The Big Picture |

- The Shifting and Twisting Beveridge Curve: An Aggregate Perspective

- McCartney Rules

- Succinct Summation of Weeks Events (10/25/13)

- Rand Paul & Janet Yellen

- China Econ Tracker

- State of the Economy

- 10 Friday AM Reads

- More Signal, Less Noise

- US Bank Fines = $95 Billion Dollars

- JPMorgan: Fish Rot from the Head

| The Shifting and Twisting Beveridge Curve: An Aggregate Perspective Posted: 26 Oct 2013 02:00 AM PDT |

| Posted: 25 Oct 2013 03:30 PM PDT

1. Excellence If it's not great, don't release it. Put it up on YouTube, not the album, if you're trying to get everybody's attention, make sure your music deserves it. 2. Availability Put your complete album on YouTube and all streaming services. That's where people discover your music. Your hard core fans will buy it, for now anyway, but casual users sample, and see if they're interested. There's plenty of money if you can get people to focus and continue to listen. 3. Be your own curator. Don't put out ten tracks, call it an album and leave us to discover what's good. Sure, you can focus on a single, but too often it's trying to be all things to all people and is not great. So point us to the two or three tracks we need to listen to. 4. Trust your heart. Don't listen to anybody else. Push the cuts that resonate with you, that make your heart sing, jump for joy and cry. People are drawn to emotion, they want to be touched. Don't second guess, unless you're playing the singles game, and that's a game controlled by the usual suspects, unless your track was made by Dr. Luke and Max Martin, don't bother. 5. Press is a circle jerk. Kinda like the wannabes want to send a CD that the writer won't listen to in order to make themselves feel good, ancient acts believe if they get enough ink, TV and radio play that they've done their job, but the truth is they haven't even scratched the surface. It's a direct to fan era. Know who your hard core is and give them tracks for free, if they're good, they'll spread the word. Fire your PR person and read Malcolm Gladwell's "Tipping Point." 6. Virality Your goal is to keep your music alive. There's nothing more frustrating than spending a year on an album and then seeing it disappear in a month, never to be heard again as you ply the boards playing your greatest hits. 7. Reviews Only matter if EVERYBODY says something is great. 8. Hunger It's a conundrum, the audience has got no time, yet is desirous of something new and exciting that will not only satiate them, but they can turn others on to. That's your job, to feed this machine. Don't ask for the audience's time, don't put yourself above them, it's a privilege to be heard, your job is to serve the audience. Interestingly, the more you focus inward, on your art, the greater chance you have of succeeding. The two biggest left field hits in recent memory are all about the track, not the campaign… Lorde's "Royals" and Gotye's "Somebody That I Used To Know." The tracks infected listeners and they spread the word. 9. Sound Don't master for radio if your track will never be played. Extreme loudness and compression is a disservice to your music unless you're playing the hit game. 10. Fame Is no guarantee anybody will listen to anything more than a single. Which is why your single must absolutely kill. It's like your first line in a bar, if it's bad, you've blown your chance. 11. It's something you feel. Great records cannot be described. They contain something that penetrates you in a way that stops time and you can't focus on anything but the pure sound and how it makes you feel. I still remember hearing "Sexual Healing" the first time…driving on the 10 East, between National and Robertson… Ha! 12. They call it show business. But it starts with art. Business is easy, and always comes last. You can always hire someone to do your business, but you can't easily hire someone to create magic. 13. Don't fake it. If you're losing your voice (or looks!) don't cover it up! The imperfections will appeal to people. Owning who you are is so enticing. 14. Artwork and album title and running order. Are irrelevant. The art is a tiny square on a person's computer or mobile, and the title is only memorable if your album is, as for running order, no one listens that way anymore, if they listen to the whole album at all. 15. Don't pay attention to musos. It's great people live for albums and music, but they vocally skew the discussion, the same way they've convinced everybody that vinyl is making a comeback, it's not, it's a pimple on the ass of the music business. Don't be afraid to alienate the holier-than-thou. _____________________________________________ These albums sound so bad on the streaming services. They say they're at 320kbps, both Spotify and MOG if you've got premium, but they're a far cry from the CD, which is a far cry from the vinyl, which still isn't as good as the master tape. In other words, what kind of world do we live in where this stuff is recorded digitally, on computers, but we can't have the version direct from the source? It's got to be compressed and remastered and by time we hear it it sounds like it's being transmitted via two Dixie Cups on a string. In the old days I probably would have bought McCartney's new album, I'm a fan. Maybe not the CD, CDs were always too expensive, you had to think twice before you laid your money down, vinyl led to experimentation. And I would have gotten home and broken the shrinkwrap and dropped the needle on my mega-stereo and been engrossed by the sound. But today, even with great computer speakers, even with the ultra-popular Beats headphones, which are mediocre, the source is so crappy that what comes out is not music. Oh, I know, you can hear a hit through mud. I believe that. But I also believe we get the music we deserve. Which is over-compressed, bass-heavy drivel, because something more sensitive loses all its sensitivity in today's digital translation. And sensitive is what "Early Days" is. I'm playing McCartney's new album, because I'm a fan, because it's scannable on Spotify, and if you're holding back from streaming services you're verging on irrelevance, like Thom Yorke's Atoms For Peace. The main challenge today isn't getting paid, it's getting someone to listen, and almost no one can accomplish this goal. Exhibit one, Miley Cyrus. Even grandmothers know who she is. Miley executed the best promotional campaign of the decade. But still no one wants the album, she only sold 270,417 copies of "Bangerz" last week, which to say is commendable is like lauding Miguel Cabrera if he hit 275 and 20 home runs. Sure, better than many, but still…positively mediocre. But almost no one can sell an album these days. Certainly not Paul McCartney. Just look at Elton John, who had an even better publicity campaign, spouting nonsense that he has never sung better, Elton's sold 78,109 copies of "The Diving Board" in three weeks, only 11,816 last week, it's on its way to being completely forgotten before Thanksgiving. So what does Paul McCartney do? What everybody else does. He goes on Stern, he plays unannounced gigs. But none of this has to do with the music. That's the problem with Miley Cyrus, she's a celebrity, her tunes are made by committee, she's a modern pop star with nothing to say, we just want to see the antics. But McCartney, once upon a time he had something to say. But first I listen for music. And I find this track "Early Days." "New" gave people what McCartney thought they wanted. Something upbeat that hearkened back to what came before. But the problem with second-guessing the audience is it only works if you're truly in touch with the audience, like Dr. Luke, the oldsters are clueless, they're best off trusting their instincts. Like with "Early Days," which was not made for radio, but home listening. It's so intimate. It's got that White Album feel. You know, that intimacy like Paul is literally sitting inside the speaker singing just for you. Anybody who was ever a fan will get it. But I doubt most fans will ever hear it. Oh, what a conundrum. One other track stuck out, "I Can Bet," which is pedestrian until it has a change so delicious 35 seconds in you'll immediately start smiling and nodding your head, wondering if you're seeing the world through sixties glasses, viewing today, but having it look so much better. That's what McCartney used to specialize in, the changes, the flourishes, no one's better. And after getting hooked by these two cuts, , when I started the album from the top again it sounded better than the first time through, I was having the old experience, but almost no one is. So where does this leave us? In a singles world in an attention economy. The album is a failed enterprise because despite so many lauding it, most have abandoned it, they just don't have the time for it, and therefore they wait for a single to surface before they pay attention, and when one doesn't, they move on, kind of like with the Elton album. Oh, we could say it's all about radio. And oldsters do listen to their NPR. But despite ridiculous protestations from the radio industry, it's dying. Not that an EP is always the answer. Fleetwood Mac released one and it's like it didn't come out. Maybe like the Dead, these acts have to insert a few new cuts in their live shows, convince audiences that way first. If everybody's going to the bathroom, it goes straight to the dumper itself. If you can get everybody to like it at the show, you've got something, maybe you then push it out to attendees for free in e-mail, I mean why are we selling these albums anyway, all the money for McCartney is on the road. What McCartney wants most is to be heard. And he deserves to be. Not because he's Paul McCartney, but because "Early Days" and "I Can Bet" are good. But that was not the message of the hype, which was all bland and non-specific. Granted McCartney's old. And an occasional act, like Drake and Justin Timberlake, can sell an album. Their audience believes they're making a statement. But McCartney was the voice of his generation. I guess we're all dependent upon virality. And McCartney's got none. As a result, his album is gonna tank, maybe not as fast as Elton's, but soon. That's what you need. Virality. To start a fire. If only these old acts realized we live in a new world and it's incumbent upon them to deliver excellence and go straight to the tastemakers, not the press, which will spread the message. The press is old school. Even television. They're too cold. What these acts need is fans sending links. And they must focus on tracks as opposed to albums. Because no one's got time for filler. And if you were never a McCartney fan, move right along. But if you are one, try these:

– |

| Succinct Summation of Weeks Events (10/25/13) Posted: 25 Oct 2013 12:30 PM PDT Succinct Summations week ending October 25, 2013.

Negatives:

|

| Posted: 25 Oct 2013 12:00 PM PDT Rand Paul & Janet Yellen

There are reports that Senator Rand Paul intends to put a "hold" on Janet Yellen's nomination for Federal Reserve Chair. Senator Paul is involved in an absolute act of lunacy. He wants to put Janet Yellen's nomination on hold in order to force a vote on his Fed Transparency bill. Fine, Senator Paul, force the vote, but doing it this way will inject disarray into financial markets – and because of a political squabble. You are going to hurt every 401K, every investor, mortgage applicant, builder, and business entity in the United States. Senator Paul's website is http://www.paul.senate.gov . His Washington, D.C., and Kentucky telephone numbers are as follows: Kentucky Washington, D.C.: (202) 224-4343 If there is ever a time for the American people to say, "We have had enough of this political nonsense," it is now. There is nothing wrong with Janet Yellen's nomination. She is the Vice Chair of the Fed. She has been the president of the Federal Reserve Bank of San Francisco. She has had a distinguished public service career and is a skilled economist. Janet Yellen is an expert in monetary affairs and banking supervision. Furthermore, she was involved in the architecture of the policies that helped save the US and others worldwide in the post Lehman-AIG meltdown. It is time for citizens to take their country back. One of the ways to do so is to use the telephone now. I already did. If you happen to be from Senator Rand Paul's state, call his local office and let them know how you feel. He will not answer, but his staff will. ~~~ David R. Kotok, Chairman and Chief Investment Officer Cumberland Advisors |

| Posted: 25 Oct 2013 11:30 AM PDT Very cool site to play with:

click for interactive site |

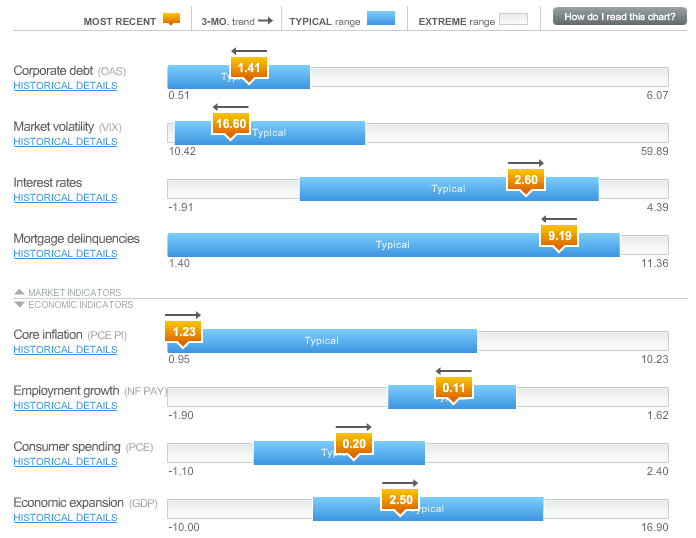

| Posted: 25 Oct 2013 08:30 AM PDT |

| Posted: 25 Oct 2013 06:00 AM PDT My early morning reads, hand selected from our fine cellar of thought provoking concepts:

What are you reading?

Forward Guidance |

| Posted: 25 Oct 2013 04:30 AM PDT Its Friday, the day I like to step back and get all Zen on y’all. As promised yesterday, our subject this morning — indeed, over the past few months — is how to reduce the meaningless distractions in your portfolio (and your life). You want less of the annoying nonsense that interferes with your investing, and more of the meaty data that allows you to become a less distracted and more purposeful investor. This is a continual process. For me, finding moments of quiet contemplation to think things through is very important. Sometimes that means taking a walk through the woods, or sitting on a boat deck or merely relaxing in a hammock with no distractions. You may prefer meditation, jogging or yoga. Anything that allows you to get out of your self for a few is enough. My daily process of waking before dawn and writing things down is an enormous aid to me figuring out what I think, to refining my understanding of what is really going on and why. I liken it to an editing process. I spend most of my quiet time deciding what to eliminate. After this process, whats left is almost all signal, no noise. Here are some things you need to understand if you want to decrease the noise:

Your consistent focus should be to keep yourself concentrating on that which truly matters and learning to reduce or even better, ignore that which does not . . . If there is interest, I might expand this into a full WaPo column.

Previously: What Do You Control? (May 30th, 2013) Asking the Right Questions (July 18th, 2013) The Price of Paying Attention (November 2012) Who Do You Trust? (January 2008) Lose the News (June 2005)

|

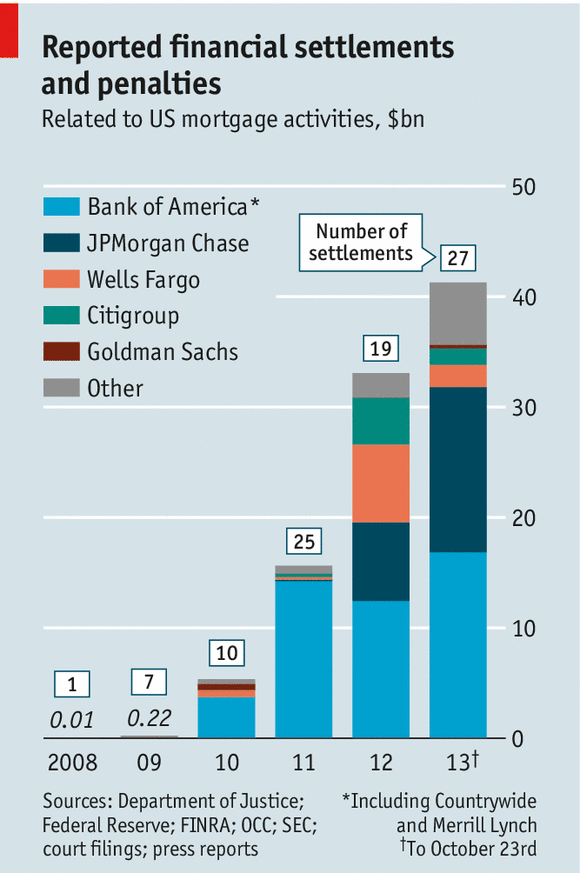

| US Bank Fines = $95 Billion Dollars Posted: 25 Oct 2013 03:30 AM PDT In less than 5 years, these 5 banks have amassed nearly $100 Billion dollars in fines n 81 settlements:

click for ginormous graphic

|

| JPMorgan: Fish Rot from the Head Posted: 25 Oct 2013 03:00 AM PDT JPMorgan: Fish Rot from the Head

The New York Times' spin of the tentative settlement of JPMorgan's latest myriad felonies begins early and runs throughout the article. JPMorgan and Attorney General Eric Holder have reached a common meme on their settlement: the Department of Justice (DOJ) and Holder are stalwarts who have demonstrated their toughness and JPMorgan is a model corporate citizen. The inconvenient facts that the senior officers of JPMorgan, Bear Stearns (Bear), and Washington Mutual's (WaMu) grew wealthy through the frauds that drove the financial crisis and that JPMorgan's senior officers will not be prosecuted and will not even have to repay the proceeds of their crimes never appear in the article. A word of caution is in order: I am discussing an article that is the product of leaks from DOJ and JPMorgan's press flacks about a tentative deal, so reality is certain to differ from the spin. This article is a longer discussion of the settlement than my October 22, 2013 CNN op ed. I am writing a side piece on the irony and implications of the civil and criminal investigation led by the U.S. Attorney for Eastern District of California, Benjamin Wagner. The NYT article suggests that his investigation is of former WaMu officers. WaMu was one of the world's largest criminal enterprises specializing in making fraudulent liar's loans and then selling the fraudulent loans to the secondary market through fraudulent "reps and warranties." These frauds destroyed WaMu. Dimon made the decision to buy WaMu – and to do so without receiving indemnification from the FDIC for any losses JPMorgan might suffer due to WaMu's massive frauds. JPMorgan purchased Bear and WaMu very quickly without conducting due diligence but that simply made the need for FDIC indemnification (or retention by the FDIC of Bear and WaMu's fraud liability) all the more essential given WaMu's notoriety on Wall Street for originating "liar's" loans and Bear notoriety that inspired the phrase: "Bear Don't Care." Here's the NYT's description of the tentative deal.

The rate of spin accelerates thereafter like an ice skater pulling her outstretched arms inward to hug her body.

To the NYT, and one prays earnestly only the NYT, the "reputational blow" to JPMorgan and Dimon does not come from JPMorgan, Bear, and WaMu committing the largest and most destructive financial crimes in history – but from JPMorgan paying a miniscule percentage of the damage its officers' frauds caused the world. The settlement does not require its controlling officers who grew wealthy from those crimes to return that wealth. The frauds by JPMorgan's officers occurred while Dimon was in charge. As I explained above, Dimon is also the one who thought, without due diligence and in the face of WaMu's and Bear's terrible reputation for fraud, that the purchase price from the FDIC was such a steal that JPMorgan should buy Bear and WaMu quickly without an FDIC indemnification lest a competitor snap them up. Dimon had tried to acquire WaMu at a higher price prior to its collapse in September 2008 but WaMu's incompetent management refused the deal. That deal also involved no FDIC indemnification and would have proved even more disastrous for JPMorgan. Similarly, Dimon was the proponent of buying Bear at a price he considered a steal – without any FDIC indemnification provision. Nevertheless, the NYT continues to portray Dimon as a genius. The NYT article repeats Dimon's claim that it is "unfair" to sue JPMorgan, which acquired Bear's assets and liabilities, without any indemnification agreement, for its liabilities. The article presents no contrary view or facts. If Dimon had demanded an indemnification agreement JPMorgan would have had to pay a far higher price to acquire Bear Stearns and WaMu. He cannot choose to take the lower price and then claim that it unfair to follow the normal rule that a firm's liabilities do not disappear because it is acquired by another firm. I am, of course, kidding. Dimon can and does choose to take the lower price and claim that it is an outrage to hold JPMorgan liable. Despite the fact that Dimon's claim is the actual outrage Holder is reported to have fallen for it. The NYT account is so delusional that it thinks that it speaks well of Dimon that he "steered JPMorgan through the crisis without a quarterly loss or major government scuffle." Hint: many of JP Morgan's frauds helped it avoid reporting "a quarterly loss." The fact that regulation had been so effectively destroyed by its anti-regulatory leaders and lobbying from the big banks, including JPMorgan, that they never even "scuffle[d]" with JPMorgan despite its thousands of felonies is why Dimon was celebrated for years for leading what was in reality a criminal enterprise instead of being denounced. Why does the NYT treat Dimon's "multifront battle" against the regulators who are (finally) trying to clean up the cesspool that is JPMorgan as valiant? Dimon needed to fight a "multifront battle" against the elite fraudsters he promoted, praised, and protected from justice rather than a "multifront battle" against the laggardly and none to tenacious regulators who finally stumbled over the frauds and sought to end them. Dimon is trying desperately to ensure that JPMorgan's senior officers, particularly Jamie Dimon, will be able to retain their positions, power, and immense wealth that are the product of the manifold frauds the senior officers led. He is enthusiastically offering the shareholders' money – not his – to buy "indulgences" for him and his senior cadre. The "$9.2 billion" in legal fees that JPMorgan expects to pay is largely a device to provide free legal representation to the senior officers. These practices are disgusting, not noble. The settlement with DOJ is a $9 billion (before taxes – probably far less after taxes) deal, not $13 billion. The $4 billion in purported "relief for struggling homeowners" reprises the cynical misrepresentation of the foreclosure fraud settlement in which the banks and DOJ agreed to call loan workouts that the banks would have done anyway because they minimized losses to the banks "relief for struggling homeowners." The NYT reporters have seen this propaganda before, but they parrot it again as if it were indisputable fact. Nine billion dollars is a large number, but relative to the damage JPMorgan's frauds caused it is miniscule – and that is without taking into account the fact that under normal remedies for repeated acts of fraud, and the remedies available under RICO, the DOJ could have trebled those damages. The $9 billion figure is not a testament to DOJ's toughness but a (dramatically understated) demonstration of the catastrophic damage JPMorgan, Bear's, and WaMu's senior officers caused our Nation and much of the world. The concluding sentences of the quoted passage demonstrate again the NYT's failure to understand the role that "accounting control fraud" played in driving the crisis and the appropriate criminal justice response to elite frauds. The reporters claim that not prosecuting JPMorgan or its senior officers or clawing back their wealth will:

The DOJ indulgences deal represents the continuing non-reckoning for Wall Street's senior officers. We need to begin with the cause of the crisis, which was not "outsize risk taking in the mortgage business." Accounting control fraud represents a "sure thing" – as Jamie Dimon explained in his March 30, 2012 letter to JPMorgan's shareholders: "Low-quality revenue is easy to produce, particularly in financial services. Poorly underwritten loans represent income today and losses tomorrow." To be more precise, poorly underwritten loans represent fictional reported "income today and [real] losses tomorrow." George Akerlof and Paul Romer made the same point in their 1993 article ("Looting: The Economic Underworld of Bankruptcy for Profit").

The reporters are correct that mortgage purchasers lost "billions" of dollars (if we clarify that to mean "hundreds of billions") – and that their recoveries will be a small fraction of those losses because if the fraudulent mortgage originators and fraudulent sellers of mortgage products (MBS and CDOs) "backed" by those fraudulent loans were made whole for their losses dozens of the world's largest banks would fail. JPMorgan's shareholders may suffer some loss, but the elite perpetrators, the senior officers, whose frauds made them wealthy and caused the crisis will not be prosecuted and will not have their wealth "clawed-back." Why exactly the NYT believes the public should find such a result "cathartic" is beyond me. The NYT article then asserts its meme of DOJ toughness, again as "fact."

Yes, that is how far the "Justice" Department has fallen – it claims to reporters (who then regurgitate the meme as unassailable "facts") that DOJ has scored "a major victory" because JPMorgan is "allow[ing]" DOJ to investigate its crimes. Two news flashes to Holder and the NYT – DOJ does not need JPMorgan's permission to investigate and prosecute JPMorgan and the necessary implication of the story is that the DOJ has only preserved the right to investigate and prosecute this one subset of JPMorgan's myriad felonies. For tens of thousands of JPMorgan felonies the deal will remove the DOJ's authority to investigate and prosecute. This passage from the article must also be read in conjunctions with this earlier segment.

As white-collar criminologists we joke about "the vice president in charge of going to jail." DOJ, for example, is prosecuting two minnows involving the London Whale frauds. (Notice that the article strips away any reference to the frauds and simply notes a "$6 billion trading loss.") The minnows' unpardonable crime is that they lost money and reduced Jamie Dimon's bonus and that they did so at an inconvenient time when Dimon's lobbyists were about to gut the "Volcker rule" barring proprietary trading. The inconvenient fact is that Dimon has turned JPMorgan into the largest proprietary trading operation in history (in violation of the everything the Volcker rule was intended to accomplish) and the London Whale's losses demonstrated that Volcker was right and Dimon was wrong. But did you notice the key word: "former?" It appears that DOJ isn't even willing to prosecute currently employed minnows in connection with the sales of tens of billions of dollars of fraudulent loans through fraudulent reps and warranties. If the article is accurate, DOJ is only investigating "former employees." Any meme that aims to make Holder heroic is bound to collapse in farce. Consider what these deals that stop investigations mean, particularly because they have been the norm in response to this crisis. Dimon's goals in priority order are: (1) avoid prosecution, (2) keep his wealth, (3) keep his job, and (4) prevent any investigation that makes public the facts of JPMorgan's, and its senior officers' frauds. Dimon and his peers are desperate to avoid what happened when we investigated prosecuted the elite S&L frauds. Every civil action, enforcement action, and prosecution put facts in the public record that journalists could freely cite without fear of being sued for libel or slander. Those facts demonstrated widespread fraud by elites. As the public came to understand these facts their view of the nature of the S&L debacle, which had been crafted by the CEOs, business reporters, and economists as the same "outsize risk taking" meme that is dominant today changed. The public realized that the control frauds used accounting fraud as their "weapon of choice" to produce a "sure thing" and avoid having to win a risky gamble. The political contributions that the S&L control frauds used to curry political allies to counter-attack us as regulators for daring to re-regulate the industry and hold them accountable for their crimes became an embarrassment for their politicians. Elected officials rushed to donate to charity political contributions they had received from fraudulent S&Ls. The elite frauds' greatest strength, their political influence, became a liability. As regulators, we knew we had won when Representative Frank Annunzio, one of the most vociferous allies of the worst frauds began wearing a button that was six inches in diameter and read: "Jail the S&L Crooks!" It was totally cynical on his part, of course, but it proved how much our investigations and efforts to hold the elite frauds accountable had changed the political dynamics. We didn't simply reduce the effectiveness of what had been the elite frauds' greatest strength – we turned their political contributions into a crippling liability. This all came at a price. Many of us still bear the scar tissue, but we would all do it again. Dimon and his peers are not stupid. They realize that even the NYT reporters will turn on them with a vengeance if competent investigations are ever conducted and the findings made public about the hundreds of fraudulent lenders whose literally millions of frauds drove the crisis. The CEOs' paramount strategic objective is to prevent real investigations staffed by vigorous financial regulators working with FBI agents that lead to hundreds of grand jury investigations of elite bankers and civil suits, enforcement actions, and prosecutions that make public the facts about the elite frauds that drove the crisis. The elite bankers and their political lackeys' greatest fear is that the public will learn the facts about the fraud epidemics that drove the crisis. One testament to this fear is indirectly, and unintentionally, revealed by the NYT article.

Why doesn't the NYT "question why no top Wall Street executives have been charged criminally for the [criminal, not "risky"] acts that triggered the crisis? One would think that this is precisely the kind of question that a great paper would ask even if it was the dominant home town industry's elite leaders that were most culpable. Recall that the fact that, for example, the FHFA in its capacity as conservator for Fannie and Freddie lacks the legal authority to prosecute does not reduce the significance of the fact that its investigations demonstrated endemic fraud in sales of fraudulent mortgages to Fannie and Freddie through fraudulent reps and warranties. Fraud is criminal even if Holder is too spineless to prosecute it. The NYT refuses to play it straight, which is why it uses the phrase "risky acts" rather than the word that (far from vigorous) government investigators have repeatedly used to describe their findings – "fraudulent." Again, it implicitly asserts as if it were undisputed fact that the crisis was driven by "risky [non-criminal] acts. " The NYT article is so cravenly bowdlerized that it never uses the word "fraud." I do not think the reporters would dare to expunge the word that is essential to understand the central public policy issue relevant to the article if Holder and his flacks were using the "f" word and expressing moral outrage that America's largest bank was a criminal enterprise that committed tens of thousands of frauds over the course of at least a decade. But the NYT far outperforms its standards for sycophancy in this passage:

I've explained why it is not "unfair" to sue JPMorgan for Bear's frauds. What is "unfair" is that the article provides no response of Dimon's claim of unfairness. It is the portrayal of "JPMorgan's board," however, as "conciliatory" that raises the article into an altered state of transcendent sycophancy. In any sane world the banking regulators would have demanded the resignation of JPMorgan's board years ago for their failure to exercise their fiduciary duties. On their watch, JPMorgan has become one of the largest and most destructive criminal enterprises in history and the Board has praised and protected Dimon rather than firing him and replacing him with a CEO who would create "an ethical tone at the top." JPMorgan is getting away with tens of thousands of frauds that made its senior officers wealthy and helped drive the financial crisis without any prosecutions of the corporation or its senior officers. Its board should be praying to whatever gods they worship in thanksgiving that Holder is the spineless Attorney General willing to sell the modern indulgences that give senior Wall Street officers and their banks immunity from prosecution and allow them to keep the wealth they gained from their frauds. The NYT has achieved epic levels of unintentional self-parody with its claim that it is JPMorgan's board that is "conciliatory" in being willing to use the shareholders' money to pay over $9 billion in additional legal and investigative fees and $9 billion in fines as the purchase price of the indulgence to ensure that none of the culpable senior officers are held accountable for their crimes or are stripped of their fraudulent proceeds. Could someone remind me whether the $18+ billion in shareholder money spent to protect the senior officers from accountability is being paid to meet the bank's fiduciary duty of loyalty or its fiduciary duty of care to its officers? I'm having some difficulty formulating my question because I am so ancient that my obviously faulty memory was that it was the officers and board members who owed fiduciary duties to the bank and its shareholders. Dimon and the board members he selects and dominates demonstrate through their actions that they believe that the bank exists to enrich them. The article commiserates with JPMorgan's board because it is purportedly faced with "vexing" "regulatory problems" about a "trading loss" and an "inquiry into the bank's credit card products." Yes, how "vexing" it must be for the poor board. It would probably be even more "vexing" if the board were to eschew euphemisms and instead describe its real "problems" which are not "regulatory" but the serial commission of massive frauds. JPMorgan's fraud "problems" were created by JPMorgan either directly or through purchases of two notorious control frauds (Bear and WaMu) that it knowingly made without indemnification and with the approval of JPMorgan's board. JPMorgan's problems are recurrent frauds led or induced through perverse compensation systems created by JPMorgan's (and Bear's and WaMu's) senior officers. JPMorgan officers violated multiple laws in covering up the London Whale's trading losses. The other nine areas of massive felonies (that according to an earlier Wall Street Journal story are also part of the deal) are also "problems" not because of regulations but because of laws and standards of ethics. These ten (and growing) areas of criminality would have led any functional board – years ago – to fire Dimon and institute an immediate top to bottom scrub to find the problems, fix them, "claw back" the officers' compensation, fire the leaders of the frauds, remove the perverse compensation systems, prevent insane acquisitions of control frauds like Bear and WaMu, make criminal referrals against the officers and employees who committed the frauds, and vigorously aid the prosecution of those officers and employees. JPMorgan's board has repeatedly failed to take these actions. It cannot even bring itself to vote to remove Dimon as Chairman and appoint an independent Chairman who would reduce Dimon's disastrous domination of JPMorgan. Fish rot from the head – and JPMorgan is rotten. The inability of the NYT to smell the stink after ten disclosures of large scale JPMorgan fraud schemes raises the question: how many frauds are JPMorgan allowed to commit before the New York Times is willing to use the "f" word? Of course, the same facts show that the rot at DOJ emanates from Holder. |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

{kind=link}

0 comments:

Post a Comment