The Big Picture |

- Deflation Fears

- 10 Tuesday PM Reads

- Student Loans Are Going to Crush the Economy! (No, they are not)

- How America’s Consumers Spend Across States

- MAD Magazine recreates Norman Rockwell’s famous 1958 painting ‘The Runaway’

- 10 Tuesday AM Reads

- Stack: Competition to Call the Next Bear Market

- MiB: Sheila Bair, Chairman of FDIC

| Posted: 26 Aug 2014 04:30 PM PDT Deflation Fear

A worldwide deflation fear is expanding and may actually be rampant. BCA Daily Insights (August 25, 2014) notes that, "out of 32 OEC countries, more than two-thirds have domestic inflation rates that fall short of 1%." BCA analysts go on to argue that the worldwide inflation rate may converge to zero over the next couple of years. Debt markets currently reflect this fear. Here are examples of yields on the benchmark 10-year interest rate for sovereign debt. This is not about credit risk. This is about the risk that the global price-level change will approach or reach zero.

These are unexpected and remarkably low yields. They reflect the results of central bank policies and the results of growing fear of disinflation or even deflation. Is it any wonder that central bank actions which expand quantitative easing produce little or nothing beyond growing balances of excess reserves as those created monies recycle back into the central banks? Is it any wonder that an alternative form of recycling monies in the US, the reverse repo, is currently functioning at an administered interest rate of 5 basis points (0.05 of 1%). The answer is No! Worldwide deflation risk is serious business, and it is rising in the eyes of market agents. It means that central bank policies are neutralized. The central banks of the world have tripled the amount of excess reserves since the financial crisis commenced. If they were to quadruple the amount of reserves in the next year, doing so would not make much difference. Does it make any difference if the Federal Reserve holds an extra half trillion dollars of Treasury securities that are reflected in a rising balance of a reverse repo or in additional excess reserves? The answer essentially is no. For the last six years, central banks worldwide have collectively offset the failure of their governments' fiscal policies. That is about all they could possibly do. They have enabled nearly all creditworthy corporate and institutional borrowers to successfully undertake refinance at very low interest rates. That is about all they could possibly do. They have enabled creditworthy individuals and households to refinance household debt in order to realign their debt service payments. That is about all they could possibly do. Unfortunately, governing executive branches, including the Obama administration in the US, still do not get it. The legislative branches in the mature economies and governments of the world continue to appear to be broken. The culprits are not the central banks. They have done all that they can. ~~~ David R. Kotok, Chairman and Chief Investment Officer, Cumberland Advisors |

| Posted: 26 Aug 2014 01:30 PM PDT My afternoon train readings:

What are you reading?

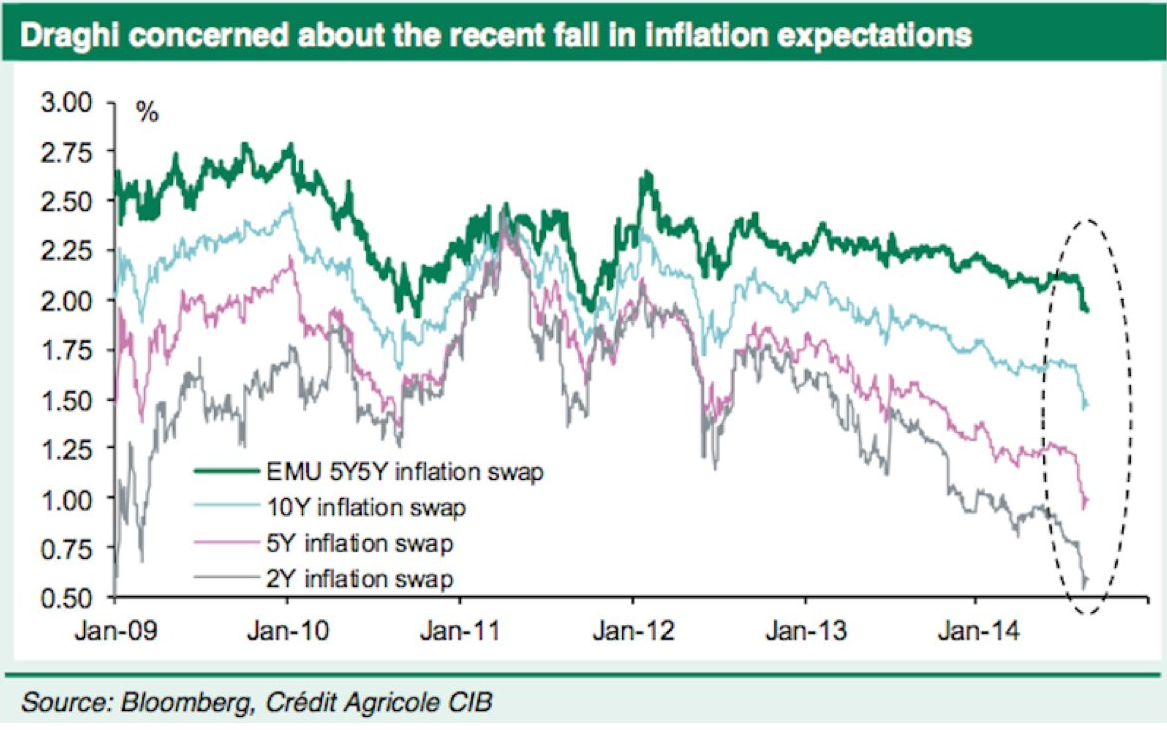

Draghi concerned about the record fall in inflation expectations

|

| Student Loans Are Going to Crush the Economy! (No, they are not) Posted: 26 Aug 2014 11:19 AM PDT

Student loans are the next great subprime crisis! At least that’s what the usual purveyors of doom and gloom say (see this, this and this). The numbers are big, the default rates are high and soon enough this is going to tip the economy into the next crisis or recession. Not so fast, writes Torsten Slok, chief international economist for Deutsche Bank AG, in his forthcoming September chart-book

|

| How America’s Consumers Spend Across States Posted: 26 Aug 2014 08:30 AM PDT |

| MAD Magazine recreates Norman Rockwell’s famous 1958 painting ‘The Runaway’ Posted: 26 Aug 2014 07:00 AM PDT |

| Posted: 26 Aug 2014 06:30 AM PDT Just because it’s Tuesday does not mean we don't have you covered with our dry-aged, prime reads: (continues here):

continues here |

| Stack: Competition to Call the Next Bear Market Posted: 26 Aug 2014 06:00 AM PDT Jim Stack of Investech has described what he calls “the competition to call the next bear market.” We have been going discussing this issue, and I am saving his comments for a Bloomberg column next week. But here is a flavor of what he has been writing, from his most recent commentary:

It would be quite amusing if it weren’t such a money loser so far . . . |

| MiB: Sheila Bair, Chairman of FDIC Posted: 26 Aug 2014 04:00 AM PDT Sheila Bair, former chairman of the U.S. Federal Deposit Insurance Corp., describes what it was like in the room with former Treasury Secretary Hank Paulson and former Federal Reserve Chairman Ben Bernanke when the global economy was on the verge of falling into the abyss in this week’s “Masters in Business” podcast. Listen to the full interview below, or click through to Soundcloud. Early in her career, Bair was recruited by Kansas Senator Bob Dole to serve as a counsel on the Senate Judiciary Committee. She eventually rose to become counsel to Dole when he was Senate majority leader. Bair was commissioner and acting chairman of the Commodity Futures Trading Commission from 1991 to 1995 before serving as senior vice president for government relations at the New York Stock Exchange from 1995 to 2000. She was appointed as chairman of the FDIC in 2006. Under her direction, the FDIC was rated the best place in government to work. Her book on her time at the FDIC and the financial crisis is “Bull by the Horns: Fighting to Save Main Street from Wall Street and Wall Street from Itself.” Bair has some surprising things to say about women in politics, bipartisanship and what it was like turning the FDIC around. You can stream the podcast at SoundCloud or download it here. Next week, I’ll talk with James O'Shaughnessy of O'Shaughnessy Asset Management and author of “What Works On Wall Street.”

|

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment