The Big Picture |

- Shadow Banking System Larger than at the Start of the Financial Crisis

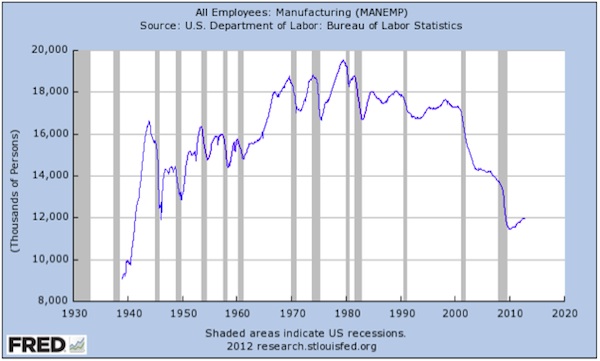

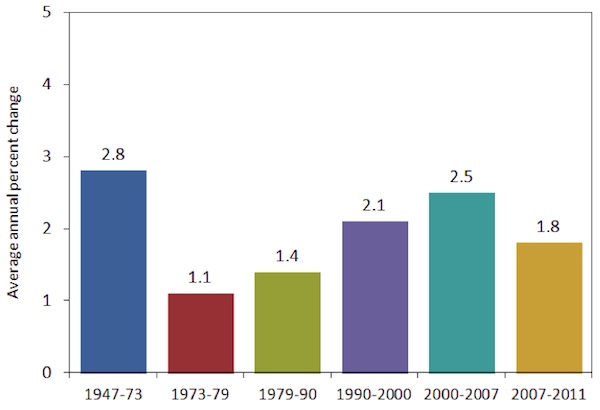

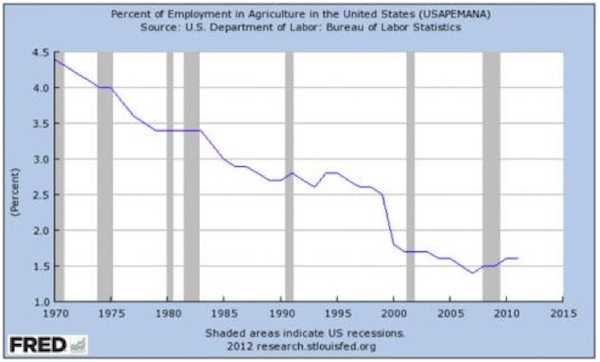

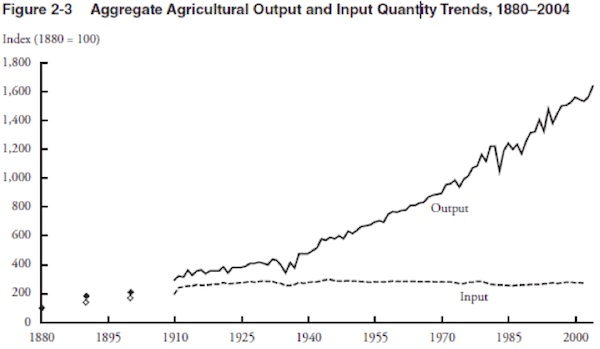

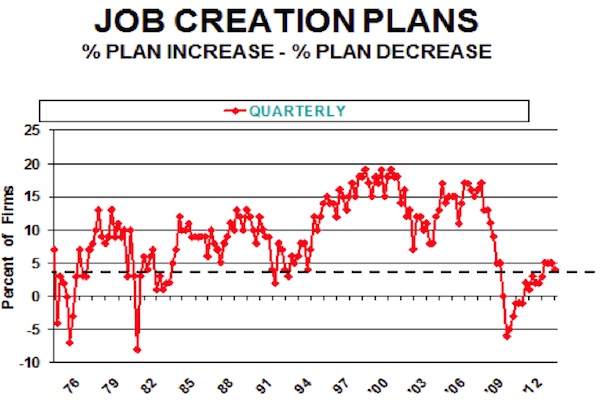

- Where Will the Jobs Come From?

- Fiscal Cliff? Try Mis-Positioned Investments

- Apple’s Big Day

- 10 Monday PM Reads

- Another Fudge Re Greece Proposed

- Foreign Holders of US Treasuries

- Home Sales Remain Bright Spot in Economy

- Existing home sales and builder sentiment

- Much better markets on hope of a solution of the US fiscal cliff

- 10 Monday AM Reads

- “You can’t always get what you want…”

| Shadow Banking System Larger than at the Start of the Financial Crisis Posted: 19 Nov 2012 10:30 PM PST One of the Main Indicators of Financial Danger Has IncreasedThe failure to regulate the shadow banking system was one of the causes of the financial crisis. As we noted in 2009, the Bank for International Settlements – often described as a central bank for central banks (BIS) – slammed the Federal Reserve for failing to rein in the shadow banking system:

Years later, the Fed and other regulators have allowed the shadow banking system to grow even bigger. As Reuters notes today:

At the same time, authorities have relaxed rules against fraud, excessive leverage and moral hazard … three of the other main causes of the financial crisis.

|

| Where Will the Jobs Come From? Posted: 19 Nov 2012 07:00 PM PST Where Will the Jobs Come From? By John Mauldin Nov 19, 2012

The Next Bubble |

| Fiscal Cliff? Try Mis-Positioned Investments Posted: 19 Nov 2012 05:44 PM PST My quote about this idiotic obsession with the fiscal cliff in the Daily Beast:

I think that’s about right . . .

Source: |

| Posted: 19 Nov 2012 05:00 PM PST Apple confirmed its Friday hammer panic bottom with a $38 plus move higher, closing up 7.21 percent on the day. Nice! How big was the move? BIG! Apple's $35.8 billion market cap increase on the day is larger than the total market cap of all but 146 listed public companies. At the high of day, Apple's market value change was larger than the entire market cap of Starbucks and almost as large as Dupont and Deustche Bank's. If ranked as a country GDP, the move is larger than 97 of the 186 economies monitored by the IMF. Stunning! Where to now? We don't know with certainty, but, after consolidating this big move, it looks like the 200-day at $596 is doable, Always with a stop!

|

| Posted: 19 Nov 2012 01:30 PM PST My afternoon train reads:

What are you reading?

Tech Sets Correction Course

Source: WSJ |

| Another Fudge Re Greece Proposed Posted: 19 Nov 2012 12:45 PM PST According to the latest leaks ahead of the EZ finance ministers meeting tomorrow, the EZ is considering the following.

Talk about being in denial, the Spanish authorities have stepped even further into cloud cuckoo land. Apparently, Spanish authorities suggest that they need just E40bn to recap their banks, as opposed to the E100bn, which the EZ has provisionally allocated and the E60bn approx which they had previously estimated. You will recall, that bad loans at Spanish banks have risen to a 15 month high of 10.7% in September, from 10.52% in August, according to data released by the Bank of Spain yesterday. The real reason for the lower alleged capital required is that Spain is worried that the greater the funds required, the higher their debt to GDP. However, the lack of funding for Spanish banks will mean that the economy will, in effect, continue to decline. By way of comparison, Southern Ireland, with a population of 4.6mn people, has had to inject E64bn into its banks, about 40% of its GDP. Spain’s population is 10 times larger at 47.2mn people. In addition, Spain is in recession (and will be next year), whereas Ireland has positive growth this year and is expected to do so next year, as well. Spanish investment into housing was much, much greater and the country has an unemployment rate of over 25%, nearly double that of Ireland. Irish property prices are over 50% lower than the peak – Spain claims that property prices are just around 30% lower. I can go on and on and Come on Mr Rajoy, do yourself a favour and get real The only good news for Spain is that it looks as if the secessionists in government in Catalonia are rethinking, though I would have thought that the public will still vote for independence; The US home builders index, the NAHB Market Index, rose to 46 in November, the highest since May 2006 and much higher than the 41 expected and 41 in October. US October existing home sales came in at an annual pace of 4.79mn, as opposed to 4.74mn expected and a revised 4.69mn in September. Home sales rose by +2.1% (+10.9% Y/Y) as opposed to a decline of -0.2% expected and a downwardly revised -2.9% in September. The median price of an existing home rose by +11.1%. Inventories declined to 2.14mn homes, down from 2.17mn homes in September and are 21.9% lower Y/Y. The numbers could well have been better, as they were affected by hurricane Sandy and next months numbers will also reflect the impact of the hurricane; European markets closed over 2.5%+ higher today. The Euro has crept up above US$1.28. US markets are about +1.5% higher. I’ll remain on the sidelines. Thought I’d send this out given the EZ proposed fudge (sorry “deal”) re Greece.

Source: |

| Foreign Holders of US Treasuries Posted: 19 Nov 2012 11:30 AM PST Treasuries' Foreign Buying Doubles China's $123 Billion Cut

Bloomberg Briefs notes that “Belgium, Luxembourg, Russia, Switzerland, Brazil, Taiwan and Hong Kong boosted their holdings of U.S. government securities by a collective $264.8 billion since the last debt ceiling debate ended in August 2011.” These purchases “more than made up for the decline in Treasuries owned by China,” down $123 billion to $1.156 trillion. One note about the chart above — I don’t see Japan, who is a huge holder as well of US treasuries.

Source: |

| Home Sales Remain Bright Spot in Economy Posted: 19 Nov 2012 09:30 AM PST click for giant graphic

The NAR reported that Existing Home Sales rose 2.1% in October, better than 2011 and 2010, but still below the tax credit driven activity in 2009. The key difference between 2012 and the prior two years has been how far the Fed has driven rates — about 3.375% for a 30 year fixed mortgage. We continue to see Distressed homes (foreclosures and short sales) below where they were prior to the voluntary foreclosure abatements — they are about 24% of October sales versus high 30% in years gone by. The NAR estimates these foreclosures sold for an average of 20% less than “market value,” but I have no idea what their basis of claiming that is. How does the NAR “know” a distressed house goes for 20% off market value — what actually is market value, and how do they assess that measure? I will see if I can dig up their methodology. The other details of the housing data were fairly decent: They were 10.9% above October 2011. The national median existing-home price was $178,600 in October, up 11.1% year-over-year, the eighth consecutive monthly year-over-year increases. Inventory also fell to 2.14 million existing homes available for sale, a 5.4-month supply. The initial monthly data continues to be a bit optimistic — September EHS were revised downwards. All-cash sales were 29% of all transactions — the combination of private equity investors, overseas buyers and high end homes being the drivers of this stat.

Sources: |

| Existing home sales and builder sentiment Posted: 19 Nov 2012 08:30 AM PST Existing Home Sales in Oct totaled 4.79mm, 50k more than expected but Sept was revised down by 60k to 4.69mm. The Oct annualized run rate is the 2nd highest (Aug at 4.83 was highest) since the tax credit influenced months in Apr and May ’10. Sales were seen for both single family and condos/co-ops and months supply fell to 5.4 from 5.6 as the absolute amount of homes for sale fell by 30k. This inventory to sales ratio is the lowest since Feb ’06 and is the main driver for the 11.1% y/o/y price increase to $178,600 but that is still below the high of ’12 of $188,800. Distressed sales made up 24% of the total, unchanged with Sept but down from 28% in Oct ’11. We are seeing a continued increase in the amount of investor buying which is helping to boost sales. Investors, who mostly in turn rent them out, made up 20% of sales vs 18% in Sept and 18% in Oct ’11. Bottom line, housing sales continue to improve, albeit it off a very depressed level. Single family home sales are just back to where they were in Dec 1997 and remain below the 20 yr average of 4.41mm annualized. The runway is thus long for improvement but the recovery will be in fits and starts. The housing data in the next few months will certainly reflect the negative impact of the hurricane Separately, home builder sentiment gained 5 pts to 46, just shy of the breakeven between growth and contraction. It’s the best level since May ’06 and was mostly led by the Present situation component which was up 8 pts to 49. The Future outlook rose 2 pts to 53 but Prospective Buyers Traffic was flat at 35. The NAHB is citing the shrinkage of inventories of foreclosed and distressed properties in markets across the country as the catalyst for the new home optimism. The caveat to the recovery remains the same, “difficult appraisals and tight lending conditions for builders and buyers remain limiting factors.” |

| Much better markets on hope of a solution of the US fiscal cliff Posted: 19 Nov 2012 07:30 AM PST Reuters reports that the recent (Yomuri) poll reveals that the LDP party has the support of 25% of the Japanese population, whilst 13% would vote for the DPJ, the current administration. However, 43% of the Japanese public remain undecided !!!!. The head of the LDP party has stated that he would force the BoJ to buy construction bonds to reverse the impact of deflation – yet more building projects which Japan does not need. The current PM, Mr Noda, warns of the risks inherent in interfering with BoJ policy. In addition, he wants to deal more constructively with China, whereas Mr Abe is likely to push for a more aggressive stance in dealings with China. The BoJ meeting concludes tomorrow; Chinese new home prices rose in 35 out of 70 major cities in October, up from 31 in September. The Chinese real estate market seems to have stabilised;

Spanish bank bad loans have risen to E182.2bn in September, some 10.7% of assets, as compared with 10.52% in August, according the the Bank of Spain; Italian September industrial orders (seasonally adjusted) declined by -4.0% M/M (-12.8% Y/Y), much worse than the -1.0% expected and +0.7% M/M in August. Recently, Italian economic data has stabilised/improved, but this number is a wake up call. It also suggests that data from other EZ countries will be awful; The most recent polling data suggests that 56% of UK voters want to exit the EU. About 68% of Conservatives want to leave, as opposed to 24% who want to remain in. Interestingly, 44% of Labour supporters want out, against 39% who wish to remain in. Even the Liberal Democrats (the most pro EU party and in coalition with the Conservatives) are increasingly opposed to membership of the EU – some 39% would probably or definitely wish to leave, whilst 47% want to remain in. The only party whose single policy is to leave the EU, the UKIP party, has the support of 10% of the UK population, higher than the Liberal Democrats, whose rating has collapsed to just 8%. Interestingly, Ed Milliband, the leader of the Labour party promised that his party would adopt a “hard headed” approach to the EU, calling for a cut of the next 7 year EU budget, which is to be discussed by EU heads of State this coming Thursday. The UK PM cannot agree to any deal, other than a cut in its budget, given the recent (OK, non binding) Parliamentary vote. Its going to get interesting. The EU is said to be working on plans to agree a budget without the UK – unlikely to work. As most of you know, I have always been opposed to a politicised EU and the Euro – the EU was supposed to be a free trade zone. I have not changed my mind – indeed, recent events have just reinforced my views. The EU remains a basket case and is becoming (has become?) the pariah of the world, with very little, at present, to suggest that it will get its act together. Even though I expect a change in EZ policy – the current policy of pushing austerity at the expense of all else, is way past its sell by date and will likely/certainly? change in 2013 – the EU remains, functionally, a disaster zone, as all can see. I recently wrote an article for MarketWatch on precisely this point – I can send you a copy if you wish; The Economist’s front cover is a picture of baguettes held together with a French Tricolor with a lighted fuse. Pretty graphic stuff. However, unfortunately, a pretty accurate description of where France is at present. How does France gets out of its self inflicted mess, particularly under President Hollande – the French remain in denial and opposed to fiscal, leading to a political union, within the EZ – the key German plan. Germany, increasingly, is becoming more assertive whilst ignoring France and relations between the two leaders are frosty, to say the least. In the past, France and Germany have been the leaders of the EU/EZ, with the French, effectively in political control – how times change. President Hollande’s approval rating has declined to just 41%, a new low, with the French PM down 6 points to 43%; Ireland has been the poster child of the EZ, whereas all the other countries have singularly failed to achieve their targets. However, Ireland has not benefited at all. Portugal has had its budget deficit targets raised. Greece, well we all know about Greece. Spain will not meet its targets and remains in denial. However, the EU Commissioner Mr Rehn acknowledged that Spain will not meet its budget targets, which he has accepted, though on the basis that Spain sticks to their “alleged” structural reform programme – I emphasize “alleged”. Italy, well recent economic data suggests some kind of stabilisation of their economy, though the Italians will not make their numbers either and, in addition, they face a general election in the 1st Q next year and today’s industrial orders number (see above) was truly awful. However, the Irish have been granted very little, in spite of meeting all that has been required of them. I spoke at the recent annual conference in Ireland (Kilkenonomics) arranged by David McWilliams, one of the best economists in Ireland and, quite frankly, elsewhere. The main theme of my presentations covered exactly this point – indeed, I suggested that the Irish policy of playing nice was the wrong strategy and Ireland needed to press much harder to extract a better deal from the EZ. I wonder whether they will – the Irish population are getting fed up of continued austerity. Better for the EZ to help the poster child than to see it turn tail – where will the EZ be then. The EZ needs to set up a carrot and stick approach, if they have any hope of succeeding – the current (German inspired) policy of wielding the cane only, is well past being credible; The FT reports that US corporate tax breaks worth more than US$150bn over the next 10 years could be closed. Many chief executives say that they would be willing to give up certain tax breaks in return for a lower tax rate – currently 35%, which is one of the highest rate in DM’s. Last Friday, both sides reported that a deal in respect of the fiscal cliff will be done, resulting in US markets rallying. Whilst I expect some compromise deal to be agreed at or maybe (more likely?) after the 1st January deadline, I’m not at all sure its going to be that easy. Sentiment, having been overly bearish has now turned – overly bullish?;

There are reports that BP is planning a share buy back – to provide some protection against the threat of a take over?. BP has settled potential criminal charges with the US DoJ , but a number of civil suits remain – a share buy back in those circumstances?. The company has been pretty much a disaster in recent years (the shares are some 35% lower since the oil spill in the gulf of Mexico), but some of the uncertainty has been cleared. For full disclosure purposes, I’m long BP;

Outlook Asian markets rose, though China and India are barely higher. European markets are much stronger, some 1.5%+ higher (the DAX is nearly +2.0% higher), following anticipation that the fiscal cliff will be settled. US futures suggest a higher open – over +0.75%. The Euro, well its higher,currently US$1.2770. Gold is trading around US$1728, with January Brent at 110.50.

I had thought that markets were oversold and expected a pick up. The better news from the US on Friday (relating to a possible agreement on the fiscal cliff) has resulted in markets rising materially. The energy and financial stocks I picked up on Friday are certainly performing well – between 3.0% to 5.5%% higher at present. However, the gloom over the fiscal cliff, in particular, has turned around too quickly. I was thinking of adding to those positions, but will back off. Volumes are dreadful. The EZ finance ministers meet tomorrow re Greece. Analysts expect a deal. Personally, whilst I acknowledge that the German’s are pressing for a deal and will never underestimate Mrs Merkel, I will wait and see.

A number of analysts keep plugging EM’s and the BRIC’s in particular – personally, I’m not at all convinced. Yes, a deal on the US fiscal cliff and the EZ on Greece (possibly Spain) will help, but EM’s have a tough road ahead of them. The US/Yen has come off its highs. However, I see no reason to close my short Yen (against the US$) position. Kiron Sarkar 19th November 2012 |

| Posted: 19 Nov 2012 06:50 AM PST My morning reads:

What are you reading?

CapEx Investment Falls Off a Cliff

|

| “You can’t always get what you want…” Posted: 19 Nov 2012 06:01 AM PST “You can’t always get what you want, but if you try sometimes, you just might find you get what you need.” I couldn’t help envisioning Nancy Pelosi, Harry Reid, John Boehner and Mitch McConnell on a park bench singing this song together over the weekend as they negotiate a tax and spending deal and ahead of the Rolling Stones 50th anniversary tour. I repeat my belief that a deal that doesn’t face healthcare spending head on and also raises taxes of substance with economic growth mediocre is not a good deal. This said, the markets will celebrate any deal in the short term but will likely deal with the economic consequences in 2013 (outside of capital gains induced selling in 2012). In Asia, the Nikkei rallied another 1.4% and is up 5.6% in the past three trading days as a new government may take hold on Dec 16th with a mandate to print a lot of yen. China said 35 cities of 70 saw home price gains in Oct vs 31 in Sept. In Europe, Spain’s Rajoy remains defiant against calls for a bailout as he said ‘the worst is over’ and the Spanish economy will be ‘better in 2013 than 2012.’ The Spanish 2 yr yield is near a two month high. European Finance Ministers meet tomorrow to try to hammer out a deal to come up with another 30b euros to bridge Greece over for the next few weeks, on top of what’s already been pledged to them. Expectations of a deal have the Greek stock market up 2.5% and the Greek 10 yr note is up 7 days in a row. On the markets response to the Israeli/Hamas confrontation, the Tel Aviv stock market is up .8% today after a 1.4% rally yesterday and has gotten back everything it lost last week. |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment