The Big Picture |

- Making Sense of Dissents: A History of FOMC Dissents

- Made in New York featuring Derek Jeter

- 10 Thursday PM Reads

- State-Level Changes in Real GDP, 2005-2013

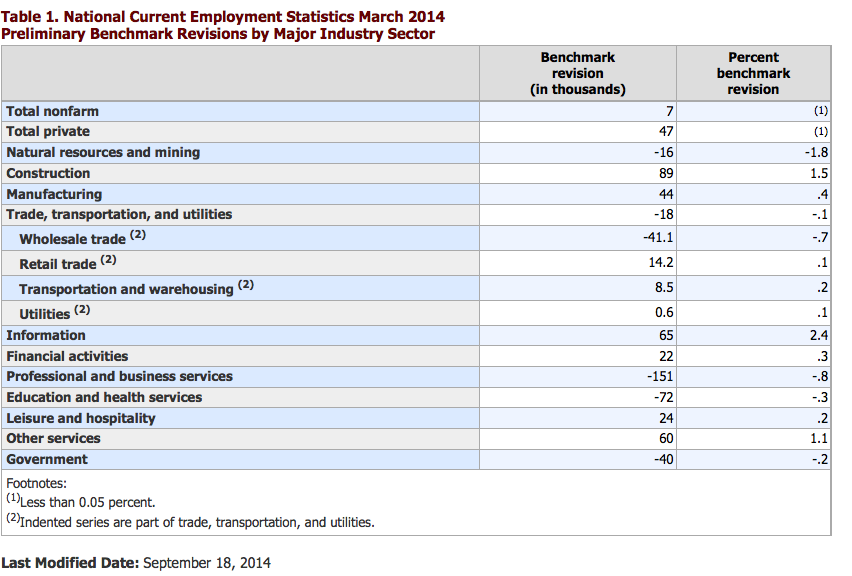

- BLS Preliminary Benchmark Revision to NFP

- State Street CIO Conference

- 10 Thursday AM Reads

- The Fed and the Media

- Supersized IRAs Under U.S. Scrutiny

| Making Sense of Dissents: A History of FOMC Dissents Posted: 19 Sep 2014 02:00 AM PDT |

| Made in New York featuring Derek Jeter Posted: 18 Sep 2014 07:30 PM PDT Ahead of his final playing days, Derek Jeter soaks in the atmosphere on a walk in the Bronx. via Gatorade |

| Posted: 18 Sep 2014 02:30 PM PDT My afternoon train reads:

What are you reading?

Russell 2000 Resistance and Support

|

| State-Level Changes in Real GDP, 2005-2013 Posted: 18 Sep 2014 09:30 AM PDT The U.S. Bureau of Economic Analysis (BEA) recently released a trove of data on the individual state economies. You can zoom in on quarterly state-level gross domestic product (GDP) series begins from 2005 through the 2013 at Macroblog of the FRBA. But I thought it might be instructive to see what the map looks like if we can animate each quarter:

How states have fared since 2005 relative to the economic performance of the nation as a whole.

|

| BLS Preliminary Benchmark Revision to NFP Posted: 18 Sep 2014 08:30 AM PDT This year’s benchmark: Surprisingly small From labor wonks at the Liscio Report:

|

| Posted: 18 Sep 2014 06:15 AM PDT Interesting day as I am scheduled to open the State Street CIO summit by interviewing Arthur Levitt, former chairman of the SEC, right about . . . NOW. I will post an update if I can |

| Posted: 18 Sep 2014 05:30 AM PDT Its the day after the FOMC meeting, and apparently, a new era is upon us:

|

| Posted: 18 Sep 2014 04:00 AM PDT The Fed and the Media

We know the Fed meeting results; the coverage has been exhaustive. Note that the new "dots" analysis of the median dot now points to an expected 1.375% Fed Funds target rate by the end of 2015. (See Craig Torres' report on the FOMC.) That is higher than the June median, which was higher than March. Some analysts concluded that the first rate hike may come sooner than midyear. Maybe it will and maybe it won't. We note that six of the FOMC members have the rate below 1% at year end 2015. And also note that only 12 members of the FOMC vote. We do not know who the six "doves" are unless they voluntarily reveal themselves since the identity of "each dot" is not revealed. Thus drawing inferences of the path of future Fed Funds rate from the dots is a problematic and risky affair. Let's get to markets. The day of the meeting was really uneventful. The fireworks preceded the meeting. A flurry of market activity occurred after Jon Hilsenrath of the Wall Street Journal articulated his views in a webcast and on his blog. Jon's journalistic beat includes following the Federal Reserve (Fed) in its activities. Other notable journalists who follow the Fed include Greg Ip with The Economist, Michael McKee with Bloomberg, and Steve Liesman with CNBC. I am not intentionally forgetting the others. There are many. Some journalists report results. Many of them, including Jon Hilsenrath, are regulars at press conferences after Fed quarterly meetings. A good example was yesterday's September 17, 2014, press conference that followed the two-day Federal Open Market Committee (FOMC) meeting. Some journalists create surveys asking financial analysts, economists, money managers, and other professionals to offer their views as to what Fed policy will be and what it should be. My colleagues and I participate in some of those surveys. There is a controversial issue regarding media coverage prior to the release of Fed minutes and policy statements. Prior to this last meeting and after the Hilsenrath column, there was an attribution in a widely followed morning newsletter that characterized Hilsenrath as a "Delphic Oracle." (For elder readers: is he the successor oracle to John Barry, or is he the designated leakee?) We find such characterizations troubling for several reasons. If someone inside the Fed is whispering policy into a favored journalist's ear, based upon FOMC materials or discussions in advance of policy decisions, a possible violation of law and FOMC rules may rise to the level of criminality. However, if nothing is being whispered, the characterization that Hilsenrath has been a "receiver of information from highly placed and well-informed sources within the Fed" was inaccurate and the language used was very strong. If Hilsenrath was simply expressing his personal view, then he has every right to do so; but the appearance that he may have access that violates rules (and influences markets) is dangerous. Either way, the discussion is distorting policy, increasing volatility, and therefore raising risk premia. Those are the exact outcomes that the Fed does not seek. If the Fed is as closed with regard to its public pronouncements and policy directives as we believe is the case, then the Fed is complying with the letter of the law and with sound principles of policymaking. Policymakers fare best when they do not favor anyone in the media. They make policy. Media commentators can guess all they want, but as a practical matter, they do not have any "inside information." My colleague Bob Eisenbeis was formerly the director of research at the Federal Reserve Bank of Atlanta. He participated in many Fed activities, including FOMC meetings. He has a long and distinguished history with the Fed. He never violated the principle that inside information should not be intentionally leaked to journalists. I asked Bob if he saw any leaks during his tenure at the Fed. His answer was "yes." Bob recalls that there were two leaks and that Chairman Greenspan sought an investigation of each leak, once by the FBI and another by the Inspector General. The outcome of these investigations was not revealed to the FOMC when Bob was present. My personal activity includes chairing the central banking series at the Global Interdependence Center (GIC). In the course of a dozen years, I can say that not once was any Fed official asked by anyone at the GIC to break the rules and disclose something that they could not legally discuss. In my experience, no one ever breached the rules. The same is true for central bankers I have met and worked with all over the world. Another Cumberland colleague, Bill Witherell, spent years at the Organization for Economic Co-operation and Development (OECD) in Paris, France. He headed the directorate that deals with governance. He joined many conversations and meetings on global economics, finance, and policy issues. Bill has affirmed how scrupulously cautious and careful the participants were when it came to media contacts and journalists. Those conversations that took place among policymakers as they wrestled with issues were kept in confidence. Now, it is possible that someone at the Fed is talking to a journalist off the record. There is no way for anyone to know. But it is potentially against the law and entails a risk to that person that there could be an FBI investigation and possible criminal penalties. Note that Hilsenrath never says he was "told" something that he should not have heard. His column offers his opinion. Therefore, the issue lies with market interpretations of people's opinions. Market agents and newsletter writers are fully entitled to interpret anything they want in any way they see fit. Market agents are making real-money bets. If they want to do so based on an opinion articulated by a journalist, that is up to them. But the allegation that the journalist had received information from a source high inside the Fed is very strong language. We believe that the Fed cannot do anything about this. It can only follow the rules it sets for its own communication policy. The Fed has introduced several changes in recent years, including press conferences, as a way to clarify that policy. Nothing in those rules permits the Fed or encourages Fed insiders to leak policy to anyone. The Greenspan model of investigation allows Chair Yellen a precedent if she believes there is a leak from inside the Fed. We, on the outside, will probably never know the outcome unless there is a prosecution. When it comes to elevating a journalist to "Delphic Oracle" status, we're opposed. The same is true for economists and analysts. We may have opinions on policy and how it is made but we do not legally "know" in advance. In this morning's newsletter, the author reversed his strong language but did so with only modest apology. He opined that he is "certain" Hilsenrath's views were not "vetted" inside the Fed. So his very strong language of yesterday has been reversed. We will leave it to him to determine if the original allegation was warranted with the language he selected. We will leave it to readers to compare Hilsenrath's pre-meeting opinion with the outcome. ~~~

|

| Supersized IRAs Under U.S. Scrutiny Posted: 18 Sep 2014 03:30 AM PDT About 9,000 U.S. taxpayers have each accumulated at least $5 million in individual retirement accounts, said the Government Accountability Office, raising questions about some investors' tax-advantaged returns. Zimmerman Edelson Partner Robert Zimmerman and Bloomberg's Peter Cook also discuss tax inversions on "Street Smart."

|

| You are subscribed to email updates from The Big Picture To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

0 comments:

Post a Comment