The Big Picture |

- The Growth Impact of Discretionary Fiscal Policy Measures

- The Ins and Arounds in the U.S. Housing Market

- Blowing the Whistle on NSA Spying on Americans

- Comparative Advantage: The Tragedy of Tasmania

- Each dot on this map represents an act of terrorism since 1970

- The Billion-Dollar Startup Club

- 10 Thursday AM Reads

- What makes Analysts Cover Stocks?

- The Universe of Pop Culture Bears

| The Growth Impact of Discretionary Fiscal Policy Measures Posted: 01 Aug 2014 02:00 AM PDT | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The Ins and Arounds in the U.S. Housing Market Posted: 01 Aug 2014 02:00 AM PDT | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Blowing the Whistle on NSA Spying on Americans Posted: 31 Jul 2014 10:30 PM PDT | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Comparative Advantage: The Tragedy of Tasmania Posted: 31 Jul 2014 04:30 PM PDT From Don Boudreaux's Everyday Economics:

What can a small, isolated island economy teach the rest of the world about the nature and causes of the wealth of nations? When Tasmania was cut off from mainland Australia, it experienced the miracle of growth in reverse, as the reduction in trade and human cooperation forced its inhabitants back to the most basic ways of living. In an economy with a greater number of participants trading goods and services, however, there are more ways to find a comparative advantage and earn more by creating the most value for others. Let’s join Bob and Ann as they teach us the “Story of Comparative Advantage” like you’ve never seen it before. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Each dot on this map represents an act of terrorism since 1970 Posted: 31 Jul 2014 11:30 AM PDT

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

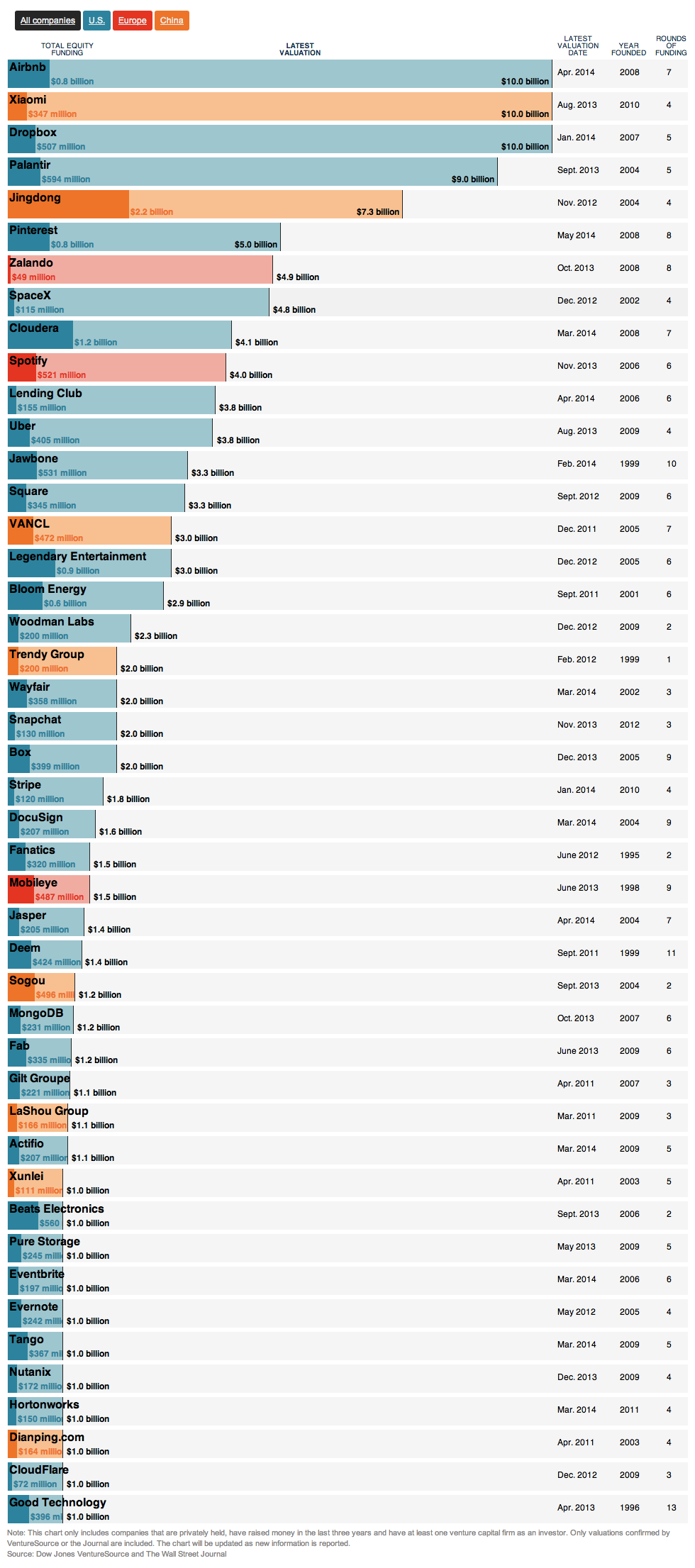

| The Billion-Dollar Startup Club Posted: 31 Jul 2014 09:00 AM PDT Click for an interactive graphic. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 31 Jul 2014 06:45 AM PDT My morning pre-fishing reads (continues here):

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| What makes Analysts Cover Stocks? Posted: 31 Jul 2014 04:00 AM PDT David J. Merkel, CFA runs his own equity asset management shop, called Aleph Investments, running separately managed stock and bond accounts for upper middle class individuals and small institutions. He has a background as a bond manager and life actuary and hold bachelor's and master's degrees from Johns Hopkins University.

While at RealMoney, I wrote a short series on data-mining. Copies of the articles are here: (one, two). I enjoyed writing them, and the most pleasant surprise was the favorable email from readers and fellow columnists. As a follow up, on April 13th, 2005, I wrote an article on analyst coverage — and neglect. Today, I am writing the same article but as of today, with even more detail. As it was, in my Finacorp years, I wrote a similar piece to this in 2008 and recently, I found it. It had been lost for some time, but it's amazing how many places a document might be stored. Anyway, to the topic at hand: For a variety of reasons, sell-side analysts do not cover companies and sectors evenly. For one, they have biases that are related to how the sell-side analyst's employer makes money. It is my contention that companies with less analyst coverage than would be expected offer an opportunity to profit for investors who are willing to sit down and analyze these lesser-analyzed companies and sectors. I am a quantitative analyst, but I try to be intellectually honest about my models and not demand more from them than they can deliver. That's why I have relatively few useful models, maybe a dozen or so, when there are hundreds of models used by quantitative analysts in the aggregate. Why do I use so few? Many quantitative analysts re-analyze (torture) their data too many times, until they find a relationship that fits well. These same analysts then get surprised when the model doesn't work when applied to the real markets, because of the calculated relationship being a statistical accident, or because of other forms of implementation shortfall — bid-ask spreads, market impact, commissions, etc. This is one of the main reasons I tend not to trust most of the "advanced" quantitative research coming out of the sell side. Aside from torturing the data until it will confess to anything (re-analyzing), many sell-side quantitative analysts don't appreciate the statistical limitations of the models they use. For instance, ordinary least squares regression is used properly less than 20% of the time in sell-side research, in my opinion. Sell-side firms make money two ways. They can make via executing trades, so volume is a proxy for profitability. They can make money by helping companies raise capital, and they won't hire firms that don't cover them. Thus another proxy for profitability is market capitalization. Thus trading volume and market capitalization are major factors influencing analyst coverage. Aside from that, I found that the sector a company belongs to has an effect on the number of analysts covering it. I limited my inquiry to include companies that had a market capitalization of over $10 million, US companies only, no over-the-counter stocks, and no ETFs. I used ordinary least squares regression covering a data set of 3,896 companies. The regression explained 84% of the variation in analyst coverage. Each of the Volume and market cap variables used were significantly different from zero at probabilities of less than one in one million. As for the sector variables, they were statistically significant as a group, but not individually. Here's a table of the variables:

In short, the variables that I used contained data on market capitalization, volume and market sector.

An increasing market capitalization tends to attract more analysts. At the highest market cap in my study, Apple [AAPL] at $585 billion, the model indicates that 10 fewer analysts should cover the company. The smallest companies in my study would have 4.4 fewer analysts as compared with a median-sized company with a market cap of $787 million.

The intuitive reasoning behind this is that larger companies do more capital markets transactions. Capital markets transactions are highly profitable for investment banks, so they have analysts cover large companies in the hope that when a company floats more stock or debt, or engages in a merger or acquisition, the company will use that investment bank for the transaction.

Investment banks also make some money from trading. Access to sell-side research is sometimes limited to those who do enough commission volume with the investment bank. It's not surprising that companies with high amounts of turnover in their shares have more analysts covering them. The following table gives a feel for how many additional analysts cover a company relative to its daily trading volume. A simple rule of thumb is that (on average) as trading volume quintuples, a firm gains an additional analyst, and when trading volume falls by 80%, it loses an analyst.

An additional bit of the intuition for why increased trading volume attracts more analysts is that volume is in one sense a measure of disagreement. Investors disagree about the value of a stock, so one buys what another sells. Sell-side analysts note this as well; stocks with high trading volumes relative to their market capitalizations are controversial stocks, and analysts often want to make their reputation by getting the analysis of a controversial stock right. Or they just might feel forced to cover the stock because it would look funny to omit a controversial company.

Analyst Neglect

The first two variables that I considered, market capitalization and volume, have intuitive stories behind them as to why the level of analysts ordinarily varies. But analyst coverage also varies by industry sector, and the reasons are less intuitive to me there.

Please note that my regression had no constant term, so the constant got embedded in the industry factors. Using the Transportation sector as a benchmark makes the analysis easier to explain. Here's an example: On average, a Utilities company that has the same market cap and trading volume as a Transportation company would attract four fewer analysts.

Why is that? I can think of two reasons. First, the companies in the sectors at the top of my table are perceived to have better growth prospects than those at the bottom. Second, the sectors at the top of the table are more volatile than those toward the bottom (though basic materials would argue against that). As an aside, companies in the conglomerates sector get less coverage because they are hard for a specialist analyst to understand.

My summary reason is that "cooler" sectors attract more analysts than duller sectors. To the extent that this is the common factor behind the variation of analyst coverage across sectors, I would argue that sectors toward the bottom of the list are unfairly neglected by analysts and may offer better opportunities for individual investors to profit through analysis of undercovered companies in those sectors.

Malign Neglect

Now, my model did not explain 100% of the variation in analyst coverage. It explained 84%, which leaves 16% unexplained. The unexplained variation is due to the fact that no model can be perfect. But the unexplained variation can be used to reveal the companies that my model predicted most poorly. Why is that useful? If my model approximates "the way the world should be," then the degree of under- and over-coverage by analysts will reveal where too many or few analysts are looking. The following tables lists the largest company variations between reality and my model, split by market cap group.

Behemoth Stocks

Large Cap Stocks

Mid cap stocks

Small cap stocks

Microcap Stocks

My advice to readers is to consider buying companies that have fewer analysts studying them than the model would indicate. This method is certainly not perfect but it does point out spots where Wall Street is not focusing its efforts, and might provide some opportunities. If you want my spreadsheet, email me. Thanks to Barry for asking me to write here. ~~~ Full disclosure: long BRK/B & CVX

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The Universe of Pop Culture Bears Posted: 31 Jul 2014 03:00 AM PDT I woke up this morning, and true to my travel history, markets are under pressure. After I saw the futures this AM, I thought of this:

|

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment