The Big Picture |

- Gates, Fees, and Preemptive Runs

- Bad Economic Policy Is Partly to Blame for Ferguson

- David Letterman Remembers Robin Williams

- 10 Tuesday PM Reads

- Oil Boom’s Effect On The U.S. Economy

- A Data Junkie Looks at the News

- 10 Tuesday AM Reads

- Quantifying the impact of chasing fund performance

| Gates, Fees, and Preemptive Runs Posted: 20 Aug 2014 02:00 AM PDT Gates, Fees, and Preemptive Runs

In the academic literature on banks, "suspension of convertibility"—that is, preventing the exchange of deposits at par for cash—has traditionally been seen as a potential means of preventing economically damaging bank runs. In this post, however, we show that giving a financial intermediary (FI) the option to suspend convertibility may ultimately increase the risk of runs by causing preemptive runs. That is, investors who face potential restrictions on their future access to cash may run when they anticipate that such restrictions may be imposed. This insight is relevant for policymaking in today's financial system. For example, in July 2014, the Securities and Exchange Commission adopted rules that are intended to reduce the likelihood of runs on money market funds (MMFs) by giving the funds' boards the option to halt (or "gate") redemptions or to charge fees for redemptions when liquidity runs short, actions analogous to suspending the convertibility of deposits into cash at par. Our results show that the option to suspend convertibility has important drawbacks: A bank, MMF, or other FI with the option to suspend convertibility may become more fragile and vulnerable to runs. In other words, we show that instead of offering a solution, policies relying on gates and fees can be part of the problem. Preemptive Runs Consider what happens if uncertainty suddenly develops about the return on the FI's investment. In particular, suppose that, at date 1, a portion of the FI's investors—call them "informed"— learn that the FI's investment returns are more volatile than originally thought. Let's also assume that both the FI and the informed investors will learn at date 2 whether the FI's investment has actually soured. At date 1, the informed investors have a choice. They can immediately redeem to obtain their cash, which would force the FI into a costly liquidation of the investment. Alternatively, they can wait for the uncertainty to be resolved, since a favorable outcome for the FI's investment will allow them to obtain a positive return at date 3. For the FI and the economy as a whole, having investors wait is clearly better. This would avoid costly liquidation and allow for the possibility that the investment might turn out to be profitable, in which case everyone will be (ex post) better off waiting until date 3. In fact, we show that under fairly general conditions, if the FI cannot suspend convertibility by imposing gates or fees on redemptions, informed investors will optimally decide not to run at date 1. Instead, they will wait until uncertainty is resolved at date 2, because waiting may allow them to partake of the positive return on the FI's investment if it turns out to be profitable. After all, these investors would still have the option of redeeming at date 2 if they learn that the FI's investment has turned out to be bad. But what happens if the FI can impose a gate or fee at date 2? We show that if the FI's investment turns out to be bad, the FI will exercise its option to impose gates or fees on investors at date 2. In this case, informed investors may obtain less than what they originally deposited with the FI, because they must share the loss with the FI's other investors. This risk causes informed investors to run preemptively from the FI at date 1 in anticipation of the possibility that convertibility may be restricted at date 2. Conclusions Even though our model does not address how runs on FIs can create large negative externalities for the financial system and the real economy, one important policy implication is clear: Giving FIs, such as MMFs, the option to restrict redemptions when liquidity falls short may threaten financial stability by setting up the possibility of preemptive runs. Disclaimer

|

| Bad Economic Policy Is Partly to Blame for Ferguson Posted: 19 Aug 2014 10:30 PM PDT The Terrible Handling of the Economic Crisis Is a Cause of the Ferguson Riots

We noted 3 years ago that the terrible handling of the economic crisis would lead to civil unrest and riots. We noted that:

The looting and chaos in Ferguson, Missouri is not justifiable … but it's largely caused and inspired by the looting on Wall Street. As basketball great Kareem Abdul-Jabbar notes, this isn't a race war … it's a class war. And corrupt government policy is largely to blame. |

| David Letterman Remembers Robin Williams Posted: 19 Aug 2014 07:00 PM PDT Dave pays tribute to the great Robin Williams.

|

| Posted: 19 Aug 2014 01:00 PM PDT My afternoon train reads:

What are you reading?

Americans are taking fewer vacations than they used to

|

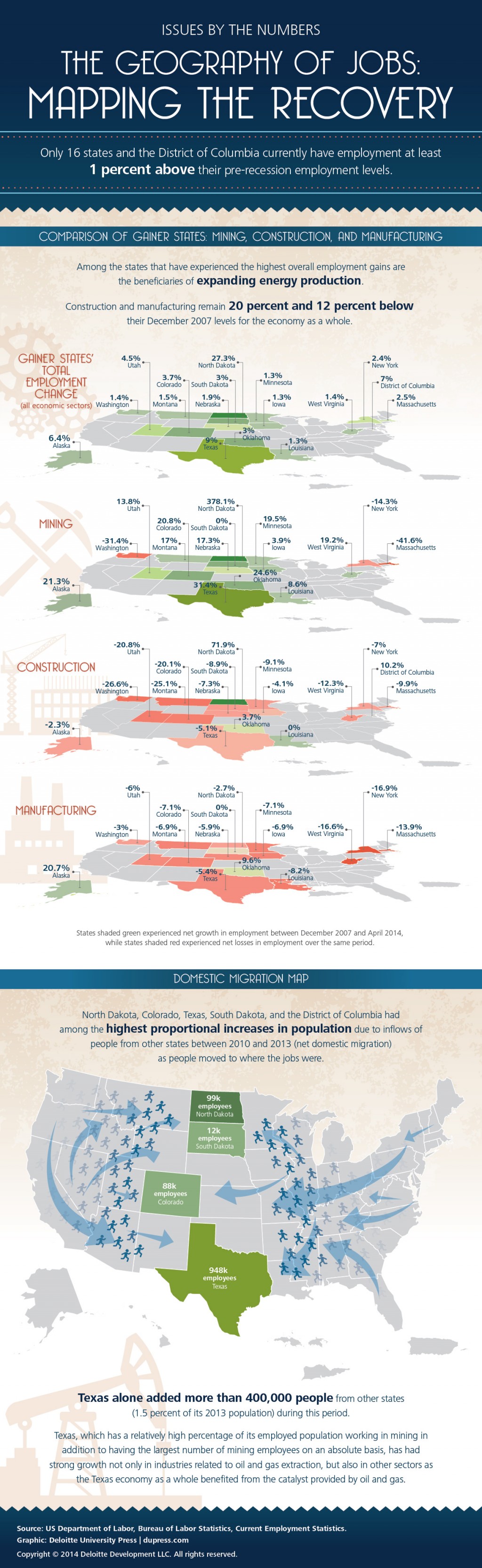

| Oil Boom’s Effect On The U.S. Economy Posted: 19 Aug 2014 11:00 AM PDT

|

| A Data Junkie Looks at the News Posted: 19 Aug 2014 08:00 AM PDT Many years ago, when I was a poor and humble graduate student, I taught the prep course for students taking the GMATs and LSATs. I understood the internal logic and game theory needed to succeed on standardized tests, and could explain techniques used to do well on them. One of the keys to succeeding on these tests was to have strong reading comprehension skills. Toward that end, I taught what I like to call active reading. It required the reader to approach text in a rigorous and logical way, challenging each sentence to find assumptions, false statements and deductive errors. Think of it as logical skepticism. I still use these muscles everyday. I can randomly pick up any newspaper article or analyst report, and find holes and flaws merely by asking questions the author left unanswered. Active reading often leads to the conclusion that the vast majority of news is at best incomplete and uninformative, while a majority of research reports are full of biases and logical errors. That is a pretty bold statement, and to demonstrate this, I am going to take a random article and dissect it using logical skepticism. When I am finished, you will have a better understanding of why I often say "Lose the News." I hope you never look at media noise in the same way. Yesterday, an article decided to take stock of investors’ concerns, quoting many strategists and managers. I chose it because it was well-written and researched, and offered the perspectives of many strategists. However, this exercise can be done with any article or research piece written by anyone anywhere.

|

| Posted: 19 Aug 2014 06:30 AM PDT Here are our morning reads, sourced exclusively from a craft brewer located in Brooklyn (continues here):

|

| Quantifying the impact of chasing fund performance Posted: 19 Aug 2014 03:00 AM PDT |

/cdn0.vox-cdn.com/uploads/chorus_asset/file/658582/vacation.0.png)

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment