The Big Picture |

- David Brooks, Alex Baldwin On Relationships

- Effective Tax Rates Around the World

- 33 Things I Know About Art Direction

- Hoisington Quarterly Review and Outlook

- Ritholtz’s rules of investing (part II)

- Jack Welch’s Gaffe – A Follow-up

- 2013 McLaren 12C Spider

- 10 Weekend Reads

- Bloomberg TV Appearance

- SEC General Counsel: Financial Markets Are Broken

| David Brooks, Alex Baldwin On Relationships Posted: 20 Oct 2012 02:00 PM PDT Who you marry is the most important decision you’ll make in life. I’d be lying if I said I was a David Brooks fan. It’s not because he signed off from my newsletter, it’s because he’s a conservative. And that sticks in my craw. Paul Krugman, Brooks’s counterpart on the Opinion page of the “New York Times,” boils it down to this… Democrats believe in a social welfare state, Republicans do not. The government is imperfect, but I like it in between myself and corporations, I like the water and the environment to be safe. There are those moments in foreign countries when you wonder… Like there’s this chairlift in Portillo. It goes virtually straight up and there’s a tower at the bottom and one at the top and nothing in between and I’m not good with heights to begin with and just as my anxiety starts to subside I realize I’m in CHILE! Are there tramway regulations? Could the cable snap while I’m on it? Could it jump the track? Kind of like in the Caribbean. Where I found myself panicking as the current took me further asea as I was snorkeling. In the U.S., the proprietor of the snorkeling service would be so scared of liability he’d be looking out for me, scanning the water for people in trouble. Whereas these guys could be back in the boat, smoking cigarettes, telling jokes… Which is exactly what they were up to. When I finally got back and hauled myself aboard they weren’t even paying attention. So I’m not worried when the man from the government says he’s there and he’s planning to help me. The same way I’ve got no sympathy for the small businessman complaining ASCAP and BMI are charging him for music, something they’re allowed to do under the law. These establishments are profiting from the tunes. Why should they get a free ride? Shouldn’t the creators be compensated? And now I’m so far off point you may not even remember where I started, but what really turned me off on Brooks was his comment that this election was all about the viability of the twentieth century welfare state. Romney wanted to reform it, Obama and the Democrats didn’t care about rising costs. If you think this election is solely about that, you’ve lost my attention. How about the nomination of Supreme Court justices? How about a woman’s right to choose? And Krugman tore Brooks a new one over the foregoing distillation. And Brooks flew to Spain to see Springsteen… Which I thought was pretty frivolous, and sort of weird, considering their respective viewpoints, but when Jim Guerinot testified about Brooks’s most recent book despite attending the latest Obama fundraiser I wondered if I’d dismissed him too soon. And that’s when I found his podcast with Alec Baldwin in my iTunes library. You’ve got to like the guy. He admits he’s a nerd, makes fun of his alma mater, and says he’s a liberal on social issues. He can make fun of himself, which too many right wingers cannot. And he explains his conservatism, by saying that despite good intentions, one cannot predict human behavior, government oftentimes gets it wrong. But what fascinated me most were his thoughts on marriage. Now let me be clear. Brooks was not pontificating, not getting up on his high horse and letting us all know the truth. He did his best to beg off, but since Alec had just gotten remarried, Brooks quoted a blog post he’d found… “Brag about your spouse and let them overhear you.” What did Pete Townshend sing, “I am an animal”? We all are. We all want to feel loved and safe. We want to feel respected. Contrary to conventional wisdom, many things should not be left unsaid. So if you want to keep your relationship going, do the above. It works wonders. And the next words of wisdom were… “Sometimes you’ve just got to go to bed.” I can be the worst offender here. Wanting to stay up all night, digging down deep to uncover the truth. But so many times you wake up the next morning and…it all just doesn’t matter that much. “…so I go to colleges and I tell kids if you have a great career and a crappy marriage, you will be miserable. If you have a crappy career and a great marriage, you’ll be happy. So every course you take in college should be about who to marry. So like you should take literature courses, theater courses, science courses. Think hard about this one. They look at me like I’m crazy. But that is absolutely true. So if you want to know what correlates to happiness, money correlates a little but when you hit a certain point, it stops. Age correlates to happiness so people in their 20s are happy and then they go through a shallow, U-shaped curve and the nadir of happiness for the average person is age 47. And that’s called having teenage children. And then the peak happiness is the first 10 years after retirement. But the people who are happy, marriage is equal to double your income; having a good marriage produces the same happiness gain as doubling your income.” I wish someone had taught me this. We think we should marry for sexual attraction, or wealth, or compatibility. We’ve got our values all wrong. First and foremost, does that person show up? Can you count on them? To do the right thing, not only with you but as your representative out in the world? Fantastic sex won’t mean much if your spouse can’t balance his or her checkbook. If he or she constantly overdraws, incurring thousands of dollars in bank fees every year, never mind angering local merchants and friends. A great conversation is wonderful, but if your spouse never calls to say he or she is late, never practices common courtesy, you’ll be tearing your hair out. And if you just got that big promotion at work, had a thrilling victory and your significant other just doesn’t care, you’re going to be very unhappy. You learn all the foregoing as you age. If you’re lucky, you make no mistakes. But this is extremely rare, based on the divorce rate, never mind the unhappy couples who stay together. And speaking of staying together… That’s another trait you want to look for in a spouse, perseverance. Breakups are never mutual. Anybody who tells you otherwise is lying. And it’s one thing if it’s just a fling, but if you’re married, if you got up in front of God and country and said “I do.” you hope your spouse is gonna give it much more than the old college try. You hope the commitment is such that not only will they not step out, but they’ll hang in there through the bad times to get to the good. And unlike so much of today’s pop music, Brooks’s wisdom stuck with me. I just wanted to pass it on to you. David Brooks on Here’s The Thing:

– http://www.twitter.com/lefsetz – http://www.lefsetz.com/lists/?p=subscribe&id=1 |

| Effective Tax Rates Around the World Posted: 20 Oct 2012 12:00 PM PDT I tweeted this during the week, and I was surprised how many times it got retweeted:

|

| 33 Things I Know About Art Direction Posted: 20 Oct 2012 11:00 AM PDT

|

| Hoisington Quarterly Review and Outlook Posted: 20 Oct 2012 08:00 AM PDT Hoisington Quarterly Review and Outlook

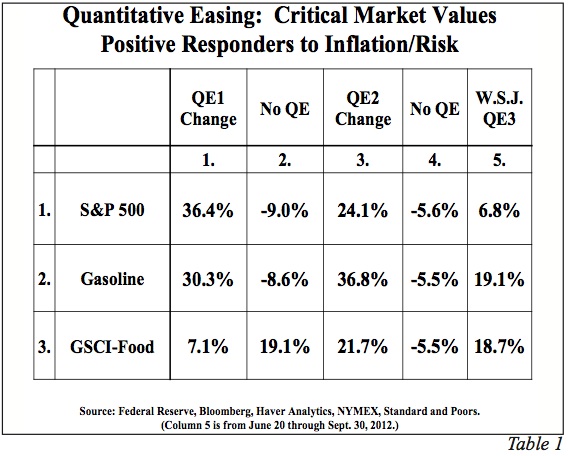

This month they waste no time in dissecting the Fed's recent move to QE3 and similar efforts in Europe, arriving at the conclusion that "While prices for risk assets have improved, governments have not been able to address underlying debt imbalances. Thus, nothing suggests that these latest actions do anything to change the extreme over-indebtedness of major global economies." Their expectation: global recession. The only issue left to sort out, they say, is How deep will the downturn be? They make the interesting observation that with each injection of liquidity by the Fed, commodity prices have surged: "During QE1 & QE2 wholesale gasoline prices jumped 30% and 37%, respectively, and the Goldman Sachs Commodity Food Index (GSCI-Food) rose 7% and 22%, respectively. From the time the press reported that the Fed was moving toward QE3, both gasoline and the GSCI Food index jumped by 19%, through the end of the 3rd quarter." The QE picture gets even muddier. The unintended consequence of the Fed's actions, say Lacy and Van, has been to actually slow economic activity: "The CPI rose significantly in QE1 and QE2 (Chart 1). These price increases had a devastating effect on worker’s incomes (Chart 2). Wages did not immediately respond to commodity price changes; therefore, there was an approximate 3% decline in real average hourly earnings in both instances. It is true that stock prices also rose along with commodity prices (S&P plus 36% and 24%, respectively, in QE1 and QE2). However, median households hold a small portion of equities, and thus received minimal wealth benefit." They proceed to tear apart the wealth effect that the Fed is banking on to restimulate the economy, drawing on several solid studies. They also make the key point that "When the Fed actions lead to higher food and fuel prices, the shock wave reverberates around the world, with many foreign economies being hit adversely. When prices of basic necessities rise, the greatest burden is on those with the lowest incomes since more of their budget is allocated to the basic necessities such as food and fuel." The next few years are not going to be pretty. We're looking right into the teeth of a rolling global deleveraging recession—the End Game, I've called it. And the decisions we make in the next couple years about how to handle our debts and budget deficits—here in the U.S., in Europe, in China and Japan, and elsewhere—are going to be absolutely crucial. Hoisington Investment Management Company (www.hoisingtonmgt.com) is a registered investment advisor specializing in fixed-income portfolios for large institutional clients. Located in Austin, Texas, the firm has over $4 billion under management, composed of corporate and public funds, foundations, endowments, Taft-Hartley funds, and insurance companies. My daughter Abbi is coming into town tonight from Tulsa with her fiancé, and most of the family will gather over the weekend for dinners and fun. And her twin Amanda is expecting, so another grandchild is in the future as well. Family and friends are among the few permanent fixtures in a world that seems to change almost weekly. I was with Pat Cox of Breakthrough Technology Alert on Tuesday night. We watched the debate and then went deep into the night talking about the future. And got up the next day and did the same between meetings. We ended up doing a tag team that night for Hedge Fund Cares, which raised a lot of money to help abused children. I talked about the global landscape (which was not so upbeat) and he talked about the changes we see in the biotech world; and we then both answered questions, which was more fun, as we got to think about the marvelous the future that is shaping up. Such totally amazing things are happening. I am really quite the optimist over the longer term. Have a great weekend, and look for your next Thoughts from the Frontline in your inbox Monday. Your bullish on the future but bearish on governments analyst, John Mauldin, Editor subscribers@mauldineconomics.com

Hoisington Investment Management Growth Recession Entering the final quarter of the year, domestic and global economic conditions are extremely fragile. Across the globe, countries are in outright recession, and in some instances where aggregate growth is holding above the zero line, manufacturing sectors are contracting. The only issue left to determine is the degree of the downturn underway. International trade is declining, so weaknesses in different parts of the world are reinforcing domestic deteriorations in economies continents away. With this global slump at hand, a highly relevant question is whether the U.S. can escape a severe recession in light of the following: a) the U.S. manufacturing sector that paced domestic economic growth over the past three years has lapsed into recession; b) real income and the personal saving rate have been slumping in the face of an interim upturn in inflation, and c) aggregate over-indebtedness, which is the dominant negative force in the economy, has continued to move upward in concert with flagging economic activity. New government initiatives have been announced, particularly by central banks, in an attempt to counteract deteriorating economic conditions. These latest programs in the U.S. and Europe are similar to previous efforts. While prices for risk assets have improved, governments have not been able to address underlying debt imbalances. Thus, nothing suggests that these latest actions do anything to change the extreme over-indebtedness of major global economies. To avoid recession in the U.S., the Federal Reserve embarked on open-ended quantitative easing (QE3). Importantly, the enactment of QE3 is a tacit admission by the Fed that earlier efforts failed, but this action will also fail to bring about stronger economic growth. Commodity Market Reactions Commodity markets have risen in reaction to the Federal Reserve's liquidity injections into the banking sector (Table 1). From the time the press reported that the Fed was moving toward QE1 & QE2 commodity prices surged. During QE1 & QE2 wholesale gasoline prices jumped 30% and 37%, respectively, and the Goldman Sachs Commodity Food Index (GSCI-Food) rose 7% and 22%, respectively. From the time the press reported that the Fed was moving toward QE3, both gasoline and the GSCI Food index jumped by 19%, through the end of the 3rd quarter.

Two theoretical considerations account for the rise in commodity prices during QE3. The first is the expectations effect. When the Fed says they want higher inflation, the initial reaction of the markets is to "go with", rather than fight the Fed. The second linkage, which is the expanded availability of funds used for collateral (margin), was identified and subsequently confirmed by Newedge economist, Dr. Rod McKnew, who stated, "In a world of advanced derivatives, high cash balances are not required to take speculative positions. All that is required is that margin requirements be satisfied." Thus, when the Fed massively expanded reserve balances in QE1 and QE2, margin risk was minimized for those market participants who wished to take positions consistent with the Fed's goal of higher inflation, and who had either direct or indirect access to the Fed's hugely inflated reserve balances. The April 22, 2011 issue of Grant's Interest Rate Observer documented support for McKnew's insight. They asked Darrell Duffie, the Dean Witter Distinguished Professor of Finance at the Graduate School of Business at Stanford University, whether excess reserves could serve as collateral for futures and derivatives transactions. Dr. Duffie's answer was "acceptable collateral is a matter of private contract, but reserve deposits are virtually always acceptable."

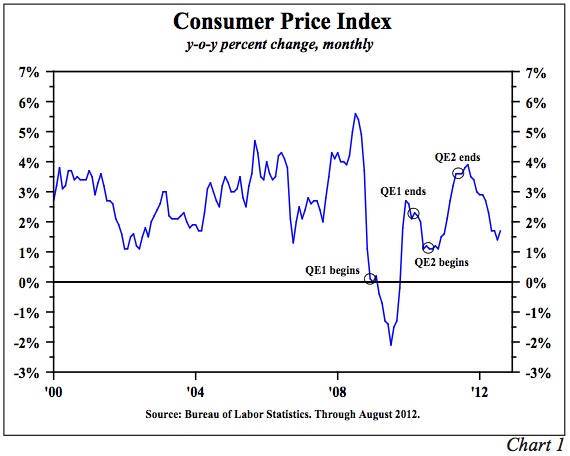

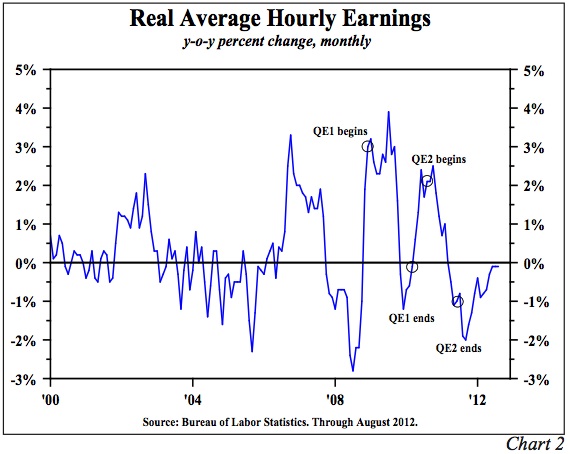

Devastation for Households The unintended consequence of these Federal Reserve actions, however, is to actually slow economic activity. The CPI rose significantly in QE1 and QE2 (Chart 1). These price increases had a devastating effect on worker’s incomes (Chart 2). Wages did not immediately respond to commodity price changes; therefore, there was an approximate 3% decline in real average hourly earnings in both instances. It is true that stock prices also rose along with commodity prices (S&P plus 36% and 24%, respectively, in QE1 and QE2). However, median households hold a small portion of equities, and thus received minimal wealth benefit.

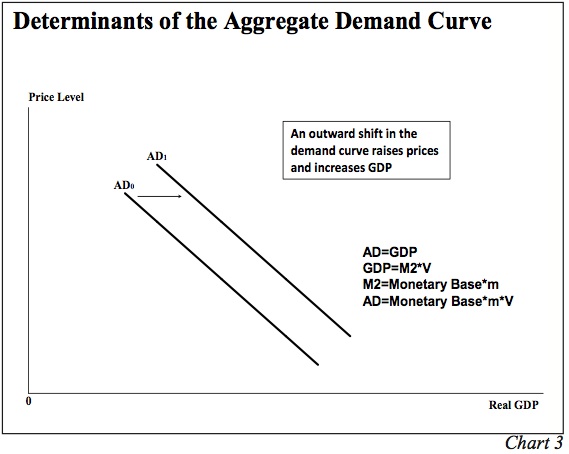

Wealth Effect Despite the miserable economic results in QE1 and QE2, we now have QE3. Fed Chair Ben Bernanke and other Fed advocates believe the "wealth effect" of QE3 will bring life to the economy. The economics profession has explored this issue in detail. Sydney Ludvigson and Charles Steindel in How Important is the Stock Market Effect on Consumption in the FRBNY Economic Policy Review, July 1999 write: "We find, as expected, a positive connection between aggregate wealth changes and aggregate spending. Spending growth in recent years has surely been augmented by market gains, but the effect is found to be rather unstable and hard to pin down. The contemporaneous response of consumption growth to an unexpected change in wealth is uncertain, and the response appears very short-lived." More recently, David Backus, economic professor at New York University found that the wealth effect is not observable, at least for changes in home or equity wealth. A 2011 study in Applied Economic Letters entitled, Financial Wealth Effect: Evidence from Threshold Estimation by Sherif Khalifa, Ousmane Seck and Elwin Tobing found "a threshold income level of almost $130,000, below which the financial wealth effect is insignificant, and above which the effect is 0.004." This means a $1 rise in wealth would, in time, boost consumption by less than one-half penny. These three studies show that the impact of wealth on spending is miniscule—indeed, "nearly not observable." How the Fed expects the U.S. to gain any economic traction from higher stock prices when rising commodity prices are curtailing real income and spending is puzzling. This is particularly relevant when econometricians have estimated that for every dollar of gained real income, consumption will rise by about 70 cents. Conversely, the Fed actions are causing real incomes to decline, which has a 70-cent negative impact on spending for every dollar loss. Compare that with the 0.004 positive impact on spending for every one-dollar increase in wealth. Former Fed Chairman, Paul Volcker, summarized the new Fed initiative as sufficiently and succinctly as anyone when he stated that another round of QE3 "is understandable, but it will fail to fix the problem." An International Corollary The unintended consequences of QE3 could also serve to worsen and undermine global economic conditions already under considerable duress. When the Fed actions lead to higher food and fuel prices, the shock wave reverberates around the world, with many foreign economies being hit adversely. When prices of basic necessities rise, the greatest burden is on those with the lowest incomes since more of their budget is allocated to the basic necessities such as food and fuel. Thus, a jump in daily essentials has a more profound negative impact on living standards in economies with lower levels of real per capita income. Can the Fed Create Demand? Can all the trillions of dollars of reserves being added to the banking system move the economy forward enough to eventually create a higher level of aggregate spending? Our analysis of the aggregate demand curve and its determinants indicate they cannot. The question is whether monetary actions can shift this aggregate demand (AD) curve out to the right from AD0 to AD1 (Chart 3). If this were possible, then indeed the economy would shift to a higher level of prices and real GDP.

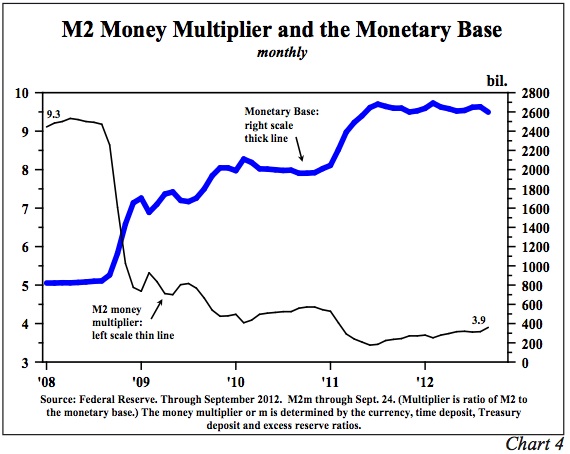

The AD curve is equal to planned expenditures for nominal GDP since every point on the curve is equal to the aggregate price level (measured on the vertical axis of the graph), multiplied by real GDP (measured on the horizontal axis of the graph). We know that GDP is equal to money times its turnover or velocity, which is called the equation of exchange as developed by Irving Fisher (Nominal GDP = M*V). Deconstructing this formula, M (or M2) is comprised of the monetary base (currency plus reserves) times the money multiplier (m). The Federal Reserve has control over the monetary base since its balance sheet is the dominant component of the monetary base. However, the Fed does not directly control the money supply. The decisions of the depository institutions and the non-bank public determine the money multiplier (m). M2 thus equals the monetary base multiplied by the money multiplier. The monetary base, also referred to as high powered money, has exploded from $800 billion in 2008, to $2.6 trillion currently, but the money multiplier has collapsed from 9.3 to 3.9 (Chart 4). Therefore, the money supply has risen significantly less than the increase in the Fed's balance sheet, with the result that neither rapid gains in real GDP nor inflation were achieved. Indeed, with the exception of transitory episodes, inflation remains subdued and the gain in GDP in the three years of this expansion was the worst of any recovery period since World War II.

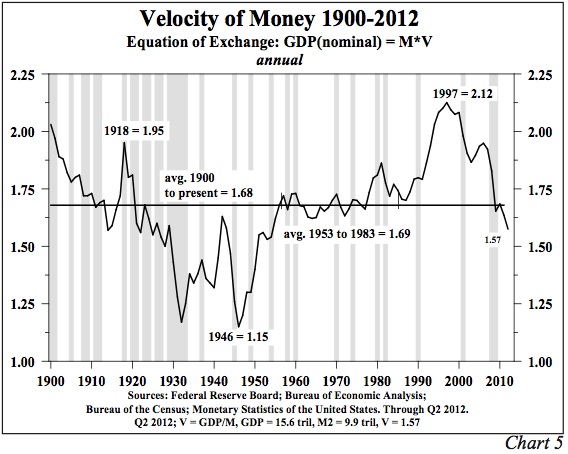

The other element that is required for the Fed to shift the aggregate demand curve outward is the velocity or turnover of money over which they also have no control. During all of the Fed actions since 2008 the velocity of money has plummeted and now stands at a five decade low (Chart 5).

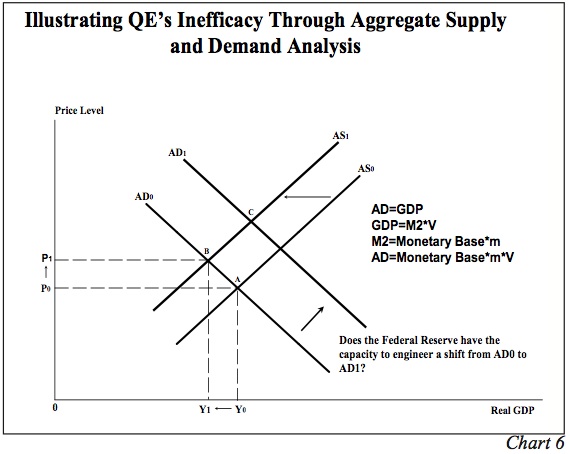

The consequence of the Fed's lack of control over the money multiplier and velocity is apparent. The monetary base has surged 3.3 times in size since QE1. Nominal GDP, however, has grown only at an annual rate of 3%. This suggests they have not been able to shift the aggregate demand curve outward. Nor, with these constraints, will they be any more successful in shifting that curve under the present open-ended QE3. Increased aggregate demand and thus rising inflation is not on the horizon. [For a more complete discussion of the complexities of the movement of the aggregate supply and aggregate demand curves please see the APPENDIX.] Treasury Bonds As commodity prices rose initially in all the QE programs, long-term Treasury bond yields also increased. However, those higher yields eventually reversed and generally continued to ratchet downward, reaching near record lows. The current Fed actions may be politically necessary due to numerous demands for them to act to improve the clearly depressed state of economic conditions. However, these policies will prove to be unproductive. Economic fundamentals will not improve until the extreme over-indebtedness of the U.S. economy is addressed, and this is in the realm of fiscal, not monetary policy. It would be more beneficial for the Fed to sit on the sidelines and try to put pressure on the fiscal authorities to take badly needed actions rather than do additional harm. Until the excessive debt issues are addressed, the multi-year trend in inflation, and thus the long Treasury bond yields will remain downward. APPENDIX One of the most important concepts in macroeconomics is aggregate demand (AD) and aggregate supply (AS) analysis – a highly attractive approach that is neither Keynesian, monetarist, Austrian, nor any other individual school, but can be used to illustrate all of their main propositions. However, before detailing the broader macroeconomics associated with the movement of the AD and AS curves, it is important to understand microeconomic supply and demand curves. This can best be illustrated through the recent impact the Fed's decisions had on commodity prices. In the commodity market, like individual markets in general, the demand curve is downward sloping, the supply curve is upward sloping, and where they intersect determines the price of the commodity and the quantity supplied/demanded. The micro-demand curve slopes downward because as the price of an item rises, the quantity demanded falls due to income and substitution effects (buyers can shift to a substitute product). The micro-supply curve slopes upward since producers will sell more at higher prices than lower ones. Both supply and demand schedules are influenced by expectation, fundamental, and liquidity considerations. When the Fed says that they want faster inflation and that they are going to take steps to achieve this objective, both economic theory and historical experiences indicate that commodity prices will rise, at least transitorily (as seen with the surge in commodity prices after the announcement of QE1, QE2 and QE3). Information and liquidity available to the buyers is also available to the suppliers, so by saying faster inflation is ahead, suppliers are encouraged to reduce or withhold current production or inventories, moving the supply curve inward. Thus, in the commodity market, the Fed action spurs an outward shift in the micro-demand curve along with an inward shift of the micro-supply curve, producing higher prices and lower quantities. These microeconomic developments transmit to the broader economy, which we will now trace through AD and AS curves.

The AD curve slopes downward and indicates the amount of real GDP that would be purchased at each aggregate price level (Chart 6). Aggregate demand varies inversely with the price level, so if the price level moves upward from P0 to P1, real GDP declines from Y0 to Y1. When the price level rises, real wages, real money balances and net exports worsen, thereby reducing real GDP. The rationale for the downward sloping AD curve is thus quite different from the sloping of the micro-demand curve since substitution effects are not possible when dealing with aggregate prices. In order to improve real GDP with a rising price level, the AD curve would need to be shifted outward and to the right (from AD0 to AD1). And as detailed in the letter, the Fed is not capable of shifting the entire AD curve. The AS curve slopes upward and indicates the quantity of GDP supplied at various price levels. The positive correlation between price and output in micro and macroeconomics is the same since the AS curve is the sum of all supply curves across all individual markets. When Fed policy announcements shock commodity markets, the AS curve shifts inward and to the left (from AS0 to AS1). This immediately causes a reduction in real GDP (the difference between Y0 and Y1) as the price increases by the difference between P0 and P1 (also Chart 6). Furthermore, as discussed in the letter, lower GDP as a result of higher prices reduces the demand for labor and widens the output gap, setting in motion a negative spiral. For Fed policy to improve real GDP, actions must be taken that either (1) shift the entire demand curve outward (to the right), or (2) do not cause an inward shift of the AS curve that induces an adverse movement along the AD curve. Accordingly, the Fed is without options to improve the pace of economic activity. |

| Ritholtz’s rules of investing (part II) Posted: 20 Oct 2012 07:00 AM PDT Ritholtz's rules of investing (part II)

This week, we're going to pick up with my rules for investing. These rules come from 20 years of experience – or 20 years of learning from my own mistakes. My list is designed to help you understand what you face as an investor and avoid the sorts of errors that cost many investors a lot of money. Understanding the philosophy here will result in fewer losses, better performance and more restful nights. Because I didn't want to overwhelm you, I broke the list into two parts. Before we get to this week's list, you can read the first part here. For those reading this in the newspaper, those six rules were:

Let's move on to part two: 7. Understand your own psychological make up. Most investors think they are competing against other traders, big institutions, hedge funds etc. In fact, they are their own most dangerous opponent. Why is that? It is because of the way we are wired. We fall prey to all sorts of cognitive errors. We are overconfident in our abilities to pick stocks, time the market, know when to sell. We suffer from confirmation bias, seeking out that which agrees with us and ignoring facts that challenge our views. We vacillate between emotional extremes of fear and greed. We are surprisingly risk-averse, and at precisely the wrong times. The recency effect has us overemphasizing recent data points while ignoring long-term trends. Our own cognitive and psychological errors often lead us down the wrong path. You can counter these foibles only if you are aware of them. 8. Admit when you are wrong. One of the biggest problems many investors have is admitting they made a bad investment. Men, suffering as they do from testosterone poisoning, are especially bad at this. Whether it's ego or just stubbornness, too many people seem to hold on to their losers for way too long. Pride can be a very expensive sin. The most effective approach is to admit your error, fix the mistake, then move on. Think of investing as more akin to batting in baseball than to being a lawyer, accountant or doctor. If you are a .333 hitter – if you get a hit one out of three times at bat – you are an all-star ball player. A doctor who loses two-thirds of his patients or an accountant who has 66 percent of his clients audited are both doing something terribly wrong. We have a saying in my office called "strong opinions weakly held." We may have a high degree of confidence in a particular investing theme – say, emerging markets dividends or municipal bonds – but as soon as we have proof we are wrong, we reverse the position, sell the holding and move on. I believe in admitting errors and, in fact, each year I publish a list of mea culpas – describing my worst investing errors. I explain what I did wrong and what I learned from it. It may be human to make mistakes, but it is foolish to make the same ones over and over. Try making some new mistakes instead. 9. Understand the cycles of the financial world. Another challenging thing to do in investing is to reverse your thinking, especially after a specific approach has been profitable for a long time. The longer the period of successful thinking, the more important – and challenging – the reversal will be. Pay attention to history, and you learn that events move in long, irregular cycles. We have the business cycle, which alternates between periods of expansion and contraction. Recessions happen, as do recoveries. Then there is the market cycle, where booms and busts occur regularly. Every bull market is followed by a bear; every bear market is followed by a bull. This can be difficult to remember when you are in throes of either one. It seemed in 1999 that almost no one could imagine that the manic price rises of the market would ever end. And in late 2008 and early 2009, it looked like the vicious market collapse would never end. But it did – and it always does. "This too shall pass" is a proverb that humbled King Solomon. Understand what it means when you mistakenly believe something will never change. 10. Be intellectually curious. There is a tendency amongst investors to settle into a comfort zone. You develop a particular style, find an investing method you like – and then think it will last forever. This is a recipe for slothful calcification. Heraclitus was a Greek philosopher whose doctrine of flux stated "The only constant is change." This is especially true in investing. The many different inputs that drive market returns constantly change. At various times, it can be profits, the Fed, the economy, interest rates, technology, tax policy, etc. It is important that you constantly upgrade your skill set, while learning to be both adaptive and flexible. The best investors all have a healthy dose of intellectual curiosity. If everything else is changing, but you are not, then you are being left behind. 11. Reduce investing friction. Friction refers to all of the little costs that, when compounded over time, can add up to big dollars. In investing, friction refers to anything that is a drag on total returns outside of market performance. Think about the long-term effects of the fees, costs, expenses and taxes on your net, above and beyond how your investments did. Since 1974, the markets have returned about 10 percent a year. The average 401(k) retirement account earned about 3 percent annually over that period. There are numerous reasons these portfolios radically underperformed the markets, but one of the primary reasons is the layers of excess fees and fund loads. Investors with lower costs tend to have better growth and retain more of their assets over the long haul. Keep your fees, costs expenses and taxes low. It is a guaranteed way to improve your returns. 12. There is no free lunch. This is the most fundamental rule in all of economics. It gets forgotten by too many investors. The temptation is to get something for nothing. You never get something for nothing. Consider: That hot stock tip? You want the upside without doing all of the tax research. High-yield junk bonds? Some people believe that an 8 percent yield when the 10-year Treasury is paying 1.62 percent does not come with an increased risk of default. They are mistaken. Sitting in way too much cash? It creates a false illusion of safety that will not keep up with inflation. No one on television is going to make you wealthy. There is no magic formula or silver bullet or secret hedge fund. The best investors generate long-term returns by making rational, unemotional decisions. They do their homework, spend time and effort learning the basics. They are unemotional, intelligent and patient. You can be as well. ~~~ Ritholtz is chief executive of FusionIQ, a quantitative research firm. He is the author of "Bailout Nation" and runs a finance blog, the Big Picture. You can follow him on Twitter: @Ritholtz. For previous Ritholtz columns, go to washingtonpost.com/business. |

| Jack Welch’s Gaffe – A Follow-up Posted: 20 Oct 2012 05:30 AM PDT Jack Welch's Gaffe – A Follow-up

We thank the many, many readers who sent comments on our missive about Jack Welch's Gaffe. See www.cumber.com for the original commentary on Welch. On October 5, the Bureau of Labor Statistics (BLS) published the report "Employment from the BLS household and payroll surveys: summary of recent trends." Here is the link: http://www.bls.gov/web/empsit/ces_cps_trends.pdf. We recommend it to anyone seriously interested in the methodology behind the BLS activity. Readers may then judge for themselves whether Jack Welch and others of his ilk are correct with their innuendos that the BLS statistics may be cooked. I employ the word may because Welch has now introduced a "question mark" at the end of his infamous tweet. Three readers used offensive language, called me a liar, and defended Welch as the only deity of truth around. They have been removed from our listserve. We do not run a blog where wannabe analysts can use four-letter-laced epithets and hide behind anonymity. That sport is for others. We do offer our direct views about issues and markets. We invite both disagreement and concurrence. We admit errors and post errata. Our purpose is to add to the serious discussion of topical issues while also communicating with our clients, their consulting advisers, our media friends, and the general public. Enough digression; let's go back to the Welch piece. Among the 35 economists and financial professionals who replied to us, agreement with our criticism of Mr. Welch was nearly universal. Several respondents were on data or statistical committees of economic organizations such as NABE (www.nabe.com). Some had personal working experience in government statistical agencies. They served Republican and Democrat administrations. Not one supported Welch's allegations. Several skilled professionals noted supporting and corroborating data from sources other than BLS. That info indicated that the statistical improvement in the recent employment report may be valid. One thoughtful response came from Madeline Schnapp. She is one very smart and hard-working lady, who is also the Director, Macroeconomic Research at TrimTabs Investment Research. Madeline sent the following comments: "BTW, to add to the confusion, our withholding tax based employment estimate was 210,000 in September vs. 114,000 from the BLS. So according to our data, there is acceleration in growth. We just do not think it is as much as currently reported by the BLS and possibly reported by the BEA come October 26th. The BLS revised August employment up 48% to 142,000 vs. our 185,000. As we have been saying since July, we think the driver is housing, based on current data and input from our stable of real estate data experts. Friday’s reports from JPM and WFC seem to support our earlier conclusion. "As is usually the case, when we generate an employment number that is unexpected I spend a great deal of time trying to throw water on the estimate. This month, I did come up with another possible explanation for non-wage, non-job withholding tax growth: re-characterization of wage income from non-taxable to taxable (eg. 401ks). I chatted with some defense industry analysts this past week and they are of the opinion that major defense contractors are already planning for an 8% budget cut. So perhaps, in anticipation of layoffs after the first of the year, employees, en masse, are canceling their 401K contributions in anticipation of losing their jobs. But in order to reduce the employment nos. significantly, I estimate that approximately $150 billion in income (annualized) would have to be re-characterized, which seems like an awful lot and thus unlikely. "So it would seem that thirty-year mortgage interest rates of 3.39%, and fifteen-year mortgage interest rates of 2.7% appear to be having the desired effect. In the past two weeks, however, the y-o-y growth in withholding taxes has retreated a bit. It is too early in the month to tell whether or not the retreat is noise, but if the growth driver is the housing sector, the seasonal nature of that sector might now also be responsible for a deceleration going forward." Thank you, Madeline. That is a helpful response and thought-provoking. There were many Welch detractors who were not personally known to me. Here is an example from Malcolm B., who resides in NY. "Welch certainly knows something about unemployment: at GE he unemployed over 100,000 men and women 'in order to make to make GE more profitable'. I used to be impressed with his record. But, if he were really that good, he could have figured out something profitable to do with those people, who were good enough to be hired in the first place. Maybe he also knows something about cooking the books: it now seems just a bit fishy that almost every single quarter he just made estimates…" Thank you, Malcolm. Many others hold similar views. We will close this commentary on the Jack Welch affair with quotes from Gene Epstein of Barron's. In the October 15 edition, he wrote: "Former CEO of GE Jack Welch – fresh from his earlier charge of data manipulation and implicitly conceding that 7.8% isn't a terrible number – decided to weigh in again in an op-ed in Wall Street Journal. Anyone reading this piece should have stopped when the author observed, 'by definition, fewer people in the workforce leads to better unemployment numbers,' thus earning Mr. Welch an 'F' on both the definition and the facts. The facts are that fewer people in the workforce have not prevented worse unemployment numbers several times in the past few years. Martin Fridson, whose book Financial Statement Analysis is in its fourth edition, observes that 'Jack Welch came by his suspicion of data-manipulation honestly, having presided over some aggressive tactics to smooth earnings fluctuations while CEO of GE.'" Ok enough about Welch. BTW, conspiracy theorists were dealt another blow when the weekly unemployment claims numbers were announced. The whole notion of a "fix" by California Democrats is just more bizarre behavior. Notice that the BLS discussed the seasonal shifts and that one state (CA?) had a one-week anomaly. Any basic statistics student knows that weekly claims are volatile and that a four-week moving average is a much better short-term indicator of labor market conditions and changes. The four-week average is on track, as it was during this whole Jack Welch, weekly claims, conspiracy-theory saga. Enough! ~~~ David R. Kotok, Chairman and Chief Investment Officer, Cumberland Advisors. |

| Posted: 20 Oct 2012 05:00 AM PDT

The 2013 McLaren 12C Spider ($265,750 plus $2,500 destination charge) is the least-compromised convertible sports car built:

Some snaps from Jalopnik:

Source: Jalopnik |

| Posted: 20 Oct 2012 04:15 AM PDT Some longer form reads to start your Saturday morning:

What are you doing this weekend?

Extreme volatility, 2 bear markets, strong recovery rally |

| Posted: 20 Oct 2012 04:00 AM PDT Fusion IQ CEO Barry Ritholtz talks about credit risk and his investment strategy. He speaks on Bloomberg Television’s “Street Smart.” How Big a Concern Is Credit Risk? ~~~~ On today’s “Chart Attack,” Fusion IQ CEO Barry Ritholtz and Bloomberg’s Adam Johnson look at the misery index state by state and who may be favored in the upcoming presidential election. They speak on Bloomberg Television’s “Street Smart.” (Source: Bloomberg) How Misery Loves Obama (Slightly) ~~~~ Jamie Stuttard, head of international bond investments at Fidelity Investments, Kathy Boyle, president and founder of Chapin Hill Advisors, and Barry Ritholtz, chief executive officer of Fusioniq, talk about Europe’s sovereign-debt crisis, Spanish stocks and bonds, and their investment strategies for the region. They speaks with Trish Regan and Adam Johnson on Bloomberg Television’s “Street Smart Stuttard Likes German, Northern Europe Corporates |

| SEC General Counsel: Financial Markets Are Broken Posted: 20 Oct 2012 04:00 AM PDT Ralph Ferrara, partner at Proskauer Rose LLP, talks with Bloomberg Law’s Lee Pacchia about the problems presented by high frequency trading and potential solutions. Ferrara says that certain policy changes made by Congress in the mid-1970′s had the effect of decentralizing financial markets and diminishing the presence of human controls over trading activity. In his opinion, the resultant market fragmentation combined with high frequency trading has led to a broken, two-tiered system that could force retail investors out of the market and fundamentally change the notion of capitalism in the United States. Ferrara served as General Counsel to the Securities & Exchange Commission from 1978 to 1981.

|

The Hoisington Quarterly Review and Outlook is one of the cornerstones of my reading on where the economy is headed. Van Hoisington and Lacy Hunt do a masterful job of turning data points into cogent, well-argued themes.

The Hoisington Quarterly Review and Outlook is one of the cornerstones of my reading on where the economy is headed. Van Hoisington and Lacy Hunt do a masterful job of turning data points into cogent, well-argued themes.

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment