The Big Picture |

- Is (Risk) Sharing Always a Virtue?

- Terry Jeffrey, Hack Extraordinaire (Fun with Numbers Again)

- Retail Theater: Beware of Bad Shopmas Data!

- 10 Weekend Reads

- Audi RS5 Cabriolet

| Is (Risk) Sharing Always a Virtue? Posted: 08 Dec 2013 02:00 AM PST Is (Risk) Sharing Always a Virtue?

The financial system cannot be made completely safe because it exists to allocate funds to inherently risky projects in the real economy. Thus, an important question for policymakers is how best to structure the financial system to absorb these losses while minimizing the risk that financial sector failures will impair the real economy. Standard theories would predict that one good way of reducing financial sector risk is diversification. For example, the financial system could be structured to facilitate the development of large banks, a point often made by advocates for big banks such as Steve Bartlett. Another, not mutually exclusive, way of enhancing diversification is to create a system that shares risks across banks. An example is the Dodd-Frank Act mandate requiring formerly over-the-counter derivatives transactions to be centrally cleared. However, do these conclusions based on individual bank stability necessarily imply that risk sharing will make the financial system safer? Is it even relevant to the principal risks facing the financial system? Some of the papers presented at the recent Atlanta Fed conference, “Indices of Riskiness: Management and Regulatory Implications,” broadly addressed these questions and others. Other papers discuss the impact of bank distress on local economies, methods of predicting bank failure, and various aspects of incentive compensation paid to bankers (which I discuss in a recent Notes from the Vault). The stability implications of greater risk sharing across banks are explored in “Systemic Risk and Stability in Financial Networks” by Daron Acemoglu, Asuman Ozdaglar, and Alireza Tahbaz-Salehi. They develop a theoretical model of risk sharing in networks of banks. The most relevant comparison they draw is between what they call a “complete financial network” (maximum possible diversification) and a “weakly connected” network in which there is substantial risk sharing between pairs of banks but very little risk sharing outside the individual pairs. Consistent with the standard view of diversification, the complete networks experience few, if any, failures when individual banks are subject to small shocks, but some pairs of banks do fail in the weakly connected networks. However, at some point the losses become so large that the complete network undergoes a phase transition, spreading the losses in a way that causes the failure of more banks than would have occurred with less risk sharing. Extrapolating from this paper, one could imagine that risk sharing could induce a false sense of security that would ultimately make a financial system substantially less stable. At first a more interconnected system shrugs off smaller shocks with seemingly no adverse impact. This leads bankers and policymakers to believe that the system can handle even more risk because it has become more stable. However, at some point the increased risk taking leads to losses sufficiently large to trigger a phase transition, and the system proves to be even less stable than it was with weaker interconnections. While interconnections between financial firms are a theoretically important determinant of contagion, how important are these connections in practice? “Financial Firm Bankruptcy and Contagion,” by Jean Helwege and Gaiyan Zhang, analyzes the spillovers from distressed and failing financial firms from 1980 to 2010. Looking at the financial firms that failed, they find that counterparty risk exposure (the interconnections) tend to be small, with no single exposure above $2 billion and the average a mere $53.4 million. They note that these small exposures are consistent with regulations that limit banks’ exposure to any single counterparty. They then look at information contagion, in which the disclosure of distress at one financial firm may signal adverse information about the quality of a rival’s assets. They find that the effect of these signals is comparable to that found for direct credit exposure. Helwege and Zhang’s results suggest that we should be at least as concerned about separate banks’ exposure to an adverse shock that hits all of their assets as we should be about losses that are shared through bank networks. One possible common shock is the likely increase in the level and slope of the term structure as the Federal Reserve begins tapering its asset purchases and starts a process ultimately leading to the normalization of short-term interest rate setting. Although historical data cannot directly address banks’ current exposure to such shocks, such data can provide evidence on banks’ past exposure. William B. English, Skander J. Van den Heuvel, and Egon Zakrajšek presented evidence on this exposure in the paper “Interest Rate Risk and Bank Equity Valuations.” They find a significant decrease in bank stock prices in response to an unexpected increase in the level or slope of the term structure. The response to slope increases (likely the primary effect of tapering) is somewhat attenuated at banks with large maturity gaps. One explanation for this finding is that these banks may partially recover their current losses with gains they will accrue when booking new assets (funded by shorter-term liabilities). Overall, the papers presented in this part of the conference suggest that more risk sharing among financial institutions is not necessarily always better. Even though it may provide the appearance of increased stability in response to small shocks, the system is becoming less robust to larger shocks. However, it also suggests that shared exposures to a common risk are likely to present at least as an important a threat to financial stability as interconnections among financial firms, especially as the term structure and the overall economy respond to the eventual return to normal monetary policy. Along these lines, I recently offered some thoughts on how to reduce the risk of large widespread losses due to exposures to a common (credit) risk factor.

Note: The conference “Indices of Riskiness: Management and Regulatory Implications” was organized by Glenn Harrison (Georgia State University’s Center for the Economic Analysis of Risk), Jean-Charles Rochet, (University of Zurich), Markus Sticker, Dirk Tasche (Bank of England, Prudential Regulatory Authority), and Larry Wall (the Atlanta Fed’s Center for Financial Innovation and Stability). |

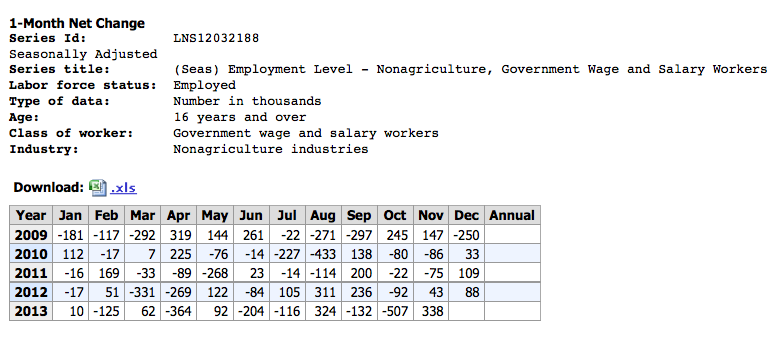

| Terry Jeffrey, Hack Extraordinaire (Fun with Numbers Again) Posted: 07 Dec 2013 12:45 PM PST @TBPInvictus here. In yet another stunning display of journalistic malpractice, Terry Jeffrey put out the following piece after last Friday’s NFP release:

Because it suited his (political) purpose, Jeffrey jumped on the Household Survey; looking at the Establishment Survey would not have provided such a dramatic headline. Indeed, it would have provided, for him, no usable headline at all. What Jeffrey seized on – a 338K gain over the month in government employees (41% of the 818K!!!) – fails to take into account that the previous month, when the Household Survey flagged a decline of 735K, 507K of those (a whopping 69%!!!) were government employees (interestingly, he did not report on that). That was, you know, when we had that government shutdown thing going on. These numbers are shown in the table immediately below. So the gain in November was essentially a reversal of the loss in October due to the government shutdown. This is exactly the same type of bullshit we see periodically with Reagan’s Million Jobs in One Month Miracle. One quick look under the hood and it all falls to pieces.

I hope to God that Terry Jeffrey never identifies himself as a journalist. I’d hope, rather, that he refers to himself as a charlatan or a montebank, devoid of any integrity whatsoever. See previously: Makers and Takers

|

| Retail Theater: Beware of Bad Shopmas Data! Posted: 07 Dec 2013 07:00 AM PST Retail theater: Beware of bad Shopmas data!

This weekend kicks off the official start of the seasonal gift-buying frenzy I call Shopmas! When it comes to retail, 'tis the season of artifice and deception. The retailers offer fake discounts via phony markdowns — no one pays full price for that, honey — or ship made-for-outlet-center goods that are not actually sold in the name-brand retail stores. In "The Dirty Secret of Black Friday 'Discounts'," the Wall Street Journal called it "retail theater." It noted that "in many cases, those bargains will be a carefully engineered illusion." The news media aren't any better. They breathlessly cover shopping as if it were an Olympic event. The big-box retailers play right into the coverage. Each year, we are regaled with stock footage of the 6 a.m. crush, a near-riot battle for the heavily discounted electronics doodad of which only a few are for sale. It is ugly and crass. I see a scene from "The Hunger Games" rather than a modern industrialized nation gratefully celebrating the bounty provided us. Footage of people camped out at Best Buy or elsewhere is not remotely a celebration. Rather, it's a reminder of just how economically distressed a large percentage of our populace is. It's a Barbie, for crying out loud — do you really need to LEAVE YOUR FAMILY FOR THREE DAYS TO camp out for that? The media mindlessly follow a script written by retailers. The footage, the news reports, the surveys, the measures of foot traffic, all serve to create a false impression of a huge shopping orgy. You better join in, or you will get left behind! Only you won't. As we first discussed in this space two years ago (and elsewhere almost a decade ago), these reports are meaningless. Don't fall for the nonsense. There are several offenders, the most egregious of which is the Holiday Consumer Intentions and Actions Survey put out by the National Retail Federation. As we showed previously, these surveys do not measure retail sales — they measure "consumer intentions." History teaches that you humans are terrible judges of your future behavior. You have no idea what you are going to do tomorrow, let alone next month. But the NRF survey ignores that simple fact, asking consumers to recall what they spent last year and to anticipate what they will spend this year. The first question is a wild guess as to past behavior; the second question is unreliable speculation about future behavior. Take the net difference between these two wild guesses and — voila! — you get this year's holiday sales numbers. Only you don't. As the numbers show unequivocally, the data have zero correlation with actual retail sales numbers. Some years, it is off by a lot; other years, it is off by even more. The 2009 survey projected an unprecedented collapse in spending by 43 percent; instead, holiday sales rose year over year by 3 percent. My favorite piece of mathematical comedy is this line in the NRF methodology: "The consumer poll has a margin of error of plus or minus 1.0 percent." That may be the funniest thing any statistician will read this holiday season. The NRF report is just the frosting on the headless gingerbread man cookie when it comes to bad holiday shopping data. Runner-up is the ShopperTrak Retail Foot Traffic report. It is a squishy head count of shoppers at "retailers, mall developers and entertainment venues." Its claims about foot traffic hardly correlate with actual sales. Yet it is reported as if it were important or accurate. The retail kudzu arrives earlier each year. Shopmas now begins on Thanksgiving Day. Apparently, escaping the families you cannot stand to spend another minute with on Thanksgiving Day to go buy them gifts is how some Americans show their affection for one another. Weird. For those who cannot wait for the official retail data to come out, look at data that actually measure retail sales. I have not found a perfect substitute, but MasterCard SpendingPulse looks pretty good. It is based on the credit card giant's "near-real-time purchase data" and runs through sophisticated models. Pardon me for being such a curmudgeon, but this is not what Thanksgiving is supposed to be about. Faux data, ginned-up excitement and consumerism have nothing to do with giving thanks for whatever bounty may have come your way this year. Instead of getting sucked into the nonsense, you could always wait a month for the December retail sales data. If you do that, however, you might actually have to spend time with your family, giving thanks. Ritholtz is chief investment officer of Ritholtz Wealth Management. He is the author of "Bailout Nation" and runs a finance blog, the Big Picture. Twitter: @Ritholtz. |

| Posted: 07 Dec 2013 04:30 AM PST Here are my longer form weekend readings:

What are you up to this weekend?

Central Banks Warn of Bitcoin Risks |

| Posted: 07 Dec 2013 03:00 AM PST Note this 450HP car lacks a manual option — perfect for you poseurs — and that means that the Audi RS5 is off my short wish list of cars. Audi RS5: Speed and style in the open air ~~~ 2013 Audi RS5 Cabriolet – WINDING ROAD POV Test Drive |

By

By

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment