The Big Picture |

- The Low Frequency Effects of Macroeconomic News on Government Bond Yields

- RIP Robin Williams – Weapons of Self Destruction

- 10 Monday PM Reads

- Current Reservoir Conditions in California

- 10 Monday AM Reads

- How Greenspan Became the ex-Maestro

- SKEW-VIX & The Fog of War

| The Low Frequency Effects of Macroeconomic News on Government Bond Yields Posted: 12 Aug 2014 02:00 AM PDT |

| RIP Robin Williams – Weapons of Self Destruction Posted: 11 Aug 2014 05:30 PM PDT Weapons of Self Destruction was the name of his last HBO special. So brilliant, funny . . . and sad.

Robin Williams stand up comedy live from Washington

HBO: Robin Williams – comedian, writer and Academy Award-winning actor – returned to HBO for his first solo TV concert since 2002. The show was filmed at Washington D.C.’s DAR Constitution Hall on his sold-out “Weapons Of Self Destruction” national tour. Robin covers such topics as global warning, health care in America (suggesting a “cash for clunkers” for elderly relatives), and more personal topics such as his recent open heart surgery. Bonus features include clips from Robin’s previous concerts – some dating back to 1978 – as well as tour highlights filmed all along the 2009 tour. |

| Posted: 11 Aug 2014 01:30 PM PDT My afternoon train reads:

What are you reading?

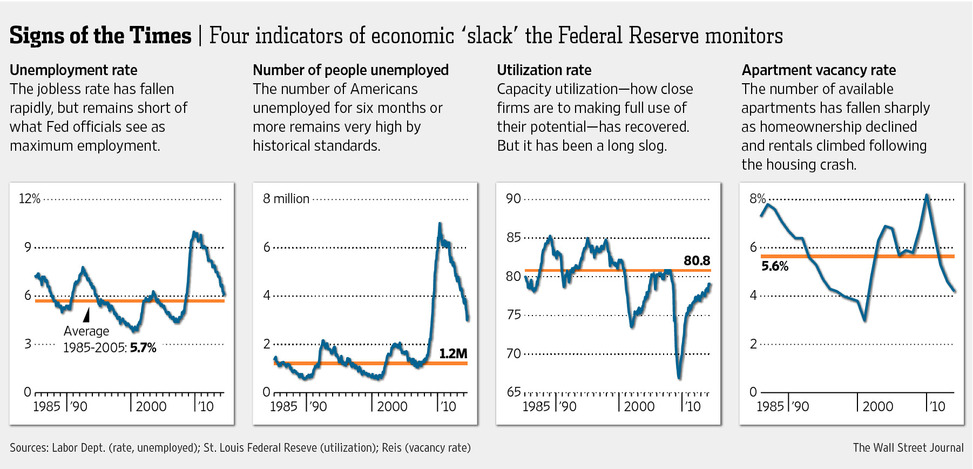

Decline in ‘Slack’ Helps Fed Gauge Recovery Source: WSJ

|

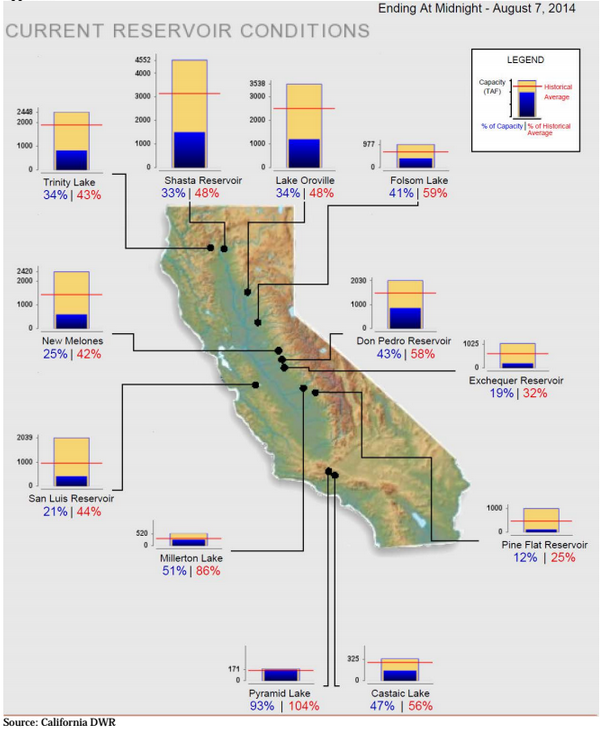

| Current Reservoir Conditions in California Posted: 11 Aug 2014 09:30 AM PDT

|

| Posted: 11 Aug 2014 07:30 AM PDT My morning afternoon train reads (continues here):

|

| How Greenspan Became the ex-Maestro Posted: 11 Aug 2014 05:54 AM PDT On this day in 1987, Alan Greenspan became chairman of the Federal Reserve Board. This anniversary allows us to take a quick look at what followed over the next two decades. As it turned out, it was one of the most interesting and, to be blunt, weirdest tenures ever for a Fed chairman. This was largely because of the strange ways Greenspan’s infatuation with the philosophy of Ayn Rand manifested themselves. He was a free marketer who loved to intervene in the markets, a chief bank regulator who seemingly failed to understand even the most basic premise of bank regulations. The stock market was having a scorching year in 1987, up 44 percent during the first seven months of the year. Stocks peaked within weeks of Greenspan being sworn in. He was still settling into the job when Black Monday came along and U.S. markets plummeted 23 percent on Oct. 19. Welcome to Wall Street, Mr. Chairman. Continues here

|

| Posted: 11 Aug 2014 03:00 AM PDT SKEW-VIX & The Fog of War

This commentary will include answers to some questions from readers about the SKEW-VIX ratio and why it is important. Here are two issue notes before we address those questions. First, our alarm about the ratcheting up of military action falls into the category of "the fog of war." Think about it in the following way. It is not about Cumberland Advisors' view of policy. Moreover, we are not commenting on what the US's, European Union's, or some other place's policies should be. The word should is not part of the dialogue. We are talking about market reactions. When you ratchet up sanctions and negative economic exchanges in a revised version of a "Cold War" between the West and Russia, market reactions ensue. Markets react when they develop a sense of the costs involved in a sanctions war. The US, European Union, and Russian Federation are engaged in a sanctions war that continues to intensify. There are and will be negative and unintended consequences. Secondly, when military activity involves rockets, bombings, movement of troops, and the merciless and murderous behavior of organizations like ISIS (recently rebranded as IS), we then have a hot war. To call it anything else is to be delusional. And in a state of war there is never full clarity. As Carl von Clausewitz declared nearly two centuries ago, there is fog. (Vom Kriege, 1837, published posthumously). When the US engages in a limited bombing campaign and attempts to assist one party in a conflict, the purpose of its policy may be to effect humanitarian relief, to rescue Americans, or to prevent genocide. The rationale or policy decision in each case is not the subject of our commentary. Our comments are about market reactions being bearish on the news of US engagement. We are fully in favor of saving innocent people and intervening where it makes sense to do so. And we also recall the final extraction from Vietnam and the image of a helicopter lifting the last people from a US facility as the enemy came through the gates. When we examine such developments as they occur in the "fog of war," we are watching in real time and may not be absolutely precise or accurate in our analysis. Drones and satellite images help, but our TV images must not be seen as a video game. Far from being exact, precise, and perfectly informed, military action that confronts terrorism on the ground is a fraught and uncertain undertaking. Interpreting what's really going on is doubly hard. Media coverage adds to the confusion when you back away from your biases and examine it with a worldwide view. A case in point is the debate about the Malaysian civilian plane that was shot down with an alleged Soviet-manufactured missile. The Western press jumped on the issue, placing the blame on the Russian leadership and Vladimir Putin in particular. However, the plane was shot down in a contested region, so it is not yet clear who launched the missile. Most of us in the West believe it was Russian-backed separatists who launched the missile. But what if you were in Malaysia and saw this article in today's New Straits Times? Would you conclude differently? Would you have doubts? What would you say if and when you saw this story on Moscow TV? In the fog of war there are folks who believe that the missile was actually launched from a Ukrainian source that may have thought the Malaysian aircraft had Soviet markings. Those reports did not get prominent coverage in American or other Western media. We were not there. We do not know who shot down the plane. Our view is formed from the media we see and is influenced by our own prejudices. We do know that the fog of war swirls with many graphic images, yet there is no clarity. There may be partial views. And there may be periods when the realities are obscured. Let's step back from the "fog of war" and think this through. Suppose it was the Russian-backed separatists who shot down the plane. That is the common assumption in the Western media. If we look at the Ukraine-Russia events through the lens of mainstream Western television, our view leans in favor of Kiev, and we react negatively to Moscow. Suppose you are in Moscow and you see the Malaysian story on Russian TV. That story may say Russian-backed separatists did not shoot the plane down. How then would you react if you arrived at the conclusion that your side was innocent and that Western media and governments were distorting events and blaming your country? Let's be clear. We are not defending Putin. We are not defending anyone who shot down the Malaysian plane. We are not supporting ISIS (Islamic State of Iraq and Syria) or ISIL (Islamic State of Iraq and the Levant). The key here is that when we find ourselves in the "fog of war" we do not have clarity, which means each event adds risk premia, puts pressure on markets, and introduces distortions. Before we take up the issue of volatility, let's add one more item. We know the news about US bombing and that it will last for months, not weeks. Let's consider the Mosul Dam. Will ISIS blow it up and kill 500,000 people if they start to lose the fight? Their behavior suggests that they view human life as insignificant, so the conclusion may well be yes. Would they blow up the dam if they are winning? They want to govern. They need electric power to do so. Thus the United States is in a catch-22. It doesn't want to cause a Tigris river flood and the deaths of half a million people downstream. But it does want to restrain ISIS' advances, avoid genocide, and help the Kurds. Bottom line? There is no way to predict the outcome. We can only watch and absorb news flow. Translate this to markets. The uncertainty premium goes up. Now back to the SKEW vs. VIX. Why? Because the ratio between them is an indicator of the uncertainty premium. It is only an indicator, but it may be one that can be used to estimate the impact of the fog of war. The ratio between the SKEW and VIX is a ratio of two different indices that measure option premiums. Those premiums give indications of market-based pricing of risk. When the SKEW-VIX ratio widens, it says that out-of-the-money options on American stocks are being bid up for the purposes of insuring against tail-risk events. Tail-risk events are higher-volatility swings, that is, swings that could be greater than one or maybe two standard deviations. History suggests that wide ratios between the SKEW and VIX result in market reactions that can be serious. That is why we watch the SKEW-VIX ratio. We give a hat tip to the analysts at BCA Research, who have discussed this in great detail in their work. We have taken the SKEW-VIX ratio, plotted it against the S&P 500 Index, and put it on our website for readers to see. The data starts in 2008. The ratio and the performance of the US stock market for the entire period of the financial crisis and subsequent rally can be seen. Look at it and draw your own conclusions. Here is the link: http://www.cumber.com/content/misc/SKEW-VIX.pdf . As this commentary is written, we still maintain a cash reserve and a defensive structure in portfolios. We think there is a still-evolving "fog of war." We think that risks are rising for accidents, military interventions, and damage to economic recoveries. The world appears to be a very dangerous place. At the same time, we think that the central banks of the world are out of bullets when it comes to additional assistance in case there are shocks. The zero interest rate policy (ZIRP) around the globe has suppressed volatility for a long time. SKEW-VIX suggests that volatility may be returning. ~~~ David R. Kotok, Chairman and Chief Investment Officer |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment