The Big Picture |

- Why Is Wage Growth So Slow?

- Our Upcoming Seattle Trip!

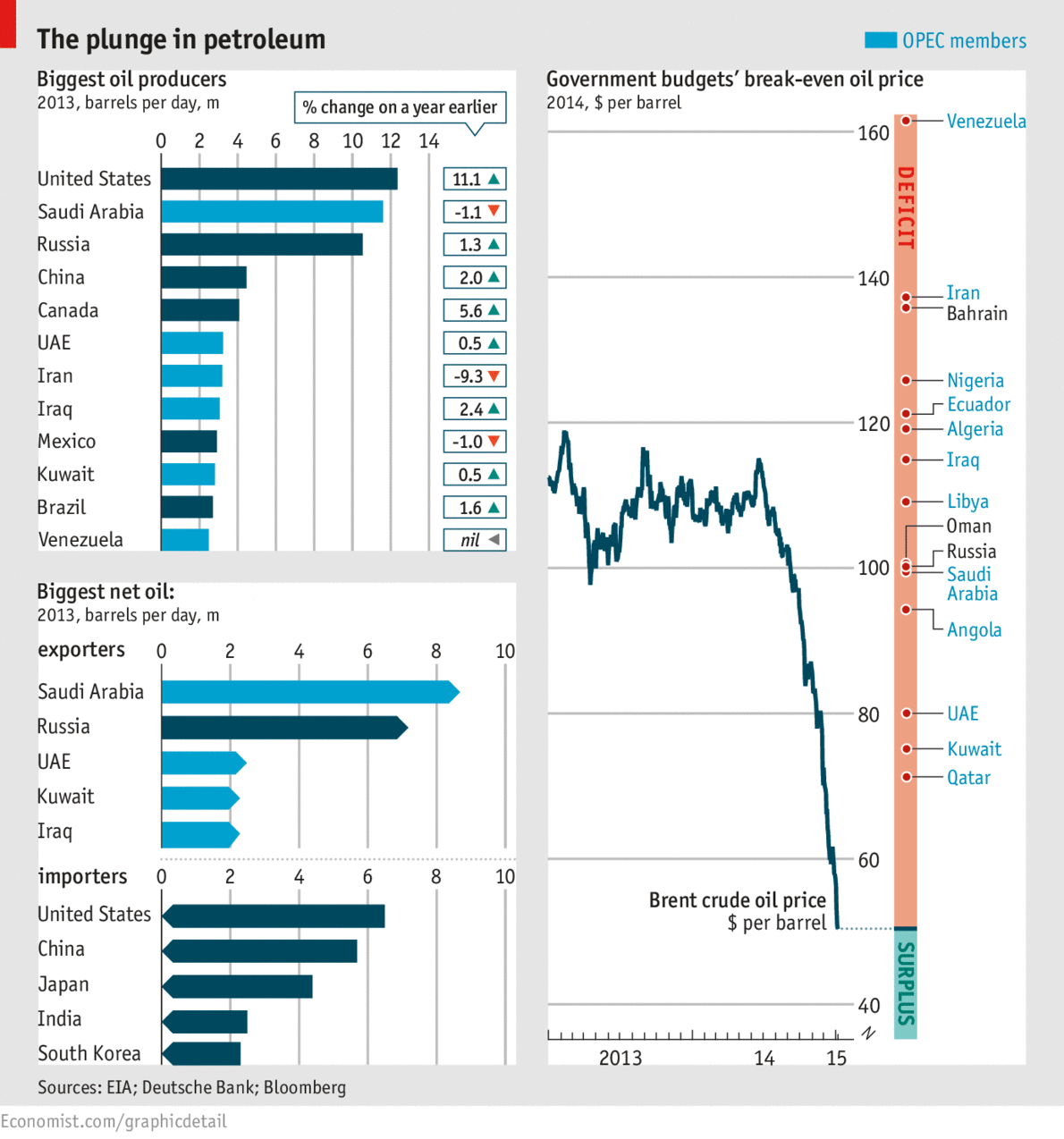

- The Plunge in Petroleum

- Revisiting Plutonomics

- Bloomberg Radio this morning 9am

- 10 Thursday AM Reads

| Posted: 09 Jan 2015 02:00 AM PST Why Is Wage Growth So Slow?

Despite considerable improvement in the labor market, growth in wages continues to be disappointing. One reason is that many firms were unable to reduce wages during the recession, and they must now work off a stockpile of pent-up wage cuts. This pattern is evident nationwide and explains the variation in wage growth across industries. Industries that were least able to cut wages during the downturn and therefore accrued the most pent-up cuts have experienced relatively slower wage growth during the recovery. A prominent feature of the Great Recession and subsequent recovery has been the unusual behavior of wages. In standard economic models, unemployment and wage growth are tightly connected, moving at nearly the same time in opposite directions: As unemployment rises, wage growth slows, and vice versa. Since 2008 this relationship has slipped. During the recession, wage growth slowed much less than expected in response to the sharp increase in unemployment (Daly, Hobijn, and Lucking 2012). And so far in the recovery, wage growth has remained slow, despite substantial declines in the unemployment rate (Daly, Hobijn, and Ni 2013). One explanation for this pattern is the hesitancy of employers to reduce wages and the reluctance of workers to accept wage cuts, even during recessions, a behavior known as downward nominal wage rigidity. Daly and Hobijn (2014) argue that this behavior affected the aggregate relationship between the unemployment rate and wage growth during the past three recessions and recoveries and has been especially pronounced during and after the Great Recession. This Economic Letter examines whether the effects of wage rigidities over the recent recession and recovery can also be seen across industries. In particular, we consider whether industries with higher or lower degrees of wage flexibility have seen different evolutions of wage growth and unemployment. Our findings suggest that industries with the most downwardly rigid wage structures before the recession have seen the slowest wage growth during the recovery, conditional on changes in unemployment. In contrast, industries with fairly flexible wage structures have seen unemployment and wage growth move more closely together. These findings provide cross-industry evidence that downward nominal wage rigidities have played an important role in the modest recovery of wages in recent years. Downward nominal wage rigidities, wage growth, and unemployment Downward nominal wage rigidities are a well-documented feature of the U.S. labor market (see, for example, Akerlof, Dickens, and Perry 1996 and Card and Hyslop 1996). With that in mind, Daly and Hobijn (2014) introduce a model to illustrate how such rigidities can affect the relationship between unemployment and wage growth. Downward rigidities prevent businesses from reducing wages as much as they would like following a negative shock to the economy. This keeps wages from falling, but it also further reduces the demand for workers, contributing to the rise in unemployment. Accordingly, the higher wages come with more unemployment than would occur if wages were flexible and could be fully reduced. As the economy recovers, the situation reverses and the pressure to cut wages dissipates. However, the accumulated stockpile of pent-up wage cuts remains and must be worked off to put the labor market back in balance. In response, businesses hold back wage increases and wait for inflation and productivity growth to bring wages closer to their desired level. Since it takes some time to fully exhaust the pool of wage cuts, wage growth remains low even as the economy expands and the unemployment rate declines. Daly and Hobijn (2014) show that this mechanism causes a bending of the wage Phillips curve—the curve that characterizes the relationship between unemployment and wage growth. Figure 1 Figure 1 shows that the bending of the Phillips curve in our model matches the data for the United States during the Great Recession and subsequent recovery. This same pattern has held in the past three recessions (Daly and Hobijn 2014). The figure shows the relationship between wage growth on the vertical axis, measured as the four-quarter moving average of the four-quarter growth rate of wages and salaries in the employment cost index, and the 12-month moving average of the unemployment rate on the horizontal axis. The figure covers the period from the first quarter of 2008 through the third quarter of 2014. The arrows show the path of the observations over time, and the size of the dots is proportional to the fraction of workers that report no wage changes over the past year. The first part of the curve shows the behavior of wage growth and the unemployment rate during the recession, when the unemployment rate increased by about 5 percentage points and wage growth slowed by about 2 percentage points. The second part of the curve shows that during the subsequent recovery wage growth did not increase as much as it declined during the downturn. The result is that the most recent reported wage growth was 1 percentage point lower than it was at the same level of the unemployment rate when unemployment was rising. This difference is the result of the bending of the Phillips curve, which can be generated by wage rigidity as described in Daly and Hobijn (2014). The recent flattening of the Phillips curve is one reason wage growth has remained sluggish during the recent recovery despite substantial declines in unemployment. Figure 2 Source: FRBSF Wage Rigidity Meter. Rigidity and wage growth across industries If downward nominal wage rigidities are an important explanation for recent slow wage growth, we should see differential effects across industries. Although all industries have some rigidity in wages, the degree of rigidity varies greatly. Figure 2 shows the difference between two industries most affected by the Great Recession: construction and finance, insurance, and real estate (FIRE). The figure plots the 12-month moving average of the share of workers who had their wages fixed over the last year—the standard measure of wage rigidity taken from the FRBSF Wage Rigidity Meter: http://www.frbsf.org/economic-research/nominal-wage-rigidity/. As the figure shows, both industries have some degree of frozen wages that move up and down over the business cycle, just like the national data. However, the level in the construction sector is almost always higher than in FIRE. In fact, with the exception of the late 1990s, the fraction of workers with their wages fixed from one year to the next, zero change, is substantially smaller in FIRE than in construction. Figure 3 Source: Bureau of Labor Statistics. The question for our analysis is whether such sectoral differences can further illuminate the relationship between wage growth and unemployment during the Great Recession and subsequent recovery. To examine this we turn again to the wage Phillips curve. Figure 3 shows the wage Phillips curves for the construction and FIRE sectors for 2008 through 2014. As in Figure 1, wage growth in each sector from the employment cost index is on the vertical axis and the industry-specific unemployment rate is on the horizontal axis. The arrows show the path of the observations over time and the size of the markers reflects the share of workers that report no wage change over the past year. Comparing the two shows that large wage stagnation in the construction sector changed the relationship between wage growth and labor market slack relative to the FIRE sector. More rigid wages in construction created a bend in the curve, consistent with the theory. This bend represents the fact that, while wage growth slowed when the unemployment rate rose, it has moved little as unemployment has declined. More specifically, although the 12-month moving average of the unemployment rate in the construction sector has declined from 20.9% in mid-2010 to 9.5% in the third quarter of 2014, wage growth has risen only 0.6 percentage point over the same period and currently stands at 1.4% per year. One way to assess how much construction deviates from the normal relationship between unemployment and wage growth is to consider what wage growth was in construction at a comparable level of unemployment during the labor market downturn. This difference is shown in the figure as the red dashed line, which indicates that the most recent wage growth is 2.3 percentage points lower than at the beginning of the recession. This gap is a measure of the degree to which the wage Phillips curve is bent. Notably, the shape of the curve in construction stands in stark contrast with that in FIRE, where wages are more flexible. FIRE wage growth fell precipitously as the unemployment rate rose. Once unemployment in the sector started to decline, wage growth accelerated. As of the third quarter of 2014, wage growth was actually 0.4 percentage point higher than it was the last time the unemployment rate was so low. Hence, FIRE does not show the curve bending associated with downward wage rigidities. Figure 4 The relationship between the shape of the wage Phillips curve and the level of the pre-recession wage rigidities for construction and FIRE is indicative of a pattern that holds across the 15 major private industries for which we have wage growth data, shown in Figure 4. The figure plots the size of the wage growth gaps (vertical axis), which we used in Figure 3 to measure the degree of bending of the curve, in the third quarter of 2014 against the degree of wage rigidity in 2007 (horizontal axis). The figure confirms what the theory implies: Sectors where wages are more downwardly rigid are the ones with the largest bends in their wage price Phillips curves. Importantly, this relationship between the level of wage rigidity and the degree of curve bending across industries is statistically significant. The dashed line plots the fitted regression line for this relationship, with each industry weighted by its size in terms of number of payroll employees. Cross-industry variation in the level of wage rigidity in 2007 accounts for 60% of the variation in the bending of the wage Phillips curve across sectors in this weighted regression. This industry-level evidence is consistent with the idea that the reluctance of employers to cut wages during the downturn has had a significant impact on the dynamics of wage growth and unemployment during the recovery. Conclusion National and cross-industry evidence shows that pent-up wage cuts reflecting downward nominal wage rigidities have been an important force during the Great Recession and subsequent recovery. The rigidity of wages in a number of sectors has shaped the dynamics of unemployment and wage growth and is likely to continue to do so until labor markets have fully returned to normal. Mary C. Daly is a senior vice president in the Economic Research Department of the Federal Reserve Bank of San Francisco. Bart Hobijn is a senior research advisor in the Economic Research Department of the Federal Reserve Bank of San Francisco References Akerlof, George A., William T. Dickens, and George L. Perry. 1996. "The Macroeconomics of Low Inflation." Brookings Papers on Economic Activity 1996(1). Card, David, and Dean Hyslop. 1996. "Does Inflation 'Grease the Wheels of the Labor Market'?" National Bureau of Economic Research Working Paper 5538. Congressional Budget Office. 2012. The Budget and Economic Outlook: Fiscal Years 2012 to 2022. Washington, DC: Congressional Budget Office. Daly, Mary C., and Bart Hobijn. 2014. "Downward Nominal Wage Rigidities Bend the Phillips Curve." FRB San Francisco Working Paper 2013-08. Daly, Mary C., Bart Hobijn, and Brian Lucking. 2012. "Why Has Wage Growth Stayed Strong?" FRBSF Economic Letter 2012-10 (April 2). Daly, Mary C., Bart Hobijn, and Timothy Ni. 2013. "The Path of Wage Growth and Unemployment" FRBSF Economic Letter 2013-20 (July 15). |

| Posted: 08 Jan 2015 01:00 PM PST I am excited about our upcoming trip to Seattle! As previously mentioned, I will be in town the week of January 20th to interview Howard Marks at the annual Seattle CFA dinner. I will also be visiting a few clients — and prospective clients — as well. So far, it looks like we be in downtown Seattle for much of the week, plus a visit to the Redmond campus of some small software start up, as well as making the trek to Bainbridge Island. Those of you who are familiar with my investing philosophy, but want to learn more about our approach to asset management and financial planning, feel free to reach out. If you are interested in meeting with us, hearing our views on the markets, or simply discussing your own personal financial circumstances, give us an email or call. Send email to Info -at- RitholtzWealth -dot- com, with the subject “Seattle Trip.” Or call 212-455-9122 and ask for Erika.

|

| Posted: 08 Jan 2015 08:30 AM PST

|

| Posted: 08 Jan 2015 05:45 AM PST

Today is the 8th anniversary of a fascinating set of observations via Robert Frank in the Wall Street Journal on income inequality. 8 years ago, long before most of us even heard of a French academic named Piketty (notably before Murdoch’s acquisition of Dow Jones) came along this gem:

Fascinating stuff . . . well worth rereading the full piece. |

| Bloomberg Radio this morning 9am Posted: 08 Jan 2015 05:00 AM PST > This is your Dulcet Tone Alert, for today on Bloomberg Radio at 9am: I am back again for another bout with Tom: If you are anywhere near a radio this mornings, I will be discussing the latest data about Oil, Makrets and the economy on "Bloomberg Surveillance" with Tom Keene from 9:00 – 10 am. You can catch it live, or via podcast at Bloomberg or at iTunes. Always lots of fun . . . |

| Posted: 08 Jan 2015 04:00 AM PST Yesterday’s snapback looks to continue today, if early futures can be believed. Despite single digit temps in NYC, we have your early morning train reads warmed up to go:

|

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

0 comments:

Post a Comment