The Big Picture |

- Discuss: Health Care Spending by Age and Country

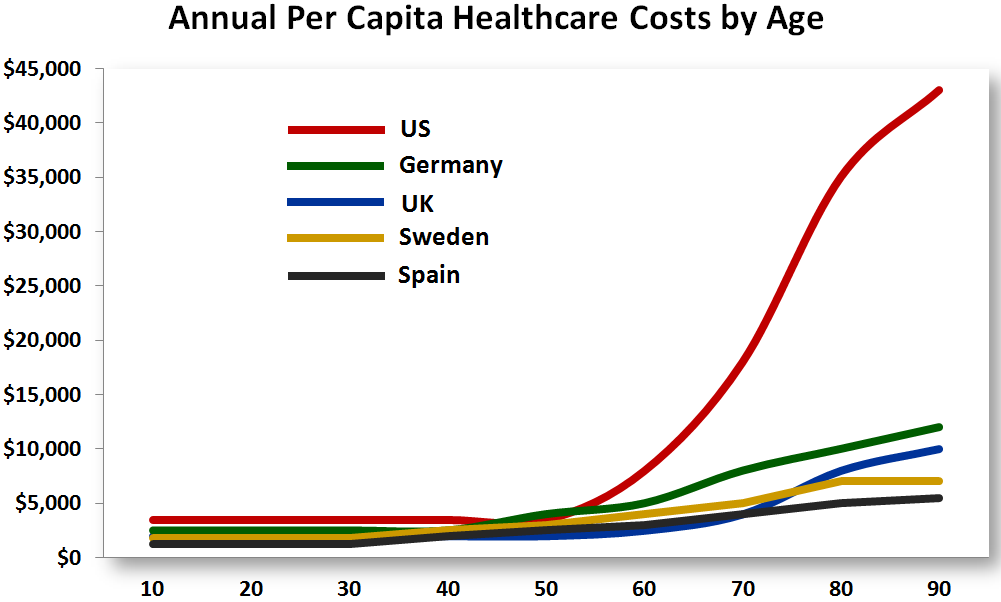

- 10 Tuesday PM Reads

- The Album

- Can Treasury Issue Coinage to Meet Congress’ Spending? (Yes)

- Why Are US Dividends So Much Lower Than the Rest of World?

- Ritholtz on Next Treasury Secretary, Hedge Fund Managers

- Saturn As Seen From CICLOPS

- 10 Tuesday AM Reads

- Chinese to restrict/limit its shadow banking market?

- Interview: Felix Zulauf

- Januarys in the Stock Market

- Belkin: Top 10 Reasons to be Bullish in 2013

| Discuss: Health Care Spending by Age and Country Posted: 08 Jan 2013 04:30 PM PST

One of these things, is not like the other . . . There are more charts at Forbes |

| Posted: 08 Jan 2013 01:30 PM PST My afternoon train reading:

What are you reading?

About That Large Drop in the VIX… |

| Posted: 08 Jan 2013 12:00 PM PST 1. Is a revenue producing item for the label, it’s how they get their money back. 2. Is a trigger for publicity. 3. Is too long. On vinyl, you were loath to put more than forty minutes of music on a side. The most classic of double albums, and the cliche is there’s not one that could not be a single, fit on one CD no problem. 4. On vinyl there were four key tracks. Openers and closers on both sides. The CD is incomprehensible. You don’t know what songs you should check out, so overwhelmed, you ignore everything but the hit. 5. Had its breakthrough with “Sgt. Pepper.” If you’ve got a rock opera or something to say over ten or twelve tracks, be my guest, create an album. But I can’t even remember the last cohesive album statement that was any good. This is a straw man. 6. Mainstream publicity is the weakest of them all. Because the mainstream constantly needs a new stream of info. And your product gets brought down by the crap they feature the following day or week. You want word of mouth publicity. And word of mouth publicity doesn’t work on albums, but tracks. You want to go viral. This depends on a cut, not an album. The days of hearing a song on the radio and buying the album so you could hear that and more are done. There’s not a single in existence that you can’t hear alone on YouTube. 7. CDs at gigs are souvenirs. People don’t buy them to listen. 8. The fact that your hard core listens to your album is fine if you’re satiated with only reaching your hard core. But if you find a musician who’s satisfied with the size of his audience, he’s not a musician. 9. Network news was killed by cable news which was killed by the Net. People want the latest on demand. And you’re dropping an album every year or so? And the radio is eking out the music track by track, if you’re lucky? In today’s world you want to be in the public eye constantly. I’m not saying you should make less music, just that you shouldn’t see it as an album. 10. With the cost of production and distribution so low, it’s time to experiment, which is anathema to the dying majors. If you’re a metal band with country roots, cut a country song, why not? The album release cycle was a prison, you’ve been unchained, why do you want to stay inside? 11. The audience has no time. There are too many stimuli. You’re looking for the one track that can set off the explosion. And you never know what track that will be, which is why you must keep creating. Otherwise you can make an album that stiffs and your career can be over. 12. The audience is looking for great things. If you create something great, there’s a plethora of people ready to spread the word. This is more powerful than any newspaper or radio station. But your track must be great, otherwise virality stops cold. You can buy a few YouTube views but you can’t fake virality. The old days of paying radio to play your middling song into a hit are dead. 13. Labels don’t want to abandon the album because it changes their revenue model. You’ve got to pay for the exec’s car, his kids’ private school, his vacation… He likes the old way, he’s gonna fight for the old way. 14. The acts listened to albums so they want to cut albums. Not realizing the way you become a hero today is to do it the opposite or a new way from your heroes. You don’t want to do what’s already been done. 15. The album will not die overnight. But it’s dying as we speak, look at track sales. 16. Sales are miniscule compared to listens. We’re going to a listen world, i.e. streaming. It’s not whether you sold it, but whether people listened to it! 17. You’re the victim of too many bad albums before you. 18. There will always be a demand for superstar albums. But are you a superstar? Furthermore, there are fewer stars than ever before. People don’t have time for more. 19. You want a career. Careers live in the minds of listeners, not gatekeepers. The listener wants nothing more than new music. You don’t want to go on a date once a year with the love of your life, but constantly. And you don’t want to go to the same places and do the same things. 20. Albums were originally collections of 78s. Don’t let the format dictate the music. That begat Napster, when there were too many overpriced CDs with only one good track. You’ve been freed. Then again, it’s a wilderness and you don’t know where to go. 21. Think outside the box. Don’t do it like everybody else does. Make a twenty minute single. Or a two minute one. Issue a challenge to yourself or your audience. This stimulates and creates heat. And what you want is heat. 22. Albums ruled in the classic rock era because of scarcity. You couldn’t hear much and you couldn’t afford much. You played every cut because it was all you had. It’s kind of like dating. Once upon a time you were limited to the people you bumped into physically, now your universe is…the universe! You can even hook up with Russians online! Tell someone to date someone undesirable while they’re hanging out at the Playboy Mansion. That’s kind of like telling someone to listen to your crap when they can listen to the best music made, which is just as free online. 23. Artists need to be leaders, not followers. In this case, the audience wants singles and it’s the artists who are locked in the past. Artists need to get in front of the audience, they need to lead, to titillate and entrance!

~~~ –

|

| Can Treasury Issue Coinage to Meet Congress’ Spending? (Yes) Posted: 08 Jan 2013 11:30 AM PST Steve Randy Waldman writes about finance and economics at interfluidity.com ~~~ Rebranding the "trillion-dollar coin"So, hopefully you know about the whole #MintTheCoin thing. If you need to get up to speed, Ryan Cooper has a roundup of recent commentary, and the indefatigable Joe Wiesenthal has fanned a white-hot social-media flame over the idea. For a longer-term history, see Joe Firestone, and note that all of this began with remarkable blog commenter beowulf. See also Josh Barro, Paul Krugman, Dylan Matthews, Michael Sankowski, Randy Wray among many, many others. Also, there's a White House petition. Basically, an obscure bit of law gives the Secretary of the Treasury carte blanche to create US currency of any denomination, as long as the money is made of platinum. So, if Congress won't raise the debt ceiling, the Treasury could strike a one-trillion-dollar platinum coin, deposit the currency in its account at the Fed, and use the funds to pay the people's bills for a while. Kevin Drum and John Carney argue (not persuasively) that courts might find this illegal or even unconstitutional, despite clear textual authorization. For an executive that claims the 2001 "authorization to use military force" permits it to covertly assassinate anyone anywhere and no one has standing to sue, making the case for platinum coins should be easy-peasy. Plus (like assassination, I suppose), money really can't be undone. What's the remedy if a court invalidates coinage after the fact? The US government would no doubt be asked to make holders of the invalidated currency whole, creating ipso facto a form of government obligation not constrained by the debt ceiling. I think Heidi Moore and Adam Ozimek are more honest in their objection. The problem with having the US Mint produce a single, one-trillion-dollar platinum coin so Timothy Geithner can deposit it at the Federal Reserve is that it seems plain ridiculous. Yes, much of the commentariat believes that the debt ceiling itself is ridiculous, but two colliding ridiculousses don't make a serious. We are all accustomed to sighing in a world-weary way over what a banana republic the US has become. But, individually and in our roles as institutional investors and foreign sovereigns, we don't actually act as if the United States is a rinky-dink bad joke with nukes. As a polity, we'd probably prefer that the US-as-banana-republic meme remain more a status marker for intellectuals than a driver of financial market behavior. Probably. The economics of "coin seigniorage" are not, in fact, rinky-dink. Having a trillion dollar coin at the Fed and a trillion dollars in reserves for the government to spend is substantively indistinguishable from having a trillion dollars in US Treasury bills at the Fed and the same level of deposits with the Federal Reserve. The benefit of the plan (depending on your politics) is that it circumvents an institutional quirk, the debt ceiling. The cost of the plan is that it would inflame US politics, and there is a slim chance that it would make Paul Krugman's "confidence fairies" suddenly become real. But note that both of these costs are matters of perception. Perception depends not only on what you do, but also on how you do it. The Treasury won't and shouldn't mint a single, one-trillion-dollar platinum coin and deposit it with the Federal Reserve. That's fun to talk about but dumb to do. It just sounds too crazy. But the Treasury might still plan for coin seigniorage. The Treasury Secretary would announce that he is obliged by law to make certain payments, but that the debt ceiling prevents him from borrowing to meet those obligations. Although current institutional practice makes the Federal Reserve the nation's primary issuer of currency, Congress in its foresight gave this power to the US Treasury as well. Following a review of the matter, the Secretary would tell us, Treasury lawyers have determined that once the capacity to make expenditures by conventional means has been exhausted, issuing currency will be the only way Treasury can reconcile its legal obligation simultaneously to make payments and respect the debt ceiling. Therefore, Treasury will reluctantly issue currency in large denominations (as it has in the past) in order to pay its bills. In practice, that would mean million-, not trillion-, dollar coins, which would be produced on an "as-needed" basis to meet the government's expenses until borrowing authority has been restored. On the same day, the Federal Reserve would announce that it is aware of the exigencies facing the Treasury, and that, in order to fulfill its legal mandate to promote stable prices, it will "sterilize" any issue of currency by the Treasury, selling assets from its own balance sheet one-for-one. The Chairman of the Federal Reserve would hold a press conference and reassure the public that he foresees no difficulty whatsoever in preventing inflation, that the Federal Reserve has the capacity to "hoover up" nearly three trillion dollars of currency and reserves at will. That would be it. There would be no farcical march by the Secretary to the central bank. The coins would actually circulate (collectors' items for billionaires!), but most of them would find their way back to the Fed via the private banking system. The net effect of the operation would be equivalent to borrowing by the Treasury: instead of paying interest directly to creditors, Treasury would forgo revenue that it otherwise would have received from the Fed, revenue the Fed would have earned on the assets it would sell to the public to sterilize the new currency. The whole thing would be a big nothingburger, except to the people who had hoped to use debt-ceiling chicken as leverage to achieve political goals. Some legal background: here's the law, the relevant bit of which—subsection (k)—was originally added in 1996 then slightly modified in 2000; here is appropriations committee report from 1996, see p. 35; and legislative discussion of the 2000 modification. Huge thanks to @d_embee and @akammer for digging up this stuff. originally published at Intefluidity |

| Why Are US Dividends So Much Lower Than the Rest of World? Posted: 08 Jan 2013 08:30 AM PST

This is a question that does not get discussed enough — Why are US dividends so much lower than the rest of the world’s ?

|

| Ritholtz on Next Treasury Secretary, Hedge Fund Managers Posted: 08 Jan 2013 08:09 AM PST Barry Ritholtz, chief executive officer of FusionIQ and author of the “Big Picture” blog, talks about potential successors to U.S. Treasury Secretary Timothy Geithner, the outlook for Microsoft Inc., and his investment strategy. He speaks with Tom Keene, Scarlet Fu and Sara Eisen on Bloomberg Television’s “Surveillance.” Ritholtz Calls Ballmer ‘Worst CEO in Technology’ |

| Posted: 08 Jan 2013 07:30 AM PST |

| Posted: 08 Jan 2013 07:00 AM PST Note that the first two reads will be taked about all day by everyone:

What are you reading?

Stock Bulls Place Bets on Earnings Growth |

| Chinese to restrict/limit its shadow banking market? Posted: 08 Jan 2013 06:15 AM PST Australia's November trade deficit rose to A$2.64bn, as compared with A$2.3bn expected and an upwardly revised A$2.44bn in October. The deficit was the widest since March 2008. Exports rose by 1.0% to A$24.7bn, whilst imports rose by 2.0% to A$27.3bn; Japanese press report that the Government will announce a stimulus plan of Y12tr (US$136bn), with the fiscal year 2013 budget to be announced by end January. The Japanese Finance Minister, Taro Aso reports that the Y44tr cap on bond issuance this year does not need to be adhered to, with expectations that it will top Y50tr. Mr Aso added today that Japan would buy ESM bonds, using its forex reserves. The size of such purchases has not been announced. The announcement has weakened the Yen against the Euro marginally. However, as the Japanese are using their forex reserves, I presume they will have to sell other currencies, to invest in ESM bonds, as Japan is facing a current account deficit; It looks as if the Japanese government and the BoJ are trying to agree on an employment goal (a la FED) as part of the BoJ's mandate; The FT suggests that Chinese authorities may limit financing by the shadow banking market. If they are right, watch out. It is estimated that the sector has been responsible for close to half of all financing (possibly more) in recent years, though accurate numbers are hard to come by. I will certainly watch this one carefully; Opinion polls show that Mr Mario Monti is trailing mainstream parties, while Berlusconi has struck an election deal with Northern League ahead of the impending elections in Italy in February. The Italian November unemployment rate came in at 11.1% M/M, slightly less than the 11.2% expected and unchanged from October; Ms. Lagarde has stated that restructuring Portugal’s debt is "out of the question" and that Portugal’s bailout programme is progressing well. Ms Lagarde may say that, but the reality is very different, in my humble view; German seasonally adjusted exports declined by -3.4% in November M/M, worse than the -0.5% decline forecast and as opposed to an increase of +0.2% in October. The decline was the steepest in more than 1 year. The trade surplus rose to E17bn, up from E15.7bn in October, with the current a/c surplus coming in at E15.3bn, as opposed to E13.2bn in October. Exports to the EZ weakened significantly. German November factory orders were -1.8% lower M/M, worse than the -1.4% expected; The ECB has found issue with collateral of Bank of France due to insufficient risk valuation discounts made on the collateral and hence Bank of France has been granted too much credit; The French November trade deficit declined to -E4.3bn, from -E4.7bn in October and -E4.8bn expected ; EZ PPI (Nov) M/M -0.3% vs Exp. 0.0% (Prev. 0.1%), Eurozone PPI (Nov) Y/Y +2.1% vs Exp. +2.4% (Prev. +2.6%). EZ November retail sales were +0.1% higher M/M (-2.6% Y/Y), though weaker than the +0.3% expected and as compared with a revised -0.7% in October. EZ November unemployment rose marginally to 11.8% in November, from 11.7% in October and in line with expectations; Eurozone Sentix indicator came in at -7 for January, measurably better than the -16.8 in December and analysts expectations of -15.The index is at the highest in 1 ½ years; BoA has agreed to pay Fannie Mae US$11.6bn in settlement of a dispute over the sale of mortgage loans to Fannie. In a separate agreement, 10 mortgage banks agreed to pay US$8.5bn in settlement of charges that the banks abused the home foreclosure process; Bloomberg reports that apartment vacancies have fallen to a 11 year low. The vacancy rate nationally has declined to just 4.5%, from 4.7% in Q3 and 5.2% a year ago. Vacancies in New York are just 2.1%, though unchanged Y/Y and the lowest nationally; Another report in Bloomberg which refers to Moody’s expectation that state and local governments will be in hiring mode this year, as their finances have improved to the best since the start of the financial crisis. Moody's expect some 220k jobs will be created by state and local governments this year. I remain positive on employment in the US; Basel III rules have been relaxed, which prompted a rally in the financial sector yesterday. Banks will now have until 2019 to meet their liquidity coverage ratios. The deal also expands the number of securities banks can use to meet their liquidity requirements. The issue of solvency remains a pressing issue; Outlook Asian markets closed weaker, with European markets up, having opened weaker. US futures suggest that markets will open lower. The Euro having started stronger is selling off and is, currently trading at US$1.3095. Gold is marginally higher at US$1652, with February Brent higher at US$112.22. I see no reason to chase these markets, as I believe that the negotiations between the Republicans and the Democrats over the spending cuts/debt ceiling will be far more contentious, than was the case over the fiscal cliff. The uncertainty caused will be market negative. Having sold out of the mining sector, I will retain my other positions for the moment, though will reduce, if markets rise in any meaningful/semi meaningful way. Kiron Sarkar 8th January 2013 |

| Posted: 08 Jan 2013 05:49 AM PST Joe Dedona, head trader at our Institutional Desk, sat down with world-renowned money manager Felix Zulauf to get his view on global markets. Felix discusses the European debt crisis, the rebound in Chinese equities, the recent Japanese election and its impact on their markets, the U.S. markets in light of our fiscal issues, and much more. ~~~ Felix Zulauf was born in 1950 in Switzerland. He started his career started in 1971 as a trader for the Swiss Bank Corporation where he mastered research and portfolio management at leading investment banks in France, Switzerland and USA. After that he worked at UBS Switzerland where between 1977 and 1988 he was the manager of UBS's global mutual funds, and a leader of the institutional portfolio management division. In 1990, he started his own hedge fund "Zulauf Asset Management," where he continues to serve as President. Mr. Zulauf is widely known for being a long-standing member of the Barron's Roundtable where every year, for the last 25 years, he shares with the world his views on investment and economic matters. Felix Zulauf is an advocate of the thesis that economies and financial markets move cyclically. This view and belief has helped him to preserve capital during difficult times. ~~~ Dedona: Looking at China, Felix, you were bearish at the start of 2012, and then very presciently called a bottom in September. Both the Shanghai Composite and Hang Sang have rallied very strongly since that call. What is your current outlook on China ? Zulauf: The new government in China wants to maintain 7-8% growth, and wants to take steps to ensure this. They may increase public spending and relax monetary policy. This won't come anywhere close to the stimulus of 2008, as China is still suffering the negative side effects. You might see a temporary improvement in economic indicators, but that's it. The real level of growth in China is probably only 3-4%. That said, there is still perhaps 20-30% upside in Chinese equities, particularly in the first half, although you won't see the sort of sustained move we saw off the 2008 low there.

Dedona: How does Japan look right now? We note you called for shorting the Yen at a Barron's conference in October – again, a very prescient call. Zulauf: Japan's economy is not doing well and still suffers from deflation. The pronounced deterioration of Japan's current account and the disappearing ability to finance her own large budget deficits are forcing some important changes. The new government in Japan, led by the LDP and Prime Minister Abe, has a 2/3 majority in parliament and can push through their own will without any problem. Abe wants some increased deficit spending, on top of a budget deficit that is already near 10% of GDP. He wants the Bank of Japan to finance a big part of it by printing new money and thereby weakening the Yen and targeting 2% inflation. If the BOJ doesn't comply, they have basically been told they will lose their independence as a central bank. The spending will increase deficits further and weaken the currency, which should improve exports. I see Dollar/Yen going to 120 within the next 2 years, and the Yen weakening decidedly against all major currencies. Dedona: So you're clearly still constructive on China and Japan … Zulauf: China's market rebound should at least last during the first half of this year. There is still another 20% to go. After a consolidation and pullback, you can buy FXI here to play it. As for Japan, I am much more bullish as nobody owns Japanese stocks. The total market cap of the market there is one quarter of what is was 23 years ago. If the currency continues to decline against all the others, there will be a tremendous lift to Japanese equities. The Nikkei has at least another 20% upside in 2013 and could do more and last longer, all in local currency terms.

|

| Posted: 08 Jan 2013 05:30 AM PST

MarketWatch.com – How special is January?

Source: Bianco Research |

| Belkin: Top 10 Reasons to be Bullish in 2013 Posted: 08 Jan 2013 04:00 AM PST It is an understatement to say Michael Belkin is somewhat skeptical of all the bullish sentiment around these days — and in response to that, he put together a list of his favorite “reasons” to be bullish:

Go forth and speculate.

Copyright © Jan 1, 2013 Belkin Report. All rights reserved |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment