The Big Picture |

- Austerity is a Four-Letter French Word

- Growing Up with Social Media

- QOTD: The World

- Missed the big market rally? Here’s what to do now.

- 10 Weekend Reads

| Austerity is a Four-Letter French Word Posted: 23 Jun 2013 02:00 AM PDT Austerity is a Four-Letter French Word

A Great Deal If You Can Get It |

| Posted: 22 Jun 2013 10:30 PM PDT |

| Posted: 22 Jun 2013 12:00 PM PDT Here is a quote to distract you from the Red on your screens this week:

|

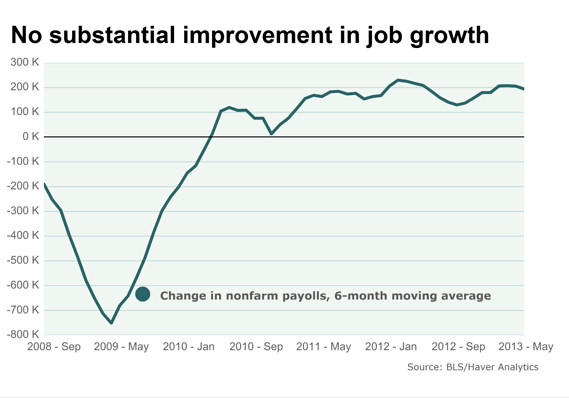

| Missed the big market rally? Here’s what to do now. Posted: 22 Jun 2013 07:00 AM PDT Missed the big market rally? Here's what to do now.

So, you missed the big market rally. U.S. stocks have moved nearly 150 percent since the March 2009 lows, and you sat out most of those gains. I've heard all the reasons: Maybe you jumped out of stocks in 2008 and stayed out. Perhaps you were in at the lows, but after the first 20 percent advance, you lost your nerve. The Flash Crash of May 2010 sent you running for cover? Or was it the 19 percent drop before QE2 was announced in August 2010? There's always some reason that looked good at the time. The asset management business, it turns out, involves a lot more behavioral counseling than you might guess. In any case, the markets have powered upward and onward without you. What do you do now? How to begin to repair the damage? It is a two-part process: The initial steps are designed to help you overcome your risk aversion — the emotional aspects of investing. Call it your "erroneous behavioral economic zone." After we fix that big underutilized brain of yours, we can move on to the investment steps that allow you to work your way back into markets. 1 Acknowledge the error: First thing you need to do is own up to the mistake. No, this wasn't the fault of the Fed or President Obama or some algorithm trading server somewhere in New Jersey. It is your portfolio, your retirement account, your future. You cannot fix it if you are still blaming everyone else. (I find that tracking my blunders in annual mea culpas to be helpful). 2 Stop beating yourself up: This market has confounded amateurs and pros alike. Unless you came to an early understanding of how the Fed has been driving liquidity and, therefore, equities, it was easy to miss. As we noted last month, even the supposed best and brightest hedge fund managers have stunk up the joint. Give yourself a break, and move on. 3 Change your sources: Most of the people I speak with who have missed this huge move have been consuming a diet of doom and gloom. If you think that it doesn't affect you, you're kidding yourself. Constantly reading about hyperinflation and the collapse of the dollar and the end of the United States as a world power and the student loan crisis and omigod Obamacare is going to crush America and the Chinese are taking over the world and . . . STOP! Right now. It is recession porn, a focus on the negative that is a leftover effect of the crash and great recession. Go through your bookmarks, and delete all of these sites: the goldbugs, the end-of-worlders, the doom-and-gloomers, the outraged Fed critics, the Obama haters. They all have agendas that typically have to do with selling you subscriptions or advertising. They are not at all concerned with your returns, your portfolio or your retirement. 4 Review your process: Now that you have eliminated the crazies, look at the rest of your process. How do you make investment decisions? Are you careening from stock pick to stock pick, after watching too much financial TV? Do you even have a process? Whatever it is you have been doing obviously has not been working. It is likely you are missing two important components of an investment plan: the plan itself and an error-correction method that allows you to reverse the inevitable mistakes that will occur. 5 Create an asset-allocation model: Of course, if you missed the entire rally, you don't have much of a plan. You need a full-blown investment strategy. Own five to nine broad indexes, typically in exchange-traded funds (ETFs) or low-cost mutual funds. In decreasing amounts (35 percent, 30 percent, 20 percent, 5 percent), you should own: large caps, small caps, emerging markets, global equities, technology, real estate, bonds (corporates, Treasurys, munis) and commodity indices. This is your asset allocation model. And here's what to do with it: 6 Deploy your capital: You need to make your capital work for you, not sit in cash. Deploy this capital based on time, on market levels, on a model or any objective metric, just so long as it is not driven by your gut instinct. When it comes to investing, your emotions will betray you every time, sending you running in the wrong direction and at the worst possible moment. Using a framework of entries that are objectively derived overcomes this risk-aversion problem. 7 Dollar-cost average: You can allow time to work in your favor by deploying your capital in 12 monthly (or four quarterly) equal amounts. This avoids the classic market timing issue, and allows any market volatility to work in your favor. The other advantage is that if the market runs away to the upside before you fully deploy, you at least have some exposure, and you are averaging up into the rally. Historically, the math works better with lump-sum investing, but understand that this strategy is about emotions, not numbers. An alternative is to use purchase points based on market levels: Set a series of levels in 5 or 10 percent increments above and below where your favorite index (Dow, Russell, etc.) is today. With each market move, up or down, deploy another 10 or 20 percent of your capital to the equity side (decide this in advance, or you will mess it up). If the market gets cut in half, you are fully invested in equities at enormously advantaged prices. This sounds great in theory, but the reality is that when markets are at their cheapest, they also look their scariest. Very few people have the discipline to make buys into the mess. 8 Rebalance regularly: You now have a simple model with various asset classes held in different weightings (35 percent to 5 percent). Over time, some will do better or worse than others. Eventually, the model drifts. The process of returning the portfolio to its original percentage weightings is called rebalancing. Plan on rebalancing regularly — quarterly for larger portfolios of more than $1 million, semiannually for mid-size and annually for accounts less than $100,000. What this means in practice is that as any asset class gets expensive or cheap, you get to make small, advantageous shifts. You buy a little of what has become cheap and sell a bit of what has become dear. The academic data show this creates about 1 percent in additional performance over longer investment cycles. It doesn't cost anything and adds no extra risk. It is the closest thing to a free lunch that exists in finance. 9 Be diversified: We own stocks and bonds and real estate and commodities (pretty much in that order). When one market or asset class is falling, others tend to go in the opposite direction. We also own a broad variety of equities: There is geographic variation, differing market-capitalization sizes and economic sectors. Diversification usually means that different asset classes behave differently. When equities get shellacked (like this past week), bonds tend to rally. (It was reversed last month: Stocks rallied, bonds sold off). A balanced portfolio approach tends to underperform markets on the way up but suffer much less on the way down. The goal is to allow you to pursue your financial goals but still sleep at night. 10 Understand your time line: People have a foolish tendency to lose sight of the long term in the midst of the day-to-day noise. Most of you have an investing timeline between 10 to 40 years. (If you plan to start withdrawing money to live on in 10 years or less, you will need to be more conservative). But those of you in your 20s, 30s, 40s or even early 50s have a much longer time horizon. Secular (or long-term) bear markets are to be expected, and they let you buy advantageously if you can overcome your own instincts. Volatility and short-term market swings are part of the nature of markets. When your investing timeline is measured in decades, you cannot afford to continually miss an ongoing rally because of day-to-day volatility. Markets that rally 150 percent come along once a generation. If you missed this one, it is probably because you based your investing on some form of guess as to what stocks were going to do. Experience teaches us that we are all pretty bad at making forecasts nearly all of the time. This is why any prediction-based investment strategy is doomed to failure. The outcome is binary: Your guesses are either right or wrong. Consider instead a probability-based investment approach. The idea behind asset allocation is to allow mean reversion, rebalancing and diversification to work in your favor. No guesswork required. ~~~ Ritholtz is CEO of FusionIQ, a quantitative research firm. He is the author of "Bailout Nation" and runs a finance blog, the Big Picture. Follow him @Ritholtz. |

| Posted: 22 Jun 2013 03:00 AM PDT Good Saturday morning. We once again have (unusually) glorious weather here in the NorthEast, so don’t expect me to be any where near a computer all day. No worries, though — here is my list of the longer form reading I have collected this week to keep you occupied:

Where are you sailing to today?

7 charts that tell the Fed not to taper QE3 |

The France that I see as I look out from the bullet train today is far different from the France I see when I survey the economic data. Going from Marseilles to Paris, the countryside is magnificent. The farms are laid out as if by a landscape artist – this is not the hurly-burly no-nonsense look of the Texas landscape. The mountains and forests that we glide through are glorious. It is a weekend of special music all over France, and last night in Marseilles the stages were alive and the crowds out in force. The French people smile and graciously correct my pidgin attempts at speaking French. I have found it diplomatic not to mention that I think France is in for a very difficult future. Why spoil the party?

The France that I see as I look out from the bullet train today is far different from the France I see when I survey the economic data. Going from Marseilles to Paris, the countryside is magnificent. The farms are laid out as if by a landscape artist – this is not the hurly-burly no-nonsense look of the Texas landscape. The mountains and forests that we glide through are glorious. It is a weekend of special music all over France, and last night in Marseilles the stages were alive and the crowds out in force. The French people smile and graciously correct my pidgin attempts at speaking French. I have found it diplomatic not to mention that I think France is in for a very difficult future. Why spoil the party?

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment