The Big Picture |

- Ending the Silence on Climate Change

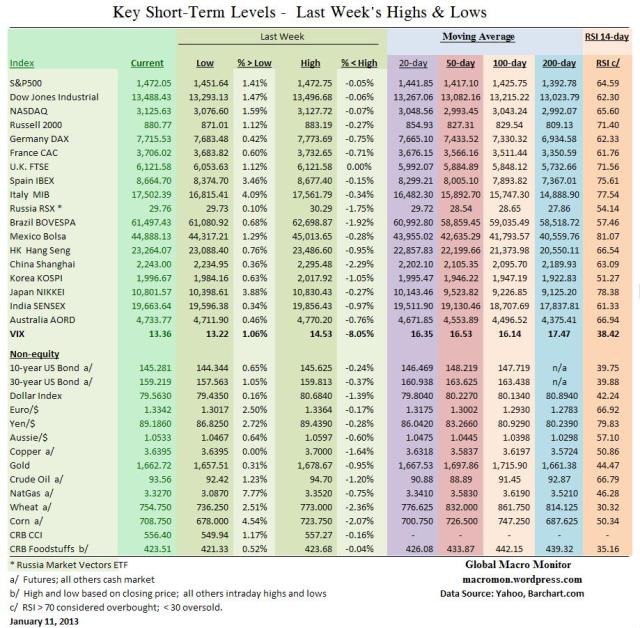

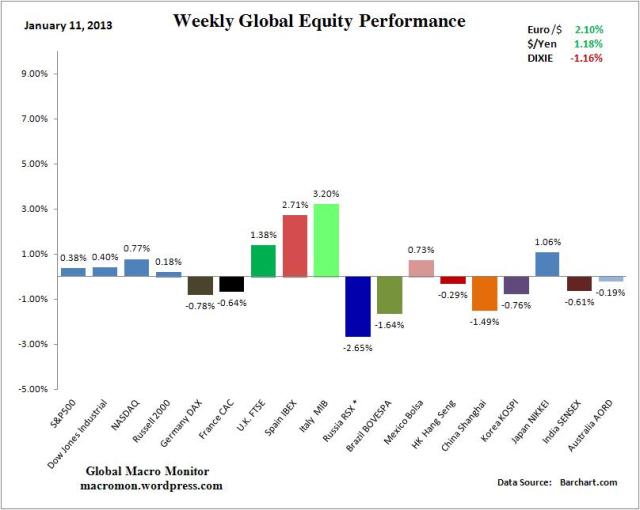

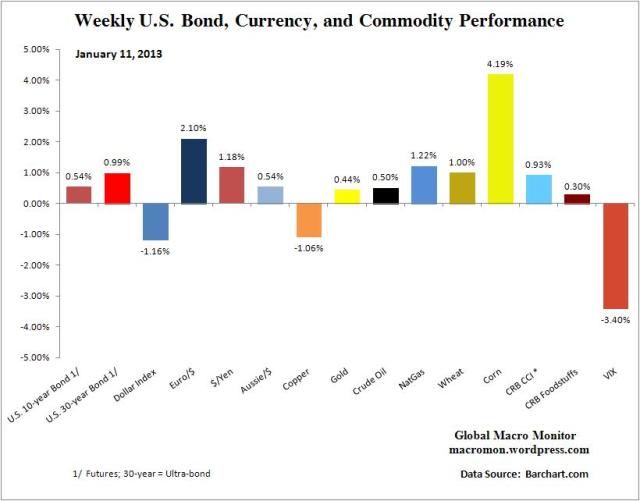

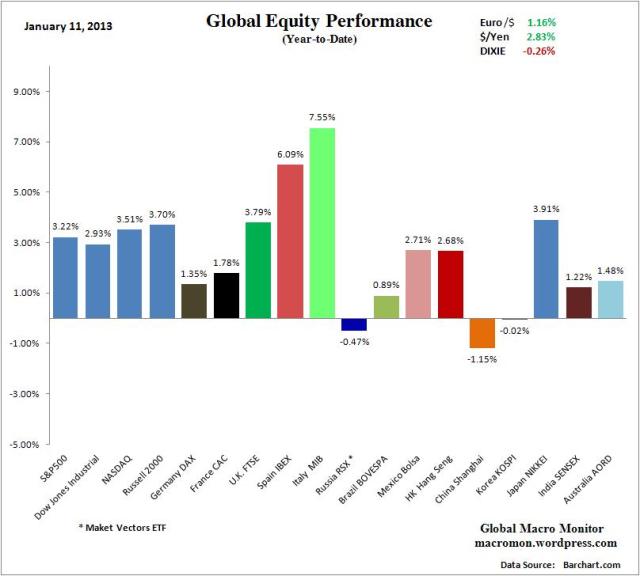

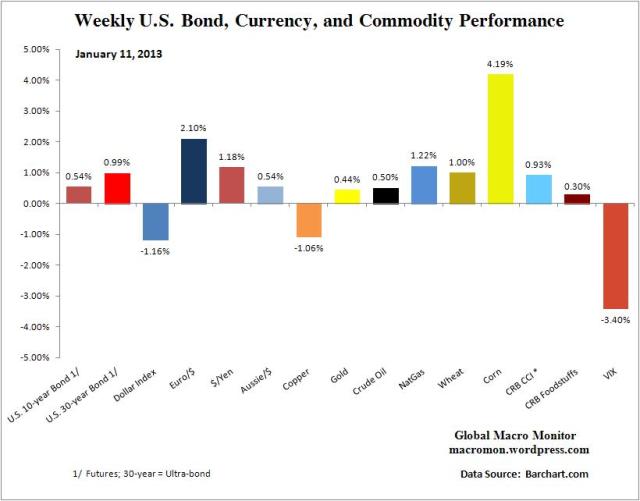

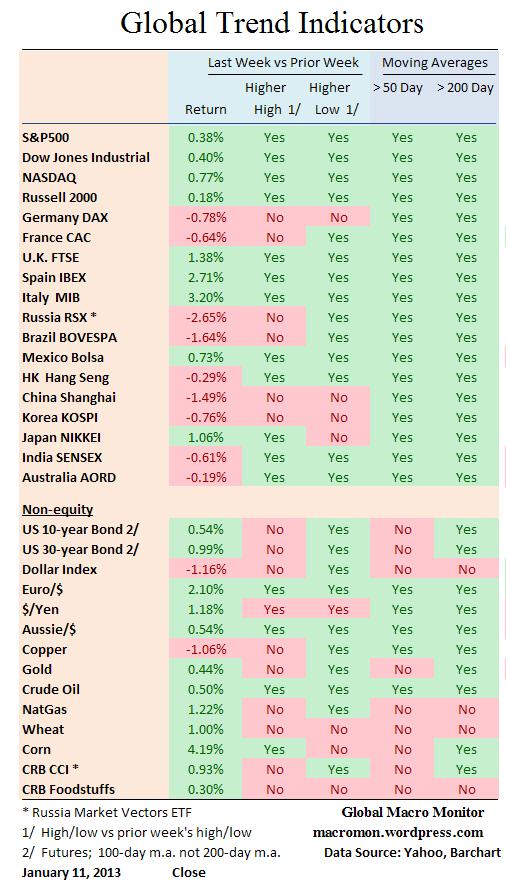

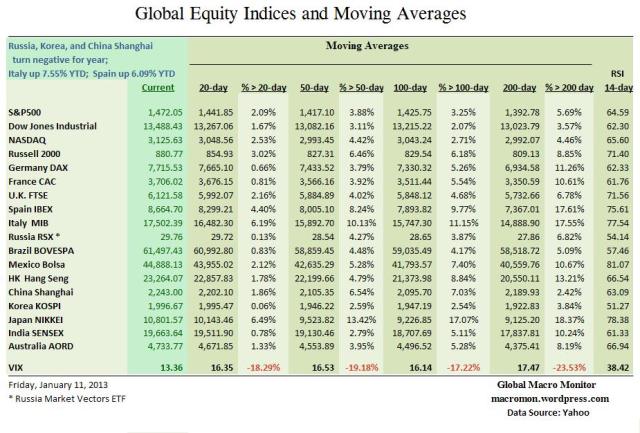

- Week in Review/Global Trend Indicators January 11, 2012

- Thought Provoking Quotes About Life

- 10 Significant Trends in Finance

- .

- Saudi Arabia Cuts Oil Production

- The Rational Optimist: How Prosperity Evolves

- Gandalf Problem Solving Flowchart

- 10 Sunday Reads

| Ending the Silence on Climate Change Posted: 13 Jan 2013 03:00 PM PST Climate change communication expert Anthony Leiserowitz explains why climate change gets the silent treatment, and what we should do about it. January 4, 2013 |

| Week in Review/Global Trend Indicators January 11, 2012 Posted: 13 Jan 2013 02:30 PM PST |

| Thought Provoking Quotes About Life Posted: 13 Jan 2013 12:00 PM PST 34 thought provoking & inspiring quotes about life

|

| 10 Significant Trends in Finance Posted: 13 Jan 2013 08:00 AM PST

> My Sunday Washington Post Business Section column is out, and its a doozy: Rather than do the usual forecasts for the new year silliness, I thought it might be interesting to look instead at the major trends driving the world of finance. Its called 10 trends to watch in finance for 2013, and the concept behind it is that most people are so busy guessing what might happen in the future, they forget to understand what is happening right now. My position is understanding precisely what just occurred is much more important than guessing about the future:

The rest of the column articulates those 10 trends. (I think this may be my first front-page-of-the-business-section column!) There are a couple of charts at the Post I pulled together from Bianco research & FRED, but the artwork is really kinda cool: click for larger graphic > Source: |

| Posted: 13 Jan 2013 07:45 AM PST |

| Saudi Arabia Cuts Oil Production Posted: 13 Jan 2013 06:00 AM PST The Japanese PM, Mr Abe, has repeated on Japanese TV this weekend that he expects the BoJ to confirm a policy to raise inflation to 2.0%, in the medium term. Given his continuing statements, a rejection of such a policy will be a major blow. However, recent comments by the current BoJ governor suggest that he will accede to such requests. In addition, Mr Abe has stated that he will appoint a "bold leader", diplomatic terminology for someone who will follow his instructions, as head of the BoJ, when the present governor, Mr Shirakawa retires in April this year. Looks like the Yen will weaken even further; China is sending aircraft to counteract Japanese aircraft which have been intercepting flights by Chinese aircraft over the disputed islands in the South China seas. This issue, I will continue to repeat, has danger written all over it. Whilst a deliberate military act by either side is unlikely, an accidental confrontation becomes increasingly possible. Watch this issue extremely carefully. Japanese PM, Mr Abe has allegedly contacted NATO, to seek assistance to counter the Chinese naval presence in the South China seas – clearly NATO will not intervene, but other countries in the region are taking this matter seriously; Pollution in major cities in China is increasingly becoming a major problem. Residents in Beijing have been advised to stay indoors as air pollution hit record levels. The cost of dealing with pollution in China, not just air pollution, but also poisoned rivers etc, are going to be crippling in coming years. In the medium to longer term, GDP is China will decline closer to 4% to 5.0%, quite possibly even lower; Goldman's, UBS and ANZ have questioned the accuracy of the recent Chinese export data, which reported a rise of +14.1% Y/Y in exports. The increase doesn’t match data of goods movements through ports and imports from trading partners according to UBS. Goldman's points to discrepancies for overseas orders in a manufacturing index. Well finally – a number of us have known for quite some time that Chinese data was, how shall I put it, "suspect". (Source Bloomberg); Leaks, obviously from Saudi Arabian officials, state that the country has cut its oil production to just 9.025mn bpd in December, down from 9.49mn in November and the lowest since May 2011. The 30 year production high was 10.1mn bpd last June, ie production has been cut by 1mn bpd from its high. The cut in production resulted in Brent rising to US$113 last Thursday, through March Brent declined to around US$110 by the close of play on Friday. Saudi Arabia is responding to higher US, Canadian and Iraqi production. US production rose by approx 780k bpd in 2012 and is set to rise by 890k bpd this year. Iraqi production is expected to rise to 3.4mn bpd in 2013, up from 2.9mn bpd last year. Whilst well below its potential production levels, Iraq has faced massive logistical and political (with the Kurds) problems, which look set to continue. However, if they manage to resolve them (highly unlikely), Iraq production could well double in a few years. For their own part, the Kurds are shipping oil directly through Turkey, though as it is by truck, the amounts are relatively small – around 20k bpd. It looks as if the Saudi's are anticipating increased supply and are acting ahead of a potential price decline – unlikely to work; Greek lawmakers have passed legislation to increase taxes by E2.3bn and to stop tax evasion. The introduction of such legislation was a prerequisite for Greece to get further aid from the EZ and the IMF; Mr Draghi's more upbeat tone at the last ECB press conference was in stark contrast with previous meetings which were dogged by crisis fighting measures. Analysts have been quick to suggest that ECB interest rates will not be cut "for the foreseeable future". Hmmmm .Mr Draghi stated that signs of stabilisation were evident in "several" growth measures, as opposed to just "some" growth measures he referred to in December. He did acknowledge that recovery would come in H2 this year, a view I agree with, if only as Y/Y comparisons become easier. Importantly, Mr Draghi stated that ECB members had voted unanimously to keep interest rates on hold, which has sent the Euro soaring against the US$. Last month, the ECB admitted that the call to keep interest rates on hold, rather than cut them by 25 bps, was close. Another positive sign for the EZ was the announcement last Thursday that no banks had made use of its emergency overnight marginal lending facility, the 1st time since August 2011 and a sign that banks are facing less stress and,in addition, that interbank lending is rising. At the press conference, Mr Draghi emphasised the increase in deposits in the peripheral EZ banks, increasing flows of capital into the EZ, a declining ECB balance sheet and a reduction in Target2 imbalances – clearly all positive developments. Mr Draghi ventured that the EZ was back to normal – Hmmmmm. There remains the peripheral EZ countries Mr Draghi and Cyprus looks like an upcoming problem. However, as you know, I believe, the EZ will stabilise in H1 and, indeed, grow in H2. Current forecasts for a decline in GDP of some -0.3% for the current year appear too pessimistic in my humble view – I have forecast positive growth for the EZ this year – quite possibly +0.25% to +0.5%. German GDP forecasts of just +0.3% by the Bundesbank look way, way too pessimistic – I believe Germany will grow by +1.25%, indeed most likely higher. Yes, there are huge risks as I set out in my 2013 forecast, but for the moment the EZ outlook is improving – famous last words !!!!; The US has privately briefed UK journalists that the"special relationship" between the US and the UK would end if the UK exited the EU. US officials state that they do not want to interfere with domestic UK politics. Yeah right. The reality is that the EU, ex the UK, will move further away from the US, in particular on foreign policy and defence related matters. As a result, the UK remaining in the EU will help the US, as the UK has always sided with the US. For full disclosure purposes, I have always been staunchly opposed to the UK remaining in the EU – it has proved to be an unmitigated disaster, in my opinion. The allegation that the UK can change the EU is a sham – the other EU members ignore and/or do not follow the UK's agenda. However, no matter how powerful, the US will need friends in the future – it will not "dump" the UK, who has proved to be a staunchly reliable partner. The special relationship is a nonsense. The US will pursue its interests, as it needs to and, increasingly, so will the UK. The UK PM, Mr Cameron is set to announce his plans for a referendum on continued UK membership of the EU, which is the reason for the US intervention. Germany is also rethinking its relationship to the UK. With its "special relationship" with France likely to end in an acrimonious divorce, Germany needs a strong and credible partner in Europe and the UK is the only possible candidate. A relationship between the UK and Germany makes sense given that the countries are the financial and industrial powerhouses in Europe. The German's are likely to become more friendly towards the UK. However, the German's are not keen on the financial services sector – indeed, they deeply mistrust it. Allegations of sanctions by the EU against the UK, if the UK leaves the EU are silly. The UK, imports far more from the EU – ie it will hurt the EU if they impose sanctions and/or withdraw trade deals. In terms of the financial services industry, the UK, free of EU anti financial sector legislation, will act as a spur to the industry. Furthermore, the UK is an international financial centre, not just an European financial centre. However, unfortunately, the bottom line is that the UK will not exit the EU, as my very well informed friends advise me; The US November trade deficit of US$48.7bn, the largest since April, does suggest that the US economy is growing strongly. Indeed, the real deficit (adjusting for prices) rose to US$52bn, from US$46bn previously. In addition, the increased deficit will reduce Q4 GDP by as much as -0.75%. Exports were +1.0% higher, though imports surged by +3.8%. Imports of consumer goods rose by +11.2%. The numbers could have been distorted by the effects of Hurricane Sandy, though the the strength of the import numbers suggest that this is only a partial explanation. I had expected US Q4 GDP to come in at +1.75%, though these trade numbers suggest that Q4 GDP will be around +1.25% to +1.50% – other data has been more positive, which partially counteracts this negative development; The US budget deficit contracted to just US$260mn, yep that's US$260mn, no typo, the lowest December deficit in 5 years and lower than the US$1bn forecast. The deficit in December 2011, was US$86bn. A great deal of the revenue generated in December was due to early payments of bonuses and dividends to avoid the tax increases in January. As a result, subsequent budget deficits will be higher than expected, though the 2.0% payroll tax, which starts on 1st January 2013 will compensate somewhat; Investors seem to be moving out of bonds and into equities. No surprise. Net inflows into equity funds amounted to US$22.2bn in the week to 9th January, according to EPFR, the highest since September 2007. Flows into US equity funds amounted to US$10.4bn, with EM's receiving US$7.4bn. European equity funds were the laggard, increasing by just US$1bn;

Outlook The fund flows into equities, both in DM's and EM's, whilst marginally positive into bond funds, except for inflows into EM bond funds which are rising, suggest to little old me that this rally has some legs. In addition, next Friday's Chinese GDP number should be positive – fears over a rising CPI last week were overdone – indeed, the CPI increase was predictable, due to the increase in fresh food prices in December, which were affected by the severe winter. The BoJ announces its policy decision on the 22nd January – likely to agree to a 2.0% inflation target, though with no set date – once again, equity positive In addition, an unemployment target could well be introduced, a la FED. Oil may well decline – positive for markets. However, the Citi US Economic Surprise Index is threatening to turn negative – not a good sign. Markets are overbought and I will look to reduce my holdings, most probably later this month. The exit out of bonds into equities has begun. I continue to be bearish of bond markets, especially DM bond markets. In particular, I will look to short US, German, Japanese and UK bonds towards the end of the month – Japanese probably earlier. I will (hopefully) wait for a likely equity market sell off, with a corresponding bond rally, before acting. The Euro looks set to rise to US$1.35, possibly somewhat higher. US GDP, to be released by the end of the month, looks like disappointing, given the larger US trade deficit, which could be Euro supportive. I shorted the Yen against the Euro, rather than against the US$. However, over US$1.35/US$1.36, I will look to short the Euro – the current Euro rise looks way overdone, in my humble opinion. Negative GDP data (Q4 may be -0.3% Q/Q lower) from Germany could negatively impact the Euro next week, it must be said. My friends are bullish on Gold. With more "stability" around and weaker inflation, especially in DM's and my expectations of a stronger US$ in coming months, I have to say, I do not see the attractions. However, I have never really understood the attractions of gold I must admit. There are some signs that oil prices (Brent) may decline due to increases in supply, as discussed above – great news if it happens, though bad news for countries such as Saudi Arabia, Russia etc. A decline in oil prices will reduce inflation, in particular, in EM's, as their inflation basket is more heavily weighted towards energy, though DM's will also benefit. There are some forecasts for Brent to decline below US$90 in 2014. That is really bad news for Russia, for example, who need over US$100 Brent to balance their budget. Going to be interesting. Have a great weekend. Kiron Sarkar 13th January 2013 |

| The Rational Optimist: How Prosperity Evolves Posted: 13 Jan 2013 05:30 AM PST Matt Ridley – Zeitgeist 2012 Beyond the Rational Optimist |

| Gandalf Problem Solving Flowchart Posted: 13 Jan 2013 05:00 AM PST |

| Posted: 13 Jan 2013 04:00 AM PST These are your reads to begin your Sunday morning.

How about some Dim Sum brunch today?

Since 2011, Three-Quarters Of Deficit Reduction Has Been Via Spending Cuts |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment