The Big Picture |

- 100 Most Iconic Shots In Movie History

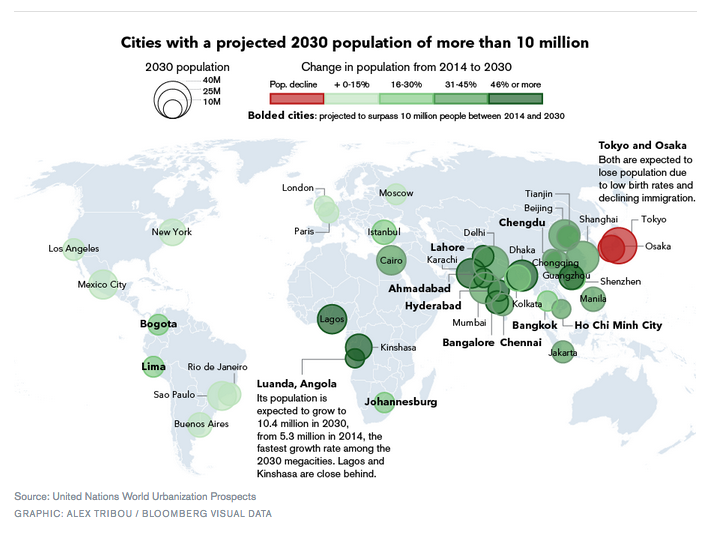

- Global Megacities

- MiB: Laszlo Birinyi

- 10 Weekend Reads

- Kiron Sarkar’s Weekly Report 9.13.14

| 100 Most Iconic Shots In Movie History Posted: 13 Sep 2014 05:00 PM PDT What if we asked you to pause your favorite movie at your absolute favorite moment, could you pick the best shot ever? Neither could we, so here are 100 of 'em. Sit back, relax and enjoy this stroll down awesome-movie-moments lane with the most iconic shots of all time. How many movies can you recognize from just the one shot? Test your knowledge in the comments below then watch for the answers here:

|

| Posted: 13 Sep 2014 11:00 AM PDT |

| Posted: 13 Sep 2014 06:45 AM PDT This week's Masters in Business Radio show at 10:00 am and 6:00 pm on Bloomberg Radio 1130AM and Siriux XM 119 (it also repeats all weekend). Our guest this week is David Rosenberg, formerly Merrill Lynch's North American Chief Economist, now strategist and economist at Gluskin Sheff & Assoc. in Toronto. You can listen to live here or stream it at Soundcloud or download the 82 minute podcast here. (might not be up yet) All of the past Podcasts are here (and coming soon to Apple iTunes). Next week, we speak with market analyst and historian Jeff Saut. |

| Posted: 13 Sep 2014 04:00 AM PDT Good Saturday morning. Following a busy and emotional week, we have some interesting food for your brain — our long form weekend reads.

Did you see the Aurora Borealis?

Oil Glut Ignites Gasoline Price Swoon

|

| Kiron Sarkar’s Weekly Report 9.13.14 Posted: 13 Sep 2014 03:00 AM PDT At the meeting on the 17th September, the key issue There has been much talk about the Scots voting The EU confirmed that additional sanctions will be imposed on Russia, a position Germany has been pressing. The impact will be particularly severe on Russia (a recession, indeed stagflation is likely), though the EU will also be affected. The Ruble declined to a record low against the US$, though the Central Bank kept interest rates unchanged. Russia has threatened to retaliate, including possibly banning flights over its territory. However, Russia/Mr Putin will not be swayed by the additional sanctions – they see it as a political issue, irrespective of the economic effects and one which they will not back off. GDP, already anemic in the EU (in particular the EZ) will decline, with the Euro weakening even further. Major countries such as Germany will be impacted, in particular. There appears to be momentum behind the sales of Japanese government bonds (JGB's) by Japanese institutions, with the proceeds being reinvested in foreign bonds and equities, a process which I expect will continue, indeed accelerate. The sell off, if it continues, (which looks likely) is yet another reason I believe that the BoJ will be forced to increase the size of its monetary accommodation programme. The impact will be particularly negative on the Yen, subject to geopolitical issues. The US$ strengthened materially against the major currencies during the week, though I believe that it has further to go. As is the case in the UK, US interest rates are set to increase, whereas rates in every other major country will remain low for a considerable period of time. Geopolitical risks (Ukraine, ISIS etc) have increased and are impacting equity markets. With the FED, I believe, set to signal that rates will start to rise (in late Q1/early Q2 in my opinion) this month or next, markets are likely to pause for a while. The ECB could well provide a positive catalyst next month as it announces details of its ABS/covered bond purchase programme. Furthermore, European corporate earnings are being upgraded. Remember Greece, well it was upgraded to B from B- by S&P, with a stable outlook. However, at present, it looks as if markets have turned cautious. Recent fund flow data indicates that investors have been selling US high yield and US equities, whilst increasing their cash positions and equity investments in the EU, with some money going into emerging markets. US US retail sales rose by +0.6% in August M/M (+5.0% Y/Y), the fastest rate in 4 months and in line with forecasts. July's data was revised higher to +0.3%, from an unchanged level previously. Auto's and building materials contributed the most, with petrol lower, reflecting the decline in prices. Retail sales, ex autos, petrol and building materials (which feeds into the calculation of GDP) rose by +0.4%, in line with forecasts and the same as that for July, which was revised higher from the initial estimate. The data supports the view that consumer spending is much better than previously thought. Furthermore, recent data suggests that income growth may just be starting to pick up, which should help consumption. Finally, US consumer sentiment rose to the highest level in 14 months, coming in at 84.6, above the forecast of 83.3 and Augusts 82.5, which further argues for increased spending. Import prices declined by a significant -0.9% in August, reducing the Y/Y rate to -0.4%, from +0.8% in July. The stronger US$, combined with, primarily, lower energy costs contributed to the decline. In addition, lower commodity prices generally and slower growth internationally resulted in the sharp fall in August. The decline suggests that inflation should not be a problem for the US at present. The US August NFIB small business confidence index increased to 96.1 M/M, slightly higher than the forecast of 96.0 and above July's reading of 95.7. It was the 2nd highest reading since October 2007. The capex and the future economic outlook components contributed the most to the higher reading, which certainly is positive, though hiring plans dipped. The FED intends to impose a capital surcharge on the large banks such as JP Morgan, Wells Fargo, Citi and BoA and those which rely heavily on short term funding, such as the Goldmans and Morgan Stanley. The amount of the capital surcharge has not yet been decided. However, analysts believe that the surcharge will amount to 2.0% above the highest range of +2.5% agreed by international regulators. US jobless claims rose by 11k to 315k, above the forecast of 300k and the highest for 2 months. The data is somewhat erratic during the holiday period, though admittedly, recent employment data has been weaker than expected. Europe EZ investor confidence declined to -9.8 in September, much worse that the rise to +1.4 expected and August's +2.7. German exports increased by +4.7% (+0.6% expected) to over E100bn for the 1st time in July, with the trade surplus rising to E23.4bn, an all-time high. Imports on the other hand declined by -1.8% (+0.2% expected), most likely due to lower oil prices. However, the Bundesbank has warned that the German economy was likely to weaken in H2 as a result of the crisis in the Ukraine. Germany and France will jointly submit proposals for a E300bn investment plan for the EU, which will involve financing by the European Investment bank. German wholesale prices declined by -0.6% Y/Y, the largest fall since November 2009. Italy is also suffering from deflation, with August's final CPI at -0.1%, in line with expectations. The French finance minister admitted that the budget deficit will widen to 4.4% of GDP this year, up from 4.3% last year. In addition, he cut the 2014 and 2015 GDP forecasts to +0.4% and +1.0%, down from the previous estimate of +1.0% and +1.7% respectively. Furthermore, he forecast that the budget deficit would decline to the 3.0% target only in 2017. However, I believe that the downside risks to the revised forecasts remain. Italy's woes continue. Italian July industrial production declined by -1.0% M/M, well below the decline of -0.2% expected and the downwardly revised +0.8% in June. Whilst a poll last weekend reported that the % of people in favour of Scottish independence (from the UK) rose above 50%, the 1st time that polls indicated that more Scots would vote for independence, subsequent polls suggest otherwise. I continue to believe that the majority of Scots will vote in favour of remaining within the UK, though it certainly looks as if it is going to be a closer call than expected previously. The referendum will take place on the 18th September. Sterling clearly declined sharply following the release of last weekends poll results, though has recovered subsequently. UK industrial production rose by +0.5% M/M in July (+1.7% Y/Y, as opposed to a forecast for a rise of +1.3%), higher than the forecast for an increase of +0.2% and the rise of +0.3% in June. The governor of the BoE suggested that a rate rise in the UK by spring next year (in line with market expectations) would be consistent with the Central Banks goals of meeting its inflation target, as the improvement of the economy had "exceeded all expectations" and "has momentum" . Wages remained weak due the slack in the market, with the BoE forecasting that wage growth will start to rise in coming Q's. Unit labour costs were below the level which was needed to meet the BoE's CPI target, with inflation remaining benign. Finally, he reiterated that rate increases would be gradual and limited. Japan Japanese core machinery orders (a key indicator of future capex) rose by +3.5% in July (+1.1% Y/Y), below the rise of +4.0% expected and the +8.8% gain in June. Japanese PPI unexpectedly declined to -0.2% in August M/M (3.9% Y/Y, lower than the +4.1% expected and July's +4.3%), below the flat reading expected and the +0.4% increase in July. The lower reading suggests that the BoJ will have to increase the size of its monetary accommodation policy if it is to meet its inflation targets. Japanese regulators approved a safety report for 2 nuclear reactors, though 2 further approvals will be required before they can be restarted, which analysts expect will be in Q1 2015. However, there remains significant domestic opposition, given the Fukushima disaster. In August, Japanese institutions increased their sales of JGB's and bought nearly US$12bn of foreign bonds (mainly US and French) and equities. No great surprise, given the declining currency and negative real returns on JGB's. Furthermore, the Japanese pension fund (GIPF), the world's largest, is set to reduce its holdings of JGB's and invest more into Japanese equities, together with foreign bonds and equities. An announcement is expected this month. The Yen looks likely to weaken further, in my view much further, subject to geopolitical issues. I would also expect the Central Bank, the BoJ, to increase its purchases of JGBs, in particular as it is likely to have to increase monetary accommodation. However, I remain deeply sceptical of Abenomics and the BoJ's policy. China Chinese August CPI rose by +2.0% Y/Y, a 4 month Aggregate lending in August amounted to Yuan 957.4bn Other Brent fell below US$100 for the 1st time since April The A$ declined sharply during the week. The decline South Africa's current a/c deficit rose to 6.2% Brazilian July retail sales, seasonally adjusted, Kiron Sarkar |

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment