The Big Picture |

- The Geography of Student Debt

- This is Why You Can’t Outrun a Cheetah

- The United States of Conspiracy

- 10 Monday PM Reads

- IQ Valumentum Screen

- US Quantitative Primer 2013

- 10 Monday AM Reads

- What Is Your Market Context?

- Is EVERY Market Rigged?

| Posted: 21 May 2013 02:00 AM PDT The Geography of Student Debt

This morning, the New York Fed released its Quarterly Report on Household Debt and Credit for 2013 Q1. The report uses the FRBNY Consumer Credit Panel to show that outstanding household debt declined approximately $110 billion (about 1 percent) from the previous quarter. The drop was due in large part to a reduction in housing-related debt and credit card balances. Meanwhile, delinquency rates for each form of consumer debt declined, with the overall ninety-plus day delinquency rate dropping from 6.3 percent to 6.0 percent. One of the unique aspects of the FRBNY Consumer Credit Panel, which is itself based on Equifax credit data, is the detail we obtain for each kind of household debt. This quarter, we have taken advantage of the geographic information available in the data set and are introducing a set of maps of our student loan data, which indicate regional variation in several dimensions of student debt. They depict:

Student loan indebtedness and delinquency continue to generate intense interest and we look forward to sharing data and perspectives that help define the scope of this important issue.

Disclaimer

|

| This is Why You Can’t Outrun a Cheetah Posted: 21 May 2013 01:00 AM PDT Source: Speed Kills |

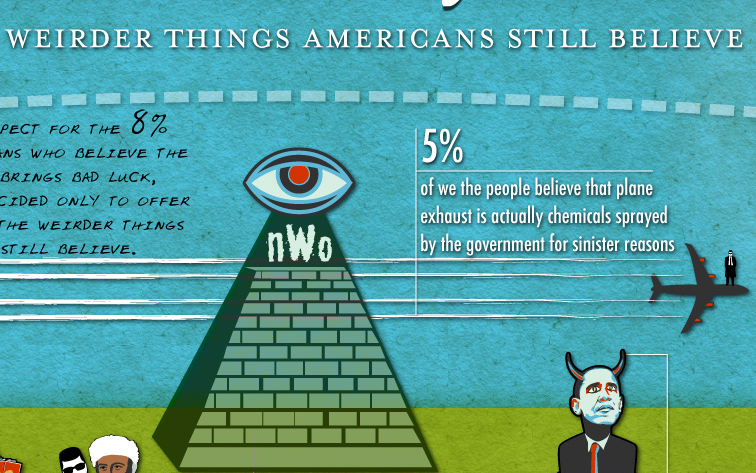

| The United States of Conspiracy Posted: 20 May 2013 04:30 PM PDT click for complete infographic The editors at Best Psychology Degrees decided to research the topic of: 12 of the weirder things Americans believe. - Barack Obama is the anti-Christ (13%)

|

| Posted: 20 May 2013 01:30 PM PDT My afternoon train reading:

What are you reading?

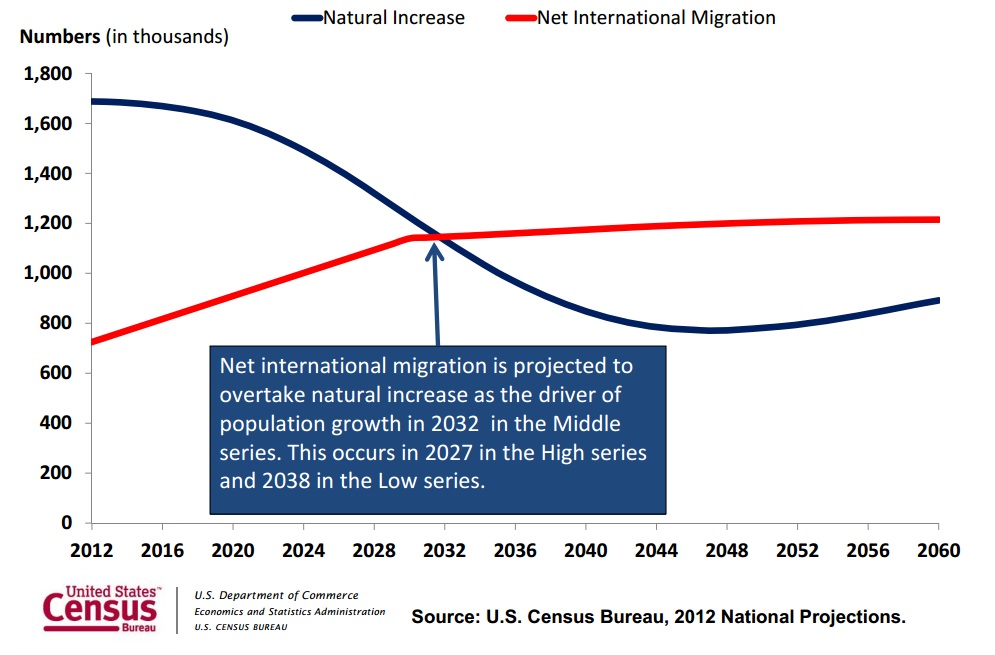

Where International Migration Passes Natural Population Increase (Births ‐Deaths): 2012 to 2060 |

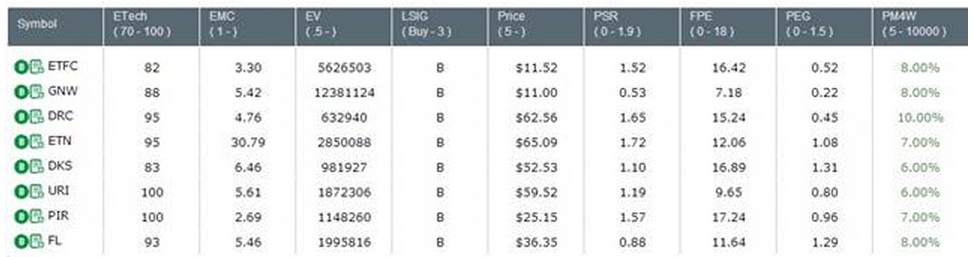

| Posted: 20 May 2013 11:30 AM PDT Here is a good valumentum (value + momentum) screen we came up with using FusionIQ It's time for another installment of FusionIQ's Screen Pass. IQ Screen Pass utilizes FusionIO's proprietary metrics along with widely followed industry metrics to create high level investing and trading screens. Today's edition of Screen Pass looks for stocks that combine both Value and Momentum, or as we like to call it … Valumentum. The variables used in today's screen are as follows: (1) Fusion Technical Scores (ETech) between 70 – 100; (2) Market Cap (EMC) of > $ 1 billion; (3) Trading Volume (EV) of 500,000 or >; (4) Closing Price (Price) of > $ 5; (5) Price to Sales Ratio (PSR) of < 1.9; (6) Forward P/E < 18; (7) Price to Growth Ratio (PEG) of < 1.5; and (8) out-performance vs. the S&P 500 (market) over the last 4 weeks of > 5 % (PM4W). With the market rising a lot of late, we wanted to add a value component to our momentum inputs, to gives us the best of both worlds. Eight stocks hit today's list; E-Trade Financial (ETFC), Genworth Financial (GNW), Dresser-Rand Group (DRC), Eaton Corp (ETN), Dicks Sporting Goods (DKS), United Rentals (URI),Pier 1 Imports (PIR) and Foot Locker (FL). Click to enlarge |

| Posted: 20 May 2013 09:00 AM PDT Last week, I mentioned Merrill Lynch’s Market Analysis Technical Handbook. I was somewhat smitten by the wire house attempt to explain the basics of technicals to a broader layperson audience. Several BP readers at Mother Merrill (as she used to be known) directed my attention to another annual release: US Quantitative Primer 2013. It is described thusly:

Again, color me impressed that a big firm would put out a document that at its heart challenges many of the fundamental principles the rest of the firm is built upon. I do not see a public link for this one (either) but I have put in a request.

Source: |

| Posted: 20 May 2013 07:00 AM PDT My morning reads:

What are you reading?

Is This the Best Time for Investors? Don’t Bet On It. |

| Posted: 20 May 2013 04:00 AM PDT What year is it? That seems to be one of the themes that keeps popping up lately. What year is 2013 like? Is it 1999 and we are about to crash? Is it 1982 and we are on the verge of a multi-decade bull run? Or are we heading for a 1987-like debacle? The answer is none of the above. The circumstances today do not have any exact parallel to prior years or cycles. A quote often attributed to Mark Twain* is that “History does not repeat itself, but it does rhyme.” My favorite rhyme this cycle has been 1973-74. I have referenced that repeatedly during and after the 2008-09 crash. To me, the 56% fall and ~74% snapback rally was hard to argue against as the closest historical analogy. That is, until ZIRP and QE1-4 began. An FOMC engineered 145% rally off of the lows at a 0% Federal Funds rate is simply a case of first impression. There are no historical analogies to the current circumstances. The Fed action has shifted the context debate into a new dimension. Now before you go accusing me of saying that phrase, a brief word: Many people seem to misunderstand the context of Sir John Templeton’s famous quote: “The four most expensive words in the English language are “this time it’s different.” I have always interpreted that to refer to the fact that since human nature is unchanging, it is never different this time. But this truism does not mean we should not discern different circumstances that drive investors at different parts of the markets cycle. Facts can and do differ. That has major repercussions — at least over the short-to medium term. How might the Fed engineering of the post-credit crisis recovery manifest itself? I can imagine three possibilities:

Let’s briefly consider each of these. What does it mean that the Fed has stopped the natural recessions and correction cycles? Here we are are, almost five years post the last recession start — and the economy continues its modest recovery. This is what Reinhart & Rogoff paper — the good one — forecast. FOMC policy is stimulating demand for anything credit-driven. This includes corporate CapEx spending, consumer auto purchases and of course Housing. I do not know of any parallels to these circumstances. Option 2 is skipping the last 5 years of the secular bear market and fast forwarding us to 1982. Problem is, P/E ratios never quite got low enough and dividend yields never got high enough. However, the credible counter argument is simply low rates removed the expected competition. Without risk-free US Treasuries yielding 14%, the major competitor to equities never materialized. Hence, stocks were prevented from finding their natural floor. The final option is that the Fed is driving us straight to the 1987 crash. Professional money managers have been forced in; dividend stocks are the new treasuries. Even mom & pop are starting to look at the stock market. The flip side of this is that after nearly 40 months of outflows from equity funds, we now have but 5 consecutive months of modest (at best) inflows. Bond funds are still attracting more dollars. ~~~ There are lots of other factors affecting markets: Taxes are low, Asia’s development, contained labor costs, international market expansion, productivity gains, practically free credit. Hence, why I say there are no direct paralleles to the current circumstances in the market’s history books. You Humans are the same as you have ever been. Your cognitive biases and emotional (over)reactions are no different than they have ever been. But the circumstances in which you make risk/reward decisions, the context of your investing analyses, are vastly different than what we have become accustomed to. I suspect this change of context may surprise all of us . . .

___________ * There is no actual written Twain quote to that effect; The closest version is “It is not worth while to try to keep history from repeating itself, for man’s character will always make the preventing of the repetitions impossible.” (Mark Twain in Eruption: Hitherto Unpublished Pages About Men and Events, edited by Bernard DeVoto, 1940). |

| Posted: 20 May 2013 03:00 AM PDT European Union Launches Investigation Into Manipulation of Oil Prices Since 2002CNN reports:

USA Today notes:

Fox points out:

The Guardian writes:

The Telegraph reports:

The New York Times notes of agencies like Platt and Argus Media:

The Observer writes that manipulation of the oil markets has long been an open secret:

Reuters points out that the probe may be expanding to the U.S.:

Not only are petroleum products a multi-trillion dollar market on their own, but manipulation of petroleum prices would effect virtually every market in the world. For example, the Cato Institute notes how many industries use oil:

The India Times explains that:

The Federal Reserve Bank of San Francisco points out:

The Post Carbon Institute notes (via OilPrice.com) that high oil prices raise food prices as well:

Economists Nouriel Roubini and Setser note that all recessions after 1973 were associated with oil shocks. Interest Rates Are ManipulatedUnless you live under a rock, you know about the Libor scandal. For those just now emerging from a coma, here's a recap:

Derivatives Are ManipulatedThe big banks have long manipulated derivatives … a $1,200 Trillion Dollar market. Indeed, many trillions of dollars of derivatives are being manipulated in the exact same same way that interest rates are fixed: through gamed self-reporting. Gold and Silver Are ManipulatedThe Guardian and Telegraph report that gold and silver prices are "fixed" in the same way as interest rates and derivatives – in daily conference calls by the powers-that-be. Everything Can Be Manipulated through High-Frequency TradingTraders with high-tech computers can manipulate stocks, bonds, options, currency and commodities. And see this. Manipulating Numerous Markets In Myriad WaysThe big banks and other giants manipulate numerous markets in myriad ways, for example:

|

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment