The Big Picture |

- RWM is Coming to Wash, D.C. Next Week

- 10 Monday PM Reads

- Masters in Business: Jack Schwager’s Market Wizards

- The United States of Oil

- Trick Question: How Low Can Gold Go?

- How substituting chicken for beef affects inflation

- 10 Monday AM Reads

- Volatility

| RWM is Coming to Wash, D.C. Next Week Posted: 06 Oct 2014 04:00 PM PDT A quick reminder that later this month, we have only a few slots left to meet with me and our the head of Financial Planning group when we will be visit with clients and prospective clients in the Washington, D.C. area on October 15h and 16th. For those of you who are familiar with our investing philosophy, it is an opportunity to have a more in depth, personal conversation about your personal financial circumstances. For those of you who want to get the news straight from the horse’s mouth, come hear what I have to say on markets, the economy, and investing. (For a flavor of the conversation, check out the audio of our last quarterly conference call is below). If you are interested in discussing about your personal financial circumstances, meeting with us, or simply hearing our views, give us a call or email. Send email to Info -at- RitholtzWealth -dot- com, with the subject “DC Trip.” Or call 212-455-9122 and ask for Erika.

Our last quarterly conference call is after the jump.

This posting includes an audio/video/photo media file: Download Now |

| Posted: 06 Oct 2014 02:30 PM PDT My afternoon train reads:

What are you reading?

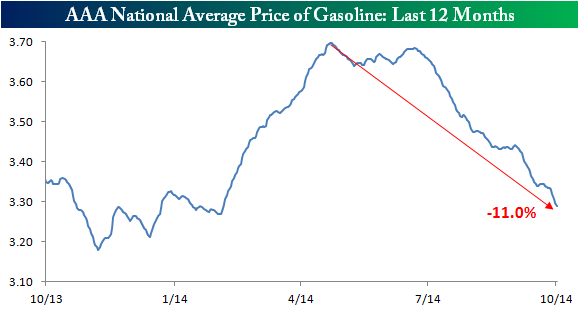

Gas Prices Down 11% From YTD Highs

|

| Masters in Business: Jack Schwager’s Market Wizards Posted: 06 Oct 2014 12:00 PM PDT In this week’s “Masters in Business” podcast, I talk with Jack Schwager, the author of “Market Wizards: Interviews With Top Traders.” More than 25 years after the first book was published in 1989, the series remains one of the most widely read books on Wall Street trading desks. In our interview, Schwager describes how he managed to convince numerous top traders and asset managers — many of whom were notoriously press shy — to have long, on-the-record conversations with him. He had begun his career as a research analyst at Commodities Corp., taking over the desk that Michael Marcus was vacating. Marcus, who went on to gain Wall Street fame by turning $30,000 into $80 million by trading commodity futures, spoke with Schwager about his approach to trading. Others who had avoided the limelight soon followed, and a classic work of finance was born. There are consistent themes found in Schwager’s interviews: discipline, risk management and capital preservation, intellectual flexibility, personal responsibility and honest self-appraisal. William Eckhardt, who famously debated with Richard Dennis about whether trading could be taught, summed up many of these rules with the quote: "Amateurs go broke taking large losses, professionals go broke taking small profits." You can hear the full interview, including the podcast extras, by downloading the podcast here or streaming it at SoundCloud. Next week, we speak with Larry Swedroe, Buckingham Asset Management's director of research.

Streaming audio podcast after the jump

|

| Posted: 06 Oct 2014 09:30 AM PDT

|

| Trick Question: How Low Can Gold Go? Posted: 06 Oct 2014 06:45 AM PDT One of the things I like to do in all of my musings is to find some thing or person who is wrong about an investing-related subject, then trying to figure out where they went awry. On occasion, small pearls of wisdom can be derived from this analytical process, as in this discussion on narrative. Other times, the lessons are simply an exercise in snarky fun, as in the “12 Rules of Goldbuggery.” Regardless, the underlying thesis is, "If only we can develop a set of intellectual tools to analyze investing errors, then we can apply them to ourselves and perhaps avoid making similar errors." The hope is that some degree of self-awareness avoids the sorts of systematic gaffes we see every day. That brings me back to the gold-industrial complex. I have criticized this group for their religious fervor, lack of discipline and deficient risk management. Their money-losing approach to investing via the narrative process, while ignoring the data in front of them, continues to bedevil unwise investors. Every possible investment has its own group of cheerleaders, including sales people and other dependents who want to see their particular asset flavor do well. It is in their own financial interest for prices to rise, so naturally they pay no heed to various warning signs. Gold’s fall below $1,200 an ounce last week is the reason I bring this up again. Reaching its lowest level since early 2010, as other precious metals such as silver and palladium are at or near five-year lows, is a good enough occasion to remind some readers of the errors of their ways.

|

| How substituting chicken for beef affects inflation Posted: 06 Oct 2014 05:00 AM PDT

I have a few words about inflation and the cowardly Boskin Commission at Marketplace Radio last week:

|

| Posted: 06 Oct 2014 04:30 AM PDT Welcome back to big show. October is now in full effect, and so you should expect some of the usual fun. Oh, and morning reads:

|

| Posted: 06 Oct 2014 02:30 AM PDT Volatility

An era is ending: for over half a decade, nearly worldwide, zero interest rates suppressed volatilities. That is over. The first sign of this evolution came over a year ago when the bond market experienced the "taper tantrum" as then Fed Chairman Ben Bernanke alluded to forthcoming rising interest rates. Since then, the re-volitization process has morphed to currencies, commodities, and stock prices. More and exciting volatilities lie ahead. We are likely to see the Dow Jones Industrial Average move precipitously up or down 200 points with greater frequency. Why not? Two hundred points is only about 1%. Contrast that with the Russell 2000 index which lost 10% since its summer peak. As the global zero-interest-rate era draws to a close, previously comforting, steady trends with smaller deviations are about to be replaced. That was the old normal of the past half-decade. In the stock market we are beginning to see the newer normal. We had some of it this week. In bonds, we have already seen the changes in volatility, first with the taper tantrum last year and now with the widening of the high-yield spread to Treasurys. Bond volatility shows up in spreads. It also shows up in large market moves when momentous news like Bill Gross's exit from PIMCO shocks markets and alters pricing. Sequential leadership changes at a two-trillion-dollar asset manager act to trigger market responses. Many know the existing holdings. They come to expect that large liquidations will occur. They know that, in a mutual fund, forced selling to raise cash may provide opportunity for the buyers who stand aside and wait for the seller to disgorge. The buyer gets the bargains, while the shareholders of the selling fund must accept the results of their redemptions. We saw some signs of that in the past week. Cumberland is ONLY a separate account manager. We do NOT manage any mutual fund. ETFs aside, we do NOT use traditional bond mutual funds in most cases. All of our clients have 100% transparency regarding their own accounts. All client accounts are private when it comes to any information about their holdings. We wouldn't have it any other way. Let's get back to market volatility. There is no central bank role in this gyration. Market agents must not and should not expect there to be. The Federal Reserve has reaches neutrality this month and is calculating a policy shift to raise interest rates. The Fed is not engaged in saving the skin of any money manager, regardless of size. That would change only if the entire system were threatened. Two trillion is a lot, but it is not enough to threaten the entire system. It is, however, big enough to produce jagged lines on volatility charts. Differentials in policy also cause higher volatility. The US is at neutral and has stopped QE. Market-based options pricing suggests that the policy-oriented Fed Funds rate will be somewhere between 0.50% and 0.75% by the end of next year. So we see volatility changes to anticipate that the US will nudge rates up from the zero boundary soon. Meanwhile, the European Central Bank is below zero and trying to figure out how to do more QE. The Bank of Japan continues its 20-year policy of zero interest rates. And the Bank of England looks to be directed toward normalizing and eventual tightening. All of that maneuvering adds to volatility in currencies. The big-four currencies used to be on the same zero-boundary path. No more. Currencies are the basic substance by which financial assets are priced. Markets clear all transactions in money. And though money was priced at zero rates, that is now changing. The dollar is getting stronger; the euro and yen are getting weaker; and the pound may be getting stronger. These are shifts from an era when the dollar remained weak for years and our QE was the leadership policy of central bank expansion. That situation has changed. Markets have changed. We have entered a new era. We may as well get used to it. Some market agents want the old regime to go on forever. Last week was a good example. Consultants contacted me over the course of the downdraft day. They expressed their relief about having a cash reserve. But Friday's surge after the labor report reversed the emails, texts, and messages to comments like, "Why didn't we spend the cash at the bottom of the down day, 24 hours preceding the up day?" C'mon. That actually came from a professional. Really! Back away from the day-to-day volatility and look at the week. Cumberland's largest overweight position in the US exchange-traded fund (ETF) portfolios is defensive. It is the Utilities sector. Last week, it was up 1.6% according to Barron's. The Telecommunications sector broke even last week. It, too, is usually characterized as a defensive choice. By the way, last week all the rest of the sectors were negative. Our most underweight positions are in Energy and Materials. Because of the relative size of the Energy sector, that sector is extremely underweight. Oil and gas sectors were down 4% last week. Energy sector ETFs do not do well when the commodity price of the substance they deal in is falling. We are watching the oil price fall. How far it falls, at what velocity, and for how long – all are yet to be revealed. Transition in monetary policy coincides with continuing heightened geopolitical risk, whether with regard to Ukraine or ISIL or Asian hotspots. Keep an eye on the developing China-Russia rapprochement. Each sees a weakened America as an opening and therefore sees alignment with the other as an advantage. All this says volatility will rise. Risks and uncertainty premiums are rising. They all go together. At Cumberland Advisors, we are maintaining a cash reserve in our US ETF accounts. We also have some cash reserve in our momentum ETF strategy and our international ETF strategy. We may change this allocation at any time. Only the sector-rotation ETF strategy is fully invested. Why? Because it never uses cash and is always fully invested. We use all four strategies at Cumberland. They serve different purposes depending on the allocation mechanism and the preferences of the client. ~~~ David R. Kotok, Chairman and Chief Investment Officer |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment