The Big Picture |

- Are Wages Flat or Falling? Decomposing Recent Changes in the Average Wage Provides an Answer

- Indiana’s SB-01– Is Not Pro Religion, Its Anti-Gay

- Howard Marks: Origins and Inspirations

- Probability, Mean Reversion and Forecasting

- Bull vs. Bear Debate: Is Biotech Is in a Bubble?

- 10 Monday AM Reads

| Are Wages Flat or Falling? Decomposing Recent Changes in the Average Wage Provides an Answer Posted: 31 Mar 2015 02:00 AM PDT Are Wages Flat or Falling? Decomposing Recent Changes in the Average Wage Provides an Answer

To answer questions like this, economists often use the Oaxaca-Blinder decomposition technique (Oaxaca is pronounced wa-ha-ka). This technique is frequently used to analyze wage differences between two groups, for example men and women. We use it to decompose the change in wages between years into two parts. One part is the change in the average wage due to within-occupation wage changes (as in the increased-competition scenario above), and the other is the change in the average wage due to changes in each occupation's share of employment (like the up-skilling scenario above). We do the decomposition for the United States, the four states in the Fourth District (Kentucky, Ohio, Pennsylvania, West Virginia), and the Cincinnati, Cleveland, Columbus, and Pittsburgh metropolitan areas. We use data from the Bureau of Labor Statistics' Occupational Employment Statistics (OES), a survey of 1.2 million establishments over three years, which provides annual estimates of employment levels and average wages for detailed occupations. Because of the overlap in the sample across years, we focus on just three years: 2007, 2010, and 2013. The 2007 to 2010 period captures the recession plus the first year of the recovery and the 2010 to 2013 period captures the rest of the recovery. The occupation codes used by OES changed between 2007 and 2010, so we combined some occupations to create time-stable occupation codes, giving us 785 detailed occupations. We adjust all wages to 2013 dollars to make it easier to compare values across time. For brevity, we call the "real average hourly wage" simply the "average wage." We use the OES rather than the most common source of overall average wages, Current Employment Statistics (CES), because the CES lacks the occupational detail we need for the decomposition. But in the areas where they overlap, the two data sets give similar results. OES's estimate of the national average hourly wage in May 2013 is $22.81, $1.60 less than the CES estimate. This may be because the OES can underestimate the average wage of occupations with very high wages. The OES also shows less growth in average wages from 2011 to 2013, which is consistent with the evidence that recent wage growth has been stronger in high-wage occupations. That said, the OES and CES have similar wage trends from 2007 to 2013. Over this time, the average wage increased 1.7 percent in the OES and 1.9 percent in the CES. Table 1. Decomposition of the Change in Real Average Hourly Wages, 2007–2013

Note: Due to rounding, the percent change may not equal the sum of the wage and occupational mix components. Our analysis shows that for the United States as a whole, the average wage rose 1.5 percent from 2007 to 2013, which is slightly below the published OES estimate. If the mix of occupations were held fixed, the average wage would have declined 0.6 percent due to declines in within-occupation wages. If instead hourly wages within each occupation were held fixed, the average wage would have increased 2.1 percent due to increases in the share of employment in higher-wage occupations. Looking at the states in the Fourth District over the same time period, we find that wages declined 0.6 percent in Ohio and rose 3.3 percent in Pennsylvania and West Virginia and 0.6 percent in Kentucky. In each state, increases in the share of employment in higher-wage occupations pushed the average wage up, but in Ohio a 3.5 percent decline in the within-occupation wage was enough to make the average wage in the state fall. A similar pattern is seen in the Cincinnati, Cleveland, and Columbus metro areas, where notable shifts to higher-wage occupations were not enough to offset falling wages within occupations, and average wages fell from 2007 to 2013. In Pittsburgh, within-occupation wage increases and shifts to higher-wage occupations contributed about equally to a 4.6 percent increase in the average wage over that time. Next we divide this six-year period into two periods: 2007 to 2010 (the recession and the first year of the recovery) and 2010 to 2013 (recovery years). The figures below show the results graphically. The blue bars are the percent change in the average wage due to changes in the mix of occupations. The tan bars are the percent change in the average wage due to within-occupation wage changes. The red dots are the actual percent change in average wage, which is the sum of the two components. When both components have the same sign, the height of the stacked bars is the total change. When the wage and mix component have different signs, the dots representing the total change fall inside the bars.

In the United States, the average hourly wage rose 3.7 percent from 2007 to 2010 and fell 2.2 percent from 2010 to 2013. The increase in the average wage during the recession came from an increase in the share of employment in higher-wage occupations as well as rising wages within occupations. In the recovery, there was a 2.5 percent decline in the average wage due to within-occupation wage changes, and shifts in the occupational mix had a small positive effect (0.3 percent). This implies that, on average, people who did not change occupations experienced declines in their real hourly wage between 2010 and 2013. Table 2. Decomposition of the Change in Real Average Hourly Wage, 2007–2010 and 2010–2013

Note: Due to rounding, the percent change may not equal the sum of the wage and occupational mix components. Source: authors' calculations from the Occupational Employment Statistics.

Average wages rose during the recession and fell during the recovery in all four of the states in the Fourth District. The increases from 2007 to 2010 ranged from 0.6 percent in Ohio to 5.0 percent in Pennsylvania. The small increase in Ohio's average wage was due entirely to changes in the mix of occupations, while the increases in the other states were due to both within-occupation wage increases and increases in the share of employment in higher-wage occupations. The declines in average hourly wages from 2010 to 2013 ranged from 0.7 percent in West Virginia to 2.6 percent in Kentucky. Though shifts to higher-wage occupations pushed the average wage up in Ohio and West Virginia during the recovery, it was not enough to counteract the effect of within-occupation declines in wages, which ranged from 2.2 percent in Kentucky to 3.6 percent in Ohio. Wage growth and its components varied widely across the four largest metropolitan areas in the Fourth District. However, all had within-occupation wage declines during the later recovery years. These declines were large enough to make the average wage fall in each metro area even as their occupational mixes shifted toward higher-wage occupations. For example, in the Columbus metro area from 2010 to 2013, within-occupation wage changes reduced the average wage by 3.7 percent and the shift to higher-wage occupations increased the average wage by 1.6 percent, which nets to a 2.1 percent decline in the average wage.

In general, we find that real average hourly wages rose during the recession and fell during the recovery. The drop in the average wage between 2010 and 2013—which occurred in the US as a whole and all of the states and metropolitan areas we looked at—would have been more severe if there had not also been an increase in the share of employment in occupations with above-average wages. Why did wages rise during the recession and fall during the recovery? It may be due to what are called "selection effects." During recessions, firms tend to retain their most productive workers, both across and within occupations. Furthermore, less productive firms are more likely to lay off workers during recessions, which would also increase average productivity within occupations. Wages are closely linked to productivity, so the selection effects that increase within-occupation productivity also increase within-occupation wages. As hiring increases during a recovery, people who were laid off during the recession—who tend to have lower productivity than people in the same occupation who remained employed—find new jobs, which would pull down the average productivity of the workers within an occupation. It is also possible that wages declined more in the recovery than in the recession due to what economists call "sticky wages." Reducing real wages is one of the ways the labor market adjusts to drops in demand for labor. However, firms generally do not cut the wages of existing employees, so their real wages tend to decline only due to inflation. When the labor market is weak, firms can reduce the wages offered to new hires. As a result, the wages of new hires are more responsive to current labor market conditions than are the wages of existing employees. This implies that within-occupation wages would not change much during the recession due to low levels of hiring, but they could decline as firms hire new workers during the recovery. In this scenario, the within-occupation wage declines indicate just how weak the labor market was between 2010 and 2013.

* * *

Source: Cleveland Federal Reserve Bank ~~~ Joel ElveryJoel Elvery is an economist in the Research Department at the Federal Reserve Bank of Cleveland. Dr. Elvery's primary fields of interest are labor, public, and urban economics. He also specializes in applied econometrics, which involves studying economic models and using statistical trials to calculate future trends. His current work focuses on the regional economy in the Fourth Federal Reserve District, which includes Ohio, western Pennsylvania, eastern Kentucky, and the northern panhandle of West Virginia. Christopher VecchioChristopher Vecchio is a research analyst in the Research Department of the Federal Reserve Bank of Cleveland. His primary interests include development economics, international economics, and the economics of terrorism. Mr. Vecchio holds a bachelor's degree in economics from John Carroll University and a master's degree in economics from Cleveland State University.

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Indiana’s SB-01– Is Not Pro Religion, Its Anti-Gay Posted: 30 Mar 2015 05:00 PM PDT Governor Mike Pence is lying about the purpose of this law. The photo below, and who the governor invited to its being signed into law, very much reveals the motivation behind SB101 — its not pro-religion, its anti-gay, and thats wrong. Its also bad business — companies like Apple and Angies List may very well be the tip of the iceberg; I suspect we may see other companies vote with their feet — and their dollars. Pence has revealed himself, and may have just torpedoed his own Presidential ambitions. The Party of Lincoln, what happened to you?

click for ginormous version | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Howard Marks: Origins and Inspirations Posted: 30 Mar 2015 01:00 PM PDT The Most Important Thing – “Origins and Inspirations Warren Buffett said “When I see memos from Howard Marks in my mail, they’re the first thing I open and read.” Howard is the Co-Chairman of Oaktree Capital Management. He is known in the investment community for his “Oaktree memos” to clients which detail investment strategies and insight into the economy. He treats investing as equal parts psychology and finance, and his book The Most Important Thing provides “uncommon sense for the thoughtful investor.” | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Probability, Mean Reversion and Forecasting Posted: 30 Mar 2015 09:00 AM PDT We’re down to the Final Four in this year’s iteration of March Madness, also known as the national collegiate basketball tournament. Our earlier discussion of “The March Madness Theory of Investing“ didn’t sit well with some readers. The lessons we sussed out from the bracket-destroying results included home-country bias, how expert forecasts are about as good as those of nonexperts, and the impact of noise and distraction. One issue I want to delve into further is why predicting the future seems to be so hard, if not impossible. That particular "lesson" caused quite a bit of pushback. There were many good responses, but Cullen Roche of Pragmatic Capitalism made perhaps the most interesting observation. In a blog post he wrote:

I don’t see this so much as a factual disagreement as simply defining epistemological elements differently. At the risk of repeating myself, let's define just what a prediction is: Continues here: March Madness and the Perils of Predicting

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

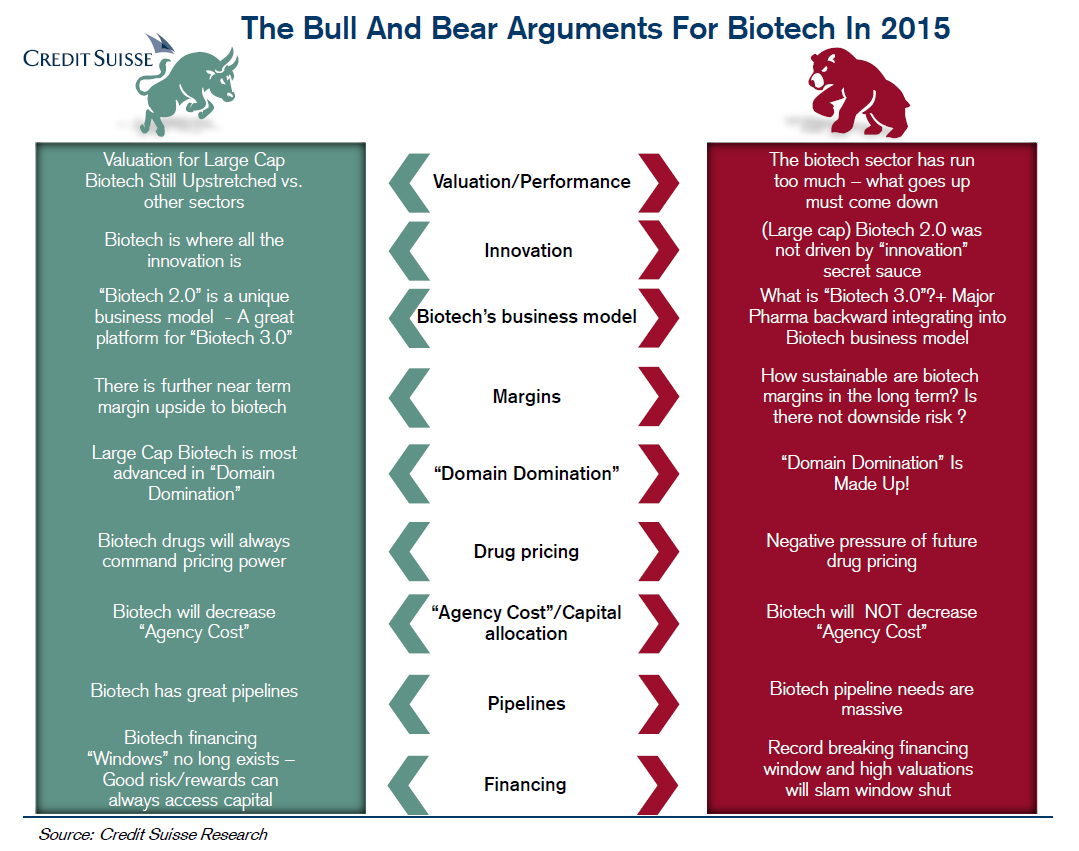

| Bull vs. Bear Debate: Is Biotech Is in a Bubble? Posted: 30 Mar 2015 05:00 AM PDT | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 30 Mar 2015 04:00 AM PDT Back to the workweek! Spring has sprung, the futures are green, and its time for our morning train reads:

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

0 comments:

Post a Comment