The Big Picture |

- Nikola Tesla: Passing Through

- Economic Inequality Is Not An Accident, It Was Created

- 10 Tuesday PM Reads

- Media Appearance: Bloomberg TV with Trish Regan (3:00 – 4:00 pm )

- NYSE Takes Over LIBOR

- HFT’s Unfair Trading Advantage / Front Running

- 10 Tuesday AM Reads

- Dealbook’s Sorkin Blows The Return of the Fabulous Fab

- Möbius Strip Levitating Superconductor

| Posted: 10 Jul 2013 02:00 AM PDT Happy Birthday Nikola Tesla!

Passing Through from Olafur Haraldsson on Vimeo. Passing Through by The text used for the narration of "Passing Through" is part of a speech Serbian scientist and inventor Nicola Tesla delivered in 1893 at the Franklin Institute in Philadelphia. Though today less known than figures like Edison and Einstein, Tesla was more or less the father of much of our modern technology, since he among other things developed the foundations of the European electrical system based on alternating currents and the principles of wireless radio communication. At the time he was deeply influenced by the Austrian physicist and philosopher Ernst Mach, believing that the world should be conceived as a whole where everything is interconnected influencing each other. And that energy is a force that runs through everything be it inorganic matter, organisms or human consciousness. According to this line of thought every single action has universal consequences, not unlike what the father of modern chaos theory Edward Lorenz in the 1960's termed 'the butterfly effect'. "Passing Through" is made at Kolding School of Design in connection to the Danish iPower-project. |

| Economic Inequality Is Not An Accident, It Was Created Posted: 09 Jul 2013 04:30 PM PDT Inequality is real, it’s personal, it’s expensive and it was created. Today, 1% of Americans are taking home nearly 20% of the country’s total income and own nearly 35% of the country’s wealth. This didn’t happen by accident. As former Secretary of Labor Robert Reich explains, we allowed it to happen. We can’t have a prosperous economy without a strong and prosperous middle class. Inequality can be fixed. So, let’s fix it. inequality.is, a new interactive site from the Economic Policy Institute, explains the causes of and solutions to income inequality. ————————————- The recent past has seen greater economic inequality in America than at any time since the Great Depression. In the three decades after World War II American incomes grew quickly and equally, but starting in the late 1970s things began to change. Today, 1% of Americans are taking home nearly 20 percent of the country’s total income, and own more than 35% of America’s wealth. And it didn’t happen by accident. It’s the result of policy decisions on taxes, education, trade, labor, macroeconomics, and financial regulation — all of which shifted economic power away from low and moderate-income American families. Economic inequality is real, it’s personal, it’s expensive. And it was created. Since the 1960s, tax rates on very high incomes have been slashed dramatically, starving public investments in schools and roads and everything else needed to build our economy, and providing ever-greater incentives to rig the economy’s rules to send more money to the top The laws we’ve created to govern globalization have protected corporate interests, but done nothing for American workers. Instead, we’ve allowed worker’s rights to be systematically dismantled, both here and abroad. Policymakers also began using high unemployment — which hurts everybody, but especially low and middle-wage workers — to protect the wealthy from any hint of inflation. And, then, corporate interests pushed to abandon safeguards preventing the financial sector from making risky bets, which had to be backstopped by American taxpayers when those bets went sour — a protection not given America’s underwater homeowners. All of this created the worst economic crisis since the 1930s — and we did it by allowing those with the most economic power to set the rules of our economy. It’s continuing today. By the end of 2012, American workers’ share of the economic pie was the lowest in more than half a century while the share going to corporate profits was the highest on record. This isn’t sustainable. We can’t have a prosperous economy without a large and growing middle-class. None of this happened by accident. We allowed it to happen. But it can be fixed. So let¹s fix it. |

| Posted: 09 Jul 2013 01:30 PM PDT My afternoon train reading:

What are you reading?

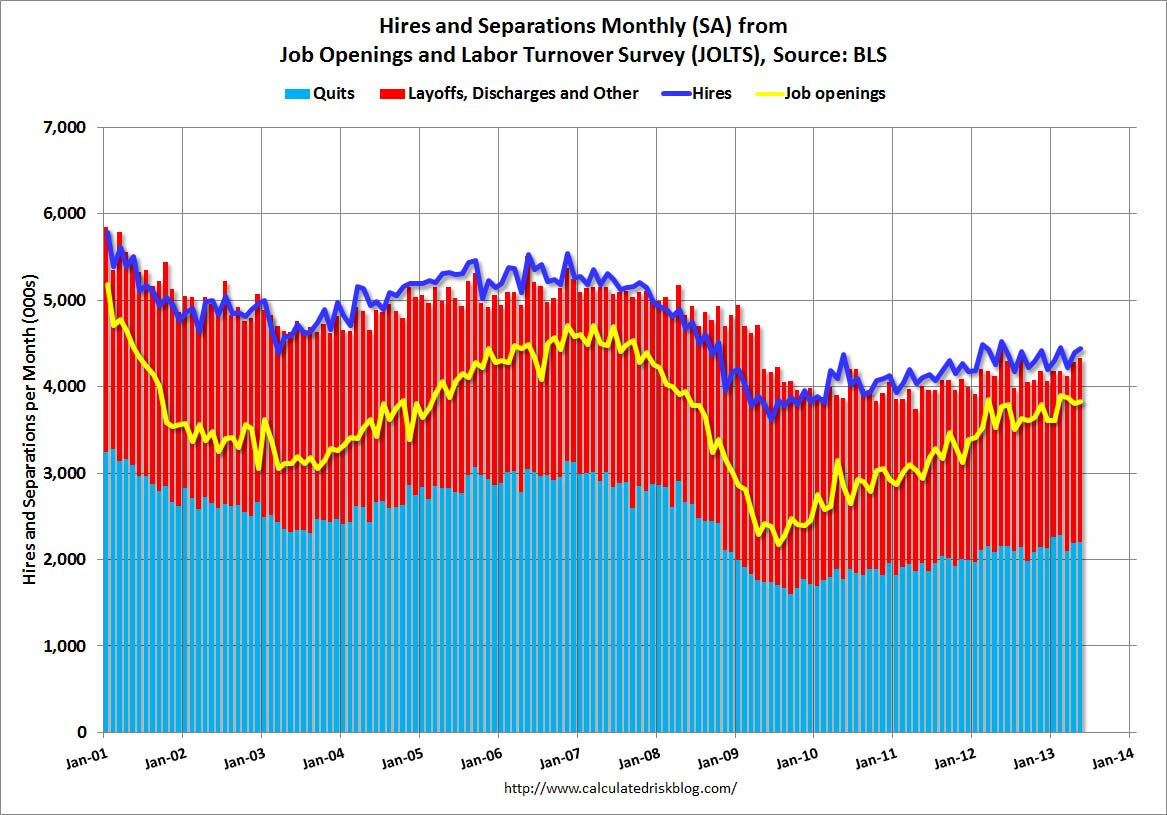

BLS: Job Openings little changed in May |

| Media Appearance: Bloomberg TV with Trish Regan (3:00 – 4:00 pm ) Posted: 09 Jul 2013 11:30 AM PDT

I will be guest hosting with the lovely Trish Regan at Bloomberg TV from 3:00 pm to 4:00 pm on Street Smart. We will talk Barnes & Noble, NYSE take over or LIBOR, and the Bond Outflows. Should be lots of fun — Check it out at their live streamer on TV.

|

| Posted: 09 Jul 2013 10:30 AM PDT

|

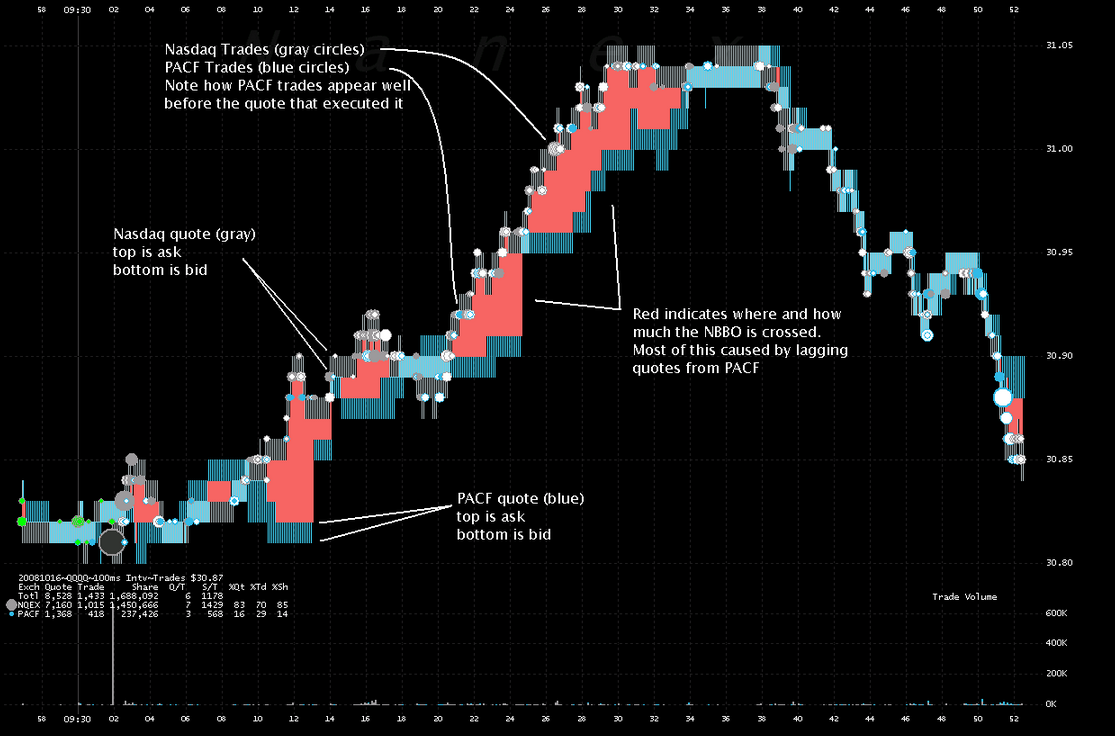

| HFT’s Unfair Trading Advantage / Front Running Posted: 09 Jul 2013 09:00 AM PDT Wherever you see red in the charts below, that’s when HFT received an unfair trading advantage and front ran other traders and investors.

Click through, scroll down a bit, then hit start for samples of HFT front running

Nanex observes that:

|

| Posted: 09 Jul 2013 07:00 AM PDT My morning reads:

What are you reading?

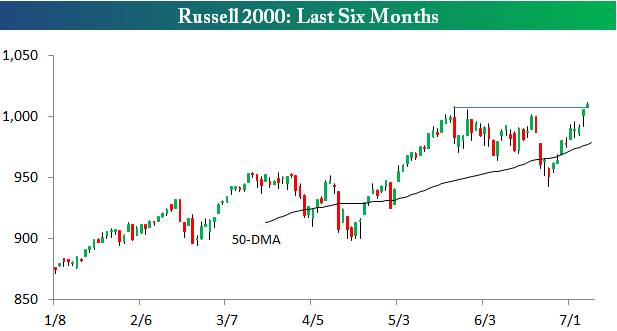

New All Time Highs For Russell 2000 |

| Dealbook’s Sorkin Blows The Return of the Fabulous Fab Posted: 09 Jul 2013 05:15 AM PDT Events have led us back to our continuing series of oversight into the goings on of all-too-rare Wall Street prosecutions, and the terrible media coverage that accompanies them. The awful media story of the day is Andrew Ross Sorkin’s botched NYT coverage of the fabulous Fabrice Tourre prosecution for Rule 10B-5. The punditry did a terrible job on initial go round with Goldman Sachs Abacus case; this is an inauspicious start with the Fabulous Fab Tourre case from NYT. The column reeks of defense attorney spin, expertly flacked. As anyone who understands security law knows, prosecutors are extemely limited about what they can say in public about an active litigation (Rights of the accused and all that). This allows clever defense lawyers to find gullible journalists to dupe with a one sided set of ridiculous accusations, knowing full well that the SEC cannot respond. The goal may be to help sway potential jurors; it could also pressure the case outside of the court room. The defense hit paydirt in legal gullibility with Sorkin: Conspiratorially headlined “Trader's Day in Court May Lack Some Details,” the article goes on to explain in painstaking details what is being kept from the jury. It also laughably makes claim this minor individual case is a stand in for all the other cases not brought to suit by the SEC:

Sadly, no: I cannot begin to explain how completely erroneous the above statements are. No, this is not a referendum on Goldman Sachs. I do not believe ANYONE at the SEC believes this simple 10b-5 case is about anything other material misrepresentations in the sale of a security. On the other hand, this is what a defense attorney says — My client is being made a scapegoat for the entire financial collapse! – not what the SEC thinks. And no, this is not about keeping the jury in the dark about the facts of the case. The facts, as we first discussed in these pages three years ago, this is a simple Rule 10b-5 case. The Security and Exchange laws, first passed in 1934 (see 17 C.F.R. 240.10b-5). It explicitly outlaws all practices that are” Manipulative and Deceptive.”

There is a rich history of 10b-5 prosecution, the statute is specific, the case law well settled, and the evidentiary standards are well known. You don’t have to show the clients were actively misled, or they should have known better, ot yhey wer or were not sophisticated investors. The prosecution doesn’t even have to show the salesman knew (or should have known) he was being deceptive. There is no mens rea (guilty mind) component; there is no need to prove actual deception on the buyer; what the buyer knew or should have known is irrelevant. All a prosecutor has to demonstrate is that the sales pitch was deceptive, and that deception was material. The laundry list of insinuated hints in Sorkin’s article about what the SEC is hiding from the jury is just so much nonsense. He either does not understand Security law of 10b-5 or simply prefers to carry the defense’s water. I cannot explain how the NYT let such a slipshod article slip through its editorial processes, but there you have it. Further I am astonished that there is not a single quote from a lawyer to give any context. The standard operating procedure is for the journalist to grab a quote from a former prosecutor to provide 2 sided context. This allows someone to speak for the prosecutor, who cannot discuss the active case in public. This was a noticeable omission and defines the article as not only one-sided, but erroneous in the extreme. What about ACA not being declared “a victim of the fraud” by the SEC? The answer, quite simply, is that unlike TRUE victims (in an SEC legal sense) ACA Capital has redress — ACA can file a civil suit against Goldman Sachs to recover their losses. And indeed, that is precisely what they did in 2011. Earlier this year, they won the right to add John Paulson to the litigation as well. End of story, next case please.

Previously: Fabrice Tourre/Goldman Emails (April 25th, 2010) Its the Law, Bitches! (July 19th, 2010) Who Steered You Wrong About the GS Case? (July 16th, 2010) Source: |

| Möbius Strip Levitating Superconductor Posted: 09 Jul 2013 03:00 AM PDT Andy takes a closer look at one of his favourite demos from the 2012 Christmas Lectures, bringing together a levitating superconductor and a bewildering Möbius strip made from over 2,000 magnets. As his super-conducting boat whizzes along the track, Andy demonstrates the remarkable properties of the superconducting material (Yttrium barium copper oxide) which allows it to seemingly float both above and below the track. Watch more science videos on the amazing Ri Channel: http://richannel.org |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment