The Big Picture |

- Sovereign CDS Spreads in Europe—The Role of Global Risk Aversion, Economic Fundamentals, Liquidity, and Spillovers

- Best Visual Effects, 1977-2013 Oscar Winners

- Howard Stern: The Birthday Bash

- Google’s Nest Labs Acquisition is a Smart Move

- 10 Weekend Reads

- 2014 BMW i8

- Let’s End Politico and Deal Book’s “Competition in Sycophancy”

| Posted: 02 Feb 2014 02:00 AM PST |

| Best Visual Effects, 1977-2013 Oscar Winners Posted: 01 Feb 2014 04:00 PM PST

|

| Howard Stern: The Birthday Bash Posted: 01 Feb 2014 01:00 PM PST What kind of crazy f____d up world do we live in where Howard Stern gets a better tribute than the Beatles? One in which Adam Levine does a spot-on rendition of “Purple Rain” and establishes his rock and roll bona fides overnight. I was planning on hearing this on the replay, but my flight was canceled by snow and I find myself…unable to stop listening. What a crazy world we live in. Wherein Howard hypes this low-rent celebration of his sixtieth birthday and the straight media completely ignores it and more celebrities turn out and reveal themselves than at the Golden Globes, the “gold standard” for celebrity looseness. But it’s not surprising, when Howard specializes in extracting nuggets from others we’re dying to know but are way too creeped out or afraid to ask. Like were your parents virgins when they married? That was one of the questions Mr. Stern put to his parents twenty years ago, it was featured in the replay of bashes past on his second channel, Howard 101. By putting it all out there himself, Howard has license to ask you… How much money you make. How frequently you have sex. Whether you’re going to invite him to your wedding. That’s what Howard asked Katie Couric. Who showed up with not only Whoopi Goldberg, but Barbara Walters. Along with Mariann from Brooklyn and so much of the rest of the Wack Pack. But not Eric the Midget/Actor. Don’t know who he is? That’s just the point. In the Stern world, Eric is a star, with more airtime than a movie star. We know Eric and his peculiarities intimately, whereas the celebrities the mainstream media promotes are airbrushed to the point where when TMZ reveals the tiniest blemish, everybody goes OOH! But we’re all imperfect, we all have blemishes, we all fart. Otherwise, why would we click the linkbait of stars without their makeup? Jewel sang her rendition of Howard’s adolescent composition, “Silver Nickels and Golden Dimes.” And Train may have covered “I Feel The Earth Move” at the Carole King/Musicares tribute, but here the band performed what we really wanted to hear, its spot-on take of Led Zeppelin’s “Ramble On.” And unlike the Grammys, Bon Jovi sang his big hit, the soundtrack to “Deadliest Catch,” “Wanted Dead Or Alive.” John Mayer didn’t utilize the occasion to promote a single, but covered Bob Dylan’s “Like A Rolling Stone.” Although hosted by Jimmy Kimmel, David Letterman made an appearance, and revealed why he made up with Jay Leno. And at this late date, hours into the bash, a Google news search of “Howard Stern” reveals nothing other than the appearance of Chris Christie. But not tomorrow. Tomorrow this will be a big story. When the herd media decides to go on it, since they’re interested in whatever stars do. But not Howard Stern. Because they don’t want to consider him a star. Because he’s not beautiful. He’s not a great singer or actor. He’s just like them. And that’s why it’s Howard Stern’s time. You stay in the game long enough and your moment arrives. In the cacophonous world we inhabit you only rise to the top and sustain if you’re constantly in the public eye, doing new things. And Howard’s creating twelve hours of new material every week, at an insanely high level, since he’s honed his craft for forty years. Yes, while music focuses on the barely pubescent, when it lauds Miley Cyrus, with songs written by old men, the truth is it’s a long way to the top if you truly want to rock and roll. And listening to the free stream on my computer it’s reminiscent of nothing so much as a 1970′s FM simulcast. Real, but at a distance. I didn’t think I needed to be there. But I was wrong. Packed with celebrities, John Fogerty is singing “Bad Moon Rising” right now, the show is fast-paced, but loose. There’s none of the airiness or phoniness of network TV. But that’s not hard to believe, because Howard Stern is the biggest star in America. And you either know it or you don’t. He’s America’s Number One Interviewer. A bigger star than Jay Leno and Jimmy Fallon and Conan O’ Brien and David Letterman. Because he’s got the audience. But you don’t see the Sirius mindshare/listeners in the Nielsen reports. But that does not mean it’s not real. What do they say, you judge a star’s wattage by the fanaticism of its audience? Just read the tweets. This is bigger than the anniversary of the Beatles’ appearance on Ed Sullivan. Because this ain’t history, this ain’t calcified, Howard Stern’s Birthday Bash is life itself.

~~~ – |

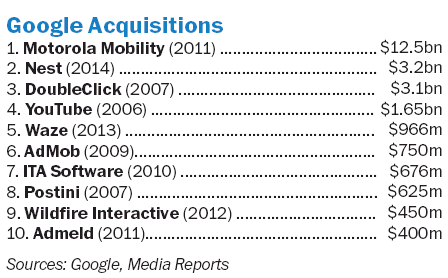

| Google’s Nest Labs Acquisition is a Smart Move Posted: 01 Feb 2014 07:00 AM PST Defense! Google's Nest Labs acquisition is a smart move

With the Super Bowl just a week away, the age-old question of whether offense or defense wins big games is at hand. "The best defense is a good offense," goes the saying, with the Denver Broncos called the best offensive team ever. The Seattle Seahawks are no slouches either, with their top-ranked defense and an explosive offense. The question of offense or defense has been on my mind since Google acquired Next Labs for the eye-popping sum of $3.2 billion. If you look at this purchase solely from the perspective of an investor, it seems quite pricey. After all, this is a relatively new start-up with modest revenue in a niche market of thermostats and smoke detectors. From the perspective of those deploying capital in the expectation of a return on investment, future gains are likely to be paltry relative to the billions invested. But if you consider this from the perspective of a technology company horrified at the prospect of becoming irrelevant, the acquisition looks very different. Rather than look at the costs of making an acquisition like this, consider the risk of failing to aggressively play defense. History is replete with examples of tech firms that were marginalized by new companies and technologies. Indeed, some of the biggest strategic errors have occurred in the past decade alone. The companies that ignored specific risks from the latest innovations came to rue that decision. Think BlackBerry circa 2007 — it hardly thought of Apple's newfangled touchscreen iPhone as a threat to its core business. Yet BlackBerry's global market share collapsed from nearly half of all smartphones sold in 2009 to less than 3 percent today. Microsoft offers a similar cautionary tale. A monopoly market share combined with an arrogant CEO — Steve Ballmer refused to let his kids have an iPod or use Google — left the software giant blindsided by threats to the core business. Indeed, hubris led the makers of the world's dominant operating system to miss or ignore many tech developments: social networking, search, cloud computing, smartphones, tablets, MP3 players, user-generated content, blogging, microblogging (Twitter) and location-aware apps. But it was Apple's iPad (along with other tablets such as those using Android) that became the biggest threat to their basic Windows laptop/desktop PC business. Perhaps the granddaddy of cautionary technology tales is Eastman Kodak. The film and camera manufacturer was so dominant that, according to a case study by Harvard Business School, in 1976 "Kodak controlled 90 percent of the film market and 85 percent of camera sales in the United States." Astoundingly, it was Kodak itself that developed the digital camera in 1975. Fearing that digital photography would cannibalize its photographic film business, the company buried its own invention. That helped sales for the next decade or two, but, eventually, digital cameras came to dominate photography. Rather than own the future, they clung to the market share of the past. It should surprise no one that Kodak eventually filed for Chapter 11 bankruptcy protection. None of this has been lost on the founders of Google, with their dominant position in search. Their acquisitions and research and development actions suggest that they are cognizant of how easy it is for a company to lose its grip on its primary market. This is especially true for dominant firms that became complacent — like Kodak, Microsoft and BlackBerry did. I credit Google for having the foresight to identify threats to its main business of selling advertising against search results. The potential loss of market share in the mobile space led them to the Android acquisition. That gave Google a solid footprint in mobile, preventing it from having to play catchup like BlackBerry and Microsoft did. Lower-priced Android phones now have a dominant market share (and Android tablets have a respectable share) — even though neither is especially profitable versus Apple's iPhone. However, they ensure that Google's core search business has a large and growing footprint in the mobile space. One can only imagine the conversations occurring in Mountain View today had Google not made that Android purchase. Might the Nest Labs acquisition look like a similar no-brainer years hence? It has the potential to be, if not quite as large as Android, then perhaps nearly as important. Most of Google's home technologies have failed to catch on in a major way. The Android@Home platform didn't, and the Nexus Q streaming media device has not set the world on fire. Don't even ask about Chromecast Dongle (whatever that is). While Google's internal R&D has not created the next YouTube (Google Plus, anyone?), it has put together a very good track record of acquisitions that enhance its core business. YouTube has grown into a huge winner, giving Google a dominant position in online video. Variety reported that the video division grossed $5.6 billion in ad revenue in 2013. (Google's stock price increase after the announcement of the YouTube deal paid for the $1.65 billion purchase). Motorola Mobility — another pricey purchase at $12 billion — as a clever patent acquisition; it has mostly insulated Google from countless mobile patent infringement lawsuits against Android.

Meanwhile, the Wall Street Journal reports that Nest Labs is selling 100,000 smart thermostats a month — a respectable number for a start-up. Yes, $3.2 billion is certainly a lot of money to you or me, but it's barely 5 percent of Google's cash. It's a pittance relative to its $388.8 billion dollar market cap. The risk to Google is not the cost of acquisitions such as these, but the risk to its core business down the road of failing to do so. If the "connected home" is a thing a few years hence, what new or existing company might be doing to Google what Apple did to BlackBerry? When big tech-driven firms make acquisitions of this sort, they are doing so for very different purposes than investors do. They are acquiring engineering talent. They shave off years of research and development with a known outcome, rather than a who-knows-what outcome years down the road. Google's founders have had a good eye for imagining what technologies will be significant in the near future. No one asked Google to develop self-driving cars, but it helped them with street views for Google Maps. Nor was there a clamor for an alternative platform for mobile, but they turned this into a tremendous asset and created competition in the space. The same can be said of purchases in e-mail security or local advertising or even robotics. Might Google be wrong that the connected home is the next new thing? Certainly. Perhaps nothing of great value will develop from this purchase. But if Larry Page and Sergey Brin believe this could be a significant technology, then it is a small price for Google to pay to ensure it participates in the integrated-smart-home market. If not, what's $3 billion to a $390 billion company sitting on $55 billion generating $5 billion per quarter in free cash flow? Consider it a small insurance payment. ~~~ Ritholtz is chief investment officer of Ritholtz Wealth Management. He is the author of "Bailout Nation" and runs a finance blog, the Big Picture. Twitter: @Ritholtz. |

| Posted: 01 Feb 2014 04:00 AM PST Pour yourself a cup of Joe, and settle in for some of our longer form weekend reading:

What’s up for the weekend?

US Economy Shows Signs of Gearing Up |

| Posted: 01 Feb 2014 03:00 AM PST

From Automobile Magazine:

|

| Let’s End Politico and Deal Book’s “Competition in Sycophancy” Posted: 01 Feb 2014 02:30 AM PST Let's End Politico and Deal Book's "Competition in Sycophancy"

Politico has joined Deal Book in a "competition in sycophancy." The contestants are competing to see which can author the most extreme version of a fantasy meme in which heroic Wall Street "banks" are oppressed by "Washington." I had not believed that any "serious" journalist could compete with Andrew Ross Sorkin's Deal Book in pounding this meme. Ben White, Politico's economics reporter, has become my dark horse favorite in the race to the bottom of the "serious" business press with his whitewash entitled "How Washington beat Wall Street."

In fairness to Sorkin and White I am focusing on them as a matter of (almost) respect. There are vastly worse business reporters than Sorkin and White. The point is that we rightly expect a great deal from the New York Times and Politico wants to compete in that league. It is fair to expect them to strive every day to be a national asset rather than a national embarrassment that harms the public. They are worth trying to save from the dark side, so I have tried to hold Deal Book's feet to the fire by pointing out their failings in great detail. We need to redirect their efforts into a competition in rigor to root out the rot that causes our recurrent, intensifying financial crises. Sorkin should be tired of writing his endless stream of "DC done JPMorgan wrong" songs. This column is the first in a series designed to try to enlist White and Sorkin in a competition for rigor. We have long understood the regulatory policies that create control fraud epidemics Effective financial regulators have known for at least 30 years, and top economists for 20 years, what produces a "criminogenic environment" in finance. The environment creates such perverse incentives that it causes crime to become epidemic. Akerlof and Romer explained the concept in their famous 1993 article ("Looting: The Economic Underworld of Bankruptcy for Profit").

Accounting is finance's "weapon of choice" because it is a "sure thing" Accounting control fraud produces three "sure things. The bank is guaranteed to report high (fictional) profits in the near term, the officers are sure to be made promptly wealthy by the bank's compensation system, and the bank is sure to suffer catastrophic losses. George Akerlof and Paul Romer drove this point home as forcefully as they could in their famous 1993 article ("Looting: The Economic Underworld of Bankruptcy for Profit").

The key implication of accounting fraud's three "sure things" is that from the perspective of the CEO running such a fraud the terms "risk" and "return" are lies and deliberate means of deceit. The CEO deliberately makes (or purchases) crappy loans with high nominal yields that will produce net losses. The three, record, fraud epidemics that drove the crisis Appraisal Fraud Consider the three fraud epidemics that drove the current crisis. No honest lender would extort appraisers to inflate the appraised value of the home because the adequacy of the true market value of the home is the lender's great protection against loss if the borrower defaults (it also makes default far less common). Liar's loans Similarly, no honest home lender would make "liar's" loans because they knew that it invariably led to endemic, severe inflation of the borrower's income (typically prompted by the lenders and their agents). The borrower's true income is the lender's great protection against default. The industry called them "liar's" loans when they were talking behind closed doors. That lacks a certain subtlety. Liar's loans also have a history. They began, as do all good U.S. financial frauds, in Orange County, California. We were the regional regulators with jurisdiction over the S&Ls making the liar's loans. This was a new product and the loans were not called "liars" loans in our era. We were also dealing with the S&L debacle, an immense task for which we had inadequate resources to respond fully to the existing epidemic of accounting control fraud. Nevertheless, as Akerlof and Romer aptly observed, "the regulators in the field … understood what was happening from the beginning." Our regional leader, Michael Patriarca, listened to what our examiners "in the field" found and concurred with their warning that no honest home lender would make loans that did not verify the borrower's income. Mike also made it a high priority, despite our inadequate resources, to shift resources to stamping out this new fraud scheme before it became epidemic. We drove liar's loans out of the S&L industry in 1990-1991. We viewed ending liar's loans by S&Ls as one of the easiest supervisory calls we ever made during the S&L debacle. Liar's loans caused hundreds of millions of dollars of losses to S&Ls in our era, but we ended these fraudulent loans before they caused expensive S&L failures. They were not able to hyper-inflate a financial bubble and they did not cause any crisis or recession. As future columns will discuss in greater detail, the regulators dealing with the current crisis should have had a far easier time than us in ending such loans. They had the advantage of our experience. The industry had developed the term "liar's" loan to describe the loans – and the regulators knew they had done so. The liar's loans in the current crisis were vastly worse loans than the loans we forced out of the industry. For example, by 2006 half of all the loans called "subprime" were also liar's loans (the two categories are not mutually exclusive). Consider for a moment what this indicates. These loans were overwhelmingly made contrary to regulators' and the mortgage industry's own anti-fraud experts' warnings. Indeed, the industry dramatically increased the quantity and radically decreased the loan quality of the liar's loans in response to those warnings. In 1994, Congress provided the Fed with the express statutory authority to ban liar's loans by any lender – even if they were not federally insured. We had no such power in our era. Congress mandated Fed hearings on predatory lending that produced urgent pleas by a host of housing advocates (including ACORN!) plus state attorney generals and prosecutors alerting the Fed to the endemic abuses and risk of terrible losses and begging the Fed to ban liar's loans. Alan Greenspan did not simply refuse to act. He refused his colleague (Board Member Gramlich's) plea that the Fed use its examiners to find the facts. Much of the senior leadership of the Fed attacked the Fed's supervisors when they provided data on the largest banks enormous origination of liar's loans. Ben Bernanke continued to refuse to use the Fed's unique authority to ban liar's loans. Finally, in 2008, in response to acute Congressional pressure, Bernanke finally used his HOEPA authority to ban liar's loans. Even then he delayed the effective date of the rule by over a year because he did not want to inconvenience the CEOs of fraudulent lenders. These non-responses demonstrate how complete and destructive the desupervision of finance were and why three fraud epidemics were allowed to grow to world record size without any serious regulatory response. More subtly, as I will explore in future columns, the desupervision is a major part of the explanation for the fact that the criminal justice response to the bank CEOs who led these record fraud epidemics that drove the crisis has been virtually non-existent. Fraudulent "reps and warranties" are essential to sell fraudulent mortgages There is no fraud exorcist. Fraudulently originated loans can only be sold through fraudulent "reps and warranties." The fraudulent sale of fraudulently originated mortgages was the third fraud epidemic. No honest purchaser of loans would continue to purchase loans from a seller when the purchaser knew that the loans being sold were frequently fraudulently originated in the manner I've described and that the lender was attempting to sell the loans through fraudulent "reps and warranties." Note these are not close questions. Each of the three fraud epidemics was driven by behavior that is unambiguously consistent with accounting control fraud and falsifies any claim that the bankers were engaged in high risk but honest "gambles." These analytics are neither difficult nor controversial. Future columns will provide data on the frequency of each of these fraud epidemics. The data are neither difficult to understand nor controversial. Any discussion of the crisis premised on the (always untested) assumption that it was caused by "risky" lending seeking "high yields" must be erroneous because it is contrary to the facts. It would also be a complete departure from the S&L debacle and the Enron-era frauds, both of which were driven by epidemics of accounting control fraud. Any competent business reporter can understand the relevant analytics, history, and data. A few major control frauds can create a "Gresham's dynamic" producing endemic fraud George Akerlof was the first economist to explain, in his classic 1970 article on markets for "lemons," why individual "control frauds" can cause fraud to become epidemic.

Akerlof called this a "Gresham's" dynamic because bad ethics tends to drive good ethics out of the markets and professions. Akerlof was far from the first person to recognize this dynamic. Over two centuries earlier, a writer observed:

These factors explain why fraudulent CEOs make weakening regulation their top priority The regulators must serve as effective "cops on the beat" to prevent "the knave" from gaining "the advantage" through fraud. Only the regulator can ensure that "the honest" banker is not "undone" by the CEOs running the control fraud. We are so dangerous to the fraudulent CEO because we are the only "control" that the CEO cannot fire and cannot suborn by controlling compensation and the opportunity for promotion. Fraudulent CEOs choose the board of directors – not the other way around. Fraudulent CEOs decide which people will be nominated as directors and vote the proxies that elect the directors. Fraudulent CEOs almost always chose well (which is to say badly). Boards rarely stop CEOs leading control frauds. Because of our unique ability to sanction CEOs running control frauds, competent regulators are their prime target. CEOs can, and do, launch wide ranging efforts to neutralize their regulators. As I will develop in future columns, the formal rules are often the least important aspect of these efforts. I will explain the three "de's" in detail (deregulation, desupervision, and de facto decriminalization) and the three primary strategies fraudulent CEOs use against effective regulators – "buy, bully, and bamboozle." Ronald Reagan's signature joke slandered regulators while he aided the S&L "knaves" Reagan: "The nine most terrifying words in the English language are: 'I'm from the government and I'm here to help.'" There are several vital implications of the fact that the crises were driven by frauds led by CEOs that typically caused massive losses to "their" corporations. Effective financial regulation protects "banks" – and their shareholders (unless the CEO is the paramount shareholder) and creditors – from their gravest threat, their CEO. Indeed, only effective financial regulation can protect banks, (honest) shareholders, and creditors from the CEO because CEOs leading control frauds have demonstrated the consistent ability to suborn internal and external "controls" and pervert them into fraud allies. "Private market discipline" is an oxymoron when it comes to accounting control frauds – and the Enron-era frauds and the current crisis demonstrate that this is not the result of deposit insurance. Private creditors eagerly fund the rapid growth of accounting control frauds because the fraud makes them appear to have record profits. These facts mean that, contrary to President Reagan's smear of government workers, effective regulators are the indispensable friends of honestly-led banks and banks' shareholders and creditors because we are the worst nightmare of bank CEOs that loot. The ten most terrifying words in the English language are "I'm from Goldman Sachs, and I'm here to help you." Reagan was aware of our reregulation of the S&L industry, our crackdown on the looters, and the furious attacks on us by the looters' political allies. Reagan and his administration repeatedly sided with the looters and attacked us. He never ceased his sneering smears of the regulators even as we exposed the lie at the core of his signature joke. (I'm not arguing that financial regulators are unique or even special in this regard. Many "government" workers such as firefighters regularly "help" people by risking their lives to save complete strangers.) Reagan continued to ally with the worst financial frauds, including Charles Keating, against us even when we were the targets of Democratic politicians who were acting in a shameful fashion to try to prevent us from closing the worst frauds. Four of the five Senators who became known as the "Keating Five" and Speaker Wright were Democrats. Each of these five prominent Democrats allied with Keating to attack us, but so did the Reagan administration in myriad ways. To give but one example, in late 1986, Reagan tried to appoint two "Members" chosen by Keating to the three-Member Federal Home Loan Bank Board. This would have given Keating majority-control over the regulatory agency – and it would have caused trillions of dollars in losses and produced the worst political-financial scandal in U.S. history and rendered Reagan the Republican Party's most embarrassing official. Fortunately for the Nation, and Reagan's reputation, one of the nominees was blocked by random politics. The second served as Keating's "mole" at the agency until I was able to blow the whistle on his surreptitious effort to aid Keating. He made a deal with the prosecutors to resign to end the criminal investigation. Politico's framing of the issues misses each of these analytical points White admirably places his thesis and framing in the first sentence of his January 16, 2014 article entitled "How Washington beat Wall Street."

This column will address only White's first sentence and his framing. First, "Washington" is too vague a term to allow analysis and it falsely implies that there is some singular entity with a singular policy. "In 2009," as at every year of its existence, different actors that work in Washington, D.C. had markedly different view about "banks" and bankers and those views often depended on the particular issue being discussed rather than some overall view about "banks." I will expand on this point in future columns, but here are a few of the major ways in which White's thesis collapses as soon as we disaggregate "Washington" and examine the facts of "Washington's" Phony War on "banks."

"From 2000 to 2007, a coalition of appraisal organizations … delivered to Washington officials a public petition; signed by 11,000 appraisers…. [I]t charged that lenders were pressuring appraisers to place artificially high prices on properties [and] "blacklisting honest appraisers" and instead assigning business only to appraisers who would hit the desired price targets" (FCIC 2011:18). By 2000, after two years of organizing the coalition and agreeing upon the text of the petition, the appraisers warned "Washington" that the banksters had declared war on America (to adopt White's martial metaphors simply for the purpose of revealing how he stacked his rhetoric). No honest lender would ever extort appraisers to inflate appraisals, so this was the perfect "signal" of the presence of an epidemic of accounting control fraud – which means that the bankster/looters were making war on "their own" banks. "Washington" did nothing material in response – even when surveys demonstrated that 90% of all appraisers had personally been subjected to such extortion in the prior 12 months. So, if "Washington went to war" only in 2009 in response to the banksters' assault on the banks – which was large enough for the honest appraisers to identify it as a crisis by 1998 – we have demonstrated that "Washington" is astoundingly slow to anger (11 years) when the banksters make war on our Nation, the banks and their customers. Oh, and as is characteristic of Dodd-Frank, it has provisions dealing with appraisers and appraisals – none of which would prevent a recurrence of the fraud epidemic.

Second, any "war" metaphor applied to financial regulation is sure to mislead. I know because I've used them. This particular metaphor is false for the reasons I've explained above. Third, "Washington" reformers aren't opponents of "banks." They are opponents of fraudulent bankers. Effective regulation is essential to "banks." More precisely, it is essential to protect their shareholders, creditors, and customers and honest bank CEOs. Why would members of Congress or regulators want to destroy "banks?" Banks are major sources of political contributions and banks are what financial regulators seek to protect from their gravest enemy – fraudulent CEOs. "Banks" aren't human. Fraudulent CEOs are the ones who seek to harm "their" banks. Fourth, for the reasons I've explained, many "Washington" actors are the fraudulent CEOs' most valuable allies and the "bank's" most dangerous foe. These actors include prominent members of Congress and senior officials in the Obama administration. Recall that a decade before "2009" the Clinton administration, Alan Greenspan, Senator Phil Gramm, and the "13 bankers" (the CEOs of the largest banks) allied to crush Brooksley Born (Chair of the CFTC) when she thought to study whether financial derivatives (including CDS) should be regulated. The result was the deliberate creation of a "regulatory black hole." Fifth, for the reasons I've explained, the crisis has little or nothing to do with "high-risk, high reward strategies." The "strategies that helped spark the financial crisis" were not "high-risk in the sense White uses the term. The strategy that drove this financial crisis, like the S&L debacle and the Enron-era scandals, was the traditional "sure thing" of accounting control fraud. Indeed, one of the fraud mechanisms, making liar's loans, reprised the fraud strategy of the non-crisis of 1990-1991. In those years, because we understood fraud schemes and why making liar's loans only made sense for fraudulent CEOs, the regulatory response was so rapid and vigorous that the incipient fraud epidemic was ended before it could cause a "Gresham's" dynamic and produce a crisis. Dodd-Frank has a provision banning liar's loans. Does White assert that such loans were honest "high-risk" "gambles" rather than endemically fraudulent? Why does he think that bank CEOs dramatically increased the quantity, and decreased the quality, of liar's loans in response to their own anti-fraud experts' and the regulators' warnings? Sixth, White is logically inconsistent and tries to hide it with his marital rhetoric. If Congress had sought to end the banking strategy that caused the crisis, that would refute White's claim that they were waging a "war" against "big Wall Street banks." Readers remember, even if White does not, that the banking strategies that caused the crisis rendered most of the world's largest banks insolvent and in deadly liquidity crises. If White were correct that Congress, President Obama, and the federal financial regulators sought to end the banking "strategies" that devastated the "big Wall Street banks then it would follow logically that they were seeking to protect rather than wage "war" against those banks. "Blow up" is nicely martial, but one does not "blow up" a "strategy." If White had claimed that "Washington" was "hoping to blow up" banks his readers would have realized that he was seeking to mislead them. Conclusion The first sentence of White's attempted whitewash states (and refutes) his thesis and demonstrates his failure to understand the causes of the crisis, the nature of accounting control fraud, and the nature and purpose of financial regulation. It turns out that the 2009 "war" on "big Wall Street banks" primarily consisted of sending them trillions of dollars to save them from collapse, secret interventions by Geithner designed to secretly use AIG as a means of funneling even more money from Treasury to Goldman Sachs and friends, and the development of a new (not so) legal doctrine of "too big to prosecute" designed to ensure that the Wall Street CEOs' could loot with impunity. "Phony War" is too kind a phrase to describe a "war" in which the Treasury and the Fed carpet bombed "the big Wall Street banks" and their CEOs for over a year with trillions of dollars in cash and cheap loans in Operation "Rolling Plunder." It is deeply offensive to call Bernanke "Helicopter Ben." Ben used the equivalent of our entire fleet of B-2 stealth bombers to shower the industry with the Fed's cash. To paraphrase Tevye in Fiddler on the Roof: "May the Lord smite me with [such a "war"]. And may I never recover!"

Originally posted on New Economic Perspectives

|

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment