The Big Picture |

- Payday Lending: New Research and the Big Question

- TBP Conference Schedule

- 10 Thursday PM Reads

- Where the Uninsured Are

- Weakest Part of Presidential Cycle

- 10 Thursday AM Reads

- Obama to Harwood: “Wall St Should be Worried”

- TBP 2013: Fireside Chat with Trading Legend Art Cashin

- Debt Limit, The Fed, Interest Rates: Day 2 of Government Shutdown

- What Investors Should Know About Obamacare

| Payday Lending: New Research and the Big Question Posted: 04 Oct 2013 02:00 AM PDT |

| Posted: 03 Oct 2013 05:15 PM PDT |

| Posted: 03 Oct 2013 01:30 PM PDT My afternoon train reading:

What are you reading? |

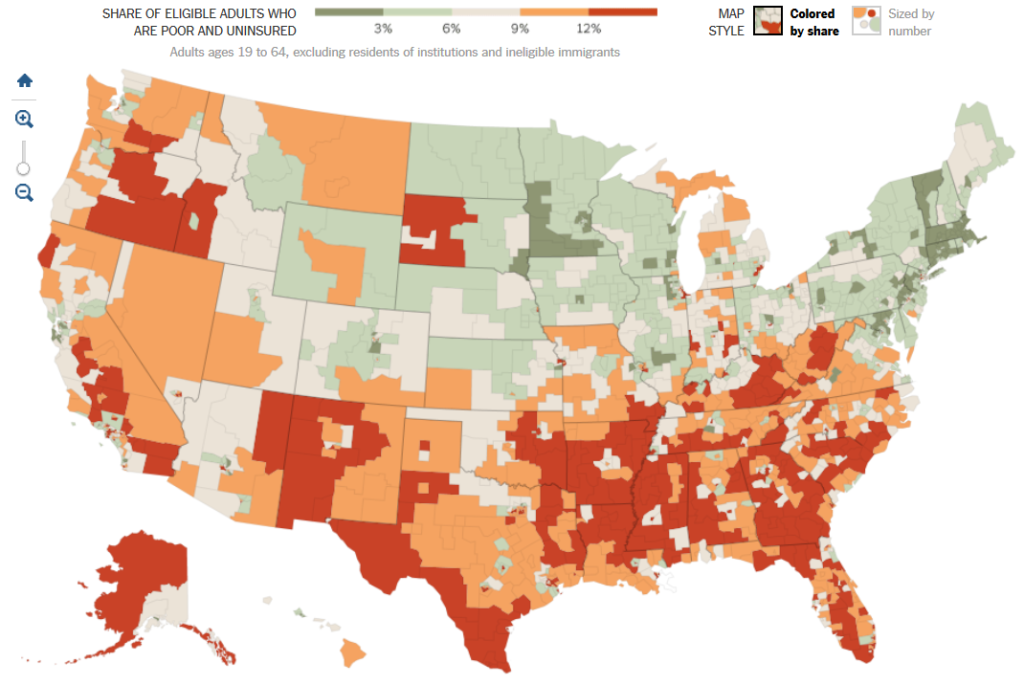

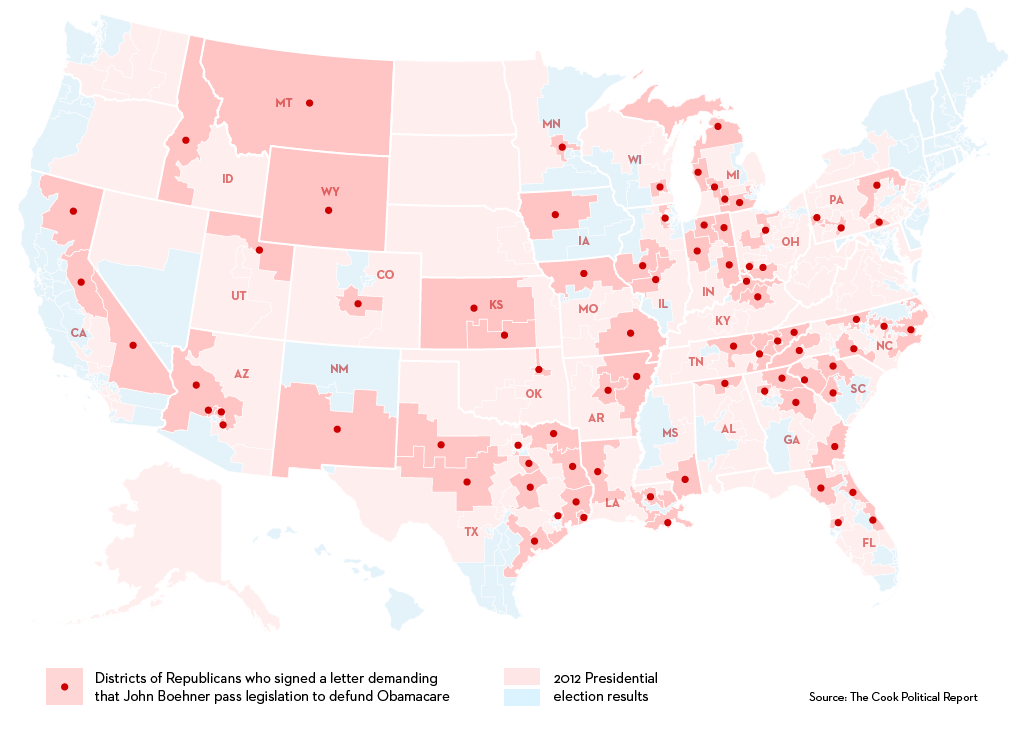

| Posted: 03 Oct 2013 11:30 AM PDT click for ginormous mao Source: NYT Update: Phil in comments adds this graphic:

This detail about where the uninsured live was rather surprising:

The headline is wrong — it should read Millions of Poor Are Left Uncovered by their State Legislatures and Governors.

Source: http://www.nytimes.com/2013/10/03/health/millions-of-poor-are-left-uncovered-by-health-law.html

|

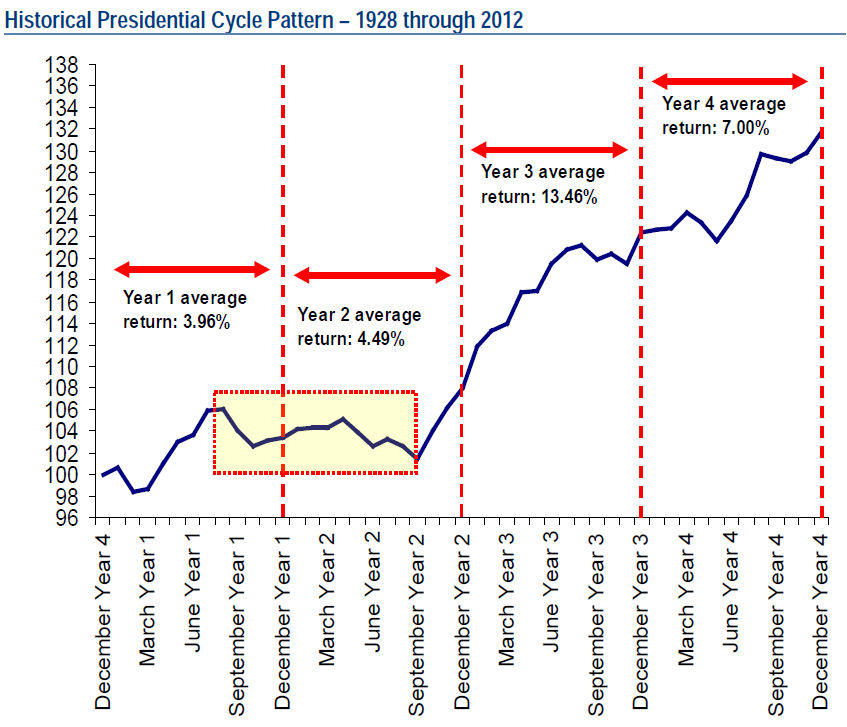

| Weakest Part of Presidential Cycle Posted: 03 Oct 2013 08:30 AM PDT Market risk: Weakest part of Presidential Cycle starts in mid 2013 (Jul/Aug peak) click for ginormous chart

From Merrill:

|

| Posted: 03 Oct 2013 06:45 AM PDT My morning reading:

What are you reading?

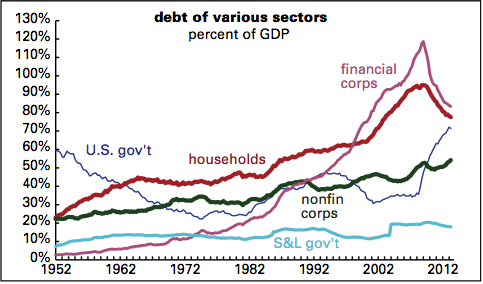

Debt of various sectors |

| Obama to Harwood: “Wall St Should be Worried” Posted: 03 Oct 2013 06:00 AM PDT |

| TBP 2013: Fireside Chat with Trading Legend Art Cashin Posted: 03 Oct 2013 04:30 AM PDT Of all the events going down at next week’s The Big Picture Conference, the one I’m probably most excited about is the fireside chat with Art Cashin that will be closing the program. Art made mention this morning in his Cashin’s Comments note for UBS:

Art’s spent fifty years on the floor of the NYSE and has quite literally seen it all. He’s got tons of great stories to tell, I can’t wait to watch it go down. If you don’t have your ticket yet, click here:

|

| Debt Limit, The Fed, Interest Rates: Day 2 of Government Shutdown Posted: 03 Oct 2013 04:00 AM PDT Debt Limit, The Fed, Interest Rates

"Today's shutdown is the culmination of over two years of political turmoil in the wake of the Budget Control Act of 2011, which capped federal spending (sequestration) and brought to the forefront the need to reign in federal spending." October 1, 2013, John Silvia, chief economist of Wells Fargo Securities and my regular fishing partner at Leen's Lodge. John was chief economist to the US Senate Banking Committee in an earlier time in his career. As we watch the Washington theatre surrounding the debt limit, the budget, and sequester squabble play out, we do not hear a single word uttered about the impact the Federal Reserve's activity has on the budget. Hmm? The Fed's QE assuredly has implications for the nation's bottom line; and the tapering of QE, when it happens, will change the picture yet again. Current Fed policy impacts the budget in two ways. First, the Fed's very low interest rate policy means that the portion of the federal budget required to pay interest on the national debt is currently lower than it would otherwise be. We could go through a detailed exercise to guess what the normalized interest rate may become after the Fed has stopped tapering and has neutralized or sterilized its expanded balance sheet. This would be a wild guess since we do not know the rate of change in the size of the Fed's balance sheet over the next few years and we do not know what the interest rates will be once the Fed reaches a neutral stance. Still, we do know what the mechanisms are, and it behooves us to understand how they will work and what the scale of the impact, in broad terms, might be. We do assume that the federal budget is likely to be running some lower level of deficit once QE has been tapered, and we estimate that marketable federal debt in the hands of the US public and the rest of the world is likely to be around 75-80% of our GDP. So we can guess that we will have about $15-18 trillion in outstanding non-federally held debt before the end of the decade. We guess that GDP will exceed $20 trillion by then. The Fed will eventually be resetting interest rates, and we can therefore guess that every 1% change in rates equates to about $150-180 billion in additional annual interest expenditures in the federal budget. If the interest rate now is, say, 2 points lower than it would otherwise be without Fed intervention, we can conclude that we would otherwise be incurring about $300-360 billion of interest expense that is not showing in the federal budget plan today but is likely to appear in the future, as and when the Fed neutralizes its policy. Of course, we do not know the maturity distribution of that debt at this time, so we are just guessing that the average interest rate on all the federal debt will be 2% higher around the end of the decade. The second dimension of the Fed's impact on the budget consists of the remittances that the Fed sends to the Treasury each year. The amount is approaching $100 billion and comprises the net income collected by the Fed because of its large holdings of federal securities. Remember, the Fed currently is creating $85 billion a month and using it to buy intermediate and longer-term US Treasury debt and federally backed mortgages. The Fed's balance sheet size is about $4 trillion and rising. This number is up from under $1 trillion prior to the Lehman-AIG collapse. The Fed's current cost of funds on the liability side of its balance sheet is zero for currency in circulation around the world and 0.25% in interest that it pays to banks for their excess reserve deposits at the Fed. Once the Fed starts tapering and when it reaches neutrality, remittances to the Treasury will peak. As the Fed normalizes interest rates and allows its assets to roll off, the remittances to the Treasury will decline. Right now they are part of the federal revenue and work to reduce the deficit. When they decline, revenue drops. So we can say something like this. About $100 billion comes to the US Treasury from the Fed's unusual operations under the QE regime, which the Fed says it wants to wind down. Another projected $300 billion is evidenced in a smaller-than-otherwise deficit because the Fed's policy is focused on maintaining interest rates at lower levels than they would otherwise be. We know the Fed is targeting a 2% inflation rate, and we have a lot of history to suggest that such an inflation rate would lead, over time, to an average interest rate on Treasury debt of about 4%. We conclude that the change in Fed policy and the normalization of interest rates will be huge in federal fiscal finance. And its impact is not mentioned much in the current political fight. Yet a great part of the present debate is about this future interest cost. Lastly, we want to offer a worst-case example of what the interplay between a central bank and a government can lead to. The case study is Argentina. The quote below comes to us from another fishing friend who has in-depth knowledge of Argentina. We will keep him anonymous since the Argentine government is known for certain vindictive practices. He wrote:

We thank both our friend for the comments and hope some of our dysfunctional politicians in both political parties read it. Of course, that assumes they can read. Hmmmmmmmmmm? ~~~ David R. Kotok, Chairman and Chief Investment Officer |

| What Investors Should Know About Obamacare Posted: 03 Oct 2013 03:00 AM PDT Click for video |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment