The Big Picture |

- Only Suckers Switch to Samsung

- Dumbest Investing Ideas of 2014

- 10 Weekend Reads

- Hunton XRS43

- Kiron Sarkar’s Weekly Report (12th July 2014)

| Only Suckers Switch to Samsung Posted: 12 Jul 2014 02:00 PM PDT Only suckers switch to Samsung. I’ve never ever been to the Genius Bar before. Because I find I can fix most problems myself. The web is a cornucopia of information, if you can’t find the answer in the Apple Support Communities, you don’t have a problem. But finally at my limit with my Mac Pro, I made the journey. And when I went to pick up my machine today, more about that later, I decided to… Tell them about my phone. The truth is Americans are abusers. Give ‘em an inch and they’ll take more than a mile. The best example is Costco, that bastion of consumer-friendliness. They had a generous return policy they had to eliminate, because people were buying new iPods and then returning them a year later, when the new model came out, even though there was nothing wrong with the first. So unless something craps out completely, unless it’s a slam-dunk case, I don’t want to deal with customer service. Because I feel I’ve got to justify myself, since everybody who’s preceded me is a lying, cheating, scumbag. Like that husband of an old friend who no longer liked his car so he drove it south of the border and reported it stolen.

Yup, I’m too embarrassed to speak up for myself even if I do have a problem. But today I did. You see the battery on my iPhone no longer had the juice. Oh, the device worked, I never would have scheduled a special trip, but while I was there…it’d crap out at 20% and the journey down to that number was oh-so-fast. So Hunter hooked it up to a program, and voila! Turned out it was failing. Not gone, but borderline. So he gave me a new phone. But it gets even better than that, the random freezing problem I was having, only in e-mail, was gone too. So this is a win-win. But I’m still gonna get a new phone in the fall. Because this one will be paid for. And it’s not about the device anyway, but the data, and the utility. As in you need something that works, but what’s on it and what it can access is more important than how it looks. So, if you’re getting something spiffy, ask yourself, what are you gonna do when it breaks? Call Korea? Or if you cheap out, buy one of those knock-off Android devices, same deal. And you know how it works, it’s never their fault. Even Apple pooh-poohs third party software. You’ve got to convince somebody that they’re responsible, and if you think that’s easy, you’re David Boies, and even he’s got a spotty track record. Sure, I bought insurance, known as Applecare. Might be expensive, but I want no questions asked. It’s less about the money than the service. I want to be covered, the same way I pay house insurance, it’s about what if? What if I’m stuck with a lame device that’s my lifeline? And that’s what smartphones are, a lifeline. If you don’t feel this way, believe me, in a couple of years you will.

And the truth is we’ve got no time. Which is why I didn’t schedule a special trip to begin with. Which is why not only was it great to instantly get a new phone, but to have all its data instantly synch from the cloud. That’s what you get when you’ve got one stop shopping, when you buy everything from one place, i.e. Apple, it all works seamlessly. So if all you want to do is make calls and text, you’re fine with another device, maybe. But what if you get a bum app? What if you’ve lost functionality? Who you gonna call, Ghostbusters? What we’re all looking for is a safety net, even the 1%. Although theirs is all about health, that’s the one thing money can’t buy. But the rest of us, we don’t want to be waylaid by a problem, we don’t want the wind taken out of our sails, we want to believe someone will be there in our moment of crisis. And the last resort should be and is the government. Which is why the uninsured go to emergency rooms and get service, because as a society we don’t want our citizens to be lame and maimed. But the government doesn’t cover everything. It’ll give you some food, some health care, but it won’t give you a phone and service. For this you’ve got to pay. So who are you going to pay? Pay Apple. Because you’re paying anyway, it’s built into your contract. The phones are not free, even though you think they are. Because someday you’re gonna want answers. And the Genius Bar is just a hop, skip and a jump away. And you’ll be glad. P.S. As for my Mac Pro, they tested it and said it was fine, which means…it won’t be, but I’m gonna find out. (They tested the hardware and the software, found no problem. Then they said a hard drive failed, then they tested all four and said they were fine. Then they installed a new OS on one and…I’ve got absolutely no faith the problem is gone. I’m gonna buy a new machine, hopefully this one will limp along and get me through.) ~~~

–

|

| Dumbest Investing Ideas of 2014 Posted: 12 Jul 2014 07:00 AM PDT The Worst Investing Ideas I’ve Heard This Year (so far)

As the second quarter comes to an end, my top 10 list of dumb investment ideas is filling up. All of these would be fairly foolish in any year. (Feel free to explain to me why these are not dumb, or to suggest investing ideas that are even more reckless or just plain silly.) Note that these aren't on the list simply because they lost money; the nature of investing is that some significant percentage of trades is going to lose money. That is a given, and it is the reason you should be a diversified investor. Smart asset allocation includes U.S. stocks, as well as those from developed countries and emerging markets. It is also why your bond portfolio should be a mix of corporates, treasuries, munis, etc. Ritholtz is chief investment officer of Ritholtz Wealth Management. He is the author of "Bailout Nation" and runs a finance blog, the Big Picture. View Archive As I have said before, good investing is about process, not outcome. These trades all suggest a fundamental misunderstanding about investing. Here is the first half of my top 10 list of dumb investments ideas for 2014 (check back at year's end for the rest): Athlete IPOs. This year, San Francisco 49ers star tight end Vernon Davis IPO'd. Fantex Brokerage Services agreed to buy a 10 percent cut of all Davis's future earnings for $4 million. There are so many reasons this is a not a good investment idea, but let's limit our discussion to three: 1) You have limited ability to pick which companies are going to do well; what makes you think you have any ability to guess what any athlete's future income stream is going to be? 2) Even a minor injury can end an athlete's career. In the NFL, the average career is short — either 3.2 years or almost 6 years. 3) Even if the 29-year-old Davis stays healthy, for investors to make money, he needs a giant new $33 million contract (according to the Fantex risk factors), plus he must "attract and retain endorsements, then generate other brand income post career." Again, the thought of most investors getting this calculation correct is laughable. This was a terrible investment concept, but it's brilliant marketing for Fantex, which describes itself as "the world's first registered trading platform that lets you invest in tracking stock linked to the value and performance of a professional athlete brand." That's a genius concept, assuming there are enough fans stupid enough to part with their money. Based on the cost of beer and hot dogs at the stadiums, I suspect there are plenty of sports fanatics with more dollars than sense. The goldbug portfolio. Every now and again, I see a portfolio that is so absurdly stupid, I can't help but slap myself upside the head. The goldbug portfolio is one of them. It starts out with the SPDR Gold Shares (GLD). Then it is seasoned with a collection of gold mining stocks, such as Yamana Gold (AUY), Goldcorp (GG), ArcelorMittal (MT), Barrick Gold (ABX), Newmont Mining (NEM). Then a few ETFs, such as the Market Vectors Gold Miners ETF (GDX). Add in the smaller miners in either individual companies or ETF flavors (GDXJ). A soupçon of a mutual fund or two. Then a dollop of leveraged holdings, such as the Direxion Daily Gold Miners Bull 3X Shares (NUGT). My favorite position in this nightmare portfolio just might be the S&P 500 Gold Hedged Index — it's perfectly hedged to never be able to make any money. What's wrong with this portfolio? It's one giant bet on the exact same trade. These positions are all highly correlated with the price of gold, and with each other. Owning all of them ain't what anyone can call diversification. Regardless of your views on gold — mine was published earlier this year — this portfolio is simply idiotic. If you want exposure to gold, than buy physical gold and store it in an investment deposit box or home safe. If you feel compelled to put it in a portfolio, than buy SPDR Gold Shares (GLD). But do not buy 50 flavors of a nearly identical investment. The people who put this portfolio together should be drummed out of the financial services industry. Mutual funds held at the mutual fund company. This head-scratcher is hard to understand. For some unfathomable reason, people hold mutual funds at the underwriting company instead of at any ordinary brokerage account. Of course, these are the "A Shares," with commissions typically approaching 5.75 percent (or higher). This is an insane amount of money to pay for a mutual fund when you can shop around and probably find a very similar fund for 80 percent less. Or find the rough equivalent in an ETF index fund with a 0.15 percent expense ratio, and pay $8 to buy it. It amazes me that it's 2014 and we are still discussing A-shares. Apparently ethics are still an optional aspect of parts of the finance industry. Ten S&P 500-index sectors instead of one S&P 500 fund. I have to admit that this puzzled me greatly when I first saw it. Why own all 10 sectors of the S&P instead of a single-transaction S&P 500 index? (The sectors are consumer discretionary, consumer staples, energy, financials, health care, industrials, information technology, materials, telecommunications services and utilities). There were two explanations, neither of which seems to be any good: The first is to hold them in equal 10 percent allocations. This means that you are wildly overweight the smaller sectors, such as telecom, which is normally 2.4 percent, or utilities, at 3.1 percent. At the same time, you would be underweight in technology (18.7 percent), financials (16.1 percent) and health care (13.2 percent). There are big advantages to owning all 500 stocks in the S&P 500 in an equal weighting — it eliminates all of the distortions that market capitalization weighting causes. Indeed, many studies find that market cap weighting is the worst way to own a broad index. (See Research Affiliates' "Beyond Cap Weight.") There are even funds that do this for you, such as the Guggenheim S&P 500 Equal Weight. However, when you own each of the 10 S&P sectors, the holdings still consists of individual components weighted according to capitalization. It's hard to see the benefit of that. The second approach is to rotate among the sectors. The odds of outperforming the index by doing this are exceedingly small. That is before you factor in trading costs and taxes. All told, this a highly suspect strategy that seems more intent on generating turnover — and commissions — than performance. Tax-deferred products sold in IRAs and 401(k)s. An entire universe of investments has one purpose: to provide a return without generating a taxable event. Think municipal bonds (or municipal bond mutual funds), or insurance products such as annuities or whole life insurance. All of these products are priced to generate an equivalent after-tax basis return. In other words, you get less in terms of yield, but on balance can come out ahead. Putting these products into tax-deferred accounts defeats their reason for existing, and instead creates an investment that is built to underperform. I don't know how this happens, but it does. As you can see, it's no trouble to find terrible investment ideas. That's the first half of my list, and no doubt by year's end we'll hit 10 — or more. Next time you feel yourself getting sucked into some nouveau crap investment, remember to stick to your sound and solid long-term strategy. ~~~ Ritholtz is chief investment officer of Ritholtz Wealth Management. He is the author of "Bailout Nation" and runs a finance blog, the Big Picture. Twitter: @Ritholtz.

http://www.washingtonpost.com/business/barry-ritholtz-offers-the-worst-investing-ideas-hes-heard-this-year/2014/07/03/0f93fc40-0067-11e4-b8ff-89afd3fad6bd_story.html

|

| Posted: 12 Jul 2014 05:00 AM PDT Settle in for some deep dives: Its our longer form, weekend reading:

Whats up this weekend?

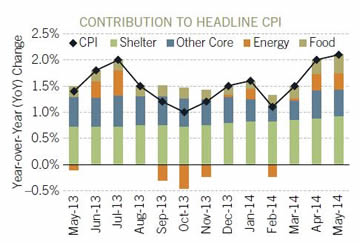

Inflationary trends have picked up in 2014

|

| Posted: 12 Jul 2014 03:00 AM PDT Hunton has been making custom, ultra-deluxe, powerboats for wealthy Europeans for 30 years. And now rich Americans can have their Hunton too. For the first time the company is marketing boats in the US. Called the Aston Martin of the Seas, the XRS43 model costs up to a million dollars. Video by: Kelly Buzby, Victoria Blackburne-Daniell. This $1M British Boat Will Make James Bond Jealous |

| Kiron Sarkar’s Weekly Report (12th July 2014) Posted: 12 Jul 2014 02:00 AM PDT Emerging market (EM) bond sales in the 1st half of this year have exceeded total sales in 2013, as investors seek higher yielding assets. The market is pricing in a rise in US interest rates in Q3 next year, though I expect, US interest rates to rise earlier than current market expectations. However, as US rates increase and the US$ rises, I suspect that a number of emerging market issuers will face significant difficulties and, in addition, refinancing will become a material problem. A sell off of bonds will also negatively impact EM currencies. Japanese investors significantly increased their purchases of foreign assets, mainly bonds, in May. Interestingly, in the Eurozone (EZ), they preferred French as opposed to German bonds, on the basis that they offer a higher yield and that the politics of the EZ makes them "safer" than would be suggested by the data. Indeed, Japanese investors were net sellers of German bunds, whilst they bought just over Yen 1.9tr of French bonds, more than their Yen1tr of purchases of US bonds. European markets were lower on the week – the concern that a major Portuguese bank (Espirito Santo) missed its debt payment weighed on markets. Furthermore, European economic data, including factory output data, came in well below expectations. While there is some evidence that UK growth is cooling, I wouldn’t be surprised if one or more members of the Bank of England’s (BoE) monetary policy committee votes to increase rates in the next few months. Such a move would be positive for Sterling. US bond yields, having risen following the much better than expected non farm payrolls report, declined last week. The 10 year closed at 2.52%. The weaker European markets, as a result of worse than expected economic data, combined with problems with one of Portugal’s largest banks, drove investors to the safety of bonds. However, I continue to believe that the 10 year US bond yield will rise to closer to 3.0% by the year end as the economy continues to improve and as expectations of an increase in interest rates by the FED are brought forward. Whilst US markets closed somewhat weaker, money continues to be allocated to equities which, combined with a lack of alternatives, suggests that markets should trend higher. The results and, in particular, forward guidance during the current US earnings season will clearly be important. US The May JOLTS survey points to a strengthening US employment market, with job openings at their highest level since Q3 2011. The FED minutes revealed that QE3 is expected to end in October. Whilst being more upbeat on the US economy, the FED minutes did not suggest that they would raise interest rates anytime soon. The market expects rates to rise in Q3, though I must admit, I believe the FED will act earlier. Various means to reach policy normalisation (ie rate hikes) were discussed, including the overnight reverse repo rate and on interest paid on excess reserves. Interestingly, "many" Fed members wanted to keep reinvesting the income of the FED's asset purchase programme until or after interest rates are increased. Overall, the minutes were more dovish than many, including myself, had expected. Consumer credit rose by US$19.6bn in May, slightly below the forecast of arise to US$20bn and the increase of US$26.1bn in April. Non-revolving credit comprised the majority of the increase. Credit is expected to increase in coming months, adding to growth. Europe French industrial output declined by -1.7% lead by a -2.3% decline in manufacturing, much worse than the rise of +0.2% expected. Italian data was also poor. Industrial output declined by -1.2%, as opposed to the rise of +0.2% expected. Furthermore, Italian and French April data was revised lower. UK factory output declined by -1.3% in May M/M, the most since January 2013. The forecast was for a gain of +0.4%. The strength of Sterling may be having an impact. The UK’s British Retail Consortium reported that prices fell by -1.8% Y/Y in June (-1.4% in May), the largest decline in prices since June 2006 and the 14th consecutive monthly decline. Supermarket wars, combined with discounting of clothing and a stronger Sterling has resulted in prices declining. As expected the BoE left interest rates unchanged at 0.5%. The UK May trade deficit rose to £9.20bn, higher than the £8.81bn in April. Exports rose by +0.6%, whilst imports increased by +1.7%. With a surplus on services, the total trade deficit came in at £2.42bn, up from £2.05bn in May. Japan Reuters reports that the BoJ may reduce its economic forecast next week to reflect the greater than expected negative impact of the sales tax rise on 1st April. The BoJ had forecast that the economy would grow by +1.1% for the fiscal year ending 31st March 2015, though Reuters suggests that the forecast will be reduced to +0.9%. Japanese core machinery orders fell by -19.5% in May M/M, the largest decline on record and much worse than the gain of 0.7% expected. Whilst a generally volatile data point, the decline suggests that consumer spending will decline following the sales tax rise and that export growth is weak, with capex low, though the recent Tankan report suggested that capex would increase by +7.4% in the fiscal year ending 31st March 2015. China Chinese PPI declined by -1.1% Y/Y in June, more than the decline of -1.0% expected and as compared with the decline of -1.4% in May. CPI rose by +2.3%, below the forecast of +2.4% and +2.5% in May. The government’s CPI target is +3.5%. The lower than expected CPI and PPI allows the government to increase its stimulus. measures to bolster its economy. However, the finance minister stated that the country would not embark on a stimulus lead growth plan. Chinese exports rose by +7.2% in June Y/Y, lower than the estimate of +10.4%. Import rose by +5.5%, lower than the rise of +6.0% expected, resulting in a trade surplus of US$31.6bn, lower than the estimate of US$36.95bn. It must be remembered that the data has been and probably continues to be suspect. The Chinese finance minister stated that the country would not stop intervention in the Yuan as the economy was weak and capital flows were not steady enough. Local authorities seem to be relaxing curbs on property purchases to avoid a decline in prices. The sector remains key problem for the Chinese economy, given (highly?) overvalued property prices. Other The 1st budget by the new BJP administration in India failed to meet expectations. The problem of increasing costs associated with subsidies was not addressed. The budget was similar to that proposed by the former government and both revenue and cost estimates seem optimistic. The euphoria which welcomed the current regime may well start to dissipate in coming months. S&P has warned some time ago that India may lose its investment grade rating, a view they repeated following the announcement of the budget. Kiron Sarkar |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment