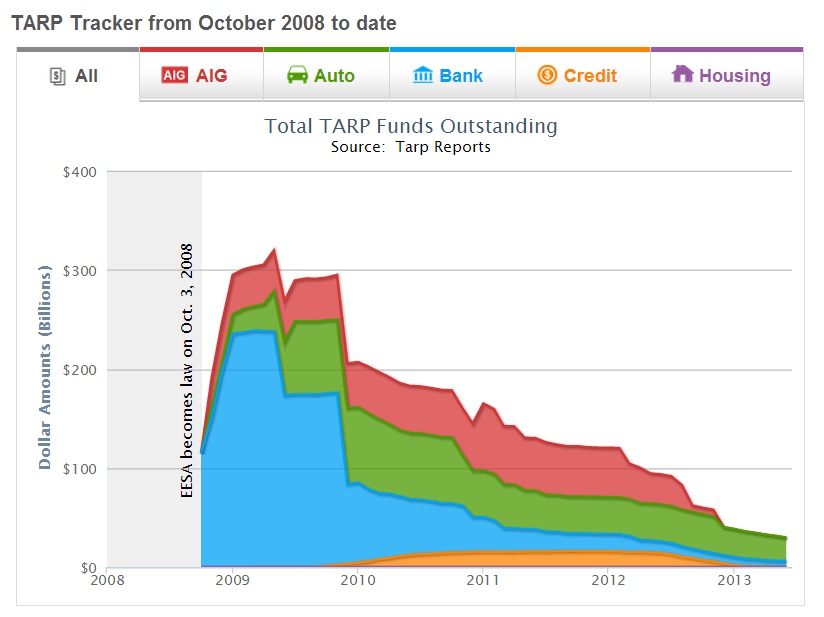

TARP Tracker from October 2008 to date |

| Posted: 24 Jun 2013 01:00 PM PDT

|

| World’s Shortest Analyst Report Posted: 24 Jun 2013 11:30 AM PDT

Hat tip Mike P

|

| Posted: 24 Jun 2013 08:30 AM PDT A Commotion to Wake the Dead

The following is the June 15th monthly strategy note that went to asset management clients of the Ritholtz Group. These are normally not distributed publicly, but given the current bond market turmoil, we thought it might make for interesting reading. If you have any questions about asset management please contact us at TheRitholtzGroup-at-FusionInvest-dot-com ~~~

This week, the entirety of the nation's investment management complex gathered in Chicago for the 25th annual Morningstar Investment Conference. From Wednesday through Friday, financial advisors sat at their banquet tables furiously scribbling notes as all the big names came out and did their predicting-the-future routines, from macro calls to stock picks. World-class quants Michael Mendelson (AQR) and James Montier (GMO) both took the stage, as did esteemed speakers from BlackRock, Vanguard, RiverNorth, T. Rowe Price, JPMorgan, PIMCO, Fidelity, Artisan, Franklin Templeton, Sage, Virtus, Brandywine, Janus and every other brand-name fund company you've ever heard of. Some were bullish, some were bearish, some were cautiously optimistic, some were recklessly pessimistic. Some talked of Europe while others focused on Asia, some were concerned about stock valuations while others were worried about bond yields. Some applauded the Fed for saving the economy in the recent past while others criticized it for jeopardizing the future. And after three straight days of very smart, well-groomed people regurgitating all of the clever, contradictory things they'd read in research reports and newsletters, I can only assume that the audience was utterly befuddled. So many articulate speakers, so many viewpoints, so many headwinds and risk factors and silver linings and unknowns and known unknowns….a complete overload, almost none of it particularly original or utilitarian. James Montier, as brilliant as anyone there, did an entire talk about why investors should do nothing right now – literally, he was lecturing on the virtues of inaction and quoting directly from the Tao of Pooh. And then, for the last presentation of the event, it was time for something completely different. My friend Carl Richards, a former financial advisor, creator of the Behavior Gap blog and contributor to the New York Times, closed out the conference as the final keynote speaker on Friday. I can picture him ascending the steps toward the podium, an easy gait and nonchalant manner distinguishing him from the other speakers before he even utters a word. Carl's berth on the heels of all these presenters, panels, picks and predictions is too serendipitous to have been an accident. He uses his time to make a very simple statement that jars the entire crowd of professionals back to reality: "When clients pay attention to noise, we call it dumb. When advisors do it, we call it research. I doubt Carl made any friends among the other three dozen speakers with that quip, but I'll bet it was the most profound remark coming from the stage all week. *** One of the most difficult aspects of running an asset allocation portfolio in the modern era is knowing what's noise and what's important. Barry and I haven't been able to quantify it mathematically, but our best guess is that actual important facts and news stories are outnumbered by sonic booms of nonsense at a rate of 100-to-1. As a fun thought exercise, punch in the ticker symbol of Apple Inc (AAPL) on Yahoo Finance some afternoon. Count the headlines that are ostensibly about Apple and then randomly click into every third or fourth story. You will find virtually nothing of value in any of these stories – and yet there will be between fifty and one hundred of them published each day of the week. Now imagine this writ large; extrapolate this noisiness across a US market containing thousands of stocks, not to mention ETFs for every conceivable country, commodity and investable index. The cacophony of half-truths, speculations and prognostications about any given financial topic has the power to deafen but certainly not to inform. This is not to say that we have the luxury of ignoring the ebb and flow of data and opinion. Our job is to, firstly, be aware of all that occurs. Secondarily, we must be able to contextualize the things we're seeing and hearing into a coherent framework. Reacting to information, however, is a tertiary task in our view, which sets us apart from the roving bands of "trade first, think later" gunslingers that are so prevalent on the open range these days. Which brings me to our current posture in the Core Asset Allocation models and the events of the coming week. Over the last month there's been quite a disruption occurring in the bond market and in various patches of the equity markets that offer "bond-like" dividend yields. In late May, an airing of the Fed's latest meeting minutes shook the global financial system as a consensus formed that the Fed was contemplating a reduction in its monthly bond-buying. On this "news", bond prices dropped and yields shot up as expectations of a more tapered approach from the Fed rippled outward from the treasurys complex. Bank of America Merrill Lynch keeps a Global Broad Market Index which tracks more than $40 trillion in bonds and it believes that these bonds have fallen an average of 1.1% between May 21st and June 13th. You'll note that nothing of any concrete nature has occurred nor have any of the Fed governors actually made any statements to this effect. And yet bond yields saw one of their sharpest jumps in history. Once treasurys began to plunge, it was only a matter of time before all income-producing assets, from Utilities and REITs to Emerging Market Bonds and Junk Corporates began convulsing. It's been estimated that a total of $3 trillion has been lost across all income and dividend securities since this bond back-up began. This week the Federal Reserve has an opportunity to either allay or exacerbate the market's fears over the longevity of their quantitative easing program. The Wall Street Journal's Jon Hilsenrath, who is said to be conducting an ongoing dialog directly with the Fed Chairman, thinks that the answer to our burning questions will be found in the Fed's economic outlook report – not in the committee's actual statement or in Bernanke's press conference remarks. And while we have no idea what will be said, how it will be construed or what the market will do afterward, we do know for a fact that there will be plenty of noise – a racket to end all rackets, a commotion to wake the dead. Most of what we hear will not be important. Some of what we hear will be filed away or added to our foundational understanding of the environment around us. Little (if any) of what we hear is likely to force us into making any kind of large-scale or dramatic changes to our forward outlook or current portfolio posture. In January of 2013, we had made the conscious decision to substantially underweight the bond portions of our allocation models in preparation for exactly this sort of increasing volatility and diminished "safe haven" status. While volatility in stocks is both expected and even desired by long-term investors, it is certainly not a welcome feature in bond investing. In a multi-asset model, we'll always prefer to take our volatility where there is the potential for long-term growth and capital appreciation – on the equity side or your portfolio. In light of this, our current allocation to fixed income in Core Models vs their benchmarks is as follows:

It is possible that the back-up in bond yields continues in the wake of Chairman Bernanke's remarks given the skittishness of the global investment community. It is also possible that the carnage across high-yielding asset classes continues as well. Should this be the case, our approach will be to pay as little attention to the resultant noise as possible and to pounce where long-term opportunities present themselves. Our underweights toward global fixed income give us the flexibility to do exactly that. * * * Original Source: Ritholtz Group Strategy Note, June 15, 2013, Joshua M. Brown. Please note any questions about asset management should be directed to TheRitholtzGroup-at-FusionInvest-dot-com |

| Posted: 24 Jun 2013 07:00 AM PDT My morning reads:

What are you reading?

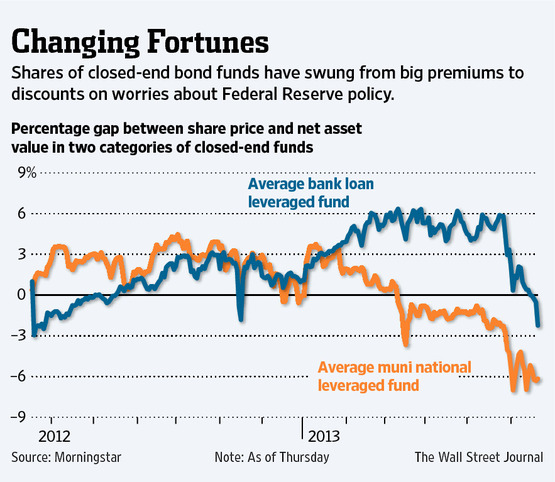

Closed-End Funds Bite Back |

| Look Out Below, Sell Off Continuation Edition Posted: 24 Jun 2013 04:15 AM PDT click for updated futures

Good Monday morning: The lovely weekend weather has been replaced with hot humid & steamy Summer heat. The markets are also skipping the pleasantries and rushing headlong into the a summer melt down. No cavalry came to the rescue after last weeks minor carnage. Hence, the summer swoon begins pretty much on time, where prior swoons began. What is somewhat different this go round is the unlikely market rescue by the Fed. Unlike prior interventions, QE4 is open-ended and continuous. Hence, we will not likely see a grand announcement about a new plan which will excite traders. Instead, we are most likely to hear minor notes and course correction discussions as various Fed agents discuss and debate policy in public. We may also hear more often from the Fed’s chosen conduit to the Street, Jon Hilsenrath. Understand that the reaction to the inevitable tapering of QE will be neither rational nor timely, but rather the typical emotion driven trading that makes up most of the daily noise. We can also expect an outsize reaction — or overreaction — as potential replacements for current FOMC chair Ben Bernanke get floated in various trial balloons. I am less convinced that we actually know what is driving these markets than most of us believe. QE Tapering, lots 0f earnings pre-announcements, China’s credit crisis, even just a market that has run too far too fast are all equally valid explanations. Some combination or perhaps none of the above are also just as valid explanations as why the rationales are likely right or wrong. Regardless of who the next Fed Chair is, they will confront the same issues as the current chairman: A post credit-crisis economic recovery which is softer than we prefer, marked by weak GDP gains and mediocre job creation. They will face a huge balance sheet that will require 7 or so years to run off its excess holdings, a financial sector that still has too much bad paper on its books but a huge appetite for leverage and risk, which helped to create a market that has run up 146% despite an investing public that is completely disinterested. Despite excellent benefits, you have to wonder who really wants this job. ~~~ More to come later

|

| How Jeff Gundlach Made His Financial Mark Posted: 24 Jun 2013 03:30 AM PDT |

| Hilsenrath: Markets Misreading Fed’s Messages Posted: 24 Jun 2013 03:00 AM PDT Since Fed Chairman Ben Bernanke said the central bank expects to curb its big bond-buying program later this year, markets tumbled. But, a close look at his comments and Fed official's interest-rate projections show the Fed took several steps aimed at sending the opposite signal. 6/21/2013 4:29:39 PM4:02 |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment