The Big Picture |

- Asset Encumbrance, Financial Reform and the Demand for Collateral Assets

- Liberals Skewer Obama Administration

- 10 Tuesday PM Reads

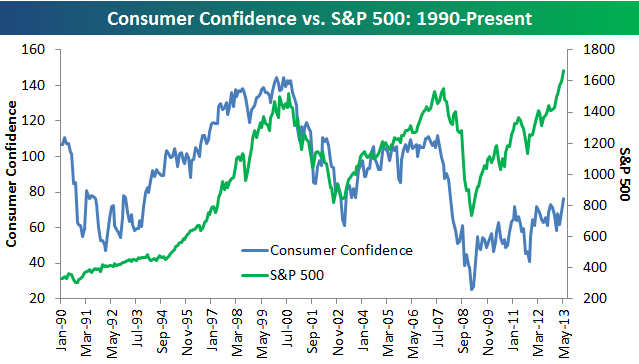

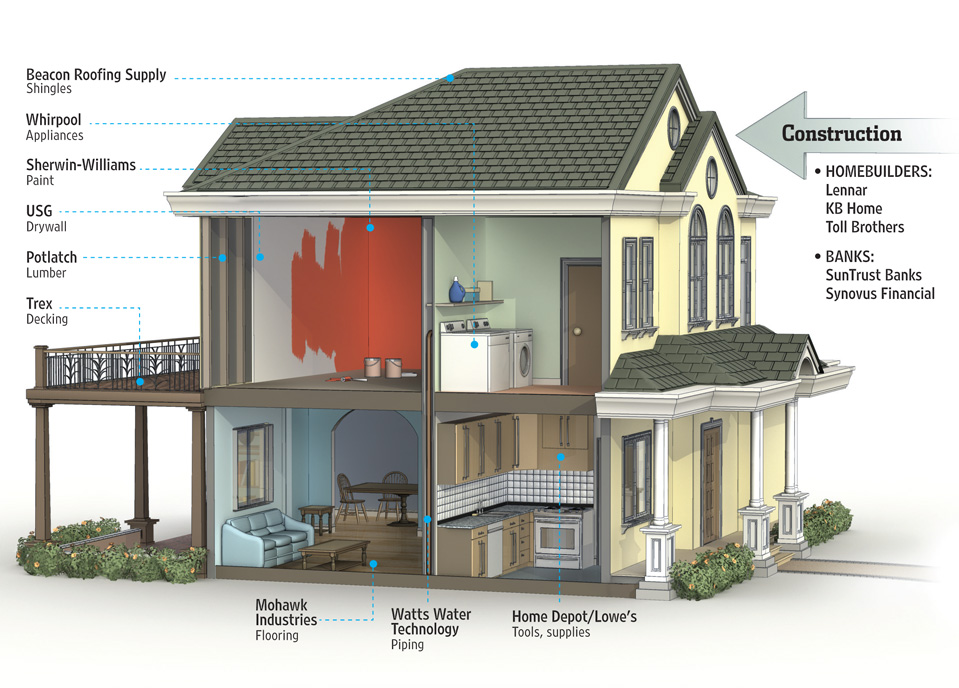

- How Investors Spread Their Housing Bets

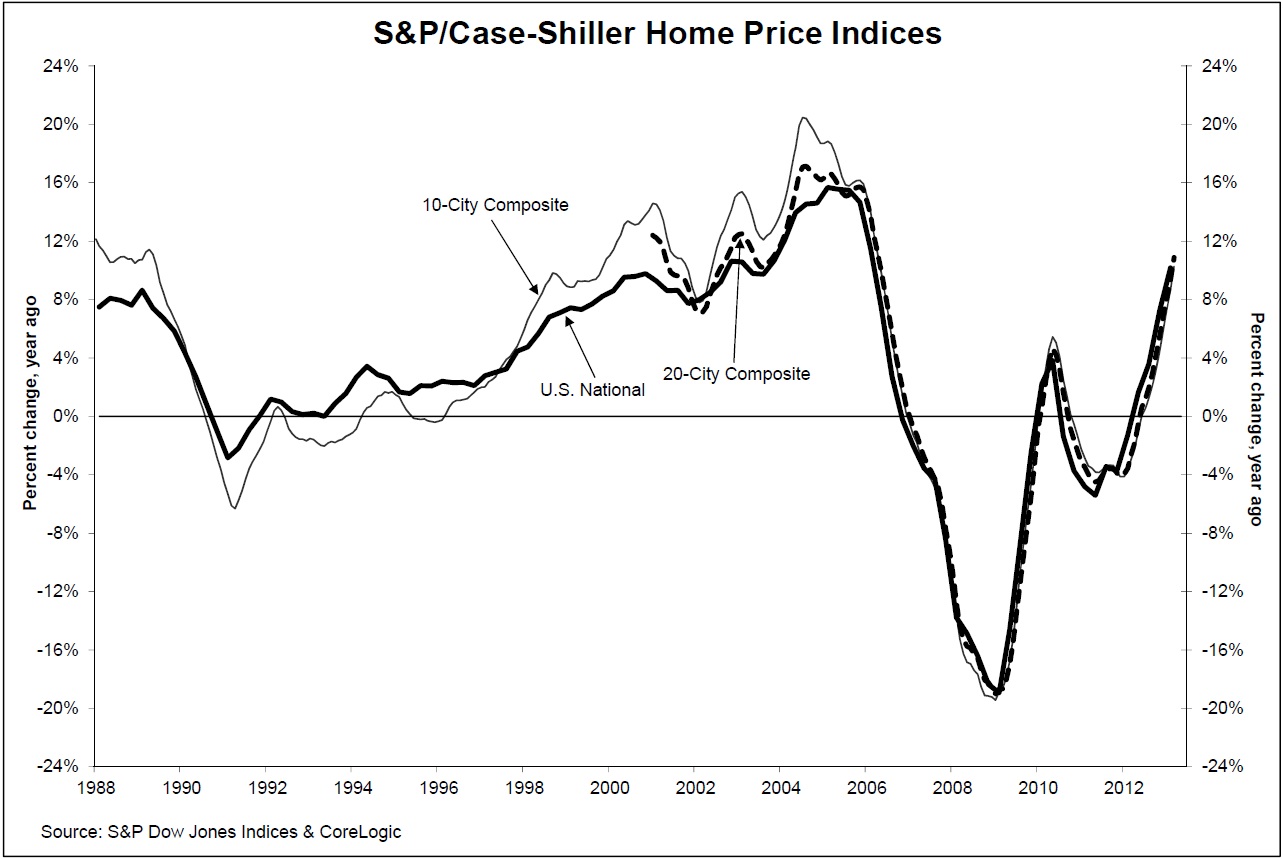

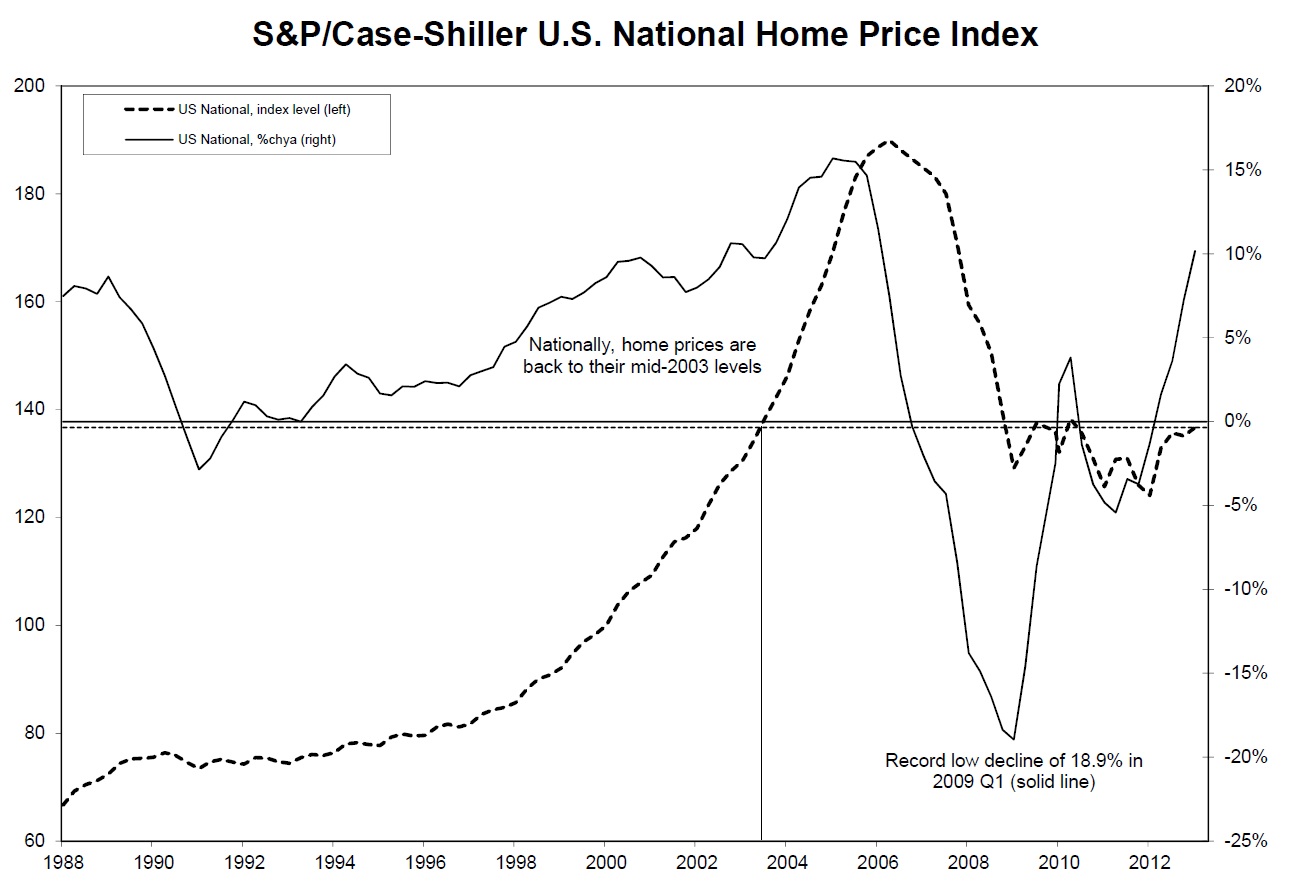

- Home Prices See Strong Gains in Q1 2013

- 10 Tuesday AM Reads

- Proposal for New Hedge Fund Fee Structure: 1% + 33% of Alpha

- Monday Morning Melt Up (Tuesday edition!)

- Nikola Tesla Pitching Silicon Valley VCs

| Asset Encumbrance, Financial Reform and the Demand for Collateral Assets Posted: 29 May 2013 02:00 AM PDT |

| Liberals Skewer Obama Administration Posted: 28 May 2013 10:30 PM PDT Liberals are starting to wake up to the fact that the Obama administration is betraying the principals of justice and economic fairness. Here's the front page of the Huffington Post tonight (each phrase at the website is linked to a separate article exposing Holder's corruption and incompetence):

|

| Posted: 28 May 2013 02:30 PM PDT My afternoon train reading:

What are you reading? |

| How Investors Spread Their Housing Bets Posted: 28 May 2013 11:30 AM PDT |

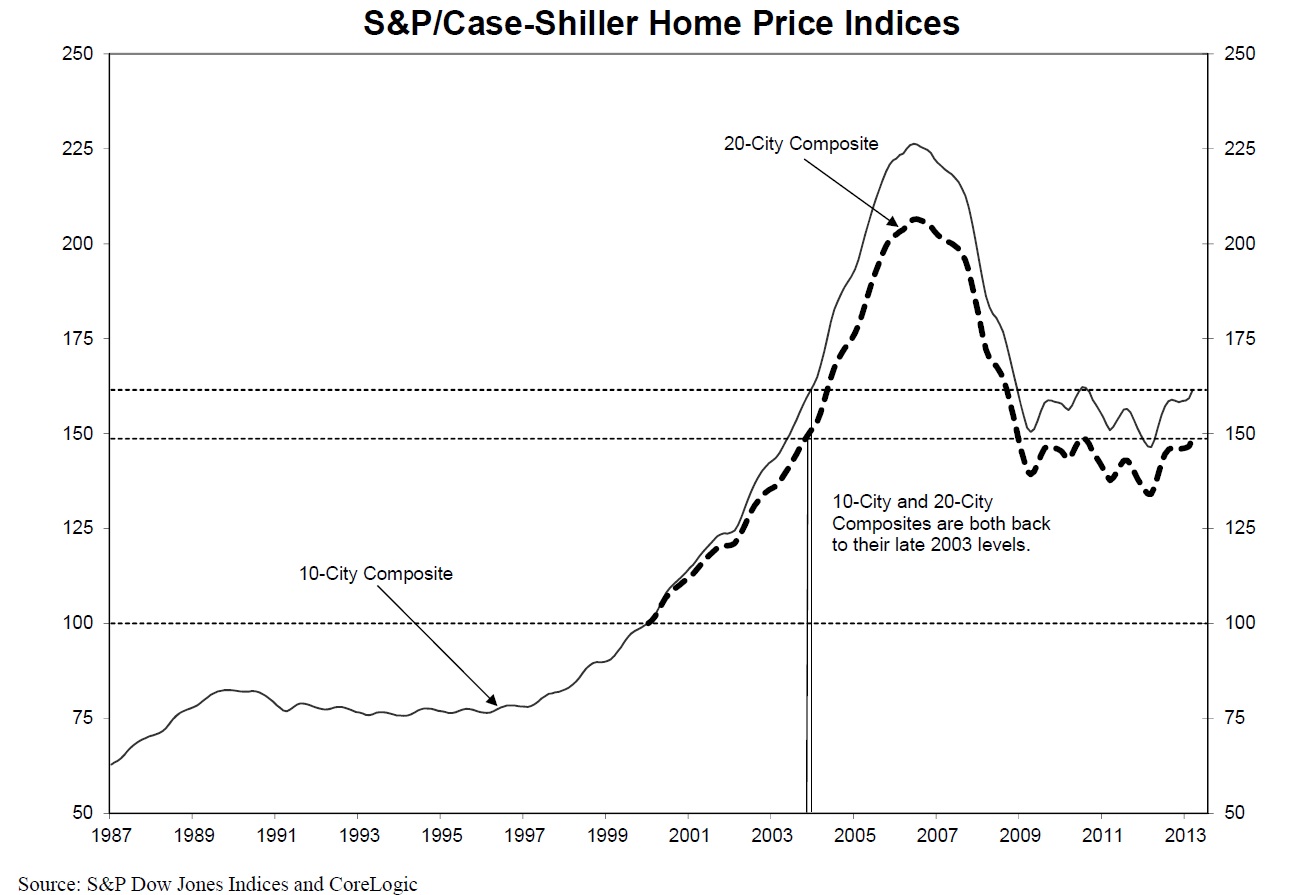

| Home Prices See Strong Gains in Q1 2013 Posted: 28 May 2013 09:00 AM PDT Click to enlarge

S&P/Case-Shiller1 Home Price Indices (data through March 2013) shows:

More charts below

Source: |

| Posted: 28 May 2013 07:00 AM PDT My Tuesday morning reads:

What are you reading?

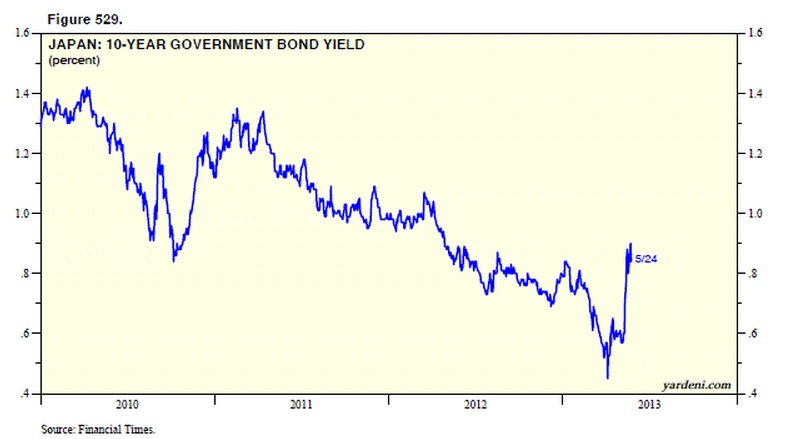

QE & Bond Yields, Japanese Edition |

| Proposal for New Hedge Fund Fee Structure: 1% + 33% of Alpha Posted: 28 May 2013 04:15 AM PDT One of my pet peeves is the way that insiders — whether corporate CEOs, hedge fund managers, or elected politicos — capture compensation (or credit) for normal cyclical gains they had little or nothing to do with. This is the approach favored by the Crony Capitalists — those people pretending to be free market participants, and who merely pretend to be creating value. They are taking credit for structural successes that would have occurred with or without them. What they are actually doing is capturing value, not creating it — and then transferring it from its true owners (shareholders/investors) to themselves. This is wrong; it is legalized theft. If you want to see a good example of how CEOs transfer shareholder wealth to themselves, a good place to start is Roger Lowenstein’s 2004 book, Origins of the Crash: The Great Bubble and Its Undoing. The section on CEO compensation is astounding; these guys were essentially getting wildly overcompensated for being CEOs during a bull market. The prime example was the CEO of Heinz, who gave himself (with the tacit approval of his Board of Here is an idea for you corporate governance types: How about a compensation scheme based on genuine Alpha generation? For corporate executives, this means their bonuses are based on something more than mere stock price irrespective of what the market and their sector is doing; I would suggest a combination of revenue gains (total sales) + total dollar profit growth (not a mere slashing of costs) + outperformance of stock relative to both the broad benchmark (S&P500/400/600 as appropriate) PLUS out-performance relative to their own sector. In other words, stop paying excess bonuses for having the good fortune to be CEO during a bull market. Which brings us to hedge funds. As we discussed over the weekend (A hedge fund for you and me? The best move is to take a pass), we discussed how much of the investing profits were captured by fund managers for themselves. It is a similar situation in that they are taking performance pay for Beta, not Alpha. A better fee structure? Replace 2% + 20% current structure with a 1% + 33% of Alpha. How would that work? Well, the 2% fee gets cut in half, for the simple reason that 2% fee on million dollars plus is excessive. But the real change is when it comes to the performance fee/bonus. That 20% of gains as of late has not been performance, its been only Beta. If their benchmark is up 20% and the manager is up 15%, there is precisely zero Alpha generated. So why should the manager get a bonus or a performance fee? They under-performed. Instead, I propose a 33% of Alpha as a performance fee. The manager gets a bonus performance fee ONLY IF THEY CREATE EXCESS ALPHA OVER BETA — only on the percentage of gains over the benchmark. Lets use a simple example: Two hedge fund managers run funds. Assume the market (their benchmark is the S&P500) is up 10%. Manager 1 (Fund ABC) is up 20%, while manager 2 (Fund XYZ) is up 10%. We will use a million dollar fund as a nice round number. Fund ABC: FUND +20%, SPX +10% Fund ABC sees the manager handily out performing the market. The fee comparisons are below. Example 1:

Example 2: Fund XYZ sees the manager under perform the market. The fee comparison is:

In both examples, managers are being wildly overpaid for Beta; in the other, they are receiving a bonus based in part on Alpha generation. Hence, their compensation is more aligned with the client’s. Note that fund manager of ABC makes less under 1 +33 when they generate Alpha — $43k versus $60k. But look at the enormous savings that come from an underperforming manager: Instead of making $60k for partial Beta generation, he makes $10k — a quarter of the fee generation for partial Beta. I don’t expect fund managers will rush out to embrace this model — unless the institutional players, trustees, and endowments demand it. |

| Monday Morning Melt Up (Tuesday edition!) Posted: 28 May 2013 03:00 AM PDT

Green on the screen as global markets recover and then some from last week’s Japanese mini-crash. 3 day weekend in US and UK show serious upward bias. Yen is weakening, dollar strengthening. Asian markets bouncing after a 5 day losing streak. ~~~ Yes, today is Tuesday. The people responsible for calling today Monday have been sacked . . .

|

| Nikola Tesla Pitching Silicon Valley VCs Posted: 28 May 2013 02:00 AM PDT Here is what would have happened if Nikola Tesla had to pitch some Silicon Valley venture capitalists to get started:

|

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment