The Big Picture |

- Inherent Vice

- What If You Were the World’s Greatest Stock Picker® ?

- Mib: BAM’s Larry Swedroe

- 10 Weekend Reads

- Kiron Sarkar’s Weekly Report 10.11.14

| Posted: 11 Oct 2014 05:00 PM PDT This looks awesome:

INHERENT VICE, in theaters December 2014. "Inherent Vice," is the seventh feature from Paul Thomas Anderson and the first ever film adaption of a Thomas Pynchon novel. When private eye Doc Sportello's ex-old lady suddenly out of nowhere shows up with a story about her current billionaire land developer boyfriend whom she just happens to be in love with, and a plot by his wife and her boyfriend to kidnap that billionaire and throw him in a loony bin…well, easy for her to say. It's the tail end of the psychedelic `60s and paranoia is running the day and Doc knows that "love" is another of those words going around at the moment, like "trip" or "groovy," that's being way too overused—except this one usually leads to trouble. With a cast of characters that includes surfers, hustlers, dopers and rockers, a murderous loan shark, LAPD Detectives, a tenor sax player working undercover, and a mysterious entity known as the Golden Fang, which may only be a tax dodge set up by some dentists… Part surf noir, part psychedelic romp—all Thomas Pynchon. The film stars Oscar nominees Joaquin Phoenix ("The Master," "Walk the Line"), Josh Brolin ("True Grit," "No Country For Old Men") and Owen Wilson ("The Royal Tennenbaums," "Midnight in Paris"); Katherine Waterston ("Michael Clayton," "Boardwalk Empire"); Oscar winners Reese Witherspoon ("Walk the Line") and Benicio Del Toro ("Traffic"); Martin Short ("Frankenweenie"); Jena Malone ("The Hunger Games" series); and musician Joanna Newsom. Oscar nominee Paul Thomas Anderson ("There Will Be Blood," "The Master") directed "Inherent Vice" from a screenplay he wrote based on the novel by Thomas Pynchon. Anderson also produced the film, together with Oscar-nominated producers JoAnne Sellar and Daniel Lupi ("There Will Be Blood"). Scott Rudin and Adam Somner served as executive producers. Anderson's behind-the-scenes creative team included Oscar-winning director of photography Robert Elswit ("There Will Be Blood"), production designer David Crank ("The Master"), Oscar-nominated editor Leslie Jones ("The Thin Red Line"), and Oscar-winning costume designer Mark Bridges ("The Artist"). The music is by Radiohead's Jonny Greenwood. Warner Bros. Pictures presents, in association with IAC Films, a JoAnne Sellar/Ghoulardi Film Company production, "Inherent Vice." Opening in limited release on December 12, 2014 and expanding on January 9, 2015, the film will be distributed by Warner Bros. Pictures, a Warner Bros. Entertainment Company. "Inherent Vice" has been rated R for drug use throughout, sexual content, graphic nudity, language and some violence. |

| What If You Were the World’s Greatest Stock Picker® ? Posted: 11 Oct 2014 08:00 AM PDT Even if you could pick huge winners, could you hold them?

Let's imagine for the moment that you are the World's Greatest Stock Picker®. You have an uncanny talent for ferreting out "the next Microsoft" — companies that are on the sharpest edge of what's next, that are about to undergo tremendous growth. These firms will rule the world: They will be the most powerful, profitable and influential corporate entities known to man. Even better, your superpower is that you can find these companies when they are tiny, before they have had their explosive growth, when hardly anyone has heard of them. You find and buy these stocks while their prices are still in the single digits. Companies like Apple, Google, Tesla, Netflix and Chipotle that will one day measure their growth in increments of thousands of a percent. Can you imagine how much wealth you could create? I have some bad news for you, kiddos: Even if you had that superpower, it would be worth surprisingly little to you. The odds are that it would not create much wealth, and it might even cost you money. How could that be possible? The short answer is your brain. The three-pound ball of gray matter sitting atop your spinal cord was never designed to make risk/reward decisions in capital markets. It took about 100,000 years to optimize for its intended purpose: Keeping you alive. The occasional Darwin Award aside, it does an outstanding job of keeping you safe from all manner of predators on the savannah. That you now live in a condo and enjoy lattes is irrelevant to its functionality. Its job remains keeping you alive long enough for you to procreate, pass your genes along and perpetuate the species. This dynamic, opportunistic, self-organizing system of systems occasionally runs into trouble when we try to force it to perform other, "off-label" uses. That includes buying and selling pieces of paper that represent tiny slices of companies. As we shall see, that big, under-utilized brain of yours is no help anytime it gets over-stimulated by your emotions. Which is precisely why being the World's Greatest Stock Picker® is unlikely to be how any of you is going to get rich. Let's use the shares of five companies as examples: Google, Tesla, Chipotle, Netflix and Apple. The performance of each since its initial public stock offering has been nothing short of astounding. Since going public, each stock has generated returns of more than 1,000 percent. A $10,000 IPO allocation in any one is now worth at least $100,000. To give you an idea of just how phenomenal these companies have done, Google is the laggard of the lot. Since its IPO in August 2004, it has gained a mere 1,282 percent. Tesla edged out the boys from Mountain View, Calif., with a gain of 1,352 percent. And they did it in less than four years — Tesla's IPO was June 2010 — vs. the decade it took Google to gain 1,000 percent. Those spectacular returns look downright paltry compared with the 2,865 percent gain Chipotle has had since going public in 2006. And Netflix beats that, rising 5,816 percent since 2002. Then there is Apple. It is a beast unto itself, racking up a mind-boggling 22,288 percent in appreciation since its 1980 debut. It has become world's biggest company by market capitalization. Even if you bought large chunks of each of these firms at their IPOs, the odds are that nearly all of these giant gains would have eluded you. Why? As I shall show you, each of these companies would have sent you running for the exits — repeatedly — over the years, screaming as if your hair were on fire. Don't believe me? Consider the facts:

How often have you invested in a stock, only to get scared out of it when things grew shaky? That's fairly typical behavior for investors. Now imagine how you would have behaved if you happened to have a significant part of your net worth tied up in that one holding. Let's say a decade ago, you put $15,000 into Apple. You bought 1,000 shares at $15 (with $13 cash) because you thought that newfangled iPod had some potential. Since then, it split two for one and then earlier this year, it split seven for one. You now are holding 14,000 shares of Apple. At the current price of about $100, it is worth $1.4 million dollars. For most people, this is a very high percentage of their net worth. How well do you sleep when 90 percent of your total net worth goes through giant swings? Apple was worth about the same amount in September 2012 — just before it gave back almost half its value, falling 44 percent. Would you have held on? What about all of those prior 50 percent corrections? This is not an academic theory. Consider how you have reacted to much more modest drops in your holdings. How often were you shaken out of a stock, only to see it rocket higher after you sold? And somebody was dumping stocks in March 2009; after all, selling climaxes (also known as capitulation) are how bottoms are made. Some years ago, I recommended to the brokers I worked with to do just that regarding Apple. They bought millions of shares at an average price of $15. At $20 dollars, they were selling it, whooping it up and high-fiving one another. When I asked why they were selling it when my price target was higher ($30!), I was told: "It's a 33 percent winner — time to ring the bell, Ritholtz!" That was even before any trouble had hit. How many of you, dear readers, could hold onto a giant winner like these five for the duration? How do you know that any of these are not about to turn into a classic disaster stock? Think about once-giant winners that collapsed: Lehman Brothers, WorldCom, Lucent, JDS Uniphase. All of these were one-time market heroes; all went bust in spectacular fashion. Your superpower gives you the ability to find the giant winners, but it does not give you the ability to hold onto them, nor does it give you the ability to distinguish between the superstars and the washouts. As we have discussed previously, this is a feature, not a bug. The good news is your brain has kept you alive long enough to read this column. The bad news, it also made you sell Apple 10,000 percent ago. The reality is, when it comes to risk/reward decisions, you are just not built for it. ~~~ Ritholtz is chief executive of Ritholtz Wealth Management. He is the author of "Bailout Nation" and runs a finance blog, the Big Picture. On Twitter: @Ritholtz. |

| Posted: 11 Oct 2014 07:00 AM PDT This week's Masters in Business Radio show at 10:00 am and 6:00 pm on Bloomberg Radio 1130AM and Siriux XM 119 (it also repeats all weekend). Our guest this week is Larry Swedroe, best known as research director for the BAM alliance, and author of 14 books on investing. You can listen to the show live here. Shortly after the show, you can stream it at Soundcloud or download the 74 minute podcast here. (all are posted now). All of the past Podcasts are here (and coming soon to Apple iTunes). Next week, we speak with Jim Bianco of Bianco Research.

Books by Larry Swedroe:

|

| Posted: 11 Oct 2014 04:00 AM PDT Heckuva a week. Settle into your favorite easy chairs, pour yourself a hot cup-o-joe, and reflect on some of the bigger issues with our longer form weekend reads:

Whats up this weekend?

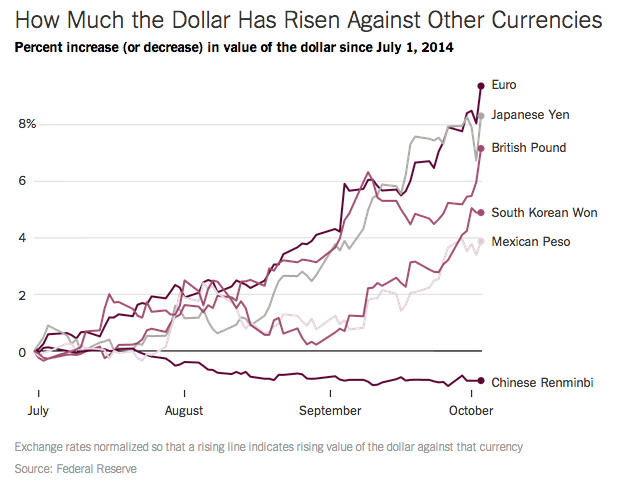

What the Dollar’s Rise Tells Us About the Global Economy |

| Kiron Sarkar’s Weekly Report 10.11.14 Posted: 11 Oct 2014 03:00 AM PDT The ECB has kept the Eurozone (EZ) afloat to date. However, I can’t help feeling that it is running out of options. A QE programme, involving the purchase of EZ sovereign debt, remains unlikely primarily due to German opposition. The ABS/covered bond purchase programme, combined with the TLTRO's will help, but will not be enough to stimulate the EZ economy, which is showing clear signs of slowing and is now impacting even Germany. Indeed, the likelihood that Germany was in recession in Q3 is rising, given the string of particularly weak August economic data. The German government is to reduce its 2014/15 growth forecasts next week. With inflation, in particular core inflation, looking as if it will decline even further, the risks of deflation in the EZ are rising. Downside risks have risen materially, which suggests that the Euro has further to fall, despite the more dovish than expected FED minutes and its reference to a stronger US$ hurting the US economy. I continue to believe that the Euro is heading for US$1.20 this Q. Commodity currencies, such as the A$ and the Peripheral EZ bond yields have fallen, with the Spanish and Italian 10 year yielding 2.07% and 2.32% respectively. The ECB is unlikely to implement a QE programme and with the slowdown in the region, combined with the deteriorating fiscal position in both countries, yields at these low levels look far too low. I would expect that yields will rise in coming months. The US Q3 earnings season is upon us. Generally, companies are expected to report positive results, though I would not be surprised if they refer to the negative impact of the stronger US$. However, the US remains the safer play and is likely to remain so for quite a while. The continued weakness in global economic data looks set to continue. Furthermore, the FED is to cease its QE programme this month, though proceeds from maturing securities will continue to be reinvested. With reduced liquidity and greater uncertainty, I remain highly cautious of equity markets. The EZ, Japan and China look particularly problematical. Emerging markets are also vulnerable, as liquidity declines and the US$ rises. US The August job openings and labour turnover survey (JOLTS) reports that there were 4.84mn job vacancies, higher than the 4.7mn expected and the 4.61mn in July. Vacancies are now at their highest level since January 2001.Weekly jobless claims came in at 287k, below the forecast of 295k and last weeks 288k. The less volatile 4 week moving average declined to 287.75k, the lowest since February 2006. A pretty decent number. The stronger US$ has reduced import prices for the 3rd consecutive month. They were down -0.5% M/M (-0.7% expected) in September and -0.9% lower Y/Y. Lower petroleum prices was the main reason for the decline. EU German industrial production collapsed by -4.0% in August M/M (-2.8% Y/Y, as opposed to -0.5% expected), much greater than the decline of -1.5% expected and the gain of +1.6% in July. It was the largest fall since January 2009. Output of investment goods declined by -8.8% M/M, with intermediate goods falling by -1.9%. German exports declined by -5.8% in August, the most since January 2009 and well below the -4.0% decline expected and the increase of +4.8% in July. Whilst the summer holidays could have impacted, it does suggest that the German economy is slowing. Imports declined for the 2nd consecutive month. They were down by -1.3%, having fallen by -1.4% in July and well below the increase of +0.9% expected. The steep decline in factory orders, industrial production and exports is yet more evidence of a sharp slowdown within the German manufacturing/export sectors, as the EZ economy deteriorates, global growth weakens (the slowdown in China is also particularly important for Germany) and geopolitical problems increase (Ukraine), though domestic consumption is holding up at present. The particularly weak data also increases the risk that Germany was in recession last Q, having declined by -0.2% in Q2. Mrs Merkel is considering options to stimulate growth, including lowering the mandatory pension contribution by -0.6%, according to Mr Michael Fuchs, the deputy leader of Mrs Merkel's CDU party. The measure, if implemented, would inject around E6bn into the German economy. The EZ October investor confidence index, the Sentix index, declined for the 3rd consecutive month to -13.7, well below the -11.0 expected and the reading of -9.8 in September. It was the lowest reading since May 2013. The ECB will release the results of its asset quality review and stress tests carried out on the largest banks in the region (130 in total) on 26th October. Some banks are expected to fail and will have to submit plans within 2 weeks to explain how they will raise the capital necessary (within 6 months) to meet the relevant criteria. UK industrial production was unchanged in August M/M (+2.5% Y/Y), in line with estimates. Manufacturing production rose by +0.1% M/M (+3.9% Y/Y), also in line with forecasts. The UK's Chamber of Commerce warned that companies have reported the weakest export growth in 2 years, with a material slowdown in manufacturing. The UK economy is slowing, mainly due to the weakening EZ economy, though GDP growth should come in at around +0.7% last Q. As expected the BoE left interest rates unchanged. The minutes are to be published on 22nd October. Other than Mr Weale and Mr McCafferty, it is unlikely that any more members of the 7 person committee voted to hike rates. Japan Importantly, the BoJ did reduce its assessment on industrial production, which suggests that it will cut its growth forecasts this month. Furthermore, a majority of board members want the BoJ to abandon its 2 year timeframe to reach their 2.0% inflation target, which ends in April 2015. With inflation, ex the impact of the April sales tax hike, at just +1.1% Y/Y in August and slowing, I believe that the BoJ will have to increase the size of its monetary accommodation policy, leading to a weaker Yen. The August trade deficit widened to Yen 831.8bn, above forecasts of Yen 770.7 bn. Furthermore, the seasonally adjusted August current account surplus came in at Yen 130.8bn, as opposed to Yen 186.8bn expected. Japanese investors are selling German, French and Italian bonds and investing in US, UK, Australian and Canadian bonds. Seems a far more sensible policy. China The Chinese Academy of Social Sciences, the main government supported research organisation, forecast that GDP for 2014/15 would come in at +7.3% this year and just 7.0% next. They added that the governments 2014 forecast of +7.5% would be "hard to meet". In reality, actual Chinese GDP is very likely to be significantly below these numbers. (Source Bloomberg). Other The IMF reduced its 2014/15 global growth forecasts marginally to +3.3% and +3.8% respectively, down from their previous forecasts of +3.4% and 4.0% respectively. They add that there is an increased risk of a correction in financial markets. In addition, they believe that the risk of the EZ falling into deflation (30%) and heading into recession (40%) are the major issues facing the world economy. EZ 2014/15 GDP was cut to +0.8% and +1.3% respectively, down from +1.1% and +1.5% previously. Furthermore, they have cut their forecasts for Japanese 2014/15 GDP growth to +0.9% and +0.8% respectively, down from +1.6% and +1.1% previously. US 2014 growth has been revised higher to +2.2%, from +1.7% previously and to +3.1%, from +3.0% for 2015. The governor of the Australian Central Bank, the RBA, stated that whilst the A$ had declined (down around 7.0% against the US$ in the last month), it "remained high by historical standards, particularly given the further declines in key commodity prices in recent months". As usual, the RBA is trying to talk down the currency. The RBA kept interest rates unchanged at 2.5%. Analysts believe that the RBA will hike interest rates next year, though I believe that the RBA will clearly try and avoid such a move. However, the key remains property prices, which continue to rise and which is a major concern for the RBA. The RBA recently suggested that they were discussing options with regulators to introduce measures to slow down property price rises. I continue to believe that the A$ will decline further and to below US$ 0.85 this Q. Russian inflation rose to +8.0% Y/Y (+0.7% M/M) in September, above the +7.6% rate in August and the highest in 3 years. Furthermore, inflation is expected to rise further, which will increase pressure on the Central Bank to raise rates yet again, despite having increased interest rates from 5.5% in February to 8.0% this year. The Rouble was one of the worst performing currencies in Q3, having declined by -14% against the US$, which has contributed to the increase of inflation. Bloomberg reports that the Russian Central Bank spent just over US$3bn this month to try and stem the Rouble's decline. It has also widened the Rouble's trading band. Russia's forex reserves fell to a 4 year low of US$456.8bn last week, the 6th consecutive weekly decline. Servicing and repaying US$ debts will increasingly become a major problem for Russian corporates. The incumbent Ms Dilma Rousseff won the most number of votes, but failed to achieve the majority needed to be re elected President in the 1st round of the Brazilian elections. Surprisingly, she now faces the more business friendly Mr Aecio Neves in the 2nd round on 26th October, rather than Ms Marina Silva, who was thought to be her main competitor. Ms Rousseff and Mr Neves are tied is the most recent polls. Oil prices continue to decline with November Brent around US$90 and in a bear market having fallen to the lowest level in over 2 years. Both Saudi Arabia and now Iran have discounted their prices by the most in 6 years. Furthermore, Saudi Arabia announced that it had increased production in September !!!. With supply rising and demand weak, as a result of the global economic slowdown, prices look as if they will remain under pressure. However, at around US$80/85, US shale oil becomes uneconomic, which could suggest a floor for prices around those levels. Kiron Sarkar |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

1 comments:

I must say, I thought this was a pretty interesting read when it comes to this topic. Liked the material. . .

cash forex russia

Post a Comment