The Big Picture |

- Paul’s Boutique’ Remixed

- Succinct Summations of Week’s Events 8.1.14

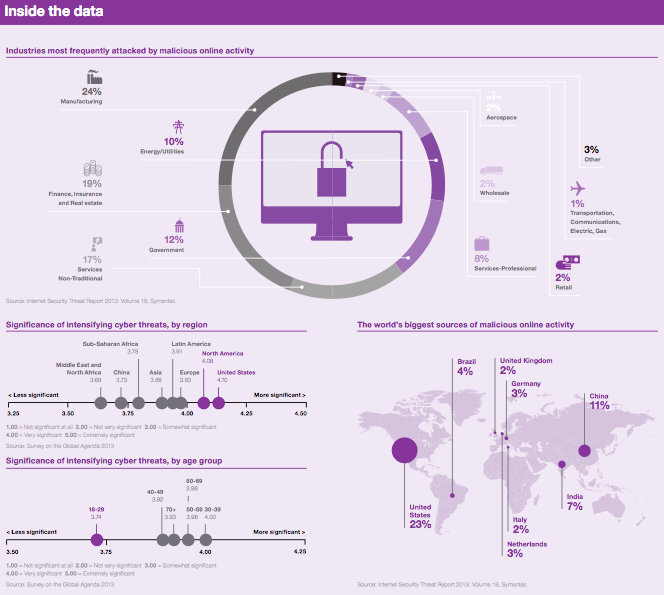

- Industries most frequently attacked by malicious online activity

- Is Work Slavery? Taleb Thinks So…

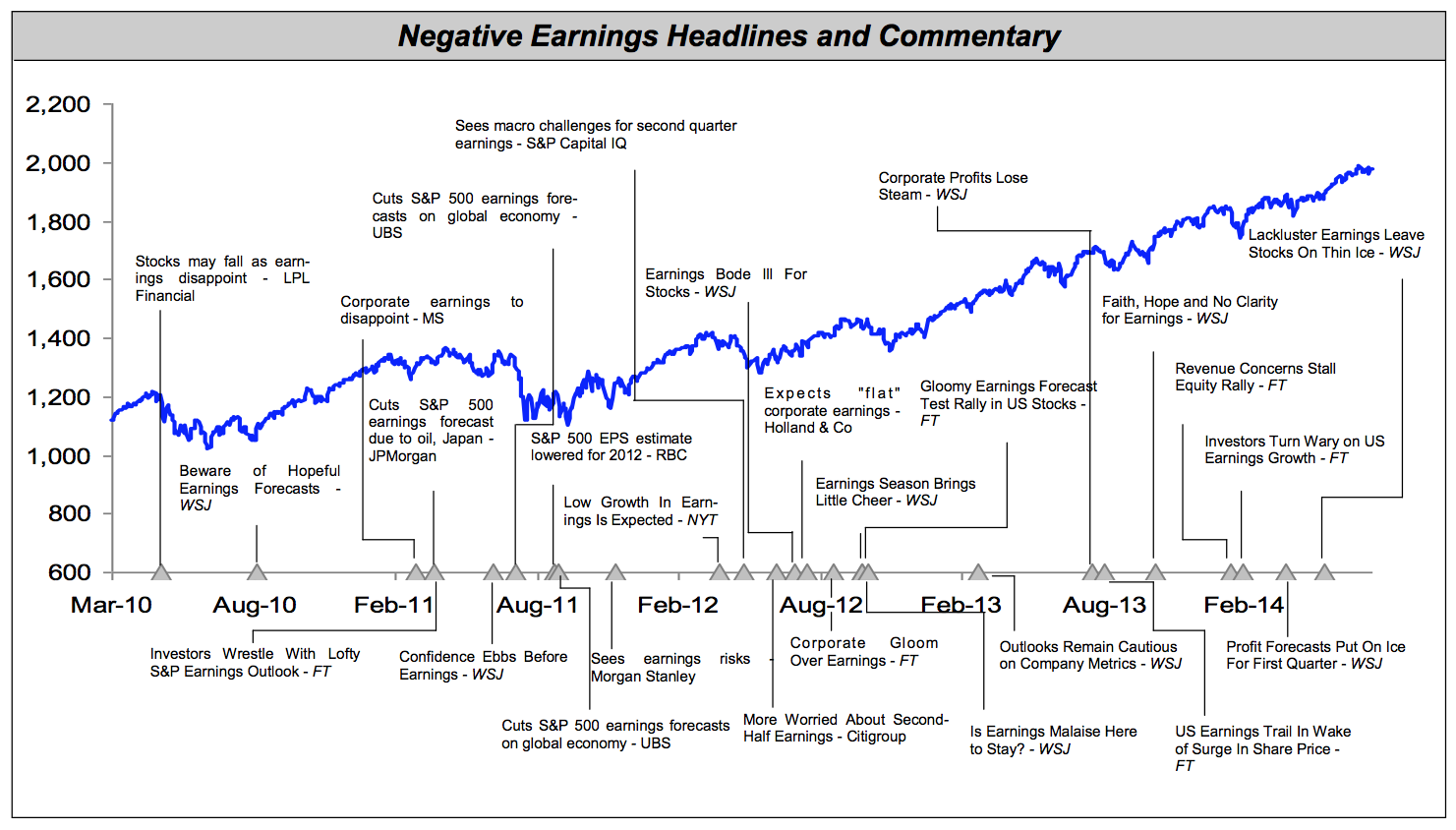

- Earnings Disappointments vs Stock prices

- 10 Friday AM Reads

- There really never has been a better time to be an individual investor

- Wall St Bullishness vs Equities Complacency

- Gentleman Jet Ski: Strand Craft V8 Wet Rod

| Posted: 01 Aug 2014 03:30 PM PDT |

| Succinct Summations of Week’s Events 8.1.14 Posted: 01 Aug 2014 02:00 PM PDT Succinct Summations week ending August 1st Positives:

Negatives:

|

| Industries most frequently attacked by malicious online activity Posted: 01 Aug 2014 11:30 AM PDT

|

| Is Work Slavery? Taleb Thinks So… Posted: 01 Aug 2014 09:45 AM PDT “By setting oneself totally free of constraints, free of thoughts, free of this debilitating activity called work, free of efforts, elements hidden in the texture of reality start staring at you; then mysteries that you never thought existed emerge in front of your eyes.” ~ Nassim Nicholas Taleb Readers of this blog are likely aware of Nassim Nicholas Taleb's first two books, his 2001 debut, Fooled by Randomness, and his 2007 work, The Black Swan, which are based upon Taleb's central idea: “our blindness with respect to randomness, particularly large deviations,” which speaks directly to the common follies of investors. I recently read (and enjoyed) his 2010 book of aphorisms, Bed of Procrustes Although Taleb covers several topics in Procrustes, the one that struck me the most was his blunt comparisons of employment to slavery, a theme that finds itself often in my own philosophical observations (and rants). Here are a few select aphorisms from the book, followed by a few of my own notes (I'd also love to hear any of your thoughts in comments that the quotes or notes may provoke):

My perspective is similar to that of Aristotle's: You're not working if you love what you do; therefore, in this case, one’s profession is not slavery. But how many are fortunate enough to love what they do? It is normal to either dislike (or, at a minimum, tolerate) one’s work. But normal is not healthy. The tension arising from “fitting ourselves” into the Procustean bed of engaging in work that we do not love is, at the root, and in my humble opinion, the reason people invest their money and it is the creator of the modern idea of retirement. We give up our freedom now for freedom later, a freedom we believe can only be purchased with money. What are your thoughts? Let me know in comments… Kent Thune is the blog author of The Financial Philosopher. You can follow Kent on Twitter @ThinkersQuill. |

| Earnings Disappointments vs Stock prices Posted: 01 Aug 2014 09:00 AM PDT

|

| Posted: 01 Aug 2014 07:00 AM PDT My pre-fishing reads (continues here):

|

| There really never has been a better time to be an individual investor Posted: 01 Aug 2014 05:45 AM PDT Tadas Viskanta in the founder and editor of Abnormal Returns which has garnered a loyal following in the investment blogosphere. He is also the author of Abnormal Returns: Winning Strategies from the Frontlines of the Investment Blogosphere. ~~~ Two and half years ago in this space I published a post arguing that there had never been a better time to be an individual investor. To me the thesis seemed obvious on its face. However many commentors were skeptical about the prospects for investors in a post-financial crisis world. Unfortunately they missed out on what turned out to be a roughly 50% total return in the S&P 500 over that time period. The post wasn’t a market call, per se. The thesis would still be valid if the stock market been flat (or down) over that time period. All that being said today: There really has never been a better time to be an individual investor.* It seems that since that post was written this idea has taken hold. At the time Jason Zweig at the WSJwrote about the travails he had trying to trade stocks back in 1970s and came to the conclusion that it was a great time to be an individual investor. Zweig wrote: (T)he informational playing field has been leveled between individual and professional investors. Individuals can trade at lower cost than institutions. Then again, you don't have to trade at all. Decades ago, a portfolio could easily have cost you 4% of your assets to assemble. Today, through index funds or ETFs, you can put a portfolio together at least 25 times more cheaply. A couple of recent posts inspired me to revisit this theme of a golden age for individual investors. The fact is that the costs of investing have only come down over the past 30 months. John Woerth at Vanguard recent wrote about “why it is a great time to invest” and noted that the access to information and the access to low-cost investments help make the case. Jonathan Clements at the WSJ in a recent article noted “three reasons why it is a good time to be an investor.” Clements who has been writing about investing for a long-time writes that since the 1980s: The financial world became a much kinder place for U.S. investors, thanks to legislation and competition that have led to a growing array of investment choices, falling investment costs and tumbling tax rates. Investors also are blessed with access to better technology and more information than they had before. While I had not focused on taxes in my earlier piece certainly the idea of greater array of investment products at a lower cost shine through. The most tangible impact is lower costs not at the fund or ETF level but also on the investment management side as well. Since 2012 the so-called robo-advisor trend has only strengthened. Herbert Moore at Medium laid out a compelling case that plain-vanilla investing, funds plus portfolio management, would be largely free in five years. The fact that “software is eating investment management” is a great one for investors and a challenging one for incumbent advisors. A big part of the reason why the investment landscape has changed has been the introduction and rise in popularity of the exchange-traded fund. Dave Nadig at ETF recently wrote that not only have ETFs changed the cost-structure of investing, they have fundamentally changed how we invest. One reason is that they have shined a light on the poor performance of active managers. More importantly, Nadig notes: The ETF puts individuals back in charge of their own fate. Don't trade much? You won't pay for transactions you aren't making. Don't incur any capital gains, or better yet, want to harvest some capital losses? You win. There's nobody at the fund company, or other investors in the fund, messing you up. One of the big areas in growth for ETFs has been the introduction of strategic or ‘smart beta ETFs‘ that attempt to outperform the market based on various factors. For the DIY active trader lower costs and a growing array of instruments to trade have opened up strategies previously available only to institutional investors. An array of services have arisen to help traders to develop and automate trading systems. While on the face of it this seems great it also represents a downside to this era of software-induced abundance. The risk is growing that investors, or more likely traders, can do damage to their portfolios in even more powerful ways. Ben Carlson at A Wealth of Common Sense notes correctly the idea that low-cost investing is a potential boon for investors. More importantly investors need to be aware that their behavior plays a large role in their ultimate investment success. He writes: Lower costs do not prevent overconfidence, short-term emotional gut reactions, over excitement, a herd mentality, loss aversion or any of the other behavioral biases which can hurt investor performance in the long run. Joshua Brown at The Reformed Broker notes that while all these cost reductions are great they don’t address the issues facing investors on a daily basis or more importantly when times get tough. Investors, including the youngest out there, need to have a plan. Brown writes: Focusing on the performance or cost of a portfolio relative to something other than a plan is like decorating a house that has no foundation. One could argue that Millennials have been hurting themselves by not having well-thought out plans AND missing this market rally. From reports it seems that the youngest cohort of investors has been reluctant to start their investing journey. They risk not only missing out on returns but the valuable experience you gain by actually going out there and putting money to work. Much has changed since my earlier post but a few things have stayed the same. There has never been a time when the individual investors has had such a powerful array of tools available at such a low cost. For those willing to farm out their portfolios things have never been simpler or in the words of Jonathan Clements “kinder.” In the meantime on all these measures things have gotten better and are likely to continue to get better. The raw materials to build a reasonable portfolio are all out there for the taking. It is up to the investor to put together a plan to pull them together so they can service your ultimate goals, whatever they may be. *THIS IS NOT A MARKET CALL! The stock market could take a meaningful tumble at any time. The point is that the today’s investor is operating in a great environment, independent of the actual level of the S&P 500. Items mentioned: There has never been a better time to be an individual investor. (Big Picture) Has there ever been a better time to be an investor? (Total Return) Why it’s a great time to invest. (Vanguard) Three reasons it is a great time to be an investor. (WSJ) Celebrating an ETF independence day. (ETF) Wall Street’s love for smart beta. (Baron’s) Software is eating investment management. (Abnormal Returns) You will be investing for free in five years. (Medium) If investing were free how would it change what you do? (Abnormal Returns) Is there a ‘robo-advisor‘ bubble? (Nerd’s Eye View) Things just keep getting better and better for investors. (A Wealth of Common Sense) A portfolio is not a plan. (The Reformed Broker) Young adults choose to save cash instead of investing. (Marketplace) |

| Wall St Bullishness vs Equities Complacency Posted: 01 Aug 2014 04:15 AM PDT Funny to wake up after yesterday’s selloff to see two such diametrically opposed views from major investment houses:

|

| Gentleman Jet Ski: Strand Craft V8 Wet Rod Posted: 01 Aug 2014 03:00 AM PDT Since I am away this week at a conference in Maine, combining fishing with economics and investing, I thought this week we would go for something water rather than land based. Hence, I present the Strand Craft V8 Wet Rod:

Source: Classic Driver |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment