The Big Picture |

- ECB, Euro, USD, Interest Rates

- Comedians In Cars Getting Coffee: Kevin Hart

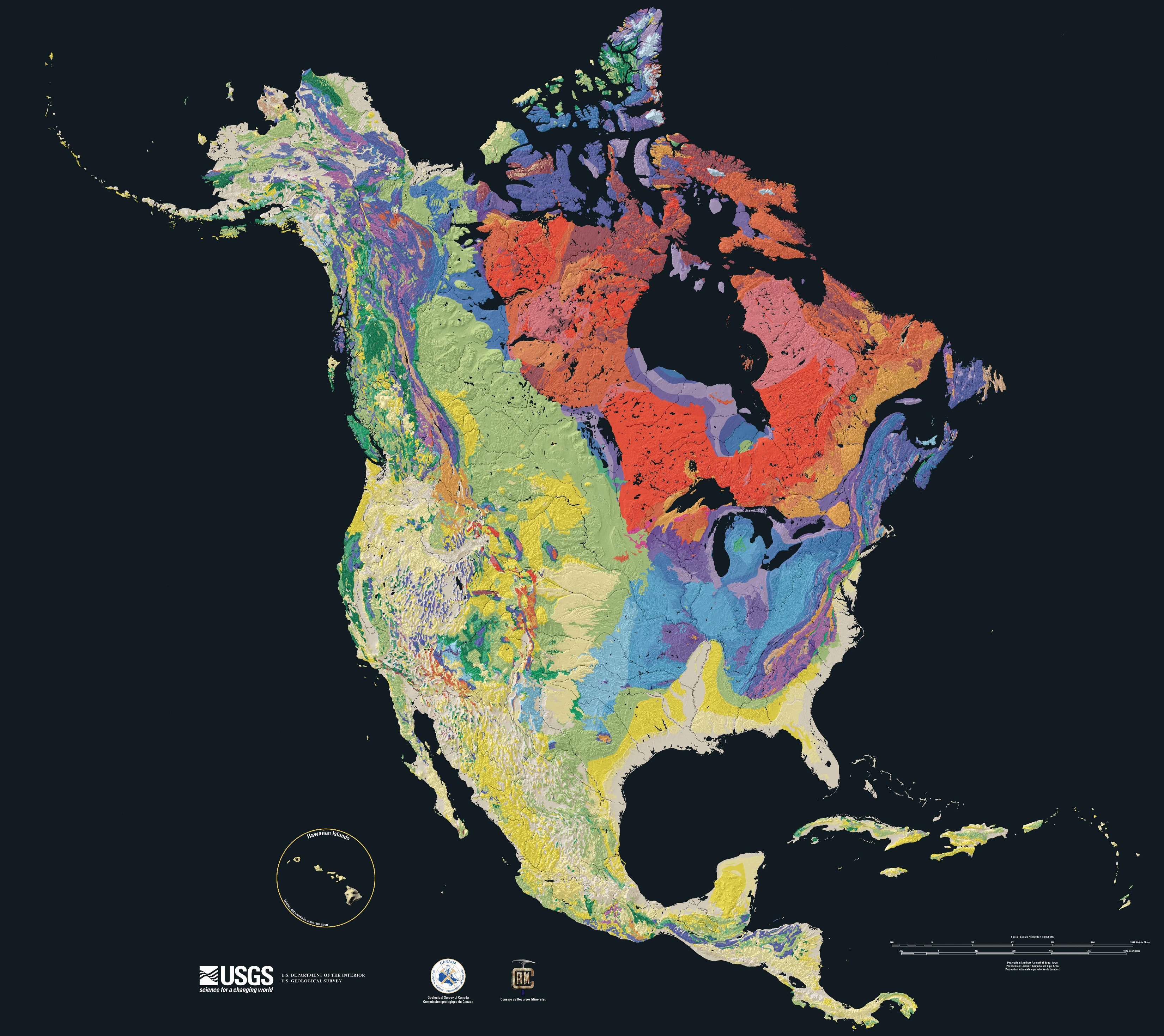

- North America’s Geological History

- Forecasting is Marketing . . .

- MiB: Bill Gross, Part II

- 10 Weekend Reads

| ECB, Euro, USD, Interest Rates Posted: 25 Jan 2015 02:00 AM PST ECB, Euro, USD, Interest Rates

After a two-and-a-half-year wait for "whatever it takes," the quantitative easing (QE) announced this week by the European Central Bank (ECB) is different from the QE undertaken by the Federal Reserve (Fed) during and after the financial crisis and now completed. The European action comes in the aftermath of the Fed's programs and is a European attempt to confront complex economics. In the 2008–2014 Fed version, QE injected liquidity into markets that were frozen. More QE was then piled on as the Fed expanded its holdings of federally backed securities. A single sovereign guaranteed that debt, and that was the United States government. The QE process quickly drove the short-term interest rate to zero but not below zero. Over time the longer-term interest rates followed a similar path to lower and lower levels. The reduction in interest rates translated to reduced mortgage and corporate-financing costs. The process has continued for seven years. A refinancing apparatus could then develop in the US economy as one agent after another took advantage of persistently lower interest rates. Lenders adjusted to the new notion of lower interest rates for longer periods. Investors were hit by financial repression as their savings instruments matured and rolled over into lower interest rates. That process is ongoing in 2015. In the US, behaviors changed over the course of seven years. Positions that were initially viewed as being temporary started to seem permanent. Forecasters warned, "The Fed is printing all this money; we'll have a big inflation; interest rates will skyrocket; and the economy and markets will go in the tank." The warnings were repeated ad infinitum in the media. They were debated by some. Cumberland Advisors numbered among the debaters. We argued "no." We were in the minority. Over and over again we heard predictions of hyperinflation and higher interest rates. We said "no." We heard all of the outcomes that would be terrible as a result of QE. We said "no." Seven years on, the debate continues, with the detractors predicting doom. Meanwhile, in the United States, interest rates are very low. There is minimal inflation. The economic recovery is strengthening. The American stock markets reached all-time highs within the last month. The detractors are still predicting the end of the world. Someday they may be correct. But not in January, 2015. At Cumberland we still say "no." Not yet! Seven years later in the US we can now add a major oil shock to the economic positives. With QE-induced refinancing in place and with growing intensity in our economic recovery, the outlook is simply marvelous. In 2015, our growth will be above 3%, employment will improve, and inflation will remain low. The positive trends continue and are becoming more robust. In addition, we have the world's strongest major reserve currency, with a long run still ahead of it. And we have a better fiscal balance in the US than most nations enjoy. In the US, QE was controversial and still is. Meanwhile, look at results. It worked. Examine the same issues in the Eurozone and the ECB, and we see a different picture than in the US. The ECB will be acquiring over €1 trillion in sovereign debt. Their allocation method is quite different from the Fed's. They have to deal with the sovereign debts of different countries that have different levels of creditworthiness, ranging from junk-bond status in Greece to the highest-grade status in Germany and Finland. There is no inflation and no expectation of inflation in the Eurozone. Interest rates for the debt of the very highest-grade sovereigns are already next to zero in the Eurozone. The same is true for nearby sovereigns like Sweden and for Switzerland. In all of Europe, interest rates on longer-term sovereign debt are remarkably low and mostly lower than in the US. Italy's 10-year benchmark sovereign debt touched 1.4% on Friday. Spain reached 1.25%. In Germany, the sovereign benchmark for the Eurozone, the 30-year bond yield is 1%, and the 10-year note is 0.2%. All German maturities under 5 years are trading at negative yields. QE by the ECB will not lower interest rates — they are already at or near zero. In fact, the ECB has announced it will acquire sovereign debt even if the yield is negative. Think about that. The central bank will be creating money in order to pay the various sovereign governments for the privilege of buying their debt. That is how a negative interest rate works. Meanwhile, the fiscal situation in Europe is still under repair, a process that will take many years. In countries like France, a great portion of the economy, more than half, is driven by the government. Italy is another case study of a huge burden of social promises and a deficient funding mechanism to pay for them. Greece is a mess without easy answers. Others in Europe no longer care whether Greece exits the Eurozone. Many hope that they do, because it is nearly impossible to throw any country out. Grexit (the term for a Greece exit from the Eurozone) would be welcomed by other peripheral countries, although the celebration in those countries would be a quiet one due to the observance of political correctness. To be blunt, the divisions in Europe cannot be healed by QE. The promises that are expensed as social benefit payments act to reduce productivity and restrain growth. This fiscal reality cannot be cured by QE. In fact, there is no liquidity shortage in Europe for QE to fix. QE is not a reform mechanism for euro-sclerosis. QE cannot cure sick governance. It cannot lower interest rates when they are at zero. It cannot stimulate credit expansion when there is no credit demand. If zero interest rates won't work, a continuation of zero interest rates also won't work. So what does QE do? In Europe, QE transfers the fiscal failure of the sovereign states involved to the monetary authority, the European Central Bank. The ECB creates money. The money is used to buy the sovereign debt of Eurozone members at an interest rate of zero or near-zero. The sovereign debt the ECB buys is likely to be held for years. It must be viewed as a permanent structure, just as it has become in Japan. The ECB will not be "tapering" in this decade. Maybe it will do so in the next decade. The proceeds of the issuance of sovereign debt will fund the social promises that governments cannot otherwise keep. Contrast that situation with that in the US, where the annualized government deficit is nearly $1 trillion smaller than it was at its worst in 2009. In Europe, QE is a circular mechanism. It has no multiplier in the credit arena. It inspires no productivity gain from investment by the private sector. It is merely circular. So, if it is circular, why have QE? There is one element that works with QE, whether in the US or Europe. We have seen it work in the US, and we will see it work in Europe. QE withdraws duration from the market and transfers it onto the government's books. The market then seeks to replace the duration in its asset mix. That is why asset prices rise when QE occurs: asset prices rise when duration is in demand, and they fall when duration is in supply. When central banks extract duration from the market, it has to be replaced with something else. Stocks are long-duration assets. Real estate is a long-duration asset. Collectibles and precious metals are long-duration assets. Patents and other forms of intellectual property rights are long-duration assets. Cash is not long-duration. The duration of cash is one day. In the US, QE has resulted in record stock market prices. They are still rising. QE has resulted in higher real estate prices. They are still rising. QE adds to the upward direction of asset prices and the accumulation of wealth by the wealthy. We see it in the statistics that track wealth and in the statistics that are derived from the income streams owned by the wealthy. Wealth effects operate with a time lag. There is a slight transfer each year from accumulated wealth into consumption spending and hence into economic growth. It is a small percentage. From a higher and rising stock market, we estimate that transfer to be 1%-2% in any given year. If stock market wealth rises and there is a positive and permanent wealth effect of $100 over the course of the year, an additional $1 to $2 in annual spending transfers slowly to economic growth. We see that at work in the US. We will see it at work in Europe as well. There is a higher transfer when real estate prices rise and are viewed as permanently heading higher. The financing mechanism for housing has a multiplier that is greater than the financing mechanism applied to financial assets. That makes sense since the credit multiplier for housing is higher than for stocks. For example, stocks can sit in your 401(k) unleveraged, while houses are mortgaged and do not sit in 401(k)s. Therefore the transmission mechanism from higher housing wealth is more robust than the transmission mechanism from higher stock prices. Yale Professor Bob Shiller notes that housing wealth effects can reach 3% to 5% a year. We already see some of those effects in the US, thanks to QE. As housing becomes more robust, we will see more of the positive housing wealth effects in the US. We will see a little of this happening in the Eurozone. The conclusion is that the extended and predictable period of QE in Europe will give some positive stimulus to economic growth via the wealth-effect transmission method. It will not be a panacea for Europe's problems. Monetary policy cannot fix fiscal policy errors or the suppression of production by governments, but monetary policy can raise asset prices. In Europe it will do so. In the US it already has done so, and the rise is not over. At Cumberland Advisors, we remain fully invested in the US stock market in our exchange-traded fund (ETF) strategies. We are focused on domestic businesses. Our largest overweight is the utility sector. It is 95% domestic, so its corporate entities do not have to worry about foreign currency translations impacting their earnings. The sector benefits from a slowly and steadily growing US economy. It pays dividend yields that exceed the riskless interest rate from Treasury notes. It is defensive and less volatile than other sectors in a period when volatility is rising. Our international ETF strategies have a majority of components that are currency hedged. Our outlook for the dollar is a prolonged period of strengthening. We expect a lot of adjustment vis-à-vis the other currencies that are involved in the present historic restructuring of monetary policy. Those currencies will weaken relative to the dollar. It is conceivable that the yen could reach 135 or 150 to the dollar over a period of several years. It is conceivable that the euro-dollar exchange rate could be 1.00, 0.90, or 0.85 over the next two or three years. The range of possibilities is unknown, and the confidence intervals on such estimates are very wide. Imagine a world where the US central bank policy rate is 1% and the Eurozone central bank policy rate is minus 0.2%. The math suggests that the dollar would then strengthen by 1.2% a year against the euro. Compare the current 10-year German Bund at 0.2% to the 10-year US note. The difference is 1.7%. That math suggests the dollar will strengthen 17% against the euro over the next 10 years. Please note that this is a very simplified model. The actual way this comparison is done is much more complex, but the concept is the same. Interest-rate differentials explain longer-term movements in currency exchange rates. We cannot fully estimate what euro-dollar exchange rates will be. The truth is, nobody knows. We anticipate the volatilities associated with this massive transition in policy to reach new levels. That means lots of activity in managed portfolios and a need for the portfolio manager to be nimble and move quickly when required. Volatility is bidirectional. It is scary when it causes prices to accelerate if they fall. It is frightening at inflection points. And it is exhilarating when it enables prices to head upward. Expect all of the above in 2015. ~~~ David R. Kotok, Chairman and Chief Investment Officer, Cumberland |

| Comedians In Cars Getting Coffee: Kevin Hart Posted: 24 Jan 2015 05:00 PM PST

|

| North America’s Geological History Posted: 24 Jan 2015 02:00 PM PST |

| Forecasting is Marketing . . . Posted: 24 Jan 2015 08:00 AM PST It's time to market forecasters to admit the errors of their ways

I come not to praise forecasters but to bury them. After lo these many years of listening to their nonsense, it is time for the investing community — and indeed, the seers themselves — to admit the error of their ways. Most forecasters are barely cognizant of what happened in the past. And based on what they say and write, it is apparent (at least to this informed observer) that they often do not understand what is occurring here and now. So there's no reason to imagine that they have the slightest clue about the future. Economists, market strategists and analysts alike suffer from an affinity for making big, frequently bold — and most often, wrong — pronouncements about what is to come. This has a pernicious impact on investors who allow this guesswork to infiltrate their thinking, never for the better. I have been beating this drum for more than a decade. What say we finally put a fork in Prediction, Inc.? There is a forecasting-industrial complex, and it is a blight on all that is good and true. The symbiotic relationship between the media and Wall Street drives a relentless parade of money-losing tomfoolery: Television and radio have 24 hours a day they must fill, and they do so mostly with empty-headed nonsense. Print has column inches to put out. Online media may be the worst of all, with an infinite maw that needs to be constantly filled with new and often meaningless content. Just because the beast must be fed does not mean you must be dragon fodder. (More on this later.) The other partner in this mutually beneficial dance is the financial industry. Forecasting is simply part of its marketing strategy. There are two principle approaches to meeting the media's endless demand for unfounded guesses about the future. Let's call them a) Mainstream and b) Outlier. The Mainstream strategy is simple: Take the average annual change in whatever the subject at hand is and extrapolate forward a year. Voila! You have a mainstream forecast. If you are talking about equities, predict an 8 to 10 percent gain in the Standard & Poor's 500-stock index. For economic data, project out the past 12 months forward. You can do the same for gross domestic product, unemployment, commodity prices, bonds, inflation, just about anything with a regularly changing data series. If you are feeling puckish, you can shade the numbers slightly up or down to separate your prediction ever so slightly from the rest of the pack — just to keep it interesting. As Lord Keynes once said, better to fail conventionally than succeed unconventionally. A perfect example is the recent collapse in oil prices. Having completely missed the 50 percent drop that occurred over 2014, analysts are now tripping all over themselves to forecast $40, $30, $20 per barrel in 2015. Since their prior guesswork completely missed the biggest energy story in decades, why should any of us care about their current guesswork? Then there is the Outlier approach, where a wildly unorthodox forecast is made. The prognosticator predicts the Dow Jones industrial average at 5,000 when it's three times that, or hyper-inflation, or $10,000 gold, or a 1 percent yield on the 30-year treasury bond, or a collapse in the Federal Reserve's balance sheet. If it comes to pass, the forecaster is feted as a rock star. If not, most people forget. (Although some of us actually track these outlier forecasts). Those in the prediction industry are pernicious survivors. They understand how to play on the human psyche to great advantage. Like the cockroach, they adapt well to conditions of chaos or uncertainty. There is a flaw in the human wetware that leads to a demand for even more (bad) predictions. The evolutionary propensity that humans suffer from is the desire for specific predictions from self-confident leaders. This is demonstrated in a wealth of academic data about forecasting track records. Research has shown there is a high correlation between a forecaster's appearance of self-confidence and believability. Unfortunately, there is an inverse correlation with accuracy, for reasons revealed by the Dunning and Kruger studies on metacognition and self-evaluation. Same with specificity: Studies show that the more precise a prediction, the more likely it will be believed, and the less likely it is to be right. These (and other) factors set up viewers to have the most faith in the people who are least likely to be right. Perhaps the biggest issue of all is the most obvious: Human beings, in general, stink at predicting the future. All of you. History shows us that people are terrible about guessing what is going to happen — next week, next month, and especially next year. In other words, expert forecasts are statistically indistinguishable from random guesses. What should investors do instead of paying attention to these unsupported, mostly wrong, exercises in futility called forecasting? I suggest three simple things:

It is important for investors to understand what they do and don't know. Learn to recognize that you cannot possibly know what is going to happen in the future, and any investment plan that is dependant on accurately forecasting where markets will be next year is doomed to failure. Never forget this simple truism: Forecasting is marketing, plain and simple. ~~~ Ritholtz is chief investment officer of Ritholtz Wealth Management. He is the author of "Bailout Nation" and runs a finance blog, the Big Picture |

| Posted: 24 Jan 2015 07:00 AM PST This week, the "Masters in Business" podcast features Part 2 of an interview with Bill Gross, formerly of Pimco, now with Janus Capital; Part 1 is here. Gross sat down with me in the Bloomberg studios in New York for an extensive two-hour interview. In part II, we discuss the Allianz takeover of Pimco, why he is a tough boss to wrk for. He said he was fired by Pimco, and was blindsided by the coup. We also talk QE and the Fed, what they did right and wrong, and what he wants to do at Janus. He also said quite a few surprising things about the Federal Reserve. You can hear it live on Bloomberg radio, download the podcast here or on Apple iTunes or stream it on Soundcloud (below). All of our prior podcasts are available on iTunes.

|

| Posted: 24 Jan 2015 04:30 AM PST Good Saturday morning. Pour yourself a strong cup of Sumatra, settle into your favorite chair, and enjoy our longer form weekend reads:

Be sure to check out part 2 of my interview with Bill Gross in our Masters in Business series.

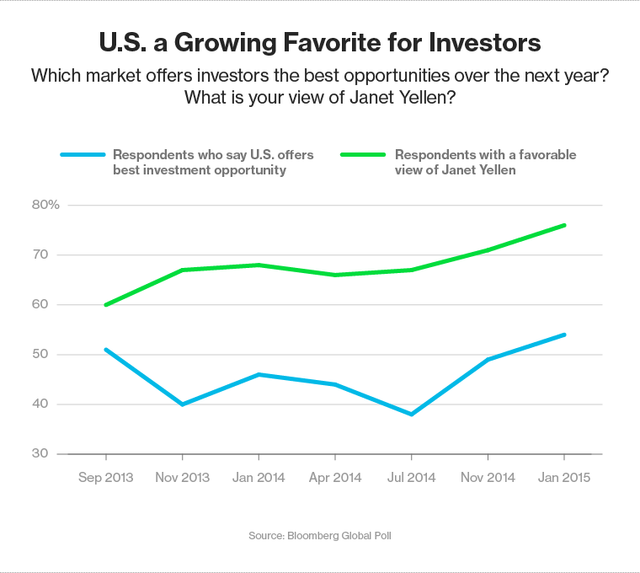

U.S. Markets Favored by Investors, Bright Spot in Dim Global Economy |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

0 comments:

Post a Comment