The Big Picture |

- What Happens During 1 Second of HFT?

- 10 Monday PM Reads

- State of the US Labor Market (in one big chart)

- 10 Monday AM Reads

- Blame Politicos, Not Reinhart & Rogoff

- Warren Buffett Explains ‘Colorful Charlie’

- Federal Deficit and Markets

| What Happens During 1 Second of HFT? Posted: 07 May 2013 02:00 AM PDT 1/2 second of trading activity in Johnson & Johnson (symbol JNJ) on May 2, 2013

The bottom box (SIP) shows the National Best Bid and Offer. Watch how much it changes in the blink of an eye. Watch High Frequency Traders (HFT) at the millisecond level jam thousands of quotes in the stock of Johnson and Johnson (JNJ) through our financial networks on May 2, 2013. Video shows 1/2 second of time. If any of the connections are not running perfectly, High Frequency Traders can profit from the price discrepancies that result. There is no economic justification for this abusive behavior. Each box represents one exchange. The SIP (CQS in this case) is the box at 6 o’clock. It shows the National Best Bid/Offer. Watch how much it changes in a fraction of a second. The shapes represent quote changes which are the result of a change to the top of the book at each exchange. The time at the bottom of the screen is Eastern Time HH:MM:SS:mmm (mmm = millisecond). We slow time down so you can see what goes on at the millisecond level. A millisecond (ms) is 1/1000th of a second. Note how every exchange must process every quote from the others — for proper trade through price protection. This complex web of technology must run flawlessly every millisecond of the trading day, or arbitrage (HFT profit) opportunities will appear. It is easy for HFTs to cause delays in one or more of the connections between each exchange. http://www.nanex.net/Research/IsNBBOI… Category |

| Posted: 06 May 2013 01:15 PM PDT My afternoon train reads:

What are you reading? |

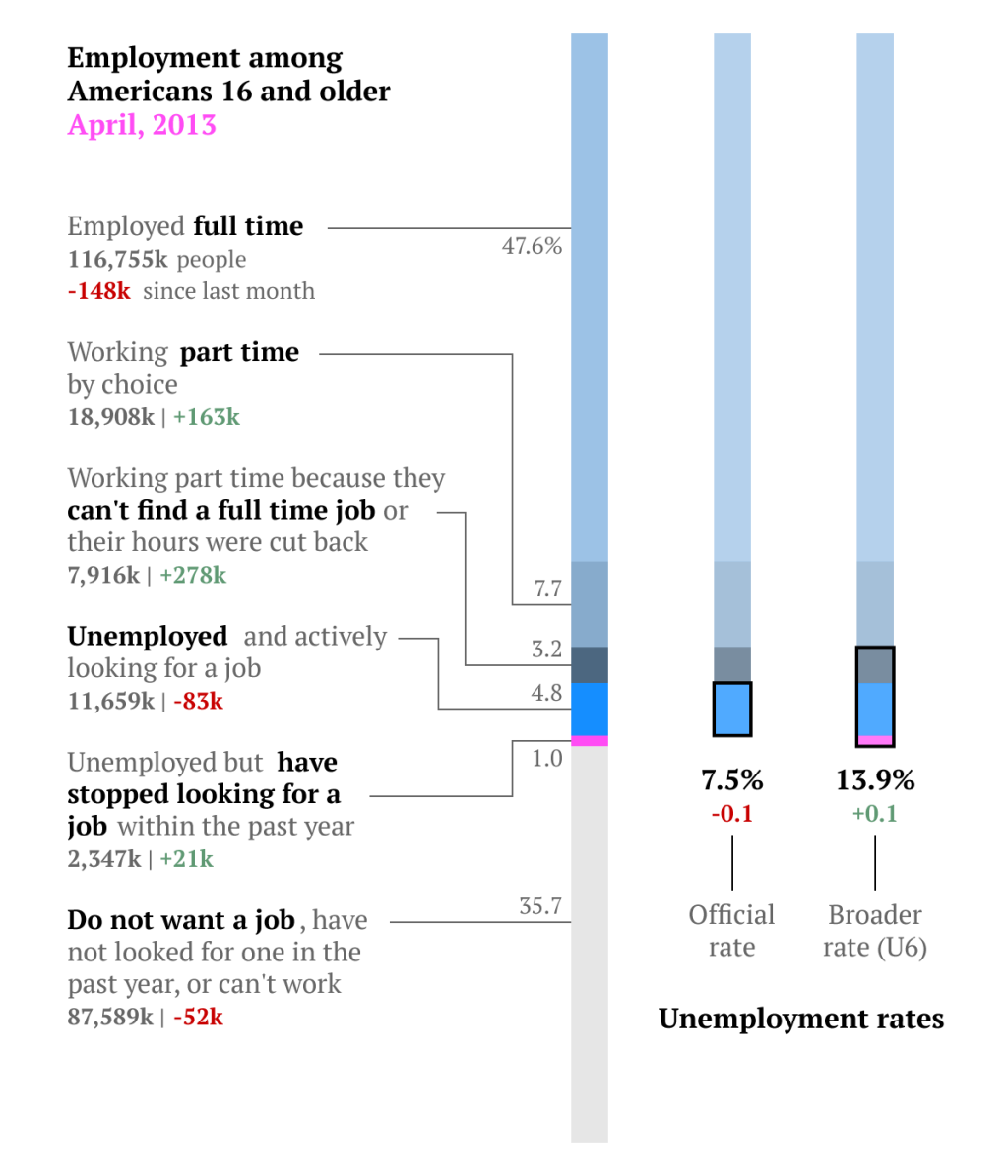

| State of the US Labor Market (in one big chart) Posted: 06 May 2013 08:30 AM PDT

click for ginormous chart

Fascinating way to look at the breakdown of various parties in the US labor market, via Ritchie King of Quartz. It shows U3 and U6 — the complete breakdown of employment status for all Americans age 16 and above, including: Full time workers, part time (by choice, and Involuntary) Unemployed (both looking and stopped looking), and Not in Labor Force.

Previously:

|

| Posted: 06 May 2013 07:00 AM PDT My Monday morning reading to start the week:

What are you reading?

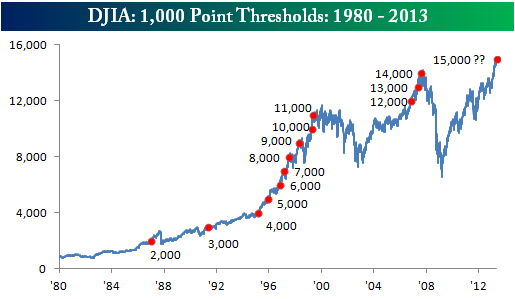

DJIA 1,000-Point Thresholds • Chasing Negative Performance (BlackRock) |

| Blame Politicos, Not Reinhart & Rogoff Posted: 06 May 2013 04:15 AM PDT

Reinhart and Rogoff are being blamed for the damaging, widespread adaption of post-crisis austerity programs in Europe and in the United States. This reflects a fundamental misunderstanding of how political decision get made. Regardless of what you think of either R&R, austerity or its opposite, stimulus spending, this blame on two academics is not based on how most Humans make decisions. After years of studying investor behavior, I believe this newly discovered conclusion is actually inverted — it is opposite to how people make their decisions — especially ideological driven politicians. Academia presents a buffet of theoretical options. Amongst the intellectual cognoscenti — those academics who toil in the world of abstract thought — this is a normal part of their process. We have an academic equivalent of millions of typing monkeys trying to produce Shakespeare — only most of the output is peer reviewed and challenged by other experts. This should inexorably lead us towards a basic form of Truth regarding specific aspects of society. Indeed, this is how soft sciences like Sociology, Political Science and Economics eventually develop and refine their understanding of how human society functions. When policy makers and politicians get involved, we run into trouble. They have no interest in pursuing the “Truth” — rather, they look for rationales for what they have decided they want to do regardless. It is confirmation bias writ large. They seek out that which agrees with their preconceived notions, and adapt it as a rationale for what they already believe in. Did Reinhart and Rogoff persuade many politicians to forgo stimulus and embrace austerity? I am unsure that their error-laden, cherry-picked data really convinced any one who wasn’t already leaning in that direction. Indeed, the fact that their magnum opus was never peer reviewed tells you much about how serious it was as an academic work. That is much more revealing about the people who championed the paper than it is about the paper itself. We now know it was little more than junk science, but it fit the pre-existing narrative of those who favor smaller government. They adopted it not despite of its flaws, but rather because of them. It said exactly what it was they wanted to hear, so why bother having it peer-reviewed? If the thinking process of investors is flawed, filled with cognitive errors and biases, imagine what the process is like for ideologues and political types. The bottom line is that, just as investors seek out those articles, research reports and commentary that support their existing portfolios, so too do politicians look for similar writings that confirm their pre-existing notions. We know that human thinking all too often is a flawed process which quite often resembles little more than James’ “rearranging of their prejudices.” We might as well blame farmers for obesity; they grow lots of different foods, but they do not force anyone eat french fries. We as a society run into a problem when we confuse confirmation bias with thought — especially in the political arena.

Previously: Are You an Investor or a Story Teller? (April 25th, 2013) |

| Warren Buffett Explains ‘Colorful Charlie’ Posted: 06 May 2013 04:00 AM PDT After a marathon question-and-answer session with shareholders, Becky Quick asks Warren Buffett to comment on some of Charlie Munger’s best lines.

|

| Posted: 06 May 2013 03:00 AM PDT Federal Deficit and Markets

Jim Bianco noted an interesting development in his May 1, 2013, chart pack. He observed that in the second quarter of this year the US Treasury was paying down debt for the first time since 2006. We started to think about that and what the implications might be for Treasury bond pricing in the present market environment. We have not seen this type of Treasury paydown since 2Q 2009. We still have the Federal Reserve (Fed) spending $85 billion a month to purchase Treasuries and federally backed mortgage paper. That differentiates the present period from 2009 and earlier eras. Part of that purchase is to replace maturities that roll off. A second part is newly printed money in the form of QE applied toward absorption of federally guaranteed bonds and notes. Meanwhile, we are now in a quarter in which the US Treasury is decreasing its outstanding debt. So, if you include the Fed with the Treasury as combined arms of the federal government, the federal debt in the hands of the public will actually shrink this quarter. Remember that the Fed, along with other major central banks, was on the sidelines the last time we had any period of paydowns. We wonder whether this development marks a regime change, a paradigm shift that helps explain why Treasury yields in the intermediate term (10-year note) are so low. Do the paydowns add to the downward momentum of yields? Let’s go a step farther. Bianco points to Treasury officials’ projections for borrowing in 3Q 2013. They estimate that borrowing at $223 billion. That number is much lower than its counterpart in any of the years since the financial crisis triggered the new Fed QE policy. If we assume that the Fed continues its present $85 billion a month QE policy in 3Q, we can argue that the combined actions of the Fed and the Treasury will mean no net impact on the publicly held Treasury supply. Half a year will go by without any net new Treasury debt being placed in the market. New debt issuance since the financial crisis has been lower than in prior comparative periods. In the combined third-quarter projection and second-quarter realization, we see, as a result of declining net issuance of federal debt with market pressures reduced by hundreds of billions of dollars. At the same time, Fannie Mae and Freddie Mac are still embroiled in their restructuring debate, and their issuance, too, is much less robust than it was prior to the financial crisis. Where are we going with this thought? Well, it appears that, while the Fed continues to absorb new issuance of federally backed securities, the amount of new issuance is declining on a net basis. That helps explain lower interest rates. Simply put, the price goes up when you have less of something produced and more of it purchased. When it comes to bonds, that means that yields go down. We note the same activity underway in the rest of the developed world. We see it in the Eurozone, where it is increasing. We see it in Japan in the form of a policy change of monumental proportions. We also see it in the UK and in other G20 countries. All this leads us to the following place. As long as these central banks continue with QE and their short-term interest rates are held near zero, the likelihood of decreasing interest rates is much higher than market expectations may reveal. And the likelihood of abruptly rising interest rates is further reduced as long as the central banks collectively are involved in quantitative easing. The outlook is for at least another year or two at the current momentum. No central banks are involved in cessation of easing and extraction of excess reserves they have created. Most are still expanding. Discussions of “tapering” are commencing. Tapering means slowing the pace of expansion of reserves. Once tapering is underway, there has to be stabilization and then a gradual period of reduction. The studies we have seen indicate that this process will take many years. No central bank wants to shock the economy the way the Fed did in the late 1930s, with its too-soon response. Chairman Bernanke, Vice Chairman Yellen, and their colleagues in the Fed’s governance structure are very familiar with Fed history and the mistake made in the 1930s. They have written about it and referred to it. That experience suggests that they will err in the direction of waiting too long before removing QE or tapering the existing process. They will not be symmetrical in the decision-making process between too soon and too late: too late wins this argument. For investors, that means a prolonged period of very low interest rates, which are bullish for asset classes of nearly all types. Cumberland’s accounts remain fully invested in US stocks. Our international accounts are fully deployed. Our bond accounts continue to hold longer-duration instruments. We are gradually introducing and developing interest-rate hedging structures in preparation for an eventual rise in interest rates. In a coming essay, my colleague, Bob Eisenbeis, will discuss what this means for collateral scarcity. ~~~ David R. Kotok, Chairman and Chief Investment Officer, Cumberland Advisors. |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment