The Big Picture |

- ML-Implode Gets “Wikileaks Treatment” As Wells Fargo Freezes, Closes Business Account

- 10 Mid-Week PM Reads

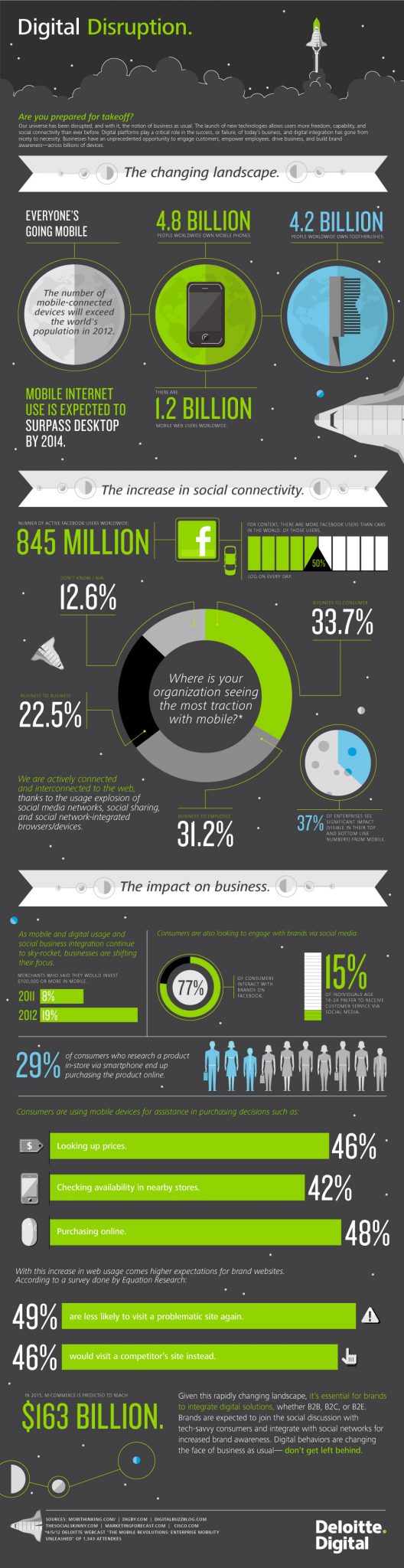

- Digital Disruption

- 10 yr auction ahead of OSYC expiration

- Are U.S. Debt Levels Now Manageable?

- Fun With Predatory Lending

- Jamie Diamond day

- 10 Mid-Week AM Reads

- The Genius of Mutual Indebtedness

- Riding The Gravy Train

| ML-Implode Gets “Wikileaks Treatment” As Wells Fargo Freezes, Closes Business Account Posted: 13 Jun 2012 04:00 PM PDT ML-Implode Gets "Wikileaks Treatment" As Wells Fargo Freezes, Closes Business AccountJune 13th, 2012

ML-Implode.com discovered yesterday (2012-06-12) in the course of its normal banking activities that Wells Fargo had frozen its bank account with no warning. Upon inquiring at the local branch (which had no direct knowledge of the incident), it was discovered the account had been flagged "credit risk", and slated to be immediately closed. While the site is effectively insolvent (due to the impact of multiple frivolous libel suits from corrupt mortgage, e.g. by the outlawed Grant America scheme) and thus typically had a minimal balance, there had been no problems with overdrafts and all charges and obligations were always dutifully covered. [ALERT: Help us fight this and other attempts to attack us and shut us down. Donate now. You can also contact us to inquire directly about sending cash or checks. We are also looking for pro bono legal support on financial threats such as this one, and first amendment threats against us. OUR FREE SPEECH IS YOUR FREE SPEECH -- and freedom isn't free!] In fact, as part of the freeze, Wells Fargo made a $3500 deposit from ML-Implode's merchant account processor "disappear", leaving a short-term advance of $1500 from an affiliate un-covered, and a similar $1500 obligation to another affiliate unpaid. The whereabouts of the monies are unknown. Other arrangements are being made; however, the actions are shocking due to their intrinsic lack of due process and harshness — no advance notice was given and no real reason was given for the action (as "credit risk" does not actually apply to the type of account in question). It is believed that the actions were taken in retaliation for a recent series of articles by ML-Implode blogger Martin Andelman which pulled no punches in criticizing Wells Fargo over its foreclosure practices — in particular the tragic and horrific case of Norm Rousseau who was driven to suicide after Wells Fargo lost a mortgage payment and mistakenly foreclosed on the family's home, despite a lengthy back-and-forth process which gave the bank ample opportunity to correct the mistake. (Other recent articles by Andelman taking Wells to task that may have angered the bank include this one and this one.) Andelman is not paid by ML-Implode and blogs wholly independently (as many others have done on in the past); ML-Implode does not dictate or control what he writes. As such, if Wells' actions are truly in retaliation for the articles, they are apparently violating federal law: USC 47 USC § 230 forbids holding an internet "common carrier" (such as an ISP, forum, or any sort of hosting outfit) liable for the content users independently post or transmit. The prior week, ML-Implode affiliate REST Report Matters (http://www.restreportmatters.com/), inspired and promoted by Andelman to give homeowners at risk of foreclosure access to the same loan analysis tools the banks have, also had its account shuttered by Wells Fargo. It appears the bank first followed Andelman's references to REST Report Matters, targetted that company, then connected REST Report Matters back to ML-Implode's business account (via affiliate transactions) and marked that account for "summary execution" as well. Martin Andelman has no ongoing financial relationship with REST Report Matters, which means Wells' shuttering of their accounts amounts to tortious interference with a legitimate, independent business. Of course, since that business constitutes giving homeowners tools to force Wells and other banks to modify loans when compelled to do so by the HAMP and other programs, one can easily imagine that they believe they are killing two birds with one stone by trying to shut down them and ML-Implode (which generally supports just and equitable treatment of homeowners facing foreclosure). The bank seems to have "covered" itself for its actions by effectively giving no reason for them, so there is nothing to appeal or argue against. However, our sources inside the bank tell us the critical blog posts were the motivating factor. There is little precedent for such authoritarian, if not illegal actions by a bank, which effectively amount to domestic economic sanctions. In one case last October, Goldman Sachs pulled its support from the credit union that was merely honoring the Occupy Wall Street group. Prior to that, in 2011, Wikileaks famously had its account frozen by PayPal and its Swiss bank account closed under pressure from the US State Department. Meanwhile, Wachovia in 2011 (by that point a subsidiary of Wells Fargo) paid a less-than-.1% fine for knowingly allowing nearly $400 billion in drug money to be laundered through itself — a fact which is essentially not discussed in the media at all, and so the outcome constitutes essentially a free pass. In a May 2010 landmark decision, the New Hampshire Supreme court ruled in the case of The Mortgage Specialists vs. Implode-Explode Heavy Industries, Inc. (ML-Implode's owner/operator) that the site constituted the "news media" and should be afforded all the journalistic protections provided by the law and our general tradition of free speech jurisprudence. |

| Posted: 13 Jun 2012 01:30 PM PDT My afternoon train reading:

What are you reading?

China’s monetary policy |

| Posted: 13 Jun 2012 12:30 PM PDT |

| 10 yr auction ahead of OSYC expiration Posted: 13 Jun 2012 10:27 AM PDT Ahead of the FOMC meeting next week and likely commentary on the fate of Operation Smother the Yield Curve that expires at months end, the 10 yr note auction was pretty good as the yield was below the when issued. Also, direct and indirect demand was the best since Dec. The bid to cover though at 3.06 was just slightly below the previous 12 month avg of 3.10. As said by a few Fed members over the past couple of weeks, if the FOMC decides to extend OSYC they will likely play in the MBS world instead of US Treasuries in order to tighten the gap between mortgage rates and the 10 yr US Treasury benchmark. The question of fresh QE remains to be seen. |

| Are U.S. Debt Levels Now Manageable? Posted: 13 Jun 2012 09:00 AM PDT Market News – U.S. debt load falling at fastest pace since 1950s Comment The chart below shows what the story above says, debt is growing slower than anytime since the 1950s (second panel). Click to enlarge:  Comment And as this next chart shows, debt to GDP has declined. However, as the chart title says, Does Anyone See Deleveraging? Private debt share of GDP is at its lowest level since 2004. Government debt to GDP is at a new high. Overall debt to GDP is at is lowest levels since 2007. Are these the levels that one would blow the all-clear signal? Is this why we had the worst recession since the great depression? To get back to the 2007 levels?  Comment As the final chart below shows, overall levels of debt are at new highs. This has been driven by a surge in government debt. Remind us again on how we can talk about deleveraging when overall debt levels are at new world records?  Source: Bianco Research |

| Posted: 13 Jun 2012 09:00 AM PDT

Wells Fargo's top-producing loan officer testified in court some of the more unsavory and nefarious lending practices WFC engaged in. Her sworn testimony involved how the bank targeted heavily African American areas for shoddy mortgages and subprime loans, even for people with “sterling credit ratings.” This arose due to Justice Department investigations into Wells Fargo’s alleged fair-lending violations. Structurally, Wells Fargo provided the sort of misaligned financial incentives that helped to create so much of the crisis. Regardless, that is a hell of a chart!

Source: |

| Posted: 13 Jun 2012 07:02 AM PDT Japanese machinery orders rose by +5.7% in April, much higher than the +1.6% expected; Chinese press reports state that the Chinese economy will grow by less than 7.0% in the 2nd Q. Well, I suspect it will, which is why China has to ratchet up its stimulus programme, particularly given the major change in leadership later this year. Quite frankly its happening already – no big headlines, but its certainly happening – expect more imminently; Greek deposit outflows are rising ahead of this Sundays general election – the precise amount is unknown, but one analyst suggested that some E700mn was withdrawn yesterday; As is always the case Fitch, downgraded 18 Spanish banks, following last weeks downgrade of the sovereign. Spanish 10 year bonds have risen to 6.72%; Italian short term yields soared in today’s 1 year auction to 3.972%, from 2.34% just 1 month ago. Bid to cover was 1.732 times. The 10 year is yielding 6.17% The French government is to revise its economic growth targets (downwards, off course), given the slow start this year. Monsieur Hollande has promised to keep the French budget deficit to 3.0% next year and to balance the budget over his term in office ie 2017. The original targets assume economic growth of +0.5% this year, rising to +1.7% next. Independent forecasts suggest that the budget deficit will be over 5.0% this year and 4.2% next, higher than the 4.5% and 3.0% proposed. A difference of 0.5% implies about E10bn of budget measures. (Source WSJ). EZ factory output declined materially in April – it was down -0.8% MoM, the steepest decline in 4 months and much higher than the -0.1% decline in March. Germany reported the largest decline of output in 7 months, though Portugal was even worse – its output was the weakest since 2000. Continuing weakness (very likely) is going to result in 2nd Q GDP coming in with a negative number; Germanys CDU Mr Kauder states that his party and the opposition will meet again on 21st June to try and reach agreement on the fiscal compact and to pass it prior to the summer break. He added that they were close to reaching an agreement wuith the opposition; The WSJ reports that Germany has commited E113bn to the EZ debt crisis to date (or 4.4% of GDP) which would increase to E401bn, in the event the EFSF/ESM are called upon in full. In addition, the Bundesbank has Target 2 claims of E644bn in April. When aggregated, Germanys total exposure soars to E671bn, or 25% of GDP and rising. Pretty big numbers. Essentially, Germany is increasingly being sucked into this crisis; Jamie Dimon, the CEO of JPM, is due to appear on Capitol Hill today to explain the losses incurred by the CIO. He is going to face tough questioning; US May PPI was -1.0% MoM versus expectations of -0.6% and April’s -0.2%. On a YoY basis, it was up +0.7%, as opposed to +1.9% in April and expectations of +1.2%. Core CPI came in at +0.2% MoM, in line with expectations; Outlook Asian markets rallied following a better performance by US markets yesterday which rose in anticipation of QE3. European markets are flat to marginally lower, though feel weak. Brent oil is around US$97.50, with gold at US$1609. The Euro has crept up to above US$1.2540. The yield on the 10 year German bund is rising – currently 1.52% (still far too low, in my humble view, in the medium/long term, in particular), with comparable US and UK yields at 1.69% and 1.77% respectively. The ECB supported the idea of an EZ wide deposit guarantee scheme – well great but I don’t believe that the Germans are on board. In addition, the EU Parliament passed a vote which supported the introduction of Euro Bonds and, amongst other things, a debt redemption fund and a stimulus programme amounting to 1.0% of GDP. Well great, but no one pays attention to the European Parliament. In addition, enthusiasm for the debt redemption fund seems to be ebbing in Germany. Pretty slow day at present. Cant see much action ahead of the Greek elections this coming weekend Kiron Sarkar 13th June 2012 |

| Posted: 13 Jun 2012 07:00 AM PDT Some morning reads:

What are you reading? > JPMorgan Builds Vast Web of Staff, Financial Ties to Lawmakers |

| The Genius of Mutual Indebtedness Posted: 13 Jun 2012 06:30 AM PDT Nigel Farage: European Parliament, Strasbourg, 13 June 2012 Speaker: Nigel Farage MEP, Leader of the UK Independence Party (UKIP), Co-President of the ‘Europe of Freedom and Democracy’ (EFD) Group in the European Parliament – http://nigelfaragemep.co.uk Hat tip Peter Boockvar Donate to UKIP: http://www.ukip.org/donations | http://www.ukipmeps.org | http://twitter.com/#!/Nigel_Farage • Joint debate: European Council meeting – Multiannual financial framework and own resources A. Preparation for the European Council meeting (28-29 June 2012) B. Multiannual financial framework and own resources Transcript: “Another one bites the dust. Country number four, Spain, gets bailed out and we all of course know that it won’t be the last. Though I wondered over the weekend whether perhaps I was missing something, because when the Spanish prime minister Mr Rajoy got up, he said that this bailout shows what a success the eurozone has been. And I thought, well, having listened to him over the previous couple of weeks telling us that there would not be a bailout, I got the feeling after all his twists and turns he’s just about the most incompetent leader in the whole of Europe, and that’s saying something, because there is pretty stiff competition. Indeed, every single prediction of yours, Mr Barroso, has been wrong, and dear old Herman Van Rompuy, well he’s done a runner hasn’t he. Because the last time he was here, he told us we had turned the corner, that the euro crisis was over and he hasn’t bothered to come back and see us. I remember being here ten years ago, hearing the launch of the Lisbon Agenda. We were told that with the euro, by 2010 we would have full employment and indeed that Europe would be the competitive and dynamic powerhouse of the world. By any objective criteria the Euro has failed, and in fact there is a looming, impending disaster. You know, this deal makes things worse not better. A hundred billion [euro] is put up for the Spanish banking system, and 20 per cent of that money has to come from Italy. And under the deal the Italians have to lend to the Spanish banks at 3 per cent but to get that money they have to borrow on the markets at 7 per cent. It’s genius isn’t it. It really is brilliant. So what we are doing with this package is we are actually driving countries like Italy towards needing to be bailed out themselves. In addition to that, we put a further 10 per cent on Spanish national debt and I tell you, any banking analyst will tell you, 100 billion does not solve the Spanish banking problem, it would need to be more like 400 billion. And with Greece teetering on the edge of Euro withdrawal, the real elephant in the room is that once Greece leaves, the ECB, the European Central Bank is bust. It’s gone. It has 444 billion euros worth of exposure to the bailed-out countries and to rectify that you’ll need to have a cash call from Ireland, Spain, Portugal, Greece and Italy. You couldn’t make it up could you! It is total and utter failure. This ship, the euro Titanic has now hit the iceberg and sadly there simply aren’t enough life boats.” ……………………………. • EU Member States: |

| Posted: 13 Jun 2012 05:30 AM PDT |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment