The Big Picture |

- Jimmy Fallon Recaps SNL’s 40th Anniversary

- Oil Supply, Energy Demand & the Rip-roaring U.S. Dollar: What it means for your portfolio

- MiB: Cliff Asness, CIO of AQR

- 10 Weekend Reads

- Succinct Summations of Week’s Events 2.20.14

| Jimmy Fallon Recaps SNL’s 40th Anniversary Posted: 21 Feb 2015 04:30 PM PST

|

| Oil Supply, Energy Demand & the Rip-roaring U.S. Dollar: What it means for your portfolio Posted: 21 Feb 2015 08:00 AM PST What do falling oil prices mean for the U.S. in the short and long term

Since early 2014, the price of oil has plummeted. It peaked last year at $105 a barrel and is now about $50.The consumption and production of energy is a major component of the global economy. The huge drop in price has a significant impact in the United States — on corporate profits, employment and capital spending. Still, there has been a lot of misinformation — scare-mongering, really — about falling oil prices. A little context here can go a long way. What's at work? Three factors drive the price of most commodities, including petroleum: the U.S. dollar, supply and demand. Oil is priced in dollars. And it will trade inversely to the price of the world's reserve currency. When the U.S. greenback fell in 2001 to 2008 (down 41 percent), the price of oil climbed over 500 percent ($22 a barrel to $147). As the dollar rallied 30 percent over the past five years, the price of crude oil has more than halved ($105 to $48). Think of the dollar as the measuring stick of oil; when the ruler changes size, so does the price of the measured goods. Demand is the next factor. The United States — the world's biggest consumer of oil (we use twice as much crude as China) — is not showing its usual post-recession uptick. Along with slower growth rates in Asia and the ongoing weakness in Europe, the global demand is softening. A number worth noting: Americans drove 2.764 trillion miles in 2014, according to the government. From the November 2007 pre-crisis peak, total miles driven by all vehicles fell 3.65 percent. In the meantime, hybrid car sales have climbed — the United States has about 3.5 million hybrid electric automobiles, second only to Japan. Even "clean diesel" car sales increased 25 percent in the first six months of 2014 (versus total U.S. car sales, up 4.2 percent). That's just transportation. As a fuel for electricity generation, oil is losing market share versus natural gas — it's cheaper, cleaner and more reliable. Supply is the last piece. Two notable changes from the past have occurred in the production of crude oil in United States and the behavior of Saudi Arabia. The United States is producing nearly twice as much oil than it has in decades. It averaged a little over 5 million barrels a day in the 2000s. At the end of 2014, we were pumping over 9 million barrels per day. If these gains continue, the United States could become energy self-sufficient within a decade. Saudi Arabia has responded to falling oil prices differently than they have in the past. Typically, its response to falling prices has been to cut back their production. That supply constraint was usually sufficient to brings prices back up. This time, they have chosen not to. The immediate impact of lower prices has been negative. Up until now, oil exploration has been a source of high-paying employment. About 500,000 jobs were created in the energy sector since the recession ended. Capital expenditure — spending on rigs, pipelines and more — in the sector has also been robust. With falling prices, such spending is down. Longer-term, however, the effects are more positive. Like so much else in the markets, energy prices are, by and large, a "zero-sum game." One company's loss is another's gain. As exploration and drilling companies suffer a profit squeeze, transportation, retail and utilities benefit from lower fuel costs. Eventually the longer-term positive of lower energy expenses should replace the short-term negative. The psychology of businesses and consumers adjusting to lower prices leads to a delay in changes in behavior. Doubts that the price change is permanent thwart additional spending. But the longer prices stay low, the more significant the changes. We have seen an uptick in the sales of SUVs, pickups and trucks — high-margin vehicles, sold primarily by General Motors, Ford and Chrysler. The longer oil prices stay low, the more of these profitable trucks will be sold. Look at the entire nation of drivers: Every day oil is down $50 from recent highs, my back of the envelope calculations say American motorists collectively save up to $750 million on gasoline. Per day! If prices were to stay below $60 until September, that's a windfall of up to $300 billion. After a few quarters go by, consumers and businesses cannot help but notice more cash in their pockets and on their balance sheets. That is likely to benefit consumer and capital expenditures (corporate spending). Price drops could also give a kick to employment. So long as the United States avoids a recession — and as of now, one does not appear on the horizon — look for the recent bumpiness to turn into economic gains and increased corporate profits. Neither of which is bad for your portfolios. ~~~ Ritholtz is chief investment officer of Ritholtz Wealth Management. He is the author of "Bailout Nation" and runs a finance blog, the Big Picture. On Twitter, @Ritholtz. |

| Posted: 21 Feb 2015 07:00 AM PST This week, the "Masters in Business" radio podcast features Cliff Asness, the founder and CIO of AQR. As CIO of AQR, Asness and his team manages $120 billion dollars. They are quants, who invests by applying mathematics to market data, making evidence based bets across a range of asset classes. In a far-ranging 90 minute conversation, we discuss everything from value to momentum to the small cap effect. We also discuss the Efficient Market Hypothesis, how and why markets can be irrational, and what it was like to be part of the Quant Flash Crash of 2007. If you are interested in what quants actually do, be sure to check out the podcast portion when its posted. Asness gives a graduate level seminar on Quantitative investing. Listen to the podcast live here, on Bloomberg, Apple iTunes or SoundCloud. All of our prior podcasts are available on iTunes. Next week, I speak with Sal Arnuk, Joe Saluzzi of Themis Trading. |

| Posted: 21 Feb 2015 03:30 AM PST Settle into your favorite easy chair, pour a cup of joe, and enjoy our longer form weekend reading:

This weekend, be sure to checkout our Masters in Business interview with AQR founder and CIO Cliff Asness.

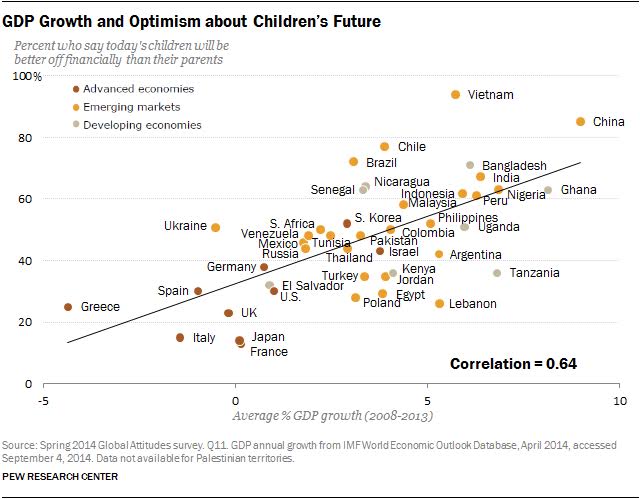

GDP Growth and Optimism About Children’s Future |

| Succinct Summations of Week’s Events 2.20.14 Posted: 20 Feb 2015 12:30 PM PST Succinct Summations week ending February 20th Positives:

Negatives:

|

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

0 comments:

Post a Comment