The Big Picture |

- Why Do Banks Feel Discount Window Stigma?

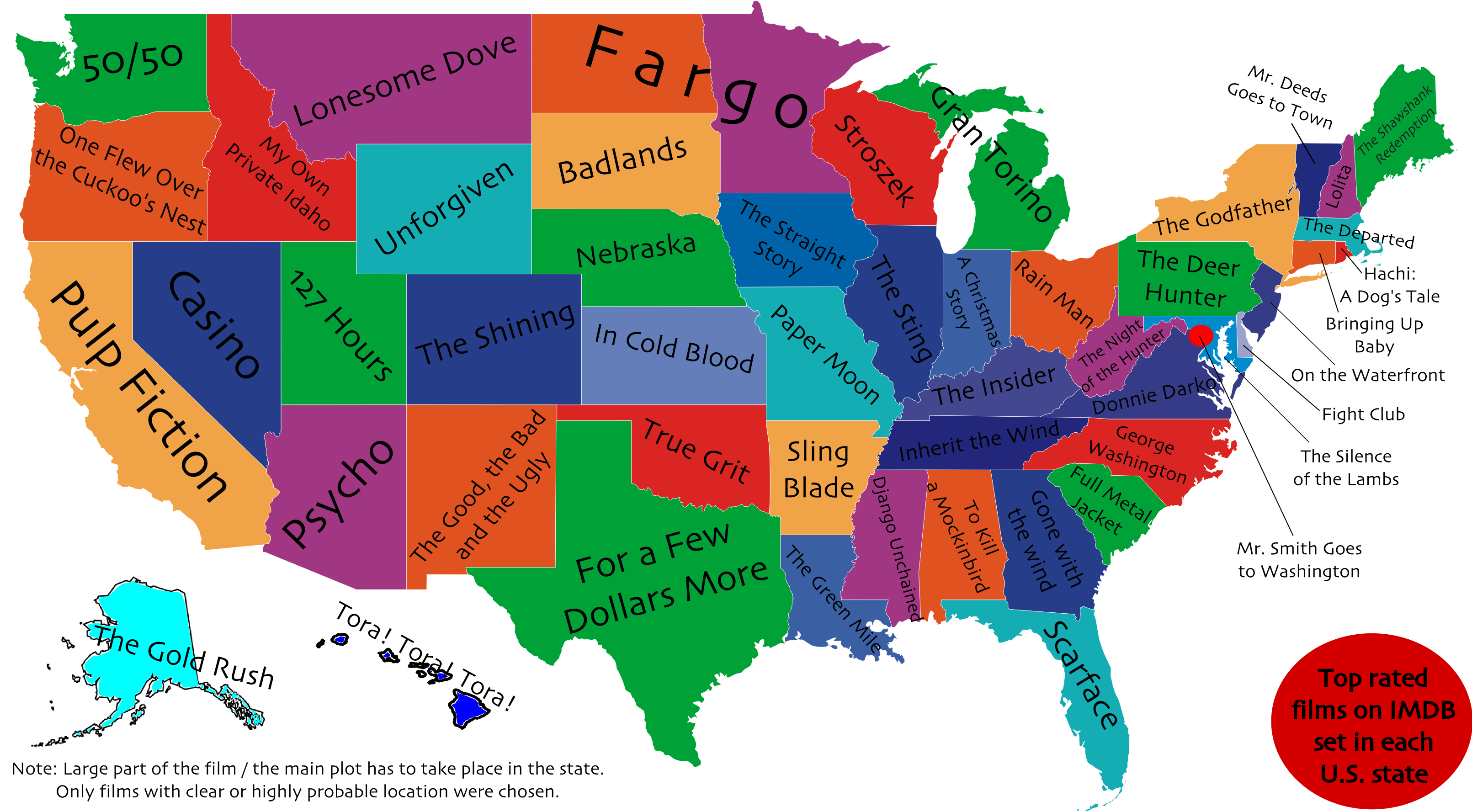

- Best Movie Set In Your State?

- The Eagles Reopen The Forum

- What Can You Learn from the Rise & Fall of Gold?

- 10 Weekend Reads

- Smallest, Faintest Galaxies of the Ancient Universe Spotted

- The Insensitivity of Investment to Interest Rates: Evidence from a survey of CFOs

| Why Do Banks Feel Discount Window Stigma? Posted: 19 Jan 2014 02:00 AM PST Why Do Banks Feel Discount Window Stigma?

Even when banks face acute liquidity shortages, they often appear reluctant to borrow at the New York Fed's discount window (DW) out of concern that such borrowing may be interpreted as a sign of financial weakness. This phenomenon is often called "DW stigma." In this post, we explore possible reasons why banks may feel such stigma. The problem of stigma has been a lingering issue throughout the history of the DW. Prior to 2003, banks in distress could borrow from the DW at a rate below the fed funds target rate. Because of the subsidized rate, the Fed was concerned about "opportunistic overborrowing" by banks. Accordingly, before accessing the DW, a bank had to satisfy the Fed that it had exhausted private sources of funding and that it had a genuine business need for the funds. Hence, if market participants learned that a bank had accessed the DW, then they could reasonably conclude that the bank had limited sources of funding. The old DW regime therefore created a legitimate perception of stigma. To address such stigma concerns, the Fed fundamentally changed its DW policy in 2003. In Regulation A, as revised in 2003, the Fed classified DW loans into primary credit, secondary credit, and seasonal credit. Financially strong and well-capitalized banks can borrow under the primary credit program at a penalty rate above the target fed funds rate (rather than a subsidized rate, as in the past). Other banks can use the secondary credit program and pay a rate higher than the primary credit rate. Finally, seasonal credit is for relatively small banks with seasonal fluctuations in reserves. For banks eligible for primary credit, the new DW is a "no-questions-asked" facility. Namely, the Fed no longer establishes a bank's possible sources and needs for funding to lend under the primary credit program. Instead, primary credit for overnight maturity is allocated with minimal administrative burden on the borrower. Hence, access to primary credit need not be motivated by pressing funding needs nor signal financial weakness. In other words, there's no structural reason why stigma should be attached to the new DW. Nevertheless, stigma concerns resurfaced in 2007 at the onset of the recent financial crisis. In fact, as adverse liquidity conditions in the interbank markets persisted at the end of 2007, the Fed had to put in place a temporary facility, the Term Auction Facility (TAF), which was specifically designed to eliminate any perception of stigma attached to borrowing from the DW. Further, as discussed in a previous post, there's strong evidence that banks experienced DW stigma during the most recent financial crisis. So why do banks still feel DW stigma? In a recent staff report, we explored different hypotheses related to factors that may exacerbate or attenuate DW stigma. To conduct our analysis, we compared the DW rate with the bids each bank submitted at the TAF between December 2007 and October 2008. As explained in our paper, it can be shown with a simple arbitrage argument that, absent DW stigma, a TAF bidder should never bid above the prevailing DW rate. We therefore interpreted a bank bidding above the DW rate as evidence of DW stigma. Then, we conducted an econometric analysis to identify a bank's possible determinants of DW stigma. Among the various hypotheses we tested, we report here the most interesting.

In summary, our study provided a better understanding of the reasons why banks may feel DW stigma. In particular, we found that the incidence of DW stigma was higher for foreign banks, banks that could be identified more easily, and banks outside the New York Federal Reserve District, as well as after financial markets became stressed. In contrast, we found no evidence that DW stigma may be due to a lack of coordination among banks when accessing the DW. Disclaimer

|

| Posted: 18 Jan 2014 04:30 PM PST click for ginormous version |

| Posted: 18 Jan 2014 02:00 PM PST I never thought I’d see Bernie play with them again. But it was that kind of night, a homecoming. No, we didn’t find out about the show on KMET, but we did all get in our cars and drive south to where a building always described as a wedding cake awaited our arrival.

Dolan told me they hired this company that put microphones all around the arena to ensure… But I could tell from the very first note, it was all anybody talked about, how good the show sounded. Usually you go to the arena and if you don’t know the song by heart, it’s indecipherable noise. But here lyrics that are questionable on the record emerge perfectly intelligible. As for the building itself… Much has been made of the high-backed chairs. But little has been told of the resculpting, wherein the bottom level of the loge has been removed and the floor is bigger and downstairs there are bars and restrooms and upstairs there are name brand restaurants, local fare like Pink’s and Carney’s, and a dedicated merch booth. Hell, you can even drink outside on the patio. Now they take your ticket before you ascend. But a building is nothing without people. And those in attendance were not the downtown crowd. The Forum always had a South Bay feel. There were plenty of Hawaiian shirts and no suits. And everybody was there to see the Eagles. Yes, right now the Fabulous Forum is the number one music venue in the world, a ton of money was injected to make it so. But almost no one will ever go there. Except for us. he natives and the transplants. Who understand finance is focused in New York and tech emerges from San Francisco, but there’s nowhere we’d rather be than Los Angeles. Randy Newman wrote a pretty good song. ut the heart of the Southern California experience is the Eagles. Because they too picked up and left to come here, to live free and make it. So funny aging, because you realize most people don’t make it. Many never try. But most miss the target. They’re afraid to work that hard, but mostly they’re afraid to look at themselves, if you’re not constantly evaluating and redressing your flaws you’re never going to get the brass ring. And that’s what the Eagles achieved, and have been on an endless victory lap ever since. They didn’t expect it to be this way. It wasn’t until the country cover album “Common Thread” demonstrated how much love was still extant for the band, when their greatest hits album exceeded the sales of “Thriller,” that they reunited. And sure, their solo careers never flew as high, but really we needed them. To remind us. Of how it once was and still could be. Boy could they play. And sing too. It’s so different from the great unwashed of today who focus on fame and refuse to practice. But that’s all the Eagles did. See the Beatles and rehearse in the garage. Every baby boomer alive picked up an instrument after the Fab Four appeared on “Ed Sullivan.” But most of us gave up. A few soldiered on. Glenn left Detroit. Don left Texas. And they came to the City of Angels to discover… No one cared. That’s how it is when you’re not famous. You’re irrelevant. You find others with the same problem, whether it be Jack Tempchin in San Diego or J.D. Souther in from the flatlands. And you play in bands, and you make friends and you get enough experience until you believe…you’re ready. That’s what the Eagles did. After backing up Ronstadt they got hooked up with Bernie Leadon and… They rented a rehearsal hall in the Valley for six bucks an hour and hunkered down. They had an immediate hit, “Take It Easy,” and then were exiled into the wilderness. Until suddenly, by a fluke, a random radio request, “Best Of My Love” from their third album, was played on a midwest station and caught on and became their first number one. The band went from struggling to selling out stadiums. It happens just about that fast. And then they proceeded to record “Hotel California” and become legends. That’s the truth, you can never leave. Oh, there’s an occasional east coaster who doesn’t get it, who moves here for a while and returns, but the rest of us…we’re lifers. And we don’t need to convince you. We just need to go to the Forum and revel in our blessedness. There’s no coat check, why would there be? There’s plenty of parking, Los Angeles doesn’t believe in public transportation, it’s the suburbs on steroids. And we sit on our aged asses and listen to…the way it used to be. You remember that, don’t you? Maybe you don’t. Well, let me tell you. First and foremost you had to know how to play. And if you were good and lucky you got a manager and a record deal and some radio action. And if you were really good, it continued. And you lived an undocumented life so wild and crazy, so fulfilling and fetter free, that to this day everybody wants to be a “rock star,” whatever that means. Want to know what it used to mean? You destroy a hotel room out of boredom and your manager peels off hundreds to make it go away and no one really cares, because the very next night you’re going to make tons more dough. You can get laid every day. By different women. And you do. There is no AIDS. And they’re lining up to blow you. The world runs on sex, just ask the President of France, and rock stars and their music were the epicenter of it. Still are. You stay in the finest places and everyone knows your name. You can barely open your wallet because everybody wants to give you stuff for free. And everybody hangs on every word. That’s the essence of the game, your music. Made only by you only for us. There are no middlemen. Corporations are abhorred. The label has no input. You lay it down raw and we want to hear everything you have to say. That’s when album rock began. Not when they created the LP, but when classic acts could fill it. So when you sit in the Forum and hear Bernie sing “Train Leaves Here This Morning” as Don and Glenn strum along on their guitars… You’re taken right back to the summer of ’72, when you couldn’t drive down the boulevard without hearing that acoustic intro with the refrain telling us to take it easy. You knew every note. And when the band plays “Witchy Woman,” you revel in what is a greatest hit, even though you’ll find it on no chart. And when Don Henley sings the “Doolin’ Dalton/Desperado (Reprise)” you’re almost ready to pick up the tonearm and start the record again after this album ending cut. And when Frey tells us he was inspired by the Beach Boys, mere miles from Hawthorne, where the Wilsons grew up and made their initial music, and that they’ve rearranged “Heartache Tonight” in tribute to “Barbara Ann” from “Beach Boys’ Party”… WE OWNED THAT ALBUM! WE KNOW WHAT HE’S TALKING ABOUT! WE DON’T WANT TO GO OUT FOR A PEE AND TEXT OUR FRIENDS, WE WANT TO STAND IN JOY AND CLAP ALONG! Joy. That’s what last night was about. A retrospective of what once was, when we were growing up and the whole world was in front of us. But it’s already gone at this point. At least most of it. But to be able to return to the scene of the crime with the greatest exponent of that era… That’s heaven. P.S. You had to be there to hear the roar after Glenn Frey introduced Don Henley, the singer-songwriter-drummer-guitarist from Linden, Texas. It was loud and vociferous and never would have stopped if it hadn’t been cut short to introduce Joe Walsh. There’s nowhere else you can get this hit. No matter how rich you are. We revere our rock stars. Not for their fame, but their talent! P.P.S. Yes, Joe Walsh keeps the second half of the show together. And reminds us there once was a paradigm known as the “guitar hero.” Those were the days. P.P.P.S. “Life in the fast lane, surely make you lose your mind.” And your life. Some didn’t make it, they’re six feet under or have been cast to the wind. But these guys survived and can still do it every bit as well and we were there to see it and if that doesn’t make you feel completely alive, you’re dead.

Take the 405 to Manchester. Or La Cienega from downtown. Southward as you go. Because five more times this month the biggest band in Southern California history, in American history, is demonstrating what it was once like. When we were addicted to the radio, when going to the record store was a pilgrimage as important as a trip to Mecca or Jerusalem. When we couldn’t wait to get home and break the shrinkwrap and hear what our favorites had to say. And there will be moments when there are so many guitars on stage you’d think you were at Guitar Center, or Fred Walicki’s Westwood Music. But late in the show, the assembled multitude will stride up to the mics and sing a cappella the Steve Young song we know by heart from their live album. And you’ll close your eyes or look to the sky and remember…not only the music, but the sex, the alcohol and the dope. Doing nothing without the music playing, going to the gig because that’s what you did, never finding it too expensive to attend. |

| What Can You Learn from the Rise & Fall of Gold? Posted: 18 Jan 2014 07:00 AM PST A gold enthusiast? Listen to the head — and history.

How much money did you make from gold's spectacular run from under $500 a decade ago to more than $1,900 two years ago? How much did you lose from the 38 percent collapse since its September 2011 peak? Last year was the first time this century that gold ended the year down from when it began. But gold investors have been making investing and trading errors for what seems like forever. The mania for gold, like all manias preceding this one, is ending badly. And while gold may yet establish a comeback, much of the damage has already been wrought. More importantly, did you learn anything from that epic boom and horrific bust? If the savvy observer approaches gold's rise and fall as an objective history lesson, there are broad principles to be derived and behaviors to be avoided. That is, if humans can ever begin to learn from experience. Consider the following lessons as applicable to not just gold, but any investment: 1 . Beware the Narrative: As we noted in July, everybody loves a good story. The narrative form has been around for thousands of years longer than the written word. It is how humans transfer information. We love a tale of heroes and villains and conflicts requiring a neat resolution. In finance, storytelling is a major part of any sales pitch, and gold is no different. The credit crisis and Great Recession created the perfect environment for the gold narrative to prosper. Bailouts and rescues and global coordinated central bank actions played right into the hands of the gold bug story. Both quantitative easement and zero-interest-rate policies were the perfect foils for what was described as inevitable: The collapse of the dollar (and all "fiat currency") and imminent hyperinflation. Instead, the dollar hit three-year highs; inflation was nowhere to be found. Even as the Federal Reserve kept up its policy of "QE infinity," gold kept heading lower. The problem with all of this was that even as the narrative was failing, the storytellers never changed their tale. When it comes to investing, there are two problems with that kind of storytelling: It ignores actual data. And it makes investors feel good, regardless of what is actually happening. 2. Carefully Examine New Investment Products: The creation of the SPDR Gold Trust exchange-traded fund (NYSE: GLD) was a major shift in how investors could buy gold. More commonly called the Gold ETF, GLD was described as "the innovation that opened gold investing to the masses." The back story is fascinating. GLD was a creation of the World Gold Council — an organization created by global gold-mining companies for the sole purpose of developing markets — after "two decades of depressed prices and a growing glut of the yellow metal," as the Wall Street Journal put it. It was enormously successful: Lipper called GLD the "fastest-growing major investment fund ever." During its bull run, the fund was buying $30 million of gold daily. By 2012, the SPDR Gold Trust was the second-biggest equity holding after Apple in self-directed 401(k) plans Salesmen always need something to sell. In GLD, they found a perfect vehicle to pull in the masses. 3. Ignore History at Your Own Peril: (or, Everything eventually becomes a trade): You cannot be in the market very long and grow attached to anything, as everything eventually disappoints you. I call this my universal entropy theorem of investing, and it is why everything from Microsoft to the 10-year bond, from Apple to gold, eventually goes to hell. (Just look at how often stocks get tossed from the Dow Industrials.) Gold has frequently had these run-ups only to get trounced eventually. See 1974-76, 1981, 1983-85, 1987-2000, 2008 and now 2011-14. 4. Leverage is Always Dangerous: Physical gold (like all commodities) is purchased via futures contracts. The leverage involved is typically 15 or so to 1 — meaning, for every $1000 of gold futures you buy, you have to put up only about $67. To buy the same amount of stocks would require $500. Any investment bought via credit always runs the risk of margin calls and, eventually, liquidation. It was true for the dot-com stocks, for no-money-down houses and for subprime collateralized debt obligations. It is just as true for precious metals. When you buy anything with lots of leverage, it does not require a whole lot to go wrong to lose it all. At 15-to-1, a mere 7 percent price drop can generate a margin call, meaning you gave have to put up more capital or you lose all of your prior investment. With all of those newbie gold enthusiasts who were inexperienced in the futures markets, it is no surprise that there were plenty of wipeouts. The CME Group, the world's largest commodities exchange, was concerned about all this leverage. It acts as both a clearing house for trades and as the guarantor of all contracts. It could get stuck holding the bag in the event of big price swings and bigger losses. As gold rallied past $1,000, the CME Group did the prudent thing — raising margin requirements. Even some pros were caught unaware by the increases. In September 2011, with volatility increasing, the CME Group raised gold margin requirements by 21 percent — leading to more margin calls, forced selling and liquidation. That marked the high point of the gold run. 5. Understand the Circumstances of the Moment: In military aviation, the concept is called situational awareness. In a dogfight, pilots have to be aware of everything in all four dimensions — 3-D space, plus how things change over time. The idea is important for investors, as well. Although gold does well when the news flow is bad, eventually, the cycle will turn. Bad news gets better as the economy recovers, people get hired, sentiment perks up, retail sales improve. Quite a few gold investors came to believe that the bad economic news had become a permanent condition. They forgot that the Great Depression eventually ended, and so, too, did the Great Recession. They got lost in the moment — an expensive mistake. 6. Don't Be Unwilling to Walk: Try this simple thought experiment before making any investment: Ask yourself "What would make me reverse this position — what would make me sell?" Most professionals have a long list of factors. Often, a simple price decrease will get traders to cut their losses. Not so with gold bugs. Whenever I asked that question — what would make you sell — the most common answer I heard was "I'll stick with gold." This is a dangerous mind-set. It is especially important to have an exit strategy with a "loved" holding — specifically because of that big emotional attachment. If nothing will make you reverse your biggest present holding, you have a huge, devastating flaw in your approach to investing. 7. Ask What is Already Reflected in the Price: This is one of the biggest differences between professional and amateur traders. Pros in the gold market understood what was already reflected in the price — whether it was the Indian wedding season or moves by China's central bank that had an impact on demand. Genuine surprises that are unknown to the market can move prices. Most of the narratives (See this or this) do not. 8. Don't Guess: For people familiar with equity investing, where the focus is on earnings and cash flow, gold can be perplexing. Relative to equities, it has no fundamentals. It also has no cash flow, or earnings, or dividends. Instead, some people tried to guess the direction of macro issues, such as interest rates, GDP, corporate earnings, debt, unemployment, inflation, and the U.S. dollar, to surmise where gold prices were going. This is a near-impossible task. It is certainly not a reasonable basis for deploying your capital. 9. Ignore End-of-World Tales, Conspiracy Theories and Other Nonsense: As we noted in 2011, after a recession, the least rational rise (temporarily) to prominence. My advice then was to ignore them. Why? Because salesmen never let the facts get in the way of a good narrative. Too many discussions about gold contain ominous forecasts about what the end of civilization is going to be like. Spurious correlations, ominous fear mongering seemed to be a key part of the narrative. Mix in one part dollar collapse and two parts hyperinflation, and the conclusion is you MUST own gold. The problem is that fear mongering is about what has already happened — and not about the future. The dollar? It already collapsed 41 percent from 2001 to 2008. Inflation? We already had very strong inflation in the 2000s. Gold is marketed through a combination of fear and dishonesty. At least various equity products are marketed through a combination of hope and dishonesty. It's a far less depressing sales spiel. 10. Pay Attention to the Skeptics: Someone challenges the belief in gold, and instead of responding with empirical, data-driven counter-arguments, the true believers revert to personal attacks. Scroll through the comment section of the blog ZeroHedge.com to see the sort of nonsense that passes for debate. A lack of reasoned discourse is overcompensation for a weak investment thesis. ~~~ The ups and downs of gold over the past 10 years are not unique. Like any other investment, people became emotionally involved with the trade. Mistake were made, money was lost. Astute investors will learn something from watching and thinking about other people's mistakes. Hopefully, you can avoid repeating these errors when the next mania rolls around.

… A longer version of this was published at Bloomberg View. Ritholtz is chief investment officer of Ritholtz Wealth Management. He is the author of "Bailout Nation" and runs a finance blog, the Big Picture. Twitter: @Ritholtz. |

| Posted: 18 Jan 2014 05:00 AM PST Here are my longer form articles for your weekend reading pleasure:

Whats up for the 3 day weekend?

Stores Confront New World of Reduced Shopper Traffic |

| Smallest, Faintest Galaxies of the Ancient Universe Spotted Posted: 18 Jan 2014 03:00 AM PST |

| The Insensitivity of Investment to Interest Rates: Evidence from a survey of CFOs Posted: 18 Jan 2014 02:00 AM PST |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment