The Big Picture |

- Negative Interest Rates

- Discuss: Why is the USA: the only rich country with growing population % who can’t afford food

- 10 Thursday PM Reads

- Agricultural and Farm Update

- The Federator

- Three Measures of Central Banks’ Effectiveness

- 10 Thursday AM Reads

- Bloomberg Appearance (May 29, 2013)

- What Do You Control?

- Don’t Be This Trader

- The Effects of Unconventional and Conventional U.S. Monetary Policy on the Dollar

| Posted: 31 May 2013 02:00 AM PDT Negative Interest Rates

There seems to be a debate at the European Central Bank (ECB). The issue is whether or not the ECB should impose a negative interest rate. I listened to the interview of Christian Noyer, Governor of the Banque de France. His personal inclination is to oppose the use of a negative interest rate as a policy mechanism. He cited other cases to support his view. ECB President Mario Draghi mentioned the possibility of using a negative interest rate. That triggered the discussion. Negative interest rates are the ultimate in market distortions. They employ only a stick and no carrot. Their use tends to progress from disincentive through penalty to punishment. There is only a limited history of the use of negative interest rates. Many decades ago, Switzerland discouraged incoming Swiss-franc deposits by imposing a negative interest rate on balances placed with Swiss banks. In other words, a person deposited money in the bank, and the bank charged the depositor for the privilege of keeping it there. During the financial crisis in the US, the Bank of New York imposed a negative interest rate – a penalty – on deposits over $50 million. The bank essentially told customers to remove their money. Sweden's central bank, the Sveriges Riksbank, also attempted a negative interest rate during the financial crisis but quickly reversed its policy. I had the opportunity to discuss the Swedish experience with the governor of the central bank at the Global Interdependence Center (GIC) meeting in Helsinki. Governor Stefan Ingves was quick to point out that benefits from negative interest rates did not seem to be observable. He did not get into the costs associated with negative interest rates, but he did affirm that it was unlikely that Sweden would use them again. In the US there is a question as to whether the existing, very low but still positive interest rates are too low. We have a Federal Deposit Insurance Corporation (FDIC) fee in the US. It is assessed on assets of US-based banks. The FDIC fee is a formulaic approach that includes excess reserve deposits at the Federal Reserve (Fed), on which the Fed pays an interest rate of 25 basis points, or 0.25 percent. The differential between the excess reserve positive rate and the federal funds rate reflects a market that is attempting to find a clearing price of overnight liquidity transacted among and between banks. The federal funds rate is set below the excess reserve rate by market forces. A second distortion occurs in the US because Fannie Mae, Freddie Mac, and other Government-Sponsored Enterprises (GSEs) do not participate directly with reserve deposits at the Fed. Fannie Mae is not a bank; it has to sell its excess cash in the federal funds market at whatever interest rate it can obtain. That is how it earns something other than zero on its large excess cash flows. The buyers of Fannie Mae federal funds recycle the funds to the Fed as an excess reserve deposit. Buyers make an arbitrage profit less the cost that they incur in payments of the FDIC fee. The whole process in the US is even further distorted by the fact that US subsidiaries of foreign-owned banks are not subjected to the FDIC fee and operate with a different formula than US banks. The principle behind that rule is that the capital determinants of foreign banks are set by a different regime than for US banks. This distortion at the short end of the yield curve in these very-low-interest-rate times exacerbates difficulties in the formulation and implementation of monetary policy. In the midst of all this turbulence we now have a European brouhaha going on over negative interest rates. Our conclusion is that the likelihood of a negative interest rate being imposed by the ECB is near zero. It is not going to happen. Cooler heads will prevail at the ECB. At least we believe so. However, Europe has other serious issues with its banking system. It has not resolved the Eurozone-wide mechanism to secure insured deposits. It attempted to penalize insured depositors in the Cyprus affair and narrowly averted a disaster. It penalized uninsured depositors and is developing a system by which uninsured depositors will have a single standing and at least know the stratification of their claims on banks. That process has not yet been resolved. In the ECB and the Eurozone, we see a wounded banking system that is only slowly discussing the mechanisms of repair. Negative interest rates should not be one of them. In the US, we see distorted pricing and its impacts on our markets. These impacts are not fully understood by the general public. The public and most depositors are taking all deposits in the US for granted. They believe they are safe. However, the US is moving toward a bail-in rather than a bailout regime. The US and the FDIC in particular have affirmed that fact in documents that are diplomatically written but transparent to those who have eyes to see. At Cumberland, we are overweight banks. We believe that the supportive impacts of the Fed’s bailout regime are still affecting US banks. We do not see a banking crisis in front of us in the near term, due to the huge excess liquidity provided by the Fed. It is hard to imagine how a banking crisis might occur when there is almost $2 trillion in excess reserves in the US banking system and over $5 trillion in excess banking reserves worldwide. We worry about the long term. The ranking order for depositor safety and the claims of bondholders, shareholders, and banks is a subject undergoing transition worldwide. Different jurisdictions are approaching this in different ways, and there is no global resolution yet. At this point we remain overweight in US financials, including big banks, regional banks, and insurance companies. We watch the developments and are seeing the markets improve. We worry, however, about the longer term. ~~~~ |

| Discuss: Why is the USA: the only rich country with growing population % who can’t afford food Posted: 30 May 2013 04:30 PM PDT |

| Posted: 30 May 2013 01:30 PM PDT My afternoon train reading:

What are you reading?

Bullish Sentiment Drops Back Below Average |

| Posted: 30 May 2013 12:00 PM PDT Summary: As the season progresses, we see corn production estimates declining, and corn prices declining. Indeed, the early information suggests yields will be less than government forecasts, and that the USDA estimates will decline starting in June. Higher corn prices and increased worries about yields should drive accelerating sales of fertilizers, pesticides and higher yielding seeds.

|

| Posted: 30 May 2013 10:00 AM PDT By now, you probably have seen this little project from the WSJ — but on the off chance you haven’t, have some fun!

click to play

Hat tip Panzner! |

| Three Measures of Central Banks’ Effectiveness Posted: 30 May 2013 08:30 AM PDT |

| Posted: 30 May 2013 06:45 AM PDT My morning reads:

What are you reading?

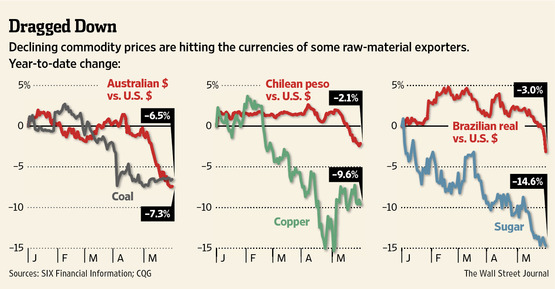

Currencies Tumble as Investors Bet on Sustained Price Declines for Materials |

| Bloomberg Appearance (May 29, 2013) Posted: 30 May 2013 06:00 AM PDT Boy Genius Report’s Jonathan Geller, Fusion IQ’s Barry Ritholtz and Bloomberg’s Jon Erlichman discuss future Apple products and outlook for the company with Trish Regan on Bloomberg Television’s “Street Smart.” Apple’s Next Product: Is It Too Little Too Late? ~~~ Fusion IQ CEO and Director of Research Barry Ritholtz discusses Federal Reserve monetary policy with Trish Regan on Bloomberg Television’s” Street Smart.’ Bernanke’s Hands Are Tied on QE: Ritholtz ~~~ Moody's Investors Service downgraded the senior unsecured debt ratings of Alcoa. Fusion IQ CEO and Director of Research Barry Ritholtz speaks with Trish Regan on Bloomberg Television’s “Street Smart.” Alcoa Senior Debt Rating Cut to Junk by Moody's |

| Posted: 30 May 2013 04:24 AM PDT During this past month, we have seen significant moves up and down. Volatility has risen; there have been some scary drops in Asia, and some follow through selling (more or less) in the US. We have seen small measures of over-reaction, along the lines of “What do I do? What should I do? Should I do nothing, something, anything?” This is, IMHO, the wrong approach. During periods of market volatility and stress, I like to step back and consider (no pun intended) the big picture. I find it is helpful to understand what is within — and out of — my control. Indeed, one of the most important things I have learned in my careers as a trader/strategist/investor was recognizing what is in my control and what is not in my control. My experience has been that when I focus on what is in my control and learn to roll with what it is out of my control, every thing else vastly improves. Consider the following two lists of dozen items — these are what is in and out of your control:

What I write, say, and do are all obviously under my control as well. The other list:

The conclusion is both obvious and simple: Focus on what you can control; do not stress over what you cannot control. Investors and traders should endeavor to stay off of the emotional roller coaster, develop an intelligent long term plan, and then execute on that plan.

Previously: ~~~

Update, May 30 2013 7:14pm Carl sends this scribble along:

Source: Carl Richards, BehaviorGap.com

|

| Posted: 30 May 2013 04:00 AM PDT Via Trader Habits, here’s another graphic to add to our massive collection of Sentiment Cycles (here, here and here):

Don’t Be This Trader

|

| The Effects of Unconventional and Conventional U.S. Monetary Policy on the Dollar Posted: 30 May 2013 03:00 AM PDT |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

3 comments:

Does your website have a contact page?

I'm having problems locating it but, I'd

like to send you an email. I've got some recommendations for your blog you might be interested in hearing. Either way, great website and I look forward to seeing it develop over time.

Here is my site :: CrossFit rubber mats

Wow, this paragraph is nice, my

younger sister is analyzing these kinds of things, so I am going to let

know her.

Feel free to visit my page: blackpeoplemeet scams

Wonderful post! We will be linking to this

great article on our site. Keep up the great writing.

Here is my web blog :: Garage Rubber Floor Tiles

Post a Comment