The Big Picture |

- Switzerland – Chapter 2

- A Visual Map of the History of Jazz

- Succinct Summation of Week’s Events (1/16/15):

- Biggest Threat to Human Progress is Relentless Stupidity

- There’s Never Been a Better Time to Be Rich . . .

- 10 Friday AM Reads

- New Ford GT

| Posted: 17 Jan 2015 02:00 AM PST Switzerland – Chapter 2 Russian businesses secured loans denominated in low-interest foreign currencies, including the Swiss franc. The franc was then pegged to the euro. The collateral for the loans depended on an assumption of $100 oil and a Russian ruble that has since plummeted. It appears that some of these agents now cannot pay. Real estate speculators in Warsaw pledged their real estate to secure loans in Swiss francs. Why? The interest rate was very low – much lower than if they had borrowed in zlotys. Or they borrowed euros with the assumption that the Swiss peg against the euro would remain in place. These borrowers around Europe and elsewhere in the world pledged collateral, took on foreign-currency risk, and based the risk-taking on the commitment of the Swiss National Bank (SNB) to maintain its currency peg at 1.2 francs to a euro. Many of these borrowers are now sweating bullets. Markets around the world are reacting in fear of contagion that could result from these debts. Is the reaction rational? We shall find out in due time. We do not know how much debt there is, who the borrowers are, or what banks and intermediaries are involved in the loans. We do not know what supervision and regulation have been applied, since this is activity that is mostly outside the US and thus not supervised under the post-Dodd-Frank regulatory regime. Markets can handle good news, and they can handle bad news. Markets have trouble, however, with uncertainty. The pressure on stock markets and the volatility that has spiked due to the SNB's move are the results of rising uncertainty about the foreign-currency-denominated debt and abrupt changes in central bank policy. The Swiss have punched new holes in their cheese. They have boiled their chocolate so that it smells bad. They committed to a course, reversed themselves, and have now lost their credibility. This is the second governor of the Swiss central bank who has suffered a loss of credibility. The first one had to resign because a member of his household was allegedly trading a foreign currency position against the euro peg. The second governor has derailed billions in loans and pressured his citizens through his unexpected policy change. When one central bank loses its credibility, all central banks suffer. The burdens on the Federal Reserve, the European Central Bank, the Bank of Japan, the Bank of England, and others have now intensified. ~~~ David R. Kotok, Chairman and Chief Investment Officer

|

| A Visual Map of the History of Jazz Posted: 16 Jan 2015 06:00 PM PST Click for the full map. |

| Succinct Summation of Week’s Events (1/16/15): Posted: 16 Jan 2015 01:15 PM PST Succinct Summation of Week's Events

Negatives:

Peter Boockvar |

| Biggest Threat to Human Progress is Relentless Stupidity Posted: 16 Jan 2015 09:30 AM PST

On Fridays, I like to wax eloquent and philosophical — about investing, analysis and asset management. Often, there are lessons from other disciplines that are applicable to our own. Sometimes I point out an especially insightful work. But most of the time, I like to highlight misguided, faulty or just plain dumb analysis. The latter is our subject today: a dishonest and disingenuous argument that is technically correct, but cynical and misleading. It only takes a bit of thinking to realize the absurdity of the claim. Writing in the Washington Times during last month’s holiday week was this column from Richard Rahn of Cato Institute with the headline, “Common folk live better now than royalty did in earlier times. ” The entire enterprise is a fatuous and politically inspired attempt to minimize the issue of income inequality, because after all, the poor today live better than kings did centuries ago! There, all problems solved, Here’s Rahn:

Let's set about fisking this intellectual detritus:

|

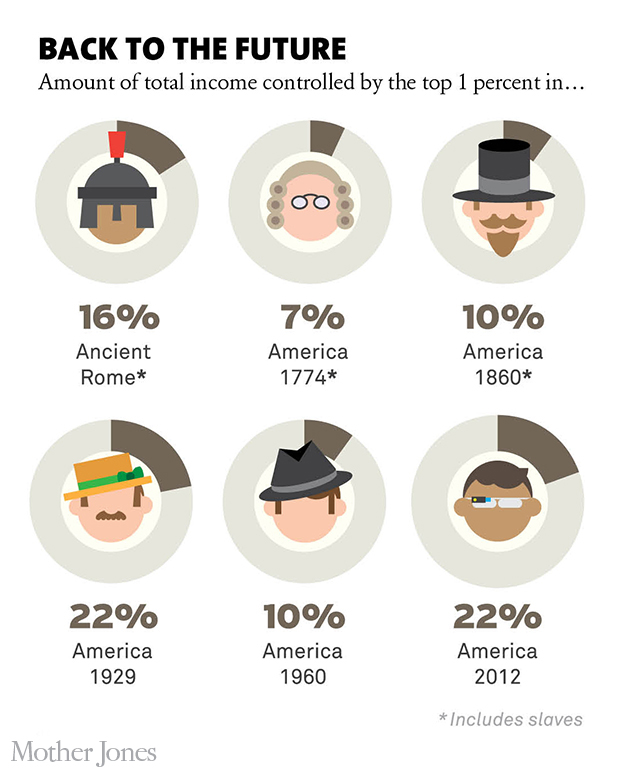

| There’s Never Been a Better Time to Be Rich . . . Posted: 16 Jan 2015 08:30 AM PST

|

| Posted: 16 Jan 2015 05:30 AM PST Good Friday morn. Heckuva week, but its almost over. To tide you til the weekend, here are our morning train reads:

|

| Posted: 16 Jan 2015 03:00 AM PST

From Top Gear:

From Road and Track:

|

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

0 comments:

Post a Comment