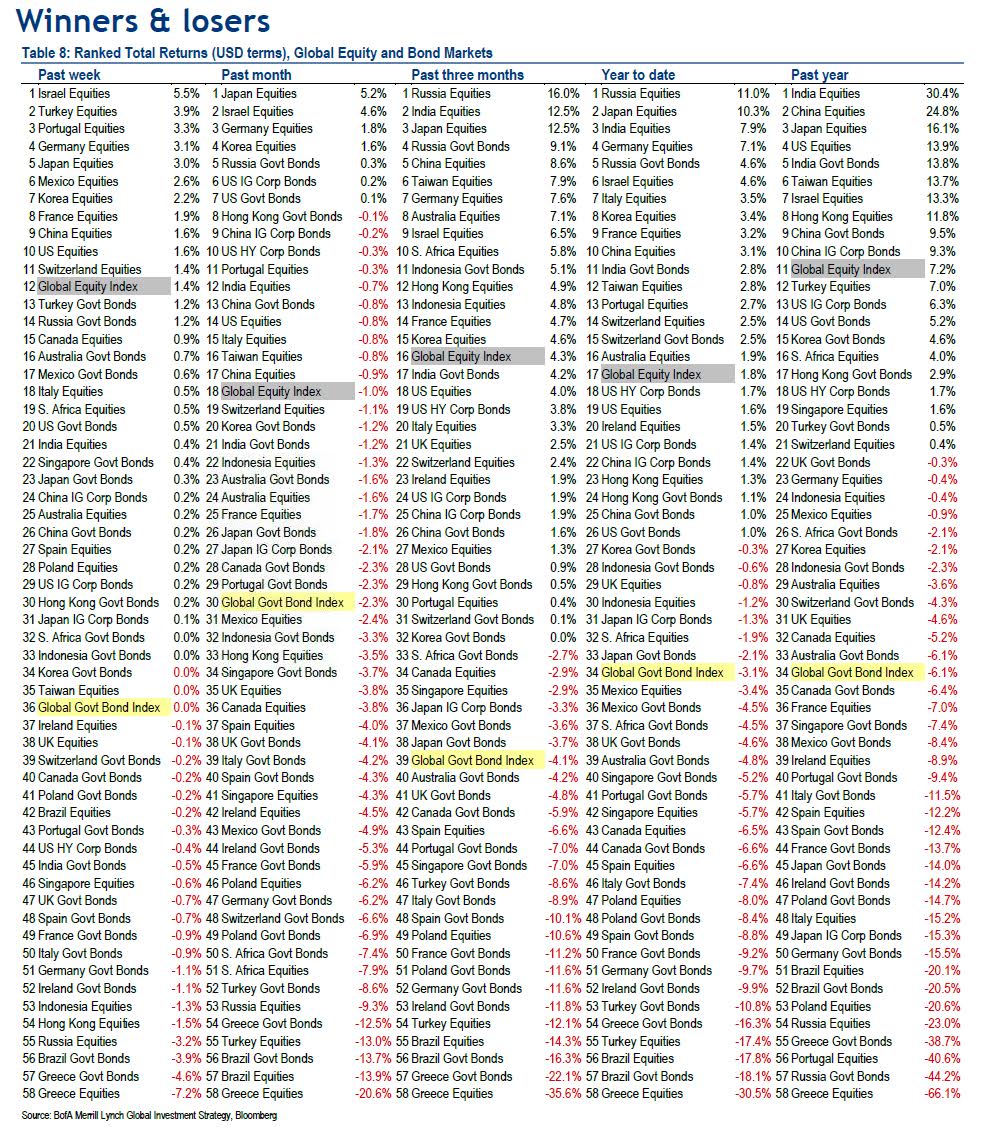

The Big Picture |

- Central Bank Solvency and Inflation

- The Shapes of Stories by Kurt Vonnegut

- The Rise of the ‘Unicorns’

- April Fools: Apple to Buy Spotify

- 10 Sunday Reads

| Central Bank Solvency and Inflation Posted: 06 Apr 2015 02:00 AM PDT Central Bank Solvency and Inflation

The monetary base in the United States, defined as currency plus bank reserves, grew from about $800 billion in 2008 to $2 trillion in 2012, and to roughly $4 trillion at the end of 2014 (see chart below). Some commentators have viewed this increase in the monetary base as a sure harbinger of inflation. For example, one economist wrote that this "unprecedented expansion of the money supply could make the ’70s look benign." These predictions of inflation rest on the monetarist argument that nominal income is proportional to the money supply. The fact that the money supply has expanded rapidly while real income has grown very modestly means that sooner or later prices will have to catch up. Most academic economists (from Cochrane to Krugman and Mankiw) disagree. The monetarist argument arguably applies only to non-interest-bearing central bank liabilities, but since October 2008 a large fraction of the monetary base has consisted of reserves that pay interest (the so-called IOER, or interest on excess reserves) and one linchpin of the Fed's "policy normalization principles" consists precisely in raising the IOER along with the federal funds rate. Since reserves pay close to market interest rates, they are close substitutes for other short-term assets such as Treasury bills from a bank's perspective. As long as the central bank can affect the return on these short-term assets by adjusting the IOER, controlling inflation with a large balance sheet seems no different than it was before the Great Recession. Our argument is very different from that dismissed at the beginning of this post. It rests on the observation that QE, almost by definition, resulted in a sizable maturity mismatch between the asset and the liability side of the central bank's balance sheet. Many recent papers (for example,Hall and Reis; Carpenter et al.; Greenlaw, Hamilton, Hooper, andMishkin; and Christensen, Lopez, and Rudebusch) have noted this mismatch, and have computed the implications of different interest rate renormalization paths for remittances from the central bank to the Treasury. Relative to these papers, we explicitly model the fact that seigniorage—revenues arising from currency creation—depends on the path of inflation and interest rates. We show that this endogeneity opens the door to the possibility of multiple equilibria in the absence of fiscal support. Imagine that you are a Treasury investor and you know that the only resource the central bank can rely upon is seigniorage. You also know that the value of the central bank's assets (long-term bonds) would fall below that of the bank's interest-bearing liabilities (reserves, which are short-term) if high inflation and interest rates were to occur in the near future. Then you put two and two together and figure out that expectations of high inflation would actually force the central bank to rely on seigniorage, thereby validating such expectations. If you can convince your fellow investors that these expectations are to materialize, then your projection can become a self-fulfilling prophecy, reminiscent of second-generation currency crisis models. Before we go any further, we should stress that this sort of self-fulfilling prophecy is unlikely to take hold in the United States for two reasons. First, we compute in our simulations that the expected present value of seigniorage for the central bank is very high, roughly the size of current U.S. GDP, under a most likely path for future interest rates. As a consequence, it would take very extreme expectations for interest rates to force the central bank to generate more seigniorage and validate the expectations. Moreover, there are reasons to believe that the assumption of no fiscal support under any circumstances is incorrect: if faced with the prospect of high inflation, the Treasury would eventually be willing to provide support to the central bank. Note that this support comes at no cost at all for the Treasury: simply being willing to provide it is enough to nip any hyperinflation in the bud. What are the policy implications of all this? Certainly not that the central bank should not have engaged in QE. Much research has shown that QE successfully eased financial conditions, thereby promoting economic recovery. Rather, we argue that it would always be appropriate for a central bank to have access to, and be willing to ask for, support for its balance sheet by the fiscal authority. In other words, central bank independence does not mean that the central bank can control inflation regardless of the actions of the fiscal authority. As shown by history, it never has. Disclaimer

Christopher A. Sims is John F. Sherrerd '52 University Professor of Economics at Princeton University. |

| The Shapes of Stories by Kurt Vonnegut Posted: 05 Apr 2015 05:00 PM PDT

|

| Posted: 05 Apr 2015 01:00 PM PDT

|

| April Fools: Apple to Buy Spotify Posted: 05 Apr 2015 08:00 AM PDT The price? A COOL TEN BILLION! It had to happen. Apple’s stock rises when it has a monopoly. And despite all the iPhone profits, Android has greater worldwide market share. This is not the iPod revolution, wherein a seamless hardware/software combination, of iPod iTunes and FairPlay DRM, ensured that no other player could gain traction. Hell, Apple is losing traction every day in music. And if you believe that Jimmy Iovine can pull a rabbit out of his hat, you believe Jay Z is gonna turn Tidal into a raging success. That’s right, Jimmy was left out of the negotiations. Tim Cook is still pissed about the U2 fiasco, wherein Iovine paid back the has-been stars and Apple ended up with egg on its face. Apple is a bigger brand than U2, and Cook feels like the company got hijacked, so therefore, just like David Geffen was left out of the MCA/Matsushita negotiations, Jimmy had no part in this purchase, it’s news to him. Actually, credit Scott Forstall. You remember him, right? Mr. Software, Steve Jobs’s right-hand man? Forstall was agitating for a music streaming service so loudly that he got fired. But after promoting Jony Ive and closing ranks Cook had a chance meeting with Daniel Ek at the San Jose airport, while their respective jets were being gassed, and Cook realized the error of his ways. He couldn’t bring back Forstall, but he was man enough to recognize he’d been wrong, as Steve was too, files are history, streams are forever. So the seed was planted YEARS ago! That’s why Spotify has never gone public. Projects at Apple take as long to develop as movies at Pixar and while you were looking for an Apple TV set and deriding Jony Ive’s Watch, Cook was positioning the company to win, and win big. That’s right, now Apple’s going to own streaming music, no one else will be able to compete, it’s monopoly time all over again. So what’s the first lesson here? Live like a king. Get a NetJet account. You can’t advance your career flying coach. Just like a wannabe leases a BMW in Los Angeles, in Silicon Valley you fly private. For the hang. For the business. ~~~ Anyway, Apple is behind the eight ball in music. iTunes sales are faltering and iTunes Radio is a disaster. Sure, iTunes Radio may ultimately triumph in countries Pandora has not entered, but it doesn’t look good. And Spotify looks great. Don’t believe the naysayers. Spotify’s footprint is immense, it’s in almost every country with an economy. And as Daniel Ek so famously says, if they stopped expanding/investing, they’d be profitable today. Sure, the business was built on musicians’ backs, but we reward superstar coders more than superstar musicians, and conception is everything. In a world of me-too music, Spotify was never a me-too music service. Spotify had first-mover advantage. Which is why Beats Music could never catch it. Why Rdio and Deezer can’t catch it. Along with the deep pockets to give the music away for free. And no one has a deeper pocket than Apple. They’re the only one who could overpay for Spotify, because not only do they have the cash, they’re the only one who can benefit from the synergy of the acquisition! That Beats Music service that Ian Rogers has been working on so hard? It’s the equivalent of Copland, the unworkable OS that caused Gil Amelio to purchase NeXT and gain what evolved into OS X. That’s why Beats/Apple Music has never relaunched. It’s too buggy! So, Spotify will now be Apple’s default service. With a reskinning and a rebranding. They’ve been working on this for two years, but the software is now launch-ready. It’s akin to the Mac’s switch from PowerPC to Intel. By time they announced it, they were ready to do it, all the work had already been done! But the free tier doesn’t go away. This is Jimmy Iovine’s middle finger to the music industry. That’s right, Jimmy is incredibly pissed the label bosses wouldn’t agree to lower the price of an Apple streaming service to $7.99 a month. And he’s now getting the last laugh. Because with Apple the only game in town, Lucian Grainge has to bow to his will. It’ll be ten bucks a month for all you can eat, or you can experience the ads and listen for free. Apple has money to lose as it tightens its grip on streaming music. That’s right, it’s over. No other enterprise has pockets this deep, software this good and mindshare/rep of an equivalent stature. Launch date is Friday May 15th. Why? BECAUSE IT’S THE START OF TAYLOR SWIFT’S 1989 TOUR! It was all a head fake. The joke is on you. Taylor’s been in cahoots with Apple for nearly a year. She removed her music from Spotify in order to drive down the purchase price! Every dollar below $10 bil was hers to keep. Alas, she was unsuccessful in this effort, but she’s coming out fine. She’s gonna get a dollar for every sign-up for the first twelve months. So, expect her to hawk Apple’s streaming service like she hawked her album, and no one’s a better marketer than Taylor, no one’s got a better relationship with the press. Didn’t you notice her absence at the Tidal press conference? She, of all people, should have been there. But “1989″ isn’t even streamable on Tidal, doesn’t that tell you something? And now you know why Mercedes-Benz was a late addition sponsor to the Rock In Rio festival in Las Vegas. That’s where Taylor’s headlining on the 15th. Mercedes-Benz is going to give everyone who purchases an automobile a lifetime subscription to Apple’s streaming service, as long as they continue to drive an MBZ. It’s a win-win. So where does this leave Tidal? Dead in the water, where it already is. A bunch of the artists involved were already eager to bolt from Live Nation’s management division after Monday’s debacle, now this sale will anger them even further. It was all masterminded by Guy Oseary, the same guy who was responsible for the U2 album fiasco. Rumor has it they’re all going to march en masse into Irving Azoff’s fold, now that his non-compete has expired, but that has not yet been substantiated. But the reason MSG is dividing in two is to free up money for further acquisitions by Irving, so all signs are pointing in this direction. The other streaming services will fade away and will not radiate. Because online only one entity wins, you gravitate to where all your friends are. All the exclusives will be on Apple. The streaming service will work on Android and Windows, but icons will not look as sharp and functionality will be hampered in order to force people to buy Apple hardware. It’s all about the hardware, you know that, right? It’s the reverse razor blade theory. You give away the software to sell expensive hardware! So now Apple owns music. They’re not going to buy labels. That’s ridiculous. Who needs the headache? But they are going to release data, so that acts will know that it’s the labels screwing artists, not the streaming service. So the war is over. You can stop bitching about Spotify. You can get back to making good music, if you ever did. As for consumers, this is heaven. And books and television are next. Apple plans to corner the market on TV distribution, their deal with HBO is just the beginning. And despite being judged guilty of price-fixing re books, the publishers are still angry at Amazon and are willing to throw in with Cook for a subscription service. They get to set the price. Apple will just take its traditional 30%. Amazon’s reading devices suck anyway, and this is just a further way to cement Apple’s power in tablets, a way to goose sales, which have suddenly stalled. So, it’s been proven that Tim Cook is quite the match for Steve Jobs. Just like he green-lit the evisceration of skeuomorphism, he’s pivoting the company to streaming content. He knows that streaming is the future. DO YOU? ~~~ – |

| Posted: 05 Apr 2015 04:30 AM PDT Good morning — round out your weekend with our Sunday morning reads:

What are you reading?

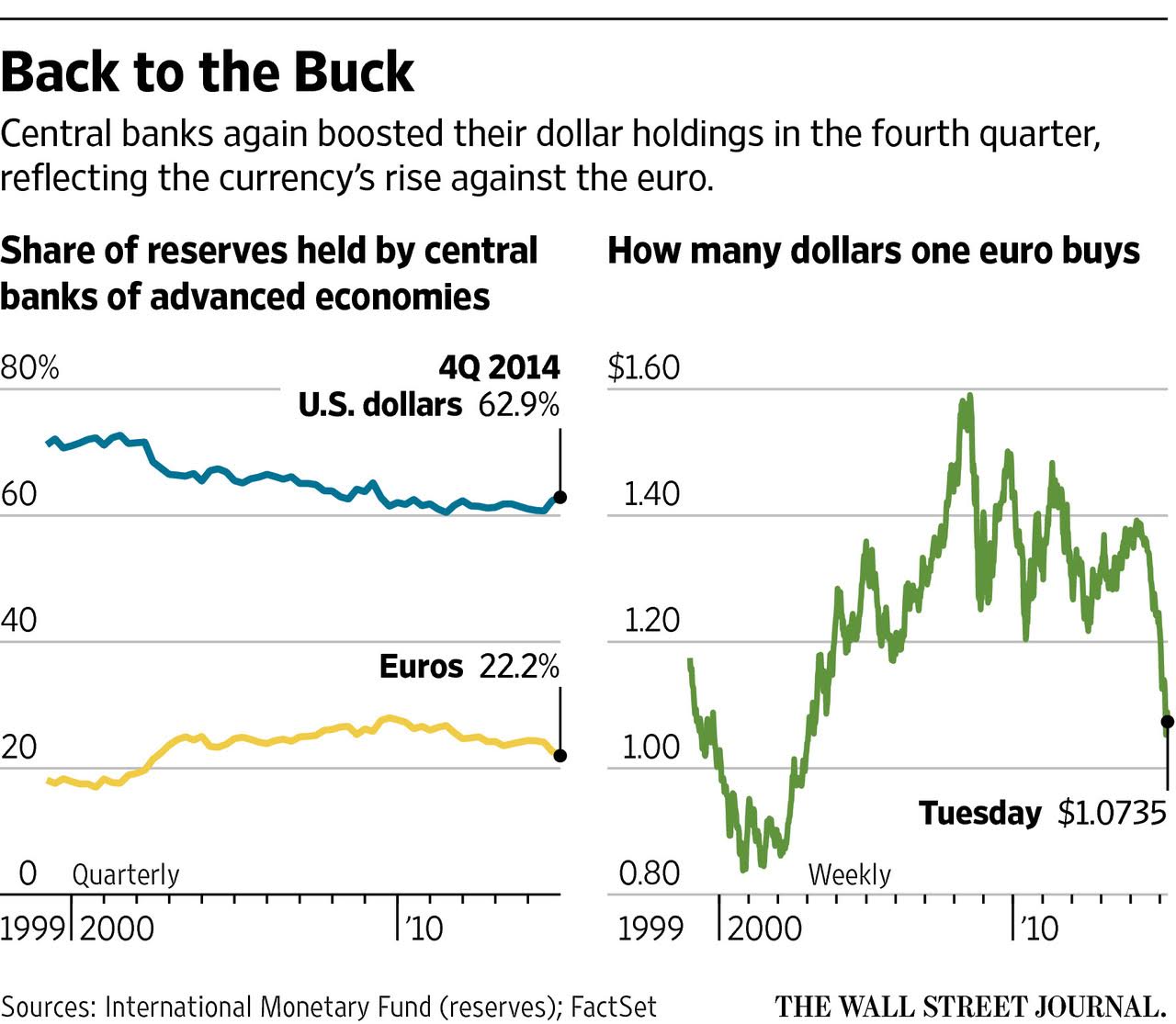

Central Banks Again Boosted Their Dollar Holdings

|

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |