The Big Picture |

- Science and Engineering Indicators 2014 (NSF)

- Daniel Kahneman, in conversation with Cass Sunstein

- How Does Facebook Make Its Money?

- What Kind of Investor Are You?

- 10 Sunday Reads

- Why You Shouldn’t Drink Coffee in the Morning

- The Demise of U.S. Economic Growth: Restatement, Rebuttal, and Reflections

| Science and Engineering Indicators 2014 (NSF) Posted: 24 Feb 2014 02:00 AM PST

|

| Daniel Kahneman, in conversation with Cass Sunstein Posted: 23 Feb 2014 04:00 PM PST On February 3, 2014, Daniel Kahneman, Nobel Prize-winning author of Thinking, Fast and Slow, spoke with Cass Sunstein, Robert Walmsley University Professor in Spangler Auditorium at Harvard Business School. |

| How Does Facebook Make Its Money? Posted: 23 Feb 2014 02:00 PM PST

|

| What Kind of Investor Are You? Posted: 23 Feb 2014 07:00 AM PST

>

My Sunday Washington Post Business Section column is out. This morning, we look at the differences between Outcome or Process focused investors. The print version had the full headline Investing's smart minority: The process people while the online version Outcome or process — what investment focus succeeds over time?. Here’s an excerpt from the column:

The conceit of the article is that your answer reveals the type of investor you are likely to be, and suggests why one is superior to the other. The Post did a very nice job in the dead tree version of the paper — the layout from page 1 of the Business section to the jump on page 4 really works. >

Source: |

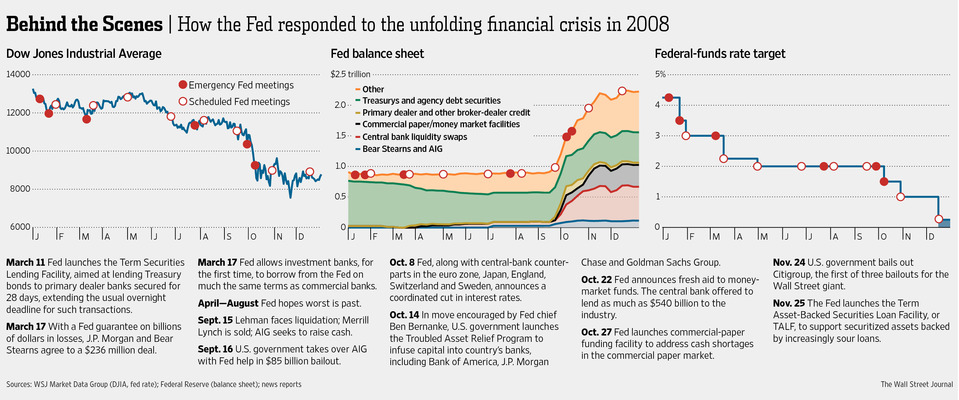

| Posted: 23 Feb 2014 05:00 AM PST Here’s what I’m reading over my Sunday morning coffee:

What’s for brunch?

New View Into Fed’s Response to Crisis

Source: WSJ

|

| Why You Shouldn’t Drink Coffee in the Morning Posted: 23 Feb 2014 03:00 AM PST

|

| The Demise of U.S. Economic Growth: Restatement, Rebuttal, and Reflections Posted: 23 Feb 2014 02:00 AM PST By Robert J. Gordon The United States achieved a 2.0 percent average annual growth rate of real GDP per capita between 1891 and 2007. This paper predicts that growth in the 25 to 40 years after 2007 will be much slower, particularly for the great majority of the population. Future growth will be 1.3 percent per annum for labor productivity in the total economy, 0.9 percent for output per capita, 0.4 percent for real income per capita of the bottom 99 percent of the income distribution, and 0.2 percent for the real disposable income of that group. The primary cause of this growth slowdown is a set of four headwinds, all of them widely recognized and uncontroversial. Demographic shifts will reduce hours worked per capita, due not just to the retirement of the baby boom generation but also as a result of an exit from the labor force both of youth and prime-age adults. Educational attainment, a central driver of growth over the past century, stagnates at a plateau as the U.S. sinks lower in the world league tables of high school and college completion rates. Inequality continues to increase, resulting in real income growth for the bottom 99 percent of the income distribution that is fully half a point per year below the average growth of all incomes. A projected long-term increase in the ratio of debt to GDP at all levels of government will inevitably lead to more rapid growth in tax revenues and/or slower growth in transfer payments at some point within the next several decades. There is no need to forecast any slowdown in the pace of future innovation for this gloomy forecast to come true, because that slowdown already occurred four decades ago. In the eight decades before 1972 labor productivity grew at an average rate 0.8 percent per year faster than in the four decades since 1972. While no forecast of a future slowdown of innovation is needed, skepticism is offered here, particularly about the techno-optimists who currently believe that we are at a point of inflection leading to faster technological change. The paper offers several historical examples showing that the future of technology can be forecast 50 or even 100 years in advance and assesses widely discussed innovations anticipated to occur over the next few decades, including medical research, small robots, 3-D printing, big data, driverless vehicles, and oil-gas fracking. Source: NBER |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment