The Big Picture |

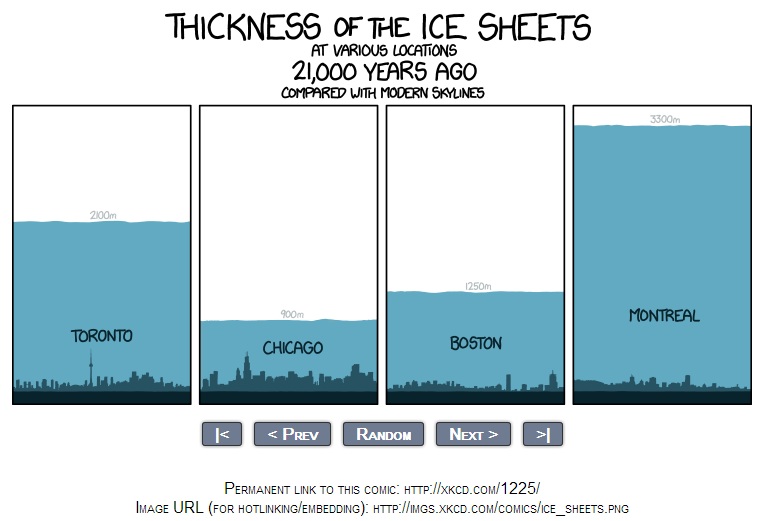

- Thickness of Ice Sheets

- 10 Tuesday PM Reads

- Taper Tantrum

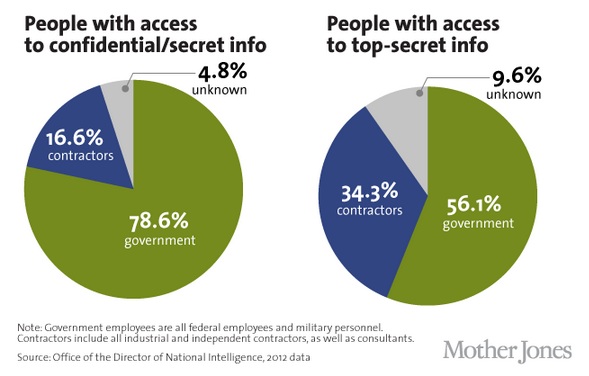

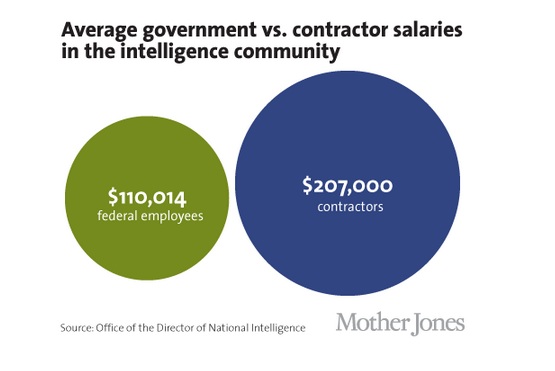

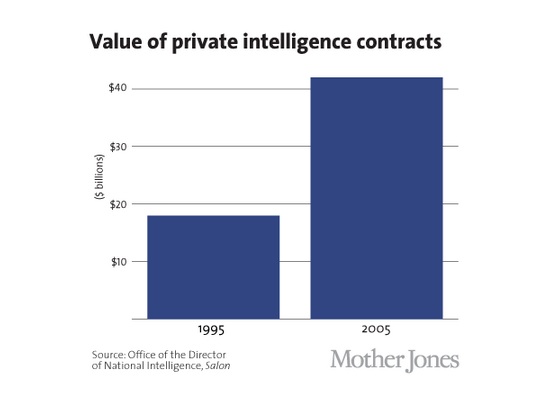

- The Private-Intelligence Boom, by the Numbers

- Looking at Asset Class Returns by Year

- 10 Tuesday AM Reads

- “What’s your outlook on the markets and the economy?”

- Tesla Versus Local Car Dealers

- A Market Built on Theft Sucks

| Posted: 19 Jun 2013 02:00 AM PDT |

| Posted: 18 Jun 2013 01:30 PM PDT My afternoon train reads:

What are you reading?

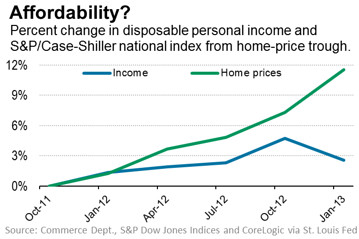

Will Home Prices Be Constrained by Stagnant Incomes? |

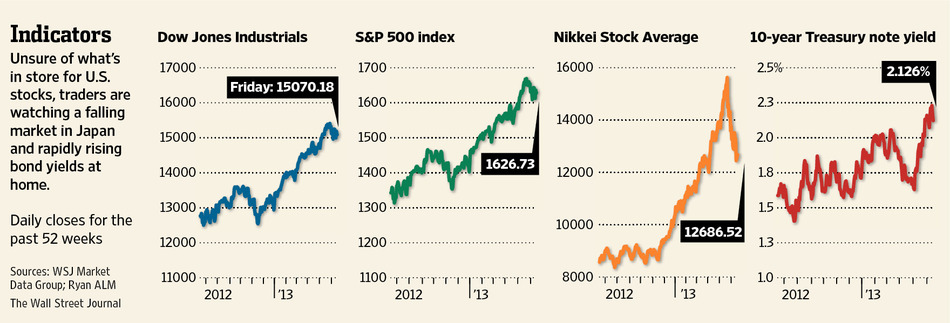

| Posted: 18 Jun 2013 01:00 PM PDT The Times's David Gillen on market gyrations as Wall Street and world economies tries to guess when the Federal Reserve will slow, or taper, its extraordinary measures to bolster the economy.

Taper Tantrum See also Obama Says Bernanke Has Been at Fed 'Longer Than He Wanted' |

| The Private-Intelligence Boom, by the Numbers Posted: 18 Jun 2013 11:30 AM PDT |

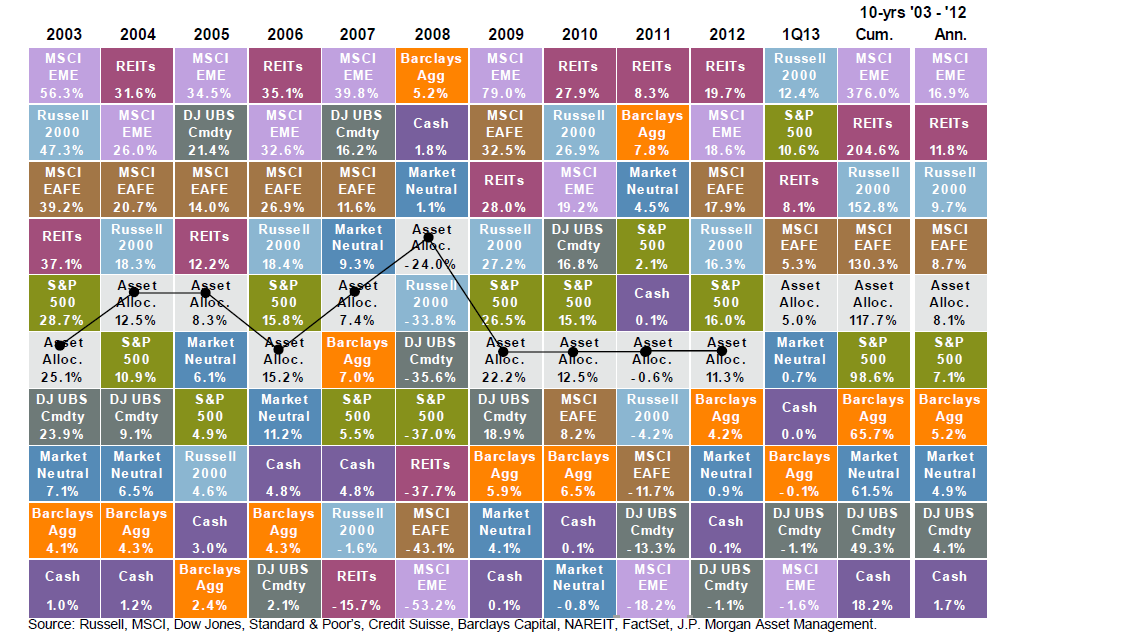

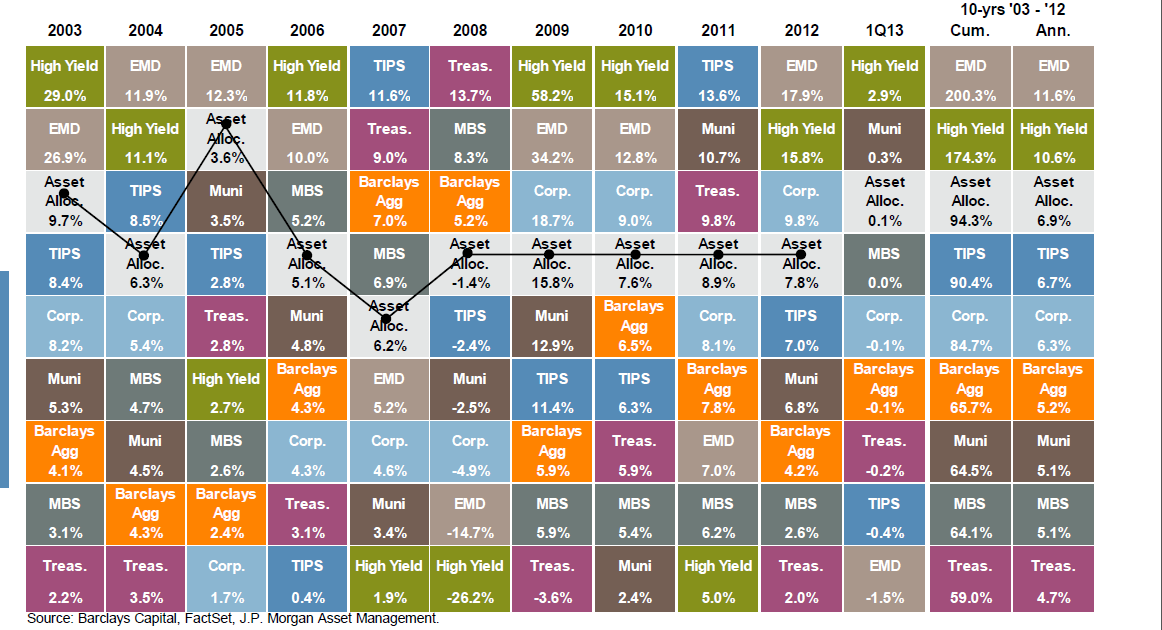

| Looking at Asset Class Returns by Year Posted: 18 Jun 2013 09:00 AM PDT The pushback from the weekend’s WaPo column was surprisingly fierce. If you can tell me what asset classes will perform best each year in advance, than by all means over-weight that sector. But if you are like the other 99.99% of investors, you are probably better off saying to yourself “Why should I guess when I can own them all? The charts below show returns for asset classes and specifically for fixed income.

Asset Class Returns

Fixed Income Sector Returns |

| Posted: 18 Jun 2013 07:00 AM PDT My morning reads:

What are you reading?

Will the Stock Market Party On? It’s All Up to the Fed. |

| “What’s your outlook on the markets and the economy?” Posted: 18 Jun 2013 04:15 AM PDT I have a few conferences coming up later this summer, and as part of one event, I was asked a series of questions in advance. Its a pre- interview, and I figured I would work my way through the questions a little bit all week. But then I read the first question — the headline of this post — and it gave me pause. It is a fairly standard query, but always makes me want to shake the reader out of their stupor, shift their perspective in an entirely different direction. Why? Because the answer people want is very different than the answer they really need. So I will attempt to answer the above inquiry three different ways: Direct challenge, a Socratic query, and discussing the present (not future) state of the markets/economy. Direct:

Socratic:

Present state of the markets/economy:

No one is happy with these answers. They are not what they want to hear, but often what they need to hear.

|

| Tesla Versus Local Car Dealers Posted: 18 Jun 2013 04:00 AM PDT

|

| Posted: 18 Jun 2013 03:00 AM PDT A Market Built on Theft Sucks

OK. Sorry for this; long note coming. You remember the latency arbitrage that HFT said doesn't exist? Manoj Narang, CEO of Tradework, the only HFT firm dying to speak about HFT strategy to regulators, big media, small media, industry panels, and folks in the mall, spent the better part of eighteen months trying to debunk the existence of latency arbitrage. He specifically singled out our white paper, Latency Arbitrage, on numerous occasions. HFT wants you to believe there is no such thing as HFT's gaming algorithmic orders traveling through the Web of Chaos and Dark Pool land. He and "the others" are wrong. Latency arbitrage does exist. And latency Arbitrage is theft. A system is in place that purposely builds in two separate speeds for "different classes" of industry traders. We draw your attention to Reg NMS, the 371 document created by the SEC. Well actually it was created by the industry and rubber stamped by the SEC, but we digress. Go to page 102/103. The rule discusses a 1 second window: Specifically, the Commission proposed that pursuant to Rule 611(b)(8) trading centers would be entitled to trade at any price equal to or better than the least aggressive best bid or best offer, as applicable, displayed by the other trading center during that one-second window. For example, if the best bid price displayed by another trading center has flickered between $10.00 and $10.01 during the one-second window, the trading center that received the order could execute a trade at $10.00 without violating Rule 61. Most of the commenters that addressed this exception supported it. The SIA noted that the exception would provide "much-needed practical relief." Several commenters, however, raised issues regarding the time frame for the exception….One commenter opposed the exception because it believed that it would create an arbitrage opportunity that could be taken advantage of by computerized market participants. Another commenter expressed concern that the exception would enable trading centers to execute trades internally and route orders using the worst quotation during the one second window. The SEC knew about latency arbitrage in 2005. They were alerted to the fact that it exists, and that differences in speeds of market centers could cause problems. What did they do? After reviewing the response from commenters, the Commission is adopting the exception as proposed. Allowing a one-second "window" prior to a transaction for trading centers to evaluate the quotations at another trading center will ease implementation of and compliance with the Order Protection Rule. Do you think this "feature" of our market structure is a benefit, or a risk? What does the SEC think? Wait. We know what the SEC thinks. In their joint post-mortem Flash Crash report with the CFTC, they lay the blame for the Flash Crash on data delays, hot potato trading, and internalizers! The Flash Crash was mostly due to two of the things the SEC was warned would happen when they were crafting Reg NMS in 2005! Oh, and in March 2009 the Wall Street Journal published an article, Measuring Arbitrage in Millseconds that discussed latency arbitrage a full fourteen months prior to the Flash Crash, and nine months before our own latency arbitrage white paper. Exchanges disseminate continuous updates of the NBBO on stocks in separate feeds to the price quotations. Many dark pools, the anonymous stock-trading electronic venues that don't publish bids and offers, price stocks at the midpoint of the NBBO because they want to give clients some benchmark for their pricing. The delay between the appearance of bids and offers on the direct feeds and the processing of the NBBO at dark pools presents arbitrage opportunities. If a fund's computers are fast enough, they can estimate where the midpoint of the NBBO will be fractions of a second faster than dark pools, which allows them to know where the price is going in that pool. "You have tomorrow's newspaper today," said Richard Gates, a portfolio manager for TFS Market Neutral fund in West Chester, Pa., who looked into a latency-arbitrage strategy after a broker outlined the success other funds had with it. "You're looking at stale prices. Those are the types of investment strategies that arbitrageurs and hedge-fund managers drool over." Scott Patterson, WSJ reporter, wrote this article in June 2010: Fast Traders' New Edge; Investment Firms Grab Stock Data First and Use It Seconds Before Others. In that article, one buy side firm laid a trap and proved how the built in arbitrage steals in dark pools: On a March afternoon, a TFS trader sent an order to a broker to buy shares of Nordson Corp., a maker of fluid dispensing equipment. The trader sent an instant message to the broker: "please route to broker pool #2," a request to send the order to a specific dark pool. The trader told the broker not to pay a price higher than the midpoint between what buyers and sellers were offering, which at the time was $70.49. Several seconds after the dark pool order was placed, the market price didn't change. Then the TFS trader set a trap: he sent a separate order into the broader market to sell Nordson for a price that pushed the midpoint price down to $70.47. Almost immediately, TFS was sold Nordson for $70.49—the old, higher midpoint—in broker pool No. 2, which didn't reflect the new sell order. TFS got stuck paying two cents more than it should have. Oh, and if you don't think that enough was proof that latency arbitrage exists, and that it hasn't been thought about and exploited since 2005, i.e. if you are Manoj, then allow us to give you the best current proof that latency arbitrage exists and is exploited: Recently, Goldman announced that they changed their data feed to eliminate the possibility that latency arbitrage could occur in their dark pool, Sigma X. Read about it here, and/or here. Isn't that the best damn proof that latency arbitrage exists you could ever hope to see? Maybe the SEC will reverse what the industry has engineered, and it rubber stamped, and realize that a market built on theft suck$. Chairman Mary Schapiro suggested as much in December 2010 in when she testified to Congress they were looking into "abusive co-location and data latency arbitrage activity in potential violation of Regulation NMS." (Transcript here). We are happy they started looking into it a full year ago. We have a one-word question: And? - See more at: http://blog.themistrading.com/a-market-built-on-theft-sucks/#sthash.556fsmJY.dpuf |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment