The Big Picture |

- Slow Recovery in Wages and Salaries Continues despite Strong Jobs Growth

- Shareholder Value Maximization: The World’s Dumbest Idea?

- 10 Thursday PM Reads

- A Global Boom, but Only for Some

- Masters in Business: Ralph Acampora

- The One Chart That Explains Democrats’ Loss

- 10 Thursday AM Reads

- Fisher: It’s Very Dangerous to `Tamper’ With Fed

| Slow Recovery in Wages and Salaries Continues despite Strong Jobs Growth Posted: 07 Nov 2014 02:00 AM PST Slow Recovery in Wages and Salaries Continues despite Strong Jobs Growth

After enduring the worst recession since the Great Depression and seeing higher levels of unemployment than at any other point in their lifetime, Americans have been finding jobs at an increasing rate. However, the workplaces to which they are returning look very different from the ones that they participated in prior to the Great Recession. Most strikingly, many of the sectors that lost jobs before or during the recession are not those that are gaining jobs now. And wages and salaries tend to be growing slowest in the sectors gaining the most jobs and fastest in those gaining the fewest.

During the pre-recession period of 2002–2007, total nonfarm employment grew by 7.4 million workers. This growth was strongly concentrated in the private services-producing sector, and to a lesser extent in the government sector. During this period, these sectors grew by 7.5 million and 1 million workers, respectively. Conversely, the goods-producing sector, primarily composed of workers in mining and logging, construction, and manufacturing, saw their employment numbers decline by 1.1 million. Manufacturing alone lost 2.0 million jobs. (By way of historical comparison, the manufacturing sector as a percent of total private sector employment has declined from a high of approximately 37 percent immediately following World War II to approximately 10 percent today.)

Both before and after the Great Recession (2008:Q1 to 2009:Q2), service sectors have fared best. Specifically, jobs growth in professional and business services has almost reached 3 million in the recovery, eclipsing the sector's pre-recession growth of 2 million jobs over a comparable period (five years). Similarly, growth remains strong in the education and health services sector and the leisure and hospitality sector. Collectively, these three sectors have seen total job growth of 6.6 million in the recovery period, slightly surpassing the 6.3 million jobs gained in the pre-recession period. Conversely, due to the onset of fiscal restraint at all levels of government, the government sector has actually lost 665,000 jobs in the recovery, while it gained 1 million in the pre-recession period. Meanwhile, wage and salary growth evolved quite differently. During the pre-recession period, real wages and salaries, as measured in 2001 dollars, were growing at an average annual rate of approximately 0.9 percent across all sectors. The variation between sectors was fairly tight with wages in the goods-producing sector growing at a 1 percent rate while the service sector was growing at approximately a 0.9 percent rate. The government sector actually led in wage and salary growth during this period, with an average annual growth rate of approximately 1.2 percent. However, in the recovery, this relative symmetry in performance has eroded. The goods-producing sector, despite having the slowest rate of growth in employment levels, has seen an average of 1 percent growth in real wages and salaries. The fast-growing service sector has seen wage and salary growth fall to approximately half that rate. The trade, transportation, and utilities sector has fallen even further, to approximately 0.2 percent average annualized growth, and the government sector has also seen a decline in average annual wage and salary growth of approximately 0.3 percent.

It may seem counterintuitive that wages and salaries are growing the slowest in industries where jobs are growing the fastest, but it actually is not. It is primarily due to the wide variance in jobs in the service sector. Some service jobs, such as high-tech professionals, health service professionals, and engineers, have higher barriers to entry, including the need to acquire more training and credentials. Many others, such as some jobs in leisure and hospitality and wholesale and retail trade, have much lower barriers to entry than the high-skilled, high-tech positions that are being created in the skilled manufacturing and construction sectors. And because these high-skilled jobs continue to increase in demand, average wage and salary rates have risen faster than they have in the lower-skilled sectors. ~~~ LaVaughn M. Henry |Vice President and Senior Regional Officer for the Cincinnati Branch LaVaughn M. Henry is a vice president and the senior regional officer for the Federal Reserve Bank of Cleveland's Cincinnati Branch. Dr. Henry is responsible for building and maintaining a strong presence and reputation for the Bank throughout central and southern Ohio, and eastern Kentucky. He works closely with key stakeholders, including the board of directors of the Cincinnati Branch, business advisory councils, depository institutions, business and civic leaders, and the public. |

| Shareholder Value Maximization: The World’s Dumbest Idea? Posted: 06 Nov 2014 04:00 PM PST

|

| Posted: 06 Nov 2014 02:00 PM PST My afternoon train reads:

What are you reading?

|

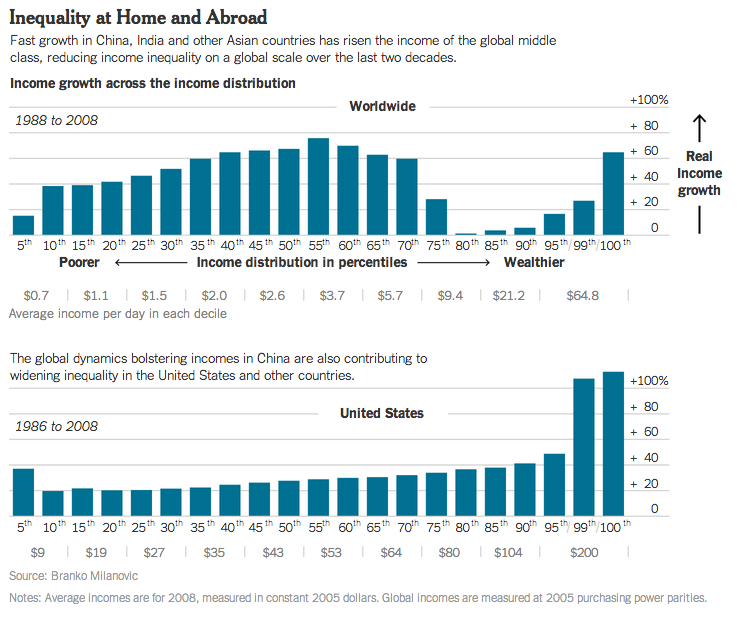

| A Global Boom, but Only for Some Posted: 06 Nov 2014 12:00 PM PST

|

| Masters in Business: Ralph Acampora Posted: 06 Nov 2014 08:30 AM PST In this week's "Masters in Business" podcast, I talk with Ralph Acampora, founder of the Market Technician’s Association. Acampora has been closely charting markets for almost a half-century. He tells how he was in the seminary, on the way to becoming a priest, when fate intervened. After a car accident, he went into the field of finance instead (much to his parents' disappointment). Today, he is high priest of charts, and has been called the “Godfather of Technical Analysis.” You can stream the podcast at SoundCloud or download it here or on iTunes. All of our prior podcasts are available for free download on iTunes. Next week, we speak with Mark Cuban, owner of Dallas Mavericks, co-founder of Broadcast.com and a regular on ABC’s Shark Tank.

|

| The One Chart That Explains Democrats’ Loss Posted: 06 Nov 2014 06:00 AM PST The elections are over. The pundits will spend the next few months dissecting the candidates and the campaigns. The Republican Party ran a strong campaign with attractive candidates, while the Democrats did neither. Voter turnout was low, which often gives an advantage to Republicans. Then there is the economy. The Democrats seem to have forgotten about that. We didn’t hear much about the slow but steady improvement during the past six years. President Barack Obama and the Democrats could have pointed to a number of economic accomplishments: Unemployment has declined to less than 6 percent; the economy grew at a 3.5 percent rate in the latest quarter; gasoline is less than $3 a gallon; the annual federal budget deficit has been cut in half. None of that got much airplay. There is an argument to be made that it wouldn’t have mattered much anyway. A reader sent in the following chart. It shows the ratio between income and liability for households. It is heading in the wrong way. The data show that median income relative to debt is falling. In other words, people are falling further behind.

|

| Posted: 06 Nov 2014 04:30 AM PST My morning train reads:

|

| Fisher: It’s Very Dangerous to `Tamper’ With Fed Posted: 06 Nov 2014 03:30 AM PST Federal Reserve Bank of Dallas President Richard Fisher talks about the central bank’s independence, monetary policy and economy. Fisher speaks with Michael McKee, Stephanie Ruhle and Matt Miller on Bloomberg Television's "Market Makers."

|

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

0 comments:

Post a Comment