The Big Picture |

- Who Are We Killing with Drones?

- Global Carbon Footprint

- Best of the Best of 2014

- Josh Brown: Investment Fads and Themes, 1996-2014

- 10 Tuesday Reads

- Oil, Europe, good and bad & Spain

| Who Are We Killing with Drones? Posted: 30 Dec 2014 10:30 PM PST West Uses Anti-Terror Laws to Murder Farmers, Small-Time Drug Dealers and Low-Level Taliban Members – Poppy Farmers, Drug Couriers and Drug DealersSpiegel reported yesterday that drug dealers and low-level Taliban members were targeted for death by drone:

We've previously noted that even the architect of America's drone assassination program says it's gone too far … creating terrorists rather than eliminating them. And that drone attacks are a war crime (more here and here). And that there is widespread murder of innocent civilians as "collateral damage". For example, American University Professor Jeff Bachman reports:

Indeed, even the process for deciding who to put on the "kill list" is flawed. People are often targeted by the metadata on their phones, a process which a former top NSA official called the drone assassination program "undisciplined slaughter." And people are targeted for insanely loose reasons. As the New York Times reported in 2012:

And then there are "double taps" … where the family members, friends or neighbors who try to rescue someone hit by a drone missile are themselves targeted for assassination. The bigger picture is that anti-terror laws are being used for all sorts of purposes besides stopping terrorists:

|

| Posted: 30 Dec 2014 04:30 PM PST |

| Posted: 30 Dec 2014 11:00 AM PST

|

| Josh Brown: Investment Fads and Themes, 1996-2014 Posted: 30 Dec 2014 07:00 AM PST

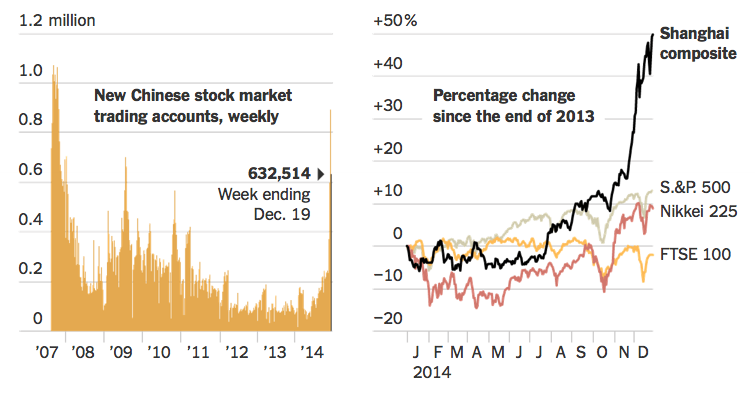

It begins with 1996 because that was my first summer working on The Street and my earliest exposure to the market. I do this every December because I agree with the eminent philosopher Bob Marley in that "If you know your history, then you would know where you're coming from." If we don't document and learn from the lunacy that grips us from year to year, how can we truly say that we've grown as investors? By documenting this stuff, it becomes a permanent part of my knowledge base, a reference to draw from in times to come as similar trends play out and the great wheel spins past an endless parade of fear and greed. So what was 2014 about? I would point to four major fads and themes that each captivated the investment community and had some overlapping influence on each other: DisinflationGeneral economic weakness in the European economy along with the continued China slowdown and a surprise mid-year technical recession in Japan helped drive prices and demand for commodities. This led to a push back of inflation expectations across the board and the resumption of yield-chasing among investors. Treasury yields hit astounding new lows – the exact opposite of what all of Wall Street's strategists predicted as the year started. Consumer discretionary stocks and consumer staples stocks were big beneficiaries, as were bond funds and utilities. USA!The US stock market – specifically the S&P 500 – outperformed almost every other investable asset class in the universe this year. Investors piled into US large cap stocks as this trend became more and more apparent. The S&P 500's year-to-date total return of 10.5 percent beat the Barclays Aggregate Bond index by 40 percent in 2014 and doubled the return of the Nikkei. In the meanwhile, MSCI EAFE (developed markets ex-US) was down 7.75 percent this year and the MSCI World Index has barely squeezed out a positive gain of less than 1 percent. Removing US stocks from the world index and its a loss of 7.65 percent for global stocks. AlibabaOne global market that did manage to perform well was a market that almost no one can participate in – the Shanghai Composite of mainland Chinese stocks. The Shanghai Comp rose 40 percent this year, outperforming Hong Kong, India and the rest of the Asian markets after having underperformed for years. This awakening was brought about through a combination of renewed Bank of China stimulus along with the China Stock Connect (or Through train) plan that linked Hong Kong's brokerage firms and markets with their mainland counterparts to allow for easier flow of funds back and forth. With foreign investors getting an expanded entrance to the Chinese bourses, the large discount between valuations narrowed a great deal. The bright spot for China bulls, however, took place on the New York Stock Exchange in September, as Alibaba listed it's shares in the largest US IPO in history. Jack Ma led his company's coming-out party on The Street and virtually every major hedge fund jumped in to play the theme. King DollarIn some way, the incredible strength of the US dollar figured into virtually all of the popular investment themes in the market this year. The dollar rose some 12% versus the yen this year and appreciated all year against the basket. It was on everyone's lips, skewed the returns of investors in foreign asset classes and informed a great deal about how we went about allocating assets. *** So those were the big stories of the year that investors and traders bought into. Below is my updated guide to the Investing Fads and Themes by Year, 1996 – 2014. Enjoy!

See previous years below! |

| Posted: 30 Dec 2014 04:30 AM PST My morning pre-holiday reads:

What are you reading?

Seeking to Ride on China's Stock Market Highs

Source: Dealbook

|

| Oil, Europe, good and bad & Spain Posted: 30 Dec 2014 03:30 AM PST Oil, Europe, good and bad & Spain

Less than two months ago, Oxford Economics modeled sensitivity to the oil price by conducting simulations on 47 countries. Their baseline then was an "$84 Brent crude price average in 2015… gradually recovering to $106 in 2019." Their updated work has tested further simulations with $70, $60, $50, and $40 per barrel oil against that baseline. In Europe, they projected "negative inflation," which is not exactly the same as "deflation," in the Eurozone. In this instance, however, negative inflation might just as well be deflation, since we are talking about declines in price levels or changes in direction of prices such that they have a downward bias. Of course, the simulations require that the decline in the oil price persist, in order for behavioral changes to occur in these economies. The simulations attempt to measure the imbalances among countries and how these grow wider (with conditions worsening for some and improving for others) as the oil price sustains a lower level. Impacts on bond yields are projected for these diverse scenarios. The takeaway is how remarkable the disparities among countries become as the oil price falls. For those with falling yields, the levels are extraordinary. For those with rising yields due to credit issues, the mirror image is true. In Asia, the Philippines is potentially one of the largest beneficiaries of low oil prices. So is Japan. Both are in Cumberland's international portfolios. Russia, Venezuela and others of similar ilk, as expected, are severely penalized. Cumberland does not own them. Spain is a big beneficiary in Europe. Out of the 45 countries Oxford considered, at the baseline oil price ($84), Spain is the only country to have negative inflation in 2015. As the price falls, more and more countries make this list. At $40 per barrel, 21 countries (47%) make the list. The leaders are all in Europe and mostly in the Eurozone. In order of impact as measured by negative inflation, they are Spain, Bulgaria, Italy, Poland, Portugal, Sweden, and Switzerland (which is now pegging its currency to the euro). At $60 per barrel for Brent, a majority of the Eurozone countries make the list. At $50 the entirety of the Eurozone does. Remember that "negative inflation" from an external shock acts as a rise in real income for Europeans. Simply put, low oil prices mean no inflation in the Eurozone, and there is nothing the European Central Bank can do to change that outcome. It also means that the potential for massive quantitative easing by the central bank is growing daily. We expect the ECB to announce large programs and to fulfill their goal of taking their balance sheet above 3 trillion euros. They will find a way to do it by linking the sovereign debt of each country to the creditworthiness of that country so that a combination package pairs debt and credit enhancement. The pairing can be used as collateral in a QE structure. Mario Draghi is about to deliver on his "whatever it takes" promise. We expect this development very soon. Meanwhile, the composition of the ECB Governing Council is about to change. It will become harder and harder for Germany to block a QE program. Cumberland's international ETF portfolios favor the use of currency-hedged exposures and include Europe. We do not expect growth to become robust. Euro-sclerosis is still rampant. But conditions will improve over the present recession levels, and the stock markets in Europe are likely to reflect that improvement as the QE unfolds. Michael McNiven, Bill Witherell, and Matt McAleer coordinate the analysis of international economics at Cumberland and incorporate some momentum work to assist in the selection of markets and ETFs. Mike acts as the portfolio manager; Bill does the economic modeling; and Matt's expertise is with the momentum work. My job is to stir up trouble. DonnaMarie Valles and Maribel Echevarria complete the team, so six pairs of eyes are on the actual trades. Let me say a word about Spain. First, Cumberland is overweight (120%) against its benchmark. Spain is a small weight, so we can go that high. We use a currency-hedged ETF structure to get to that position. Bill likes the outlook for Spain in economic terms, and Matt supports the decision with his momentum analysis. A few weeks ago (on December 16), we reproduced an email from a reader in Spain. He was harshly critical of the government and the intrusion that he saw into the Spanish economy. He wrote:

We thank our good friend (who remains anonymous by request) for making the opposing case. Now back to a bottom line: 2015 is shaping up to be a challenging year for investors and their advisors. We expect higher volatilities in many markets, surprises from unanticipated corners, and a lot of monetary stimulus in Europe. At the same time, the US will lead the world, and our growth rate now looks likely to be closer to 3.5% for the year. Cheaper oil is a wonderful thing for the winners. The gap between them and the losers will certainly widen. ~~~ David R. Kotok, Chairman and Chief Investment Officer

|

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

0 comments:

Post a Comment