The Big Picture |

- Abenomics – Mission Impossible?

- Who Gets the Biggest Tax Breaks?

- The Future of the Web is Video

- Why Do You Want To Be A Hedge Fund Investor?

- 10 Weekend Reads

- Seth MacFarlane’s Harvard Class Day Speech 2006

- At Least One Reason Why People Shouldn’t Hate QE

| Abenomics – Mission Impossible? Posted: 02 Jun 2013 02:00 AM PDT

| ||||||||||||||

| Who Gets the Biggest Tax Breaks? Posted: 01 Jun 2013 04:30 PM PDT | ||||||||||||||

| The Future of the Web is Video Posted: 01 Jun 2013 12:00 PM PDT Video is not only the future of the web—it’s the future of digital communication, and a disruptive force across platforms. This presentation follows video’s journey on the web, then focuses on where it lives today, where it’s going tomorrow, and how different players are to leverage its potential. Emerging technologies are part of this transition, but there’s a human story at the core—how we process information and how we tell stories. This presentation was part of a keynote I gave at the Portland Webvisions Conference on May 23, 2013.

by Leslie Bradshaw on May 28, 2013 | ||||||||||||||

| Why Do You Want To Be A Hedge Fund Investor? Posted: 01 Jun 2013 06:30 AM PDT A hedge fund for you and me? The best move is to take a pass

Earlier this year, Goldman Sachs Asset Management announced that it would launch a new mutual fund that — apparently — will bring the joy of hedge fund investing to the masses. For as little as $1,000, the Multi-Manager Alternatives Fund (GMAMX) allows mom-and-pop investors to put their life savings into some of Wall Street's riskiest and most expensive products. This "fund of funds" will, according to its prospectus, let investors gain exposure to the trading strategies of hedge funds. The obvious question is: "Why would investors want that?" Despite all the media coverage, glitz and glam of hedge funds, they have not done well for their investors. They have high — some say excessively high — fees; their short- and long-term performance has been poor. Before delving into the details, let's define exactly what we are discussing: Hedge funds are private investment partnerships. The general partner is typically the fund manager (on occasion it includes his financial backers). The investors in the fund are the limited partners, normally institutions and accredited investors. This partnership structure typically has a max of 99 limited partners. Unlike mutual funds or brokerages, hedge funds are mostly unregulated. The global hedge fund industry manages $2.13 trillion, or about 1.1 percent of all assets held by financial institutions, according to the Coalition of Private Investment Companies. Given what a relatively small asset class this is, hedge funds certainly receive an excess of media attention. Many hedge fund managers have become billionaires; perhaps this — plus their reputations as the smartest guys in the room — is why they have captured the investing public's imagination. Most hedge funds are "go anywhere" funds — they can own derivatives, mortgage-backed securities, credit-default swaps, structured products and illiquid assets. They also can use nearly unlimited leverage. Gee, that sounds kinda hazardous. Why would anyone want to assume all of that risk? Originally, hedge funds earned their outsize compensation by, well, hedging their investments. This is a risk-mitigation strategy that can reduce the gains investors reap when markets are up but avoids much of the losses when markets are down. That no longer seems to be the case with modern hedge funds. They have morphed into "absolute return" funds — more aggressive, greater leverage, more speculative, all in an attempt to generate returns that outperform their benchmarks. Not surprisingly, they have become riskier than the overall market. Given these increased risks (and higher fees), how have hedge funds performed? By most measures, not well. They have failed to keep up with major averages when markets were up — and they got mangled (like nearly everyone else) during the 2008-09 downturn. It turns out, most hedge funds are not very hedged. The latest performance data (via the HFRX Global Hedge Fund Index) reveal that hedge funds haven't fared well at all: They returned a mere 3.5 percent in 2012, while the S&P 500-stock index gained 16 percent. Over the past five years, and the hedge fund index lost 13.6 percent, while the indices added 8.6 percent. That's as of the end of 2012; it has only gotten worse in 2013. Most hedge funds have fallen even further behind their benchmarks this year, gaining 5.4 percent vs. the market's rally of 15.4 percent. As a source of comparison, the average mutual fund is up 14.8 percent. Which brings us to fees. Most hedge funds charge an industry standard "2 and 20." This is a 2 percent annual management fee against the original investment, plus 20 percent of the investment profits. Compare this with annual mutual fund fees, which average about 1.44 percent. Fees for an index ETF are typically under 0.25 percent. Those outsize hedge fund fees are an enormous drag on performance. But they do create wealth — for the managers. "Two and twenty" as the industry calls it, is why even middling hedge fund managers can become billionaires. According to Simon Lack, author of "The Hedge Fund Mirage," this fee arrangement is effectively a wealth transference mechanism, moving dollars from investors to managers. As he puts it: "While the hedge fund industry has generated fabulous wealth and created many fortunes, it has largely done so for itself." Lack is no ordinary critic — he spent his career at JPMorgan Chase, where he allocated more than $1 billion to emerging hedge fund managers. Some of the statistics he amassed in the process are nothing short of astonishing: ●From 1998 to 2010, hedge fund managers earned $379 billion in fees. The investors of their funds earned only $70 billion in investing gains. ●Managers kept 84 percent of investment profits, while investors netted only 16 percent. ●As many as one-third of hedge funds are funded through feeder funds and/or fund of funds, which tack on yet another layer of fees. This brings the industry fee total to $440 billion — that's 98 percent of all the investing gains, leaving the people whose capital is at risk with only 2 percent, or $9 billion. What other concerns should investors have? Hedge funds are not especially liquid. Many are "gated" — meaning there are only small windows when you can withdraw your money. They typically have a high minimum investment and often require investors keep their money in the fund for at least one year. Why would anyone in their right mind invest in these funds? So many kids dream of becoming LeBron James, but most will never play in the NBA (to say nothing of amassing championship rings). So it also goes with hedge fund investors. Most of the more than 10,000 hedge funds out in the wild are not big moneymakers for their investors. Investors tend to discover "hot" mutual fund managers just after a successful run and just before the inescapable force of mean reversion is about to kick in. Similarly, hedge fund darlings are born at exactly the same moment in their trajectory. John Paulson is a classic example. The bet against subprime mortgages that he and Paolo Pellegrini created in 2005-06 put them on the map and turned Paulson into a billionaire. He became widely known, and the money flowed in. Within a few years, Paulson was managing a slew of hedge funds, and his assets under management had swelled to $36 billion. Soon after, he hit the skids, with losses of 52 percent in one fund and 35 percent in another. But the lure of the superstar manager — the guy who can make you fabulously wealthy – continues to attract capital. In 1997, $118 billion was managed by hedgies; as of the first quarter of 2012, that had grown to $2.04 trillion. Investors have also embraced other non-financial remunerations: Client-only market commentary, access to star managers, attendance at exclusive conferences. These perks generate cocktail party bragging rights, despite the poor performance. But what about the top-performing funds, such as Jim Simon's Renaissance Technologies or Ray Dalio's Bridgewater? Sure, give them a call. The Lebron James of hedge fund managers are few and far between. This is the crux of the issue with hedge funds. A small percentage have significantly outperformed the markets; an even smaller percentage have done so after fees are taken into account. While we all know which ones have outperformed over the past few decades, no one has even the slightest clue which ones will outperform over the next one. It is akin to picking out from the ranks of high school sophomores who will be the next NBA superstar. Best of luck with that. Every fund in the world warns that past performance is no guarantee of future results. It is too bad that investors refuse to believe it. ~~~ Ritholtz is CEO of FusionIQ, a quantitative research firm. He is the author of "Bailout Nation" and runs a finance blog, the Big Picture. | ||||||||||||||

| Posted: 01 Jun 2013 04:00 AM PDT My longer form journalism for your less hassled weekend reading pleasure:

Whats up for the weekend?

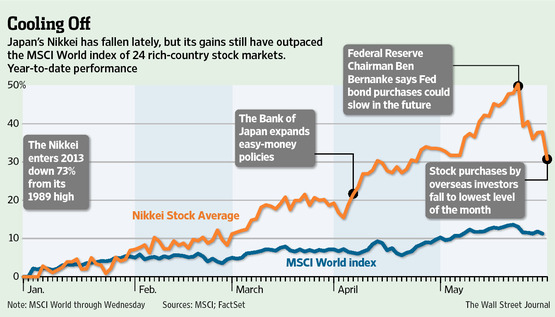

Dow Moves Up Despite Bad Week in Japan

| ||||||||||||||

| Seth MacFarlane’s Harvard Class Day Speech 2006 Posted: 01 Jun 2013 03:00 AM PDT Seth MacFarlane's Harvard Class Day Speech 2006 Part 1: Part 2 (Peter): Part 3 (Stewie): Part 4 (Quagmire): | ||||||||||||||

| At Least One Reason Why People Shouldn’t Hate QE Posted: 01 Jun 2013 02:00 AM PDT At Least One Reason Why People Shouldn’t Hate QE

You might not expect me to endorse an article titled “The 7 Reasons Why People Hate QE.” I won’t disappoint that expectation, but I will say that I do endorse, and appreciate, the civil spirit in which the author of the piece, Eric Parnell, offers his criticism. We here at macroblog, like our colleagues in the Federal Reserve System more generally, pride ourselves on striving for unfailing civility, and it is a pleasure to engage skeptics who share (and exhibit) the same disposition. What the world needs now is…well, maybe I’m getting carried away. Let me instead appropriate some of Mr. Parnell’s language. It is worthwhile to explore some of the reasons that people do not like QE from someone who does not share this opposing sentiment. In particular, let me focus on the first of seven reasons offered in the Parnell post:

This statement seems to presume that monetary policy does not normally have differential impacts across distinct sectors of the economy. I think this presumption is erroneous. The Federal Open Market Committee’s (FOMC) asset purchase programs have long been seen as operating through traditional portfolio-balance channels. As explained by Fed Chairman Ben Bernanke in an August 2010 speech that set up the “QE2″ program:

I think this is a pretty standard way of thinking about the way monetary policy works. But you need not buy the portfolio-balance story in full to conclude that even traditional monetary policy operates on “selected areas of the economy such as the U.S. housing market.” All you need to concede is that policy works by altering the path of real interest rates and that not all sectors share the same sensitivity to changes in interest rates. Parnell goes on to discuss other problems with QE: stress put on individuals living on fixed incomes, the promotion of (presumably excessive) risk-taking, and the general distortion of market forces. All topics worthy of discussion, and if you read the minutes of almost any recent FOMC meeting you will note that they are indeed key considerations in ongoing deliberations. These issues, however, are not about QE per se, but about monetary stimulus generally and the FOMC’s interest rate policies specifically. As the conversation turns to if, when, and how Fed policymakers will adjust the current asset purchase program, it will be important to clarify the distinction between QE and the broader stance of policy.

May 30, 2013 in Federal Reserve and Monetary Policy, Monetary Policy | Permalink | ||||||||||||||

By

By | You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment