The Big Picture |

- Commercial Real Estate and Low Interest Rates

- Business is Booming in Texas: Discuss

- 10 Tuesday PM Reads

- Flows say: Still No Confidence in Equities

- Case Shiller: Home Prices Rise in February 2013

- 10 Tuesday AM Reads

- TBTF: Terminating Bailouts for Taxpayer Fairness Act

- Jeffrey Sachs’ Speech on Wall Street Corruption

- Now What?

| Commercial Real Estate and Low Interest Rates Posted: 01 May 2013 02:00 AM PDT |

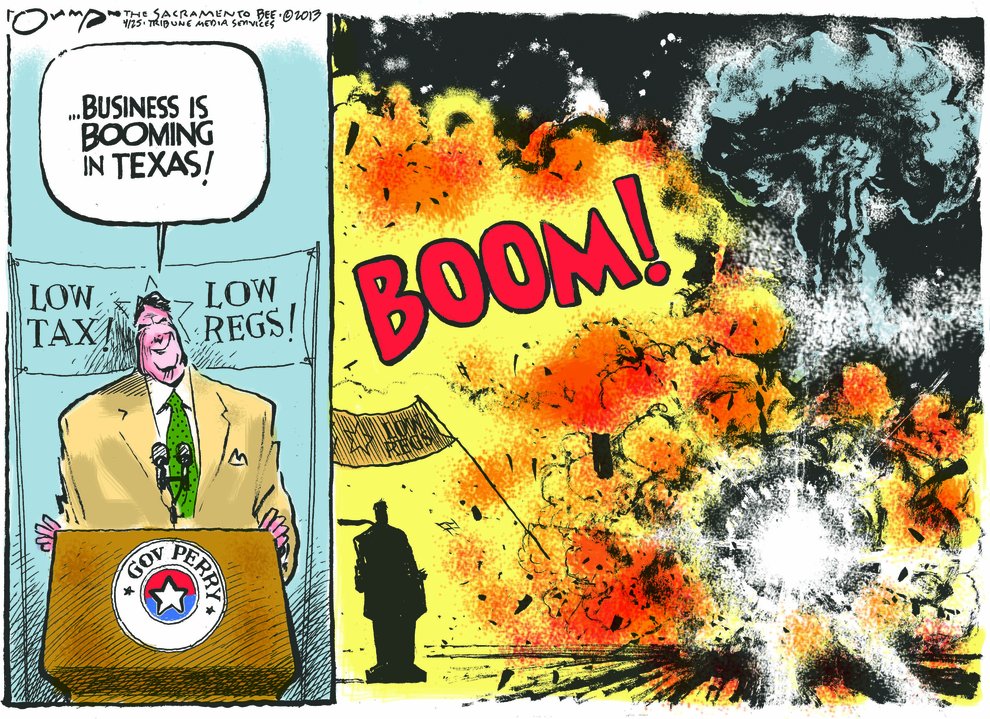

| Business is Booming in Texas: Discuss Posted: 30 Apr 2013 04:30 PM PDT

Interesting war of words between Texas governor Rick Perry and SacBee's cartoonist Jack Ohman. Perry is demanding the cartonist be fired for his insensitivity to the deaths at the fertilizer plant. Ohman responded: “When you have a politician traveling across the country selling a state with low regulatory capacity, that politician also has to be accountable for what happens when that lack of regulation proves to be fatal.”

Source: SacBee's Jack Ohman won't apologize for Texas explosion cartoon (Poynter) |

| Posted: 30 Apr 2013 01:00 PM PDT My afternoon train reading:

What are you reading?

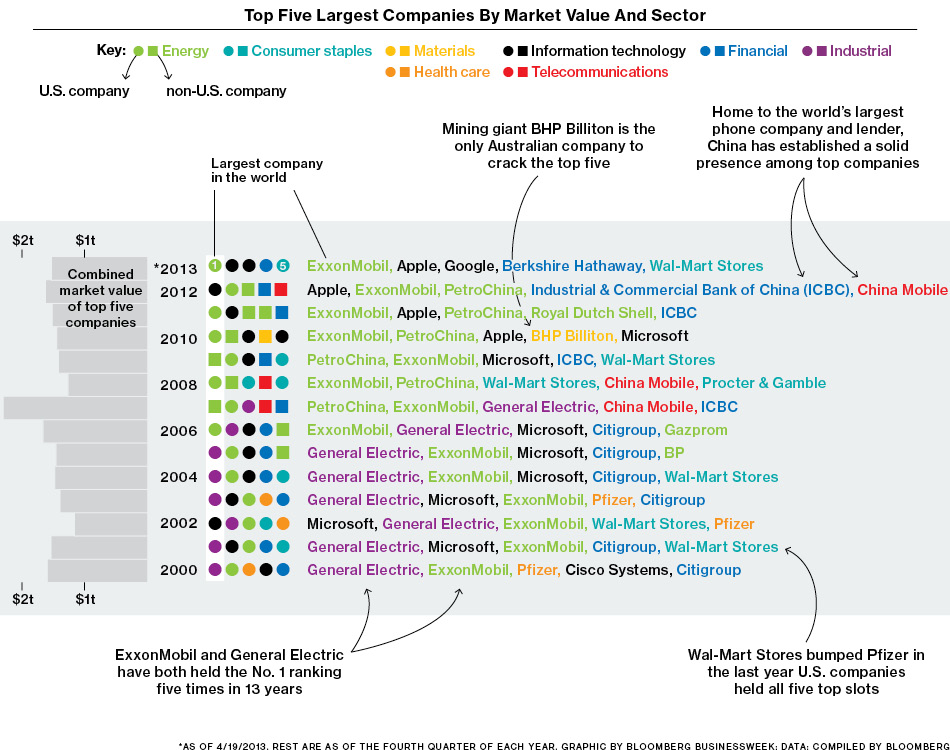

U.S. Companies Are Back on Top |

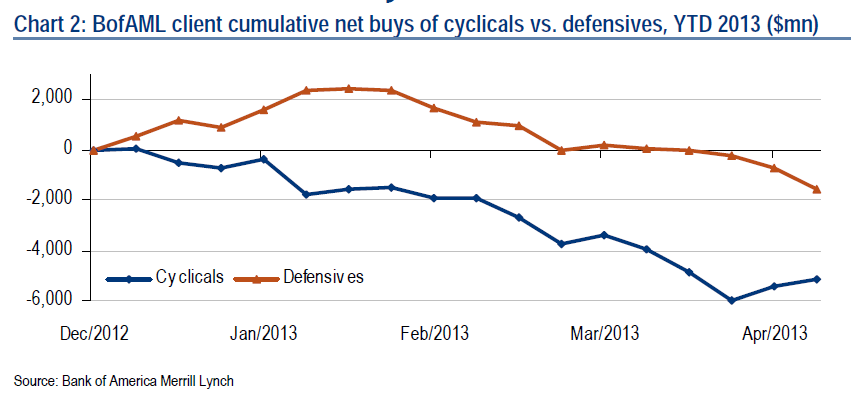

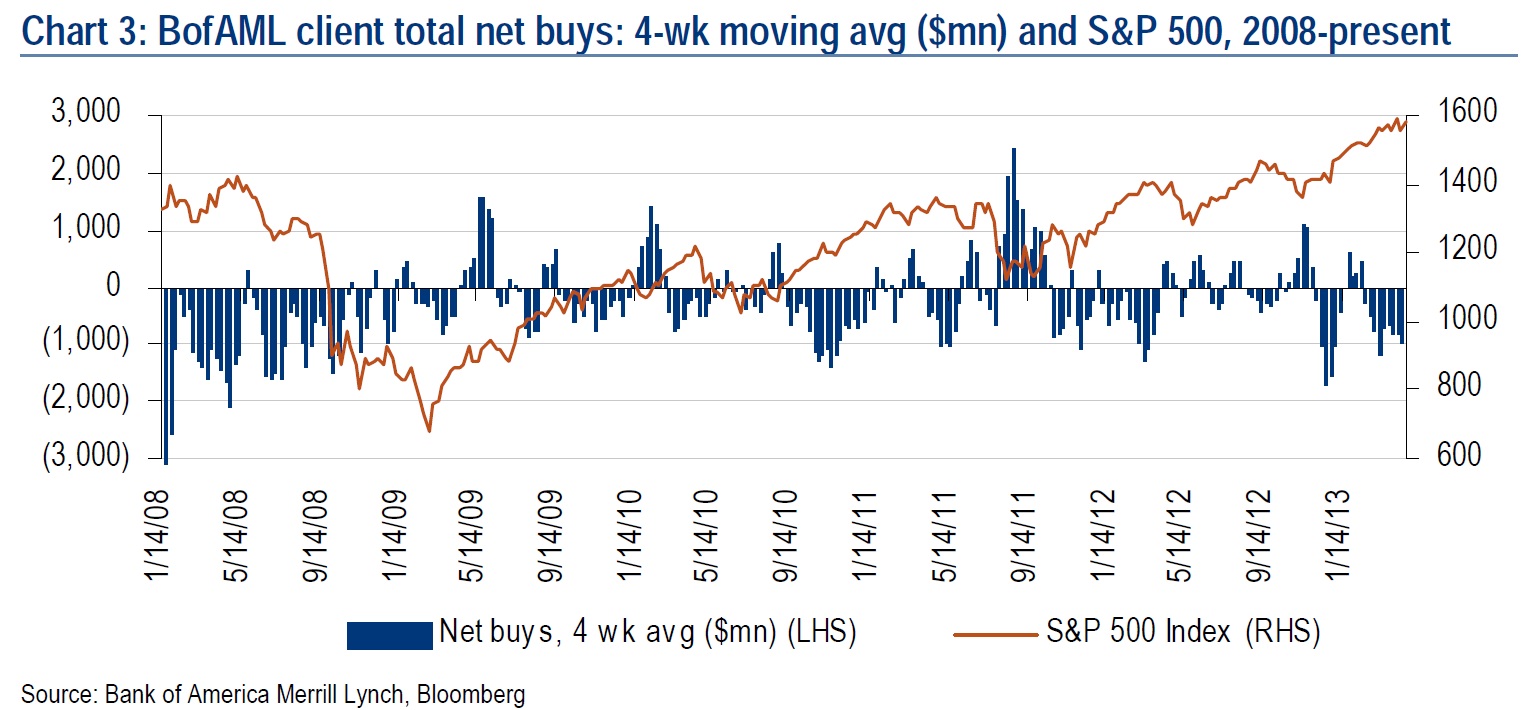

| Flows say: Still No Confidence in Equities Posted: 30 Apr 2013 09:30 AM PDT Cyclicals vs. Defensives

There are many different ways to measure investor confidence and market sentiment.BoA Merrill Lynch looks at their client flows relative to the market. Some of this is instructive: On the one hand, private clients were net sellers in four of the last five weeks. However, as the chart shows above, there is a possible rotation starting away from Defensives and towards Cyclicals. That move might suggest that sentiment is improving. One caveat: It is easy to cherry pick what you want when it comes to investor sentiment. This has a bullish color to it, but there are lots of other bearish readings as well.

BofA Merrill Lynch’s Equity Client Flow Trends: Cyclicals vs. Defensives

Source: |

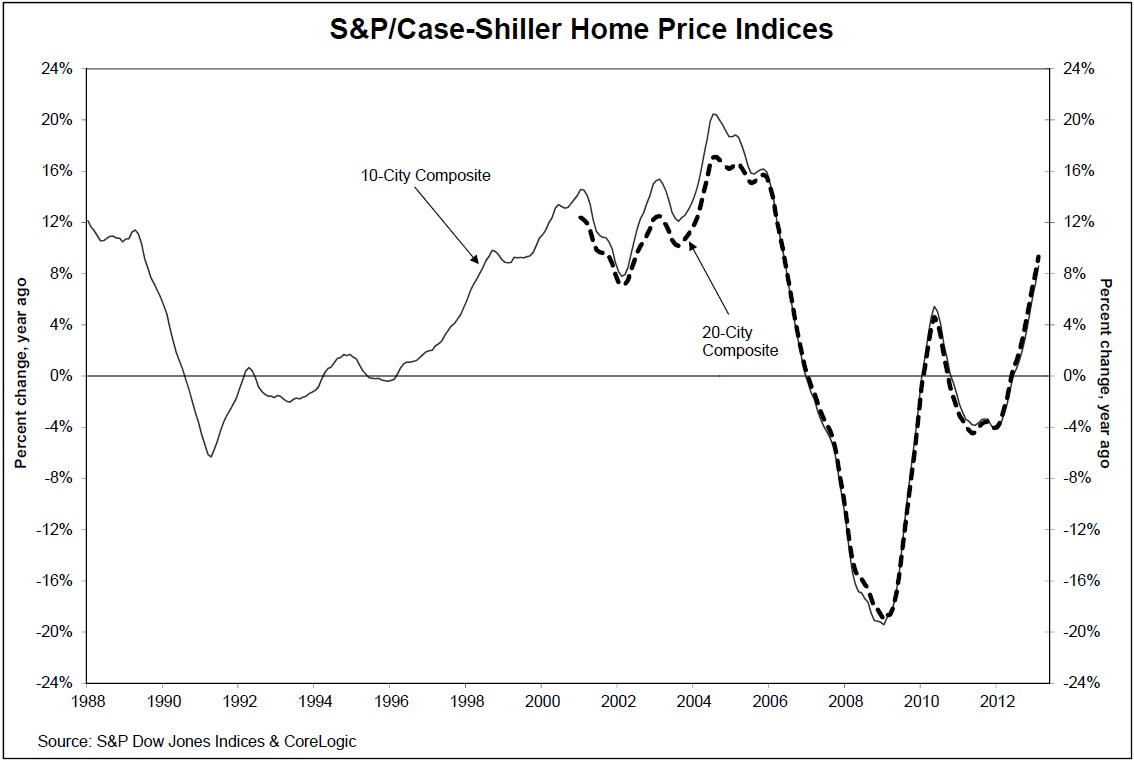

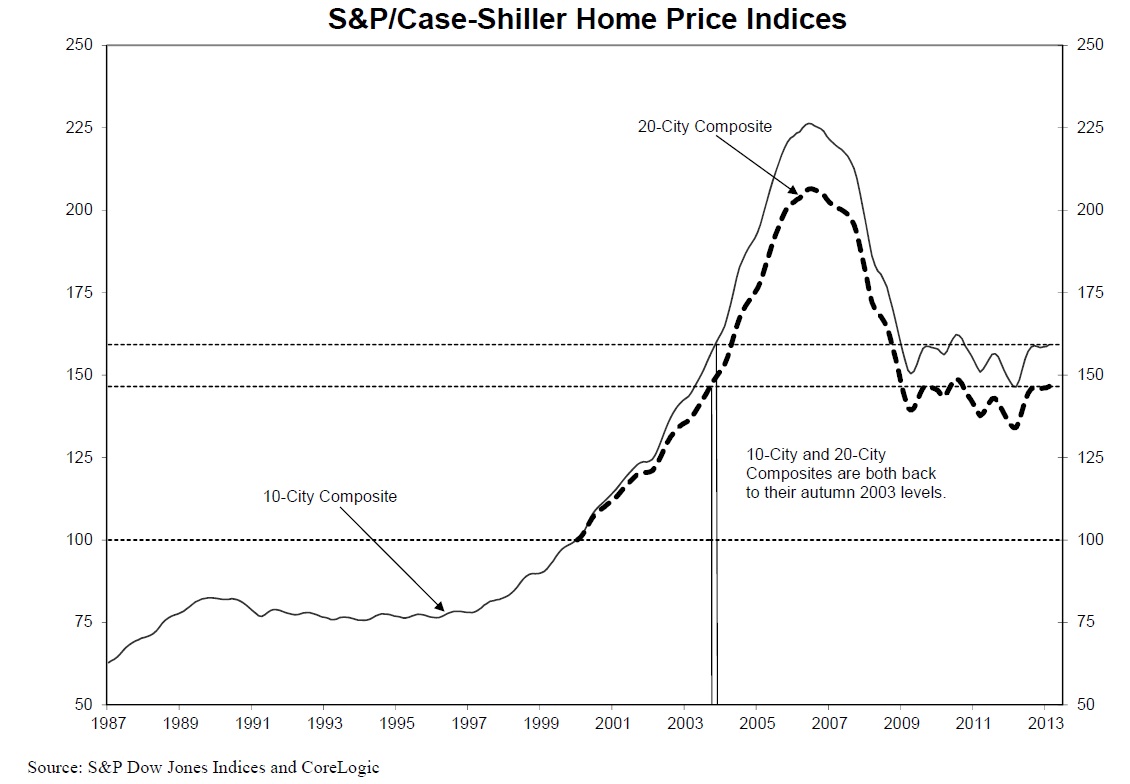

| Case Shiller: Home Prices Rise in February 2013 Posted: 30 Apr 2013 08:00 AM PDT Data through February 2013 showed average home prices increased 8.6% and 9.3% for the 10- and 20-City Composites in the 12 months ending in February 2013. For data junkies, you can access more than 26 years of history for these series in full by going to

S&P/Case-Shiller Home Price Indices

|

| Posted: 30 Apr 2013 07:00 AM PDT My morning reads:

What are you reading?

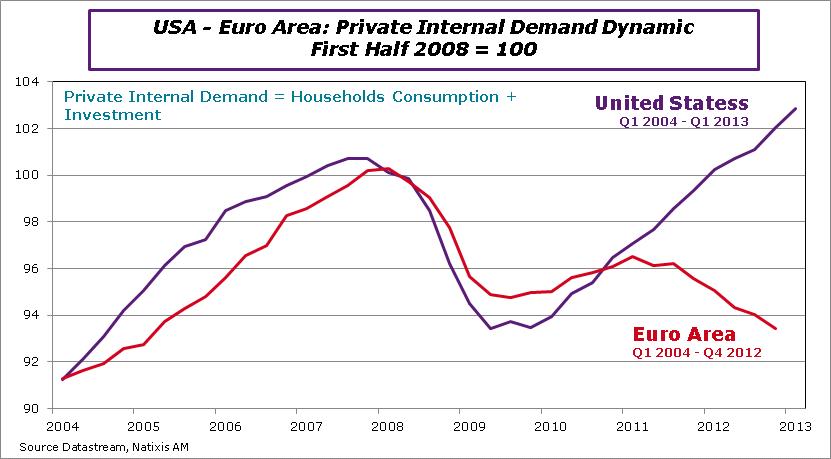

United States versus Euro Area: A Chart that shows the Difference |

| TBTF: Terminating Bailouts for Taxpayer Fairness Act Posted: 30 Apr 2013 05:30 AM PDT

This weekend, we saw a flurry of reporting on a new bi-partisan proposal introduced by Senators Sherrod Brown, an Ohio Democrat, and David Vitter, a Louisiana Republican. This is a very simple, straight forward piece of legislation that mandates adequate capital reserves, eliminates the opportunity for bankers to hide liabilities off balance sheet or game the various asset classes:

For those people who complain Dodd-Frank is too complex, let’s see how they like “the new simplicity.” Brown-Vitter faces two large, deeply intertwined opponents: Wall Street banks and the Obama administration. The pushback has already begun. For the banker’s views, we go to the NYT’s Dealbook. It is overseen by Andrew Ross Sorkin, author of Too Big to Fail and now a CNBC morning anchor. As seen in its recent headline, The Seductive Simplicity of a New Banking Bill, Dealbook is a touch skeptical of the legislation, but notes “in a major way, the Brown-Vitter bill effectively sidesteps the need for reliable regulators. It simply says that all big banks would have to set up a buffer for potential losses – called capital in the industry – that is equivalent to 15 percent of their total assets.” Simon Johnson takes a different tack. He warns that there are two competing narratives about financial-reform efforts, with the financial-sector executives claiming that “all necessary reforms have already been adopted.” Johnson pushes back on this, noting “the world's largest banks remain too big to manage and have strong incentives to engage in precisely the kind of excessive risk-taking that can bring down economies. Last year's "London Whale" trading losses at JPMorgan Chase are a case in point.” The best read of the proposal comes from FDIC Vice-chairman Thomas Hoenig — he is in favor the legislation. Hoenig is the single best reason you know the TBTF act is the a good step in the proper direction for bank regulation.

Sources: Sherrod Brown Takes On Megabanks — And The Obama Administration Trying to Slam the Bailout Door The Seductive Simplicity of a New Banking Bill |

| Jeffrey Sachs’ Speech on Wall Street Corruption Posted: 30 Apr 2013 03:45 AM PDT Columbia Economist Dr. Jeffrey Sachs speaks candidly about corruption in the United States: from Washington DC and Wall Street, including the entire financial/banking system |

| Posted: 30 Apr 2013 03:00 AM PDT Now What?

Last week, the public was enraged by the needless disruption in air traffic. People created websites, made calls and sent email to Congress and the White House, and launched an attack on Democrats and Republicans alike. In one week, the wrath of the American citizenry created a necessary and successful change in policy. It demonstrated that angry American voters can coalesce around an issue when their anger reaches the boiling point and they set aside partisan politics. They said to their elected representatives, “You, Senator and Congressman [not "Democrat" or "Republican"] are responsible for poor governance.” It took a week of pain. It cost the US economy billions of dollars. It cost operating businesses time and money and discouraged them from investing and hiring – and this particular disruption only lasted a week. Now, imagine the ongoing effects of sequestration on the rest of the federal government. Keeping in mind the Federal Aviation Administration (FAA) experience, let’s speculate a little about other potential trouble going forward – particularly the sort of trouble that could be made worse by the federal government’s failure to allow departments to prioritize, as we saw last week. Will the next crisis take the form of a public-health disaster? Are we going to see a lack of sufficient preparation in case H7N9 bird flu mutates and emerges as a pandemic? We have a rapidly mutating and very troubling flu virus spreading in the world. There are over 100 confirmed human cases. One out of every five cases has resulted in death, and almost all other reported cases have been hospitalized, with most remaining seriously ill. Only a handful have walked out of the hospital fully cured. Are we now missing information about this risk because of sequestration? Or will the next crisis happen due to inadequate care for the poor and elderly? Will it instead result from inadequate flood control on our rivers or perhaps from cutbacks to the National Oceanic and Atmospheric Association's (NOAA) national weather forecasting services? Will the next big failure occur because the Food and Drug Administration (FDA) can no longer adequately oversee the safety of our food, or will it be a deadly disaster that could have been prevented had there not been a falloff in bridge and rail-safety inspections? Or is there another major issue that will emerge, take center stage, and then trigger rage once more because we citizens will not be content with the quality of our governance? If so, then we will again light up the White House switchboard; email Senators and Congressman, call them on the phone, and send them telegrams; and launch another round of hot-issue websites. In place of "Don't Ground America,” the website might be "Don't Sicken America" or "Don't Starve America" or "Protect America" or "Make America Safe and Secure Against Terrorist Attacks" – or something else. From where we sit, a milestone has been reached in the US: citizen anger rose to the point of reaction. Americans are very slow to anger. We tolerate awful governance in Washington. We go on about our business and act as though we cannot do anything about the problem. Over half of us give up and don't vote. But once angered, the citizens of the US have the capacity to take their country back. And we did it last week. Now we have to do it again, or we’ll soon lapse back to divisive partisan politics, finger pointing by Democrats at Republicans and by Republicans at Democrats, finger pointing by the White House at the Congress and by Congress at the White House. America, if the finger pointing continues, I hope we will inflict more wrath on our Senators and Congressmen, both Democrats and Republicans – the men and women who we elected to represent us in Washington. Meanwhile, markets are facing a slowdown in 2Q2013. Worldwide, statistics are trending in favor of a slowdown. Incomes are rising, but very slowly. The corporate-profit share is very wide, but it may have peaked. The labor-income share, on the other hand, is very low, and it may be bottoming. Each shock delivered by Washington sets back the process of recovery, whittles the growth rate and jobs, and extends the period in which interest rates will remain near zero according to the central banks of the developed world. This trend is bullish for stocks and other asset classes. Low interest rates, very low growth, and no inflation pressure create rising prices for assets of all types. In the longer run, this is a terribly unhealthy circumstance, and our longer-term outlook deteriorates progressively as our Washington politicians continue their disjointed puppets' dance. From a strategic point of view, we remain fully invested. We are back and fully invested in the US stock market and have been participating in the rally. There was a temporary respite during which we raised some cash that has now been redeployed. On the bond side, we expect interest rates to remain low for an extended period. We are gradually transitioning accounts in preparation for rising interest rates, although we do not expect to see them this year and perhaps not for another 2-4 years. The timing of the interest-rate shift makes future strategic moves is impossible to determine. We continue to gradually phase in hedged accounts in order to protect against long-term interest-rate risk. We watch and worry about Washington. And we worry about our country. ~~~ David R. Kotok, Chairman and Chief Investment Officer, Cumberland Advisors |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment