The Big Picture |

- Withstanding Great Recession Like China

- State of Love and Sex in Single America

- Abbey Road Medley: Acapella

- Lefsetz’s Business Rules

- What’s the problem with 401(k)s? You.

- 10 Weekend Reads

| Withstanding Great Recession Like China Posted: 16 Mar 2014 02:00 AM PDT |

| State of Love and Sex in Single America Posted: 15 Mar 2014 04:30 PM PDT Match.com, the world’s largest dating site, has released its annual Singles in America survey. Match.com’s Helen Fisher and Justin Garcia discuss what over 5,000 singles have to say about the state of love and sex in America today. |

| Posted: 15 Mar 2014 03:00 PM PDT |

| Posted: 15 Mar 2014 12:00 PM PDT 1. You’ve got to get along. If you don’t have good people skills, you’ll never succeed, even if you run your own business. 2. Money talks. He who has cash has leverage, and someone always has more than you do. There’s rarely a deal between equals. 3. Leverage is not always about money. I.e. if you’re an unsigned band that can sell out arenas, you’ll get an incredible deal from the label. 4. If a deal is too good, it probably is. In other words, if the other person can’t make any money, there’s going to be a problem. 5. The best deals are win-wins. 6. If you’re not willing to risk, if you’re not willing to give something up, you’re going to sit on the sidelines. Sure, the label might not offer you your dream deal, but the alternative is to go it alone, which is an option, but probably not the one you want since you entered negotiations in the first place. 7. You don’t know everything, you just think you do. If you’re not learning every day, you’re hanging with the wrong people and not applying yourself. 8. The more powerful the person, the less the chance you’ll see them at the conference. The conference is for never have and wannabes and for the purveyor to make coin. In other words, have a good time at SXSW, but the real winners are the people who put on the conference. 9. A contract does not guarantee behavior. At most it’s a guideline. If you think suing to get what you want is a solution, that the contract entitles you to win, you’re naive. 10. Some people use litigation as both a business strategy and a profit center. If someone has deeper pockets than you, you’re not on an equal footing. 11. The real world is very different from books. In other words, there are very few professors who can succeed in the real world. Theory is one thing, practice is another. 12. Lawyers are worth every dollar you pay them. So choose wisely and don’t expect a deal. You need an outside voice. Someone who knows the pitfalls. 13. News often isn’t. It may be on the Business page, but frequently the corporation has a relationship with the journalist and wants a certain story told. 14. If you haven’t been screwed, you haven’t been in business. There’s more than one way to fail, you learn lessons from your defeats, which is why so many want to hire those who’ve failed, because they’ve gained so much experience! 15. Nitpicking is for losers. If you can’t let something go by, if you want the other party to live up to every letter of a contract, you’re going to find yourself an outcast by the sidelines. 16. Winners see tomorrow as well as today. If you don’t have the exit strategy in place when you’re negotiating a deal, you’re going to find yourself in an uncomfortable position down the line. 17. Those who give the best advice are the hardest to get to know, and the hardest to get to speak at length. The powerful don’t want to know the powerless, there has to be an advantage in it for them, or else the response will be very brief. 18. Time is irreplaceable. Never waste someone else’s. Make your pitch short and to the point and thank the other person for listening. You think you’re explaining your point, ensuring success by going on at length, but the truth is the other person is rolling their eyes and looking at their watch, wondering how they can get out of this meeting and never ever speak with you again. 19. Most conference calls are a waste of time. Do your best to avoid them. If you’re on one, talk only business and make it brief. 20. Respect your adversary/opponent. Treat people with dignity, dividends will follow. 21. Don’t take you or your business too seriously. Make jokes. 22. Have fun. Work takes up too much of your time not to. 23. Break the rules. All the winners do. School is all about rules, which is why those who’ve done well in school rarely do well in business. ~~~ – |

| What’s the problem with 401(k)s? You. Posted: 15 Mar 2014 06:30 AM PDT There's nothing wrong with 401(k)s, except the players involved

This past year has seen a firestorm of criticism casting 401(k)s as mostly terrible. Their performance is too poor, and the fees too high, with poor investment choices built into most of them. Typical plans are complicated to manage and difficult to administer. Most people remain invested at levels far below their retirement needs. Is all of this the fault of the 401(k)? No. The problem with 401(k)s, dear reader, is you. As we shall see, the parties involved in designing, running and investing in 401(k)s have made a hash of it. You, your employer and your plan's investment managers fail to follow even the most basic rules of investing. You overtrade, chase performance, do not think long term. All of you — ALL OF YOU — have done a horrible job managing your retirement plans. The good news is that it's all terribly easy to fix. First, some history: The Revenue Act of 1978 had buried within it an unnoticed provision creating a deferred compensation plan for retirement savings, technically known as Internal Revenue Code Section 401(k). It was mostly ignored until Ted Benna, a Pennsylvania benefits consultant, petitioned the IRS for an important rule change allowing these contributions to be made pretax. That was approved, and a few decades and many trillions of dollar later, 401(k)s have become the prime vehicle for individual retirement planning. What's wrong with these plans? Human behavior, which has managed to turn a relatively simple idea into a complex, overpriced, underperforming mess. Returns have lagged behind a myriad of asset classes doing exceptionally well over the long haul. The solution is not very difficult: Simplify the plans, reduce the fees, make enrollment automatic and get out of the way. To understand how to do this better, consider the three parties to any tax-deferred retirement plan, and what each gets out of it: the employer, the employee and the investment-management firm. The employer gets a low-cost compensation tool. Nearly all companies — the exception being AOL, which seemingly uses its 401(k) plan to discourage people from working there — use these plans to attract and retain high-quality employees. The employee gets a tax-deferred way to fund retirement. The investment community gets a huge pile of dollars to manage. Not long ago, workers actually got "defined-benefit" plans. But they were expensive, and most companies long ago ended them. Hence, the modern "defined contribution" plan. Over my career, I have reviewed countless 401(k) plans. Nearly all suffer from the same three problems: 1) An overemphasis on active fund management (versus passive, low-cost indexing). 2) A bewildering array of investment choices. 3) Excessive fees each step of the way. Combined, these problems are a drag on 401(k)s returns and long-term performance. An additional 1 percent in fees over a 30-year investment can reduce a plan's final value by as much as half, according to a study by Vanguard. Low fees should be a priority for all employers when assembling plans. The look on potential clients' faces when I tell them that "I need you to pay people like me much, much less" is priceless. The second fix is behavioral: "Active" management should be mostly (not necessarily entirely) replaced with passive indexing. This will result in numerous improvements. It generally lowers internal expense ratios by about 1 percent. Those are the fees that investors don't see but are disclosed in the fine print somewhere. Mutual funds actually pull these expenses straight out of your holdings. It's invisible, right off the top of the fund and only shows up in weaker annualized returns. The solution is simple: Put nearly all of a portfolio into a broad asset allocation model consisting of a dozen or so classes. You can use low-cost funds or ETFs. If you want to have two or three 10 percent slugs to put with an active manager, I can live with that. But the goal is to get yourself out of the way of your portfolio and let the magic of long-term compounding interest work. It is a bit of an urban legend that Albert Einstein said compounding is the "most powerful force in the universe," but it gets the point across. Active management leads to lots of poor investor behavior. It sends people chasing after whoever has the hot hand at the moment. Often, investors will discover a manager after he's had a terrific run, usually when he lands on a magazine cover somewhere. Invariably funds swell up with new investor money just before they revert to their long-term averages. Tying the biggest percentage of your portfolio to a passive index avoids this foible. Third, the fees in passive indexing are far lower than in actively managed funds. Lower fees accrue to the employee's benefit. Lastly, many parties take an administrative fee from 401(k)s. There is the custodian, who charges a fee to hold the assets; the reporting firm that generates regular statements showing the assets' performance; the plan manager who either charges a flat fee to the employer or a percentage of the total assets to the employee. As you might imagine, employers would rather not pay a flat fee when they can simply let the employee cover it by paying a percentage on assets. If the employer is unwilling to pay the flat fee, it should secure the lowest possible fees its employees pay on assets. These fees should be below 0.50 percent, and ideally as low as 0.25 percent. Too often, they can be as high as 2 percent. How can we fix these issues? In theory, all it requires is an educated employer concerned with the long-term financial well-being of its employees. Then we need employees to stop making foolish investment choices. Finally, the people who are compensated for managing these plans must agree to be paid less. It's that simple! It sounds farfetched, but it's really not. A well-designed 401(k) plan is an enormous competitive edge when recruiting and retaining employees. Investors can be taught to stop making so many bad choices in their investing. A default allocation plan helps a lot when designing these. And, finally, the competitive bidding process for 401(k)s is an opportunity to negotiate fees lower. The 401(k) structure is just fine. See if you people can stop messing it up. ~~~ Ritholtz is chief investment officer of Ritholtz Wealth Management. He is the author of "Bailout Nation" and runs a finance blog, the Big Picture. Twitter: @Ritholtz. |

| Posted: 15 Mar 2014 04:00 AM PDT Pour yourself a strong cuppa Joe, and start your Saturday morning with my longer form, weekend reads:

60 and sunny in the NYC area — looks like a top down kinda day!

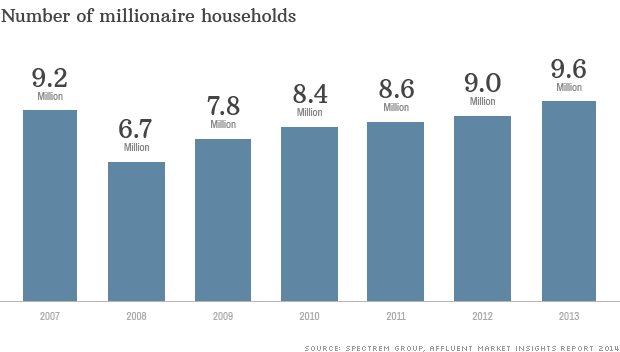

Number of U.S. Millionaires Reaches Record High

|

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment